Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 39.01 Billion |

| Market Size (2026) | USD 40.65 Billion |

| Market Size (2031) | USD 49.94 Billion |

| Growth Rate (2026 - 2031) | 4.21% CAGR |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Spain Office Real Estate Market Analysis by Mordor Intelligence

The Spain office real estate market size is expected to grow from USD 39.01 billion in 2025 to USD 40.65 billion in 2026 and is forecast to reach USD 49.94 billion by 2031 at 4.21% CAGR over 2026-2031. Political stability, competitive operating costs, and the positioning of Madrid and Barcelona as prime European hubs for technology and financial services support growth. Grade A buildings attract the bulk of leasing demand because their modern specifications match hybrid-work requirements and rising ESG standards. Flexible leases remain the preferred route for occupiers, with rental transactions accounting for the lion’s share of activity. Foreign direct investment momentum is intact as evidenced by the jump in financial-services projects and by institutional appetite for certified green assets that offer dependable cash flows.[1]Blanca García-Moral and M.ª Isabel Laporta-Corbera, "Developments in Spanish Public Debt in 2023," Banco de España, bde.es

Key Report Takeaways

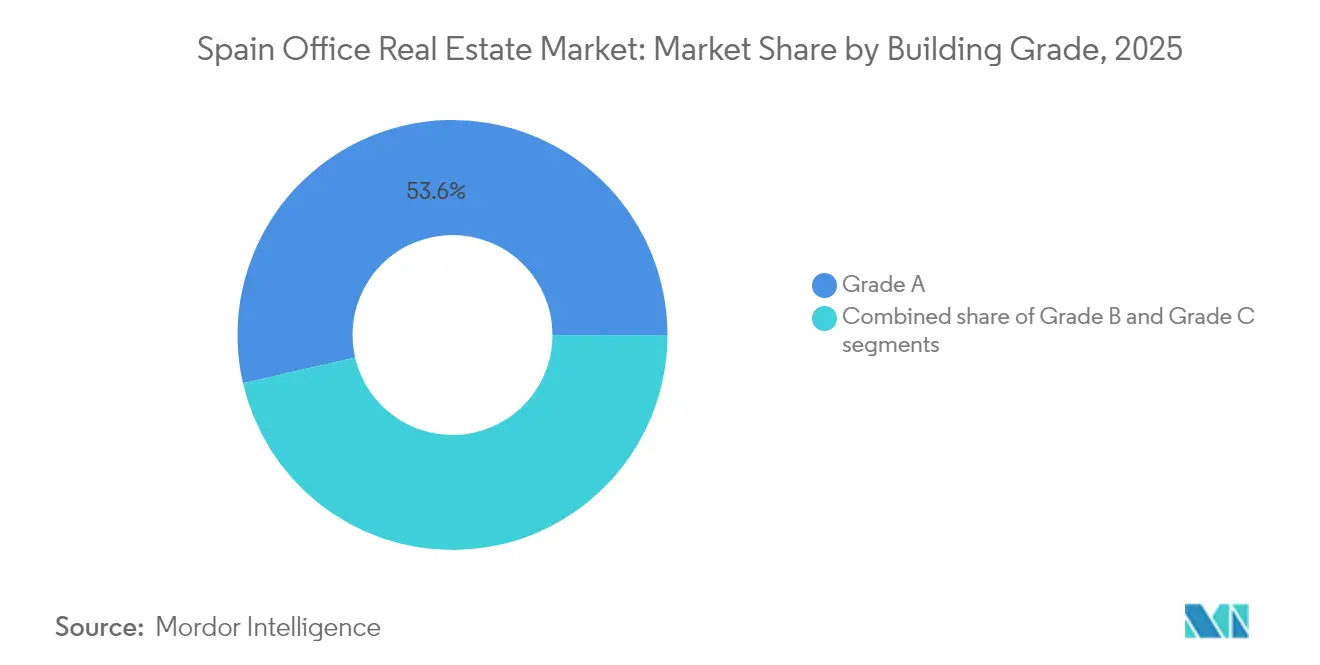

- By building grade, Grade A assets held 53.60% of the Spain office real estate market share in 2025, while Grade B stock is projected to post the fastest 4.58% CAGR to 2031.

- By transaction type, the rental segment dominated with 78.30% of revenue in 2025; sales transactions are expected to grow at a 4.73% CAGR through 2031.

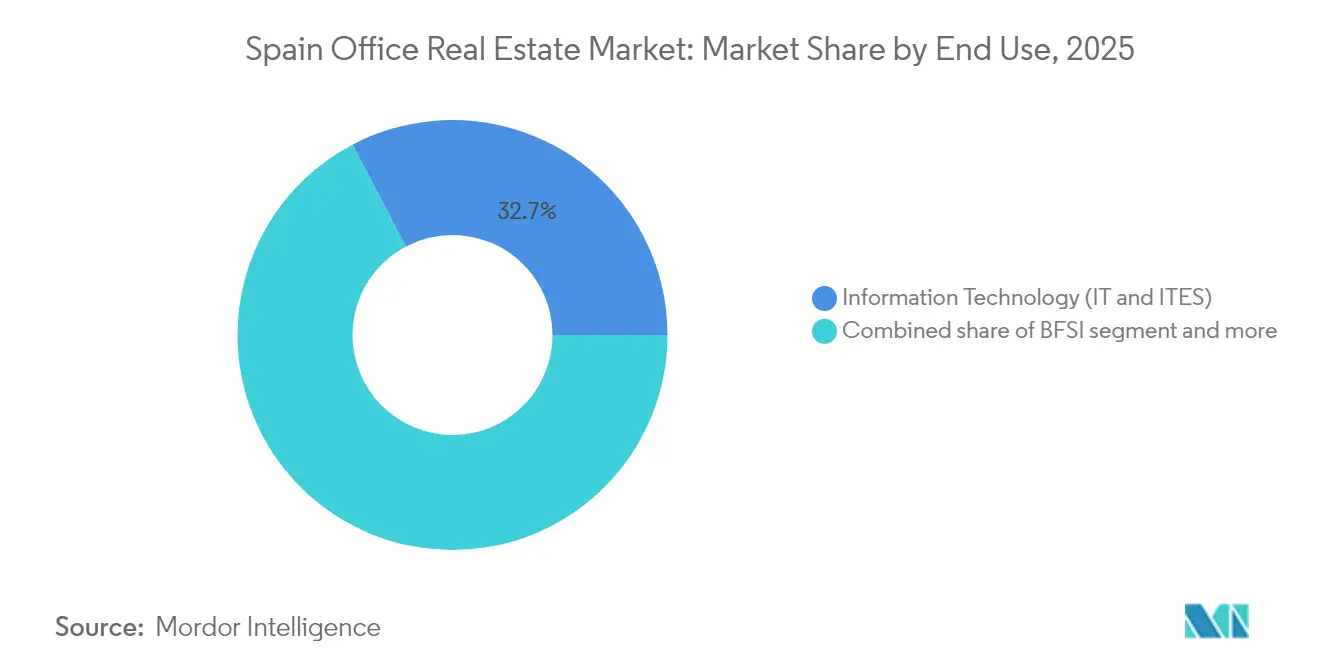

- By end use, information technology and IT-enabled services captured 32.70% of demand in 2025, and this segment is set to expand at a 4.92% CAGR to 2031.

- By city, Madrid commanded 41.40% of total activity in 2025, whereas Valencia is forecast to witness the highest 5.12% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Spain Office Real Estate Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of tech and startup ecosystems | +1.2% | Madrid, Barcelona, spillover to Valencia | Medium term (2-4 years) |

| Nearshoring of IT and shared service centers | +0.8% | Madrid, Barcelona, Valencia | Long term (≥ 4 years) |

| Surge in demand for flexible workspaces | +0.9% | National, major urban centers | Short term (≤ 2 years) |

| Institutional investor focus on ESG-compliant assets | +0.7% | Madrid, Barcelona prime zones | Medium term (2-4 years) |

| Government incentives for energy-efficient retrofits | +0.6% | National, emphasis on large cities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Expansion of Tech and Startup Ecosystems in Madrid and Barcelona

Spain’s technology economy generated more than USD 129.6 billion in 2024 and employed 764,000 people, cementing Madrid and Barcelona as magnets for high-growth digital firms. Venture capital inflows surpassed USD 3.24 billion in 2024, encouraged by the 2022 Startup Law’s tax incentives and a network of 300-plus incubators. Barcelona’s 22 district alone accounted for 32% of annual leasing, proof that tech clustering drives rental premiums. Demand skews toward Grade A space larger than 1,000 m², enabling firms to embed sophisticated IT infrastructure. As startups mature into scale-ups, their need for long leases in top-spec buildings intensifies, ensuring steady absorption of the Spain office real estate market.

Nearshoring of IT and Shared Service Centers from Northern and Western Europe

Latin American corporates invested USD 72.2 billion in Spain between 2020 and 2024, launching 360 greenfield projects that often anchor back-office and software operations in Madrid or Barcelona. Although detailed Northern European nearshoring metrics are scarce, cost-competitive Spanish hubs serve as strategic gateways into both the EU and Latin America. Eight Advisory’s 2025 establishment of a Madrid base illustrates the draw of Spain’s 93% high-capacity network coverage and favorable labor costs. These factors underpin a long-duration uplift in the Spain office real estate market as corporates consolidate service-center footprints.

Surge in Demand for Flexible Workspaces and Hybrid Office Models

Hybrid work policies now cover 55% of Spanish employees, re-shaping space planning to favor collaboration-rich environments. CBRE acquired full ownership of Industrious, which reflects the growing institutional recognition of flexible workspace demand, while companies increasingly prioritize collaboration-focused designs over traditional density models. Valencia mirrors this pivot: requests for units above 1,000 m² rose sharply in 2024, led by technology occupiers seeking plug-and-play layouts. Although hybrid models marginally trim aggregate footprints, they boost demand for premium, experience-oriented buildings, lifting effective rents within the Spain office real estate market.

Institutional Investor Interest in Prime, ESG-Compliant Office Assets

European real estate investment is projected to grow 23% year on year to USD 231.1 billion in 2025, with value-add investors targeting non-prime stock for green upgrades. Spain’s buildings account for 30% of national energy use, and more than 80% hold low efficiency ratings, presenting ample retrofit opportunities. Colonial’s 99% green-certified USD 12.58 billion portfolio illustrates how sustainability drives high occupancy of 95% and steady rent growth. Heightened ESG regulation under the EU’s CSRD accelerates the bifurcation between future-ready assets and obsolete stock within the Spain office real estate market.[2]European Commission, “Corporate Sustainability Reporting Directive (CSRD): Official Journal L 322/15,” European Union, eur-lex.europa.eu

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent oversupply in non-core zones | -1.1% | Madrid, Barcelona secondary areas | Medium term (2-4 years) |

| High retrofit costs for outdated buildings | -0.8% | National, older urban stock | Long term (≥ 4 years) |

| Slow rebound in full-time occupancy | -0.7% | National, major cities | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Persistent Oversupply in Non-Core Office Zones of Major Cities

Madrid’s vacancy stood at 9% in 2024, yet prime CBD availability stayed below 5%, revealing a stark performance gap between core and fringe. Barcelona displayed a similar 11.36% city-wide vacancy, heavily centered in peripheral districts. Rent concessions in secondary areas erode landlord cash flow, while ESG-non-compliant buildings risk prolonged emptiness as occupiers gravitate to top-spec options. Without extensive upgrades, roughly 77% of Madrid’s stock could turn obsolete by 2030, locking in a structural drag on the Spain office real estate market.

High Retrofit Costs for Outdated Office Buildings

Europe needs USD 43.2 billion a year to raise low-rated assets to upcoming standards, yet only 17% currently comply. Spanish stock faces acute challenges due to aged mechanical systems and façades. Basel III rules have curtailed bank lending capacity by USD 135 billion, nudging owners toward pricier alternative financing. When projects occur in live buildings, tenant decanting inflates costs and disrupts rental income. Owners unwilling or unable to fund upgrades risk significant value erosion, deepening the split within the Spain office real estate market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Building Grade: Premium Assets Drive Market Polarization

Grade A premises captured 53.60% of the Spain office real estate market share in 2025, highlighting the sharpening flight-to-quality trend. Prime Madrid rents reached USD 41.0/m²/month while Barcelona registered USD 32.1/m²/month, underscoring the pricing power of top-specification stock. Vacancy inside CBD corridors remained under 5%, demonstrating robust tenant preference for ESG-certified, tech-enabled workplaces. The Grade A slice of the Spain office real estate market size is forecast to grow at a 4.52% CAGR through 2031, well ahead of legacy categories. Demand is anchored by multinational expansions, particularly from the IT and financial sectors, which value energy-efficient systems capable of lowering total occupancy costs and advancing net-zero agendas.

Grade B and C buildings confront mounting obsolescence risk unless owners commit to deep retrofits. Roughly 77% of Madrid’s total inventory must receive meaningful ESG investments by 2030 to stay relevant. Value-add investors see upside in repositioning Grade B assets, yet feasible projects demand precise cap-ex control and agile leasing strategies. Colonial’s portfolio demonstrates the income resilience of an all-green Grade A strategy: its 95% occupancy and 6.3% rental uplift in 2024 outpaced the broader market. This dichotomy suggests future development pipelines will concentrate on premium, low-carbon stock, while secondary space may transition toward alternative uses.

By Transaction Type: Rental Dominance Reflects Market Flexibility

The rental format accounted for 78.30% of 2025 activity, reinforcing occupier appetite for agility as hybrid work alters long-term space planning. Leasing volumes benefited from Spain’s tenant-friendly structures that facilitate break clauses and term renegotiations. With a 3.4% growth in like-for-like rentals and an occupancy rate of 96.7%, Merlin Properties has contributed to the effectiveness of Spain's office real estate market leasing model. Although rentals remain dominant, sales transactions are expected to clock a 4.73% CAGR to 2031, suggesting a gradual rebound in institutional buying once pricing stabilizes.

Investor confidence is recovering alongside clearer asset repricing and regulatory visibility. Projected office investment could reach USD 2.16 billion in 2024, up 32% on 2023, with a heavy tilt toward ESG-compliant properties. Flexible-workspace operators form a growing tenant segment, often signing management agreements that bridge traditional leasing and turnkey service provision. As hybrid working matures, landlords that can blend core leases with flex options and hospitality-style amenities are best placed to retain tenants across cycles within the Spain office real estate market.

By End Use: Technology Sector Leads Demand Evolution

Information technology and IT-enabled services absorbed 32.70% of all leased space in 2025, solidifying the sector’s standing as the lead growth driver. The segment is forecast to expand at a 4.92% CAGR to 2031, outpacing other occupier groups. Spanish tech firms gravitate toward innovation districts such as Barcelona’s 22@, where single-tenant requirements above 1,000 m² are commonplace. BFSI demand remains healthy, buoyed by Madrid’s 14 fresh financial-services projects in 2024. Consultancies and professional-services groups exhibit more modest growth as remote-work uptake drives portfolio rationalization.

The Spain office real estate market size for technology occupiers is widening because companies need collaboration zones, robust connectivity, and green credentials to meet internal carbon targets. Valencia's office market highlights rising demand from the technology sector, with companies requiring spaces over 1,000 square meters to support growth and collaboration, as noted by BNP Paribas Real Estate. Sectors like Retail, Life Sciences, Energy, and Legal show varied trends, with Life Sciences and Energy poised for growth due to Spain's leadership in renewable energy and pharmaceuticals. The dominance of the technology sector emphasizes the need for future office developments to focus on high-speed connectivity, flexible layouts, and sustainable features aligned with tech companies' priorities.

Geography Analysis

Madrid’s command of 41.40% of 2025 volume reflects its twin roles as government seat and foremost finance hub. Fourteen new financial-services projects last year validate sustained foreign interest, lifting prime CBD rents to USD 41.0/m²/month and compressing vacancy inside 5%. The dichotomy between Grade A scarcity and fringe surplus deepens, granting core landlords pricing power but challenging owners of legacy assets. Without aggressive ESG refurbishments, more than three-quarters of the capital’s inventory risk will slip into functional obsolescence by 2030, creating both retrofit prospects and stranded-asset threats.

Barcelona leverages its globally ranked startup ecosystem and cosmopolitan brand to sustain office demand. The city logged a 22% jump in gross take-up and pushed prime rents to USD 32.1/m²/month, while its 22@ innovation district captured almost a third of all deals. Supply-side pressure persists in peripheral rings, keeping the overall vacancy rate at 11.36%. Still, investors favor Barcelona for its liquid leasing market, depth of talent, and proven rental growth when assets hold LEED or BREEAM certificates.

Valencia is evolving into Spain’s breakout office location. A historically tight vacancy of 4.3% and rent increases nearing 9% illustrate robust demand from technology, maritime logistics, and support-service occupiers. Prime rents at USD 18.4/m²/month remain competitive, yet the differential is narrowing against Madrid and Barcelona, attracting opportunistic capital. Elsewhere, cities such as Málaga, Seville, and Bilbao gain slow but steady traction as corporates seek cost-efficient back-office sites, aided by improving digital infrastructure.

Competitive Landscape

Market structure is moderately fragmented, with global advisors CBRE, Jones Lang LaSalle IP, Inc., and Savills vying against Spanish REITs Merlin Properties and Colonial. International brokers leverage cross-border client networks and deep capital-markets expertise to secure outsized roles in mega-deals. Local landlords, in turn, capture value through ownership positions and granular market knowledge. Merlin’s USD 994.7 million capital raise in 2024 finances a 200 MW data-center pipeline, expanding revenue streams beyond conventional office rents. Colonial’s 99% green-certified portfolio illustrates a premium rent and occupancy edge that peers aim to replicate.

Digitalization and ESG analytics form the next competitive frontier. CBRE deepened its flexible-workspace capability by acquiring the remainder of Industrious and integrated Turner & Townsend to enrich project-management offerings. Such moves address occupier demands for turnkey solutions that blend space, services, and sustainability metrics. Meanwhile, specialized value-add funds target older Grade B and C stock for repositioning, betting on regulatory shifts to drive rental re-rating. This dual track—premium core holding plus opportunistic refurb—defines current portfolio strategy in the Spain office real estate market.

Opportunities are most pronounced in emerging secondary cities where barriers to entry are lower and early-mover advantages endure. Local developers that forge municipal partnerships can secure prime parcels for mixed-use precincts integrating offices, residential units, and last-mile logistics. The popularity of tenant experience platforms and real-time energy dashboards favor managers able to invest in prop-tech stack, further separating leaders from laggards.

Spain Office Real Estate Industry Leaders

-

CBRE

-

Jones Lang LaSalle IP, Inc.

-

Savills

-

Cushman & Wakefield

-

Knight Frank

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Eight Advisory launched its Madrid office on Paseo de la Castellana, targeting high-value M&A and transaction advisory mandates.

- March 2025: Spain’s Recovery and Resilience Plan opened a USD 648 million call for public-building retrofits, accelerating demand for ESG-grade upgrades.

- February 2025: Merlin Properties posted USD 422.3 million funds from operations for 2024, up 9.4%, and allocated USD 994.7 million from a capital increase to build 200 MW of data-center capacity.

- February 2025: CBRE registered 14% net-revenue growth in 2024, completed the Industrious acquisition, and advanced a USD 32 billion global development pipeline.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines Spain's office real estate market as the aggregate capital value of purpose-built multitenant and single-tenant office buildings, Grade A, B, and C, located in Madrid, Barcelona, Valencia, and other metropolitan zones, irrespective of whether space is leased or sold during the base year. Valuations incorporate rental income streams capitalized at market yields and recorded investment transactions; they also reflect stand-alone flexible work hubs that operate in office-zoned buildings.

Scope Exclusions: Owner-occupied industrial campuses, mixed-use sites where office space is below 50% of gross floor area, and assets already slated for conversion to residential or hospitality use are excluded.

Segmentation Overview

-

By Building Grade

- Grade A

- Grade B

- Grade C

-

By Transaction Type

- Rental

- Sales

-

By End Use

- Information Technology (IT & ITES)

- BFSI (Banking, Financial Services and Insurance)

- Business Consulting & Professional Services

- Other Services (Retail, Lifesciences, Energy, Legal)

-

By City

- Madrid

- Barcelona

- Valencia

- Rest of Spain

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts conducted structured conversations with leasing directors, valuation surveyors, and institutional investors active in Madrid, Barcelona, and fast-growing hubs such as Valencia. These discussions validated achievable rents, vacancy breakpoints, retrofit premiums, and forward yield expectations, thereby grounding the assumptions that desk research alone cannot capture.

Desk Research

We began with official macro and sector datasets, such as Spain's MITMA building permits, Eurostat construction cost indices, the Bank of Spain commercial-property lending dashboard, and APCEspana vacancy bulletins, because they set the factual groundwork for stock, pricing, and financing trends. Complementary insights were pulled from open press releases on prime-rent deals cataloged by property portals like idealista, together with annual reports filed by listed Spanish SOCIMIs. To sharpen company-level inputs, analysts accessed D&B Hoovers financials and screened news hits through Dow Jones Factiva. This list is indicative; many additional public and proprietary sources were reviewed for validation and gap-filling.

Market-Sizing & Forecasting

A top-down model converts reported office investment flows and registry data into total stock value, using city-level yield curves and rent series to reconstruct hidden segments. Selective bottom-up checks, sampled Grade A tower roll-ups and average rent multiplied by occupied area, are then applied to reconcile totals. Key inputs include prime monthly rent, vacancy trajectory, Grade A share of new take-up, GDP-linked office employment, and pipeline completions. Forecasts leverage a multivariate regression that ties capital values to real GDP, service-sector employment, and yield compression scenarios agreed upon by interviewed experts. Data voids in secondary cities are bridged by applying validated rent-to-price ratios from comparable markets.

Data Validation & Update Cycle

Outputs pass anomaly screens, variance checks against historic series, and peer review by a second analyst tier. Models refresh annually, with interim revisions triggered by material events such as tax reforms or sudden yield shifts. A final pre-publication sweep ensures clients receive the latest calibrated view.

Why Mordor's Spain Office Real Estate Baseline Earns Trust

Published estimates frequently diverge because firms apply different geographic scopes, asset filters, and refresh cadences.

Key gap drivers include: some studies count only Madrid and Barcelona Grade A towers, others rely solely on closed investment deals, and a few freeze exchange rates at older benchmarks, all of which pull totals down or up versus our integrated rent and transaction lens that spans five major cities and three building grades.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 39.01 B (2025) | Mordor Intelligence | - |

| USD 28.00 B (2024) | Global Consultancy A | Omits secondary cities, focuses on Grade A only, uses 2024 FX rate |

| EUR 15.00 B (2025) | Industry Association B | Captures investment deals only, excludes rental income capitalization, voluntary data submissions |

These comparisons show that, by aligning scope, variables, and timely updates, Mordor delivers a balanced, transparent baseline that decision-makers can replicate and audit with confidence.

Key Questions Answered in the Report

What is the current size of the Spain office real estate market?

The market is valued at USD 40.65 billion in 2026 and is projected to reach USD 49.94 billion by 2031.

Which segment holds the largest share of the Spain office real estate market?

Grade A buildings dominate with 53.60% of total volume thanks to strong demand for ESG-certified, tech-ready space.

Which city is forecast to grow the fastest?

Valencia is expected to post a 5.12% CAGR to 2031 as its logistics hub status and lower operating costs attract technology and back-office functions.

How big is the technology sector’s footprint?

Technology and IT-enabled services account for 32.70% of all office demand and are expanding at a 4.92% CAGR.

What drives investor interest in Spanish offices?

Investors pursue prime, green-certified assets because EU ESG regulations, robust occupancy, and rent premiums support stable cash flows.

How is hybrid working influencing leasing patterns?

Hybrid models reduce aggregate footprints but lift demand for premium, flexible space, reinforcing the rental dominance within the market.

Page last updated on: