Spain Artificial Intelligence (AI) Data Center Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

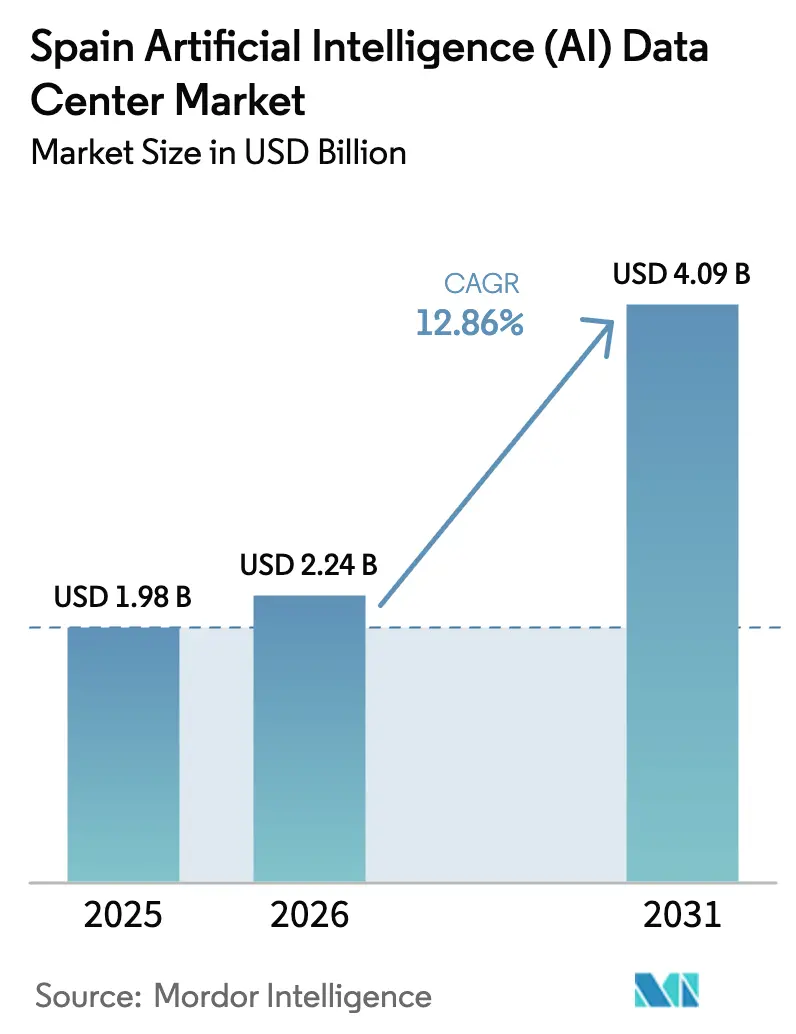

| Base Year Market Size (2025) | USD 1.98 Billion |

| Market Size (2026) | USD 2.24 Billion |

| Market Size (2031) | USD 4.09 Billion |

| Growth Rate (2026 - 2031) | 12.86% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Spain Artificial Intelligence (AI) Data Center Market Analysis by Mordor Intelligence

The Spain artificial intelligence data center market size is expected to grow from USD 1.98 billion in 2025 to USD 2.24 billion in 2026 and is forecast to reach USD 4.09 billion by 2031 at 12.86% CAGR over 2026-2031. This Spain artificial intelligence data center market size expansion reflects more than USD 23 billion in hyperscaler capital already committed, with AWS, Microsoft and Oracle anchoring large-scale roll-outs underpinned by sovereign-cloud mandates and stringent GDPR compliance requirements. Demand is amplified by the rapid shift to GPU-dense architectures, sustained public incentives totaling EUR 1.5 billion under the Spanish AI Strategy 2024 and a pronounced turn toward renewable-backed power purchase agreements (PPAs) that lower lifetime operating costs. Cloud service providers currently dominate capacity additions, yet enterprise edge build-outs are rising as 5G proliferation and latency-sensitive AI inference workloads take hold. At the component level, software retains the largest revenue share, but hardware accelerates the fastest as operators deploy liquid-cooled racks and 200-400 G switch fabrics. Regional disparities persist: Madrid concentrates the bulk of IT power, Aragón offers the largest development pipeline and Barcelona attracts colocation expansions despite grid constraints.

Key Report Takeaways

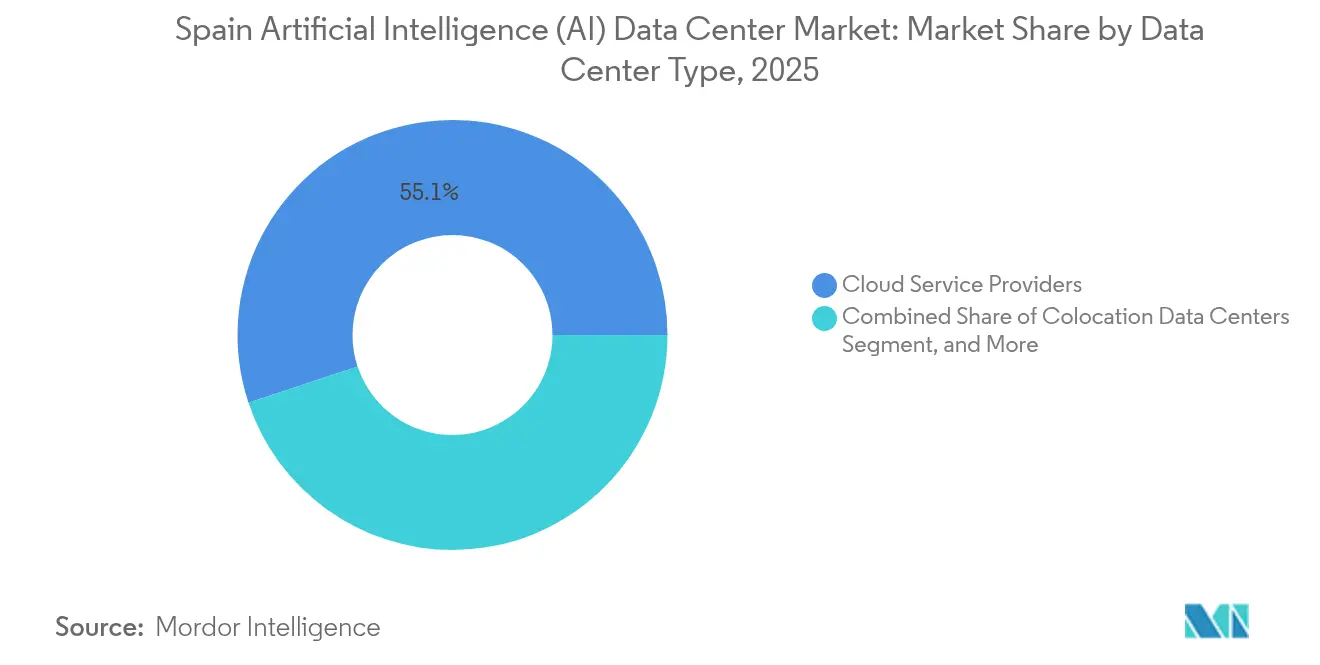

- By data center type, cloud service providers led the Spanish artificial intelligence data center market with 55.10% of the market share in 2025, whereas colocation data centers are expected to advance at a 15.58% CAGR through 2031.

- By component, software accounted for 45.20% of the Spain artificial intelligence data center market size in 2025, whereas hardware is advancing at a 15.47% CAGR through 2031.

- By tier standard, Tier IV facilities held a 61.05% share of the Spanish artificial intelligence data center market size in 2025, while Tier III is growing at a 15.86% CAGR through 2031.

- By end-user industry, IT and ITES captured 33.40% of Spain's artificial intelligence data center market share in 2025, with the internet and digital media sector forecasted to expand at a 15.74% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Viewed independently, Spain offers depth on local conditions but not full coverage of the overall global system. Mordor Intelligence's coverage on the artificial intelligence (ai) data center market brings the wider geographic picture into focus.

Spain Artificial Intelligence (AI) Data Center Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| AI-tailored cloud build-outs by hyperscalers | +4.2% | Madrid, Aragón, Barcelona | Medium term (2-4 years) |

| Rising adoption of sovereign-cloud and data-residency compliance | +3.1% | National, concentrated in Madrid | Short term (≤ 2 years) |

| Accelerated roll-out of 200-400 G switch fabrics | +2.8% | Madrid, Barcelona, Valencia | Medium term (2-4 years) |

| Surging deployment of AI training clusters in Madrid region | +2.3% | Madrid metropolitan area | Long term (≥ 4 years) |

| Availability of 100% renewable PPAs in Iberia | +1.9% | National, strongest in Aragón | Medium term (2-4 years) |

| Tax incentives on battery-based energy-storage integration | +1.2% | National, early adoption in Madrid | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

AI-Tailored Cloud Build-Outs by Hyperscalers

More than USD 23 billion in announced hyperscaler spending is re-shaping facility specifications toward liquid cooling, high-density GPU clusters and grid-connected battery storage. Microsoft alone has earmarked EUR 10 billion across several Aragón campuses, marking the largest single-region investment in continental Europe. AWS is deploying EUR 15.7 billion in and around Madrid, while Oracle has committed an additional USD 1 billion for a third local cloud region. EDGNEX is adding a 40 MW AI-ready plant focused on high-performance computing, further widening the Spain artificial intelligence data center market opportunity for specialized service providers. These concurrent programs concentrate over 1,800 MW in pipeline capacity in Aragón, positioning Spain as a central AI training node within Europe.

Rising Adoption of Sovereign-Cloud and Data-Residency Compliance

Full enforcement of the EU AI Act, coupled with Spain’s Organic Law on Data Protection, compels government agencies and regulated enterprises to localize AI workloads. The National Security Scheme and Royal Decree-Law 8/2023 stipulate that public-sector data must remain on Spanish soil and favor bids that demonstrate lower emissions and sovereign safeguards.[1]Garrigues Editorial Team, “Spain: New Measures for the Electricity Sector in Royal Decree-Law 8/2023,” Garrigues, garrigues.com BBVA’s migration to Google Cloud Spain underscores how financial institutions are setting a precedent for compliant multi-cloud strategies. Premium pricing for sovereign-aligned facilities boosts revenue per MW, supporting higher returns for in-country operators and reinforcing the Spain artificial intelligence data center market trajectory.

Accelerated Roll-Out of 200-400 G Switch Fabrics

Nokia has enabled Spain’s first 400 G Internet Exchange Point at ESpanix, replacing multiple 100 GE links and cutting power draw by 30%.[2]Ariana Lynn, “ESpanix Deploys Spain’s First 400G IXP Connectivity with Nokia,” The Fast Mode, thefastmode.com Operators are now standardizing on Arista 7700R4 and NVIDIA Spectrum-X platforms to connect GPU clusters, facilitating distributed training across metro campuses. The resulting low-latency backbone supports large language model development, fosters edge deployment and underpins the Spain artificial intelligence data center market scale-up across all major metros.

Surging Deployment of AI Training Clusters in Madrid Region

Madrid hosts the majority of Spain’s research institutes, benefits from public funds allocated under the EUR 1.5 billion Spanish AI Strategy and will house roughly 792 MW of IT capacity by 2030. The MareNostrum 5 upgrade and CSIC talent programs ensure a steady pipeline of data-science professionals, reducing operational risk for new entrants. With GPU-dense racks exceeding 80 kW per cabinet, Madrid’s facilities differentiate themselves from traditional enterprise environments, cementing the metro’s status as an AI model-training stronghold.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Grid congestion in Barcelona and Valencia metros | –2.8% | Barcelona, Valencia metropolitan areas | Short term (≤ 2 years) |

| Heightened water-use restrictions in drought-prone provinces | –2.1% | Catalonia, Valencia, Andalusia | Medium term (2-4 years) |

| Rising construction-material inflation after 2024 | –1.7% | National, acute in Madrid/Barcelona | Short term (≤ 2 years) |

| Limited domestic talent pool for AI-optimized facility O&M | –1.4% | National, concentrated in Madrid | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Grid Congestion in Barcelona and Valencia Metros

Barcelona’s installed IT load reaches just 42 MW, a quarter of Madrid’s footprint, because transmission nodes are saturated and new users must post a EUR 40 per kW security under Royal Decree-Law 8/2023.[3]DataCenterDynamics Staff, “News Spain – DCD,” DataCenterDynamics, datacenterdynamics.com Recent outages that saw Vodafone operating at 70% capacity highlight supply instability and have redirected many developers to Cantabria and Extremadura. While Panattoni secured approval for an 88 MW build, such projects carry higher development risk and extend timelines, muting near-term growth within the Spain artificial intelligence data center market for these metros.

Heightened Water-Use Restrictions in Drought-Prone Provinces

Extended drought in Catalonia and Valencia pushes local governments to tighten industrial water allowances, challenging traditional evaporative cooling. Operators now deploy closed-loop or liquid-immersion systems that add 15-25% to capex yet remain essential for GPU rigs that dissipate over 400 W per chip. District-cooling and heat-recovery schemes are turning into competitive differentiators, giving incumbents with advanced thermal designs an edge while curbing expansion by less-capitalized entrants.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Data Center Type: Cloud Providers Lead Sovereign Shift

Cloud service providers held 55.10% of Spain artificial intelligence data center market share in 2025, banking on hyperscaler roll-outs that dominate total megawatt deployments. This segment benefits directly from sovereign mandates that oblige public workloads to remain within national borders. Enterprise customers, particularly in finance and healthcare, migrate AI applications to these locally hosted hyperscale regions to meet data-sovereignty rules, deepening revenue visibility for operators. Colocation data centers, though smaller in installed base, are projected to register a 15.58% CAGR, driven by hybrid-cloud strategies that blend on-premises control with hyperscaler economics. Platform-neutral providers emphasize compliance certifications, inter-metro connectivity and on-demand GPU availability to capture workloads unsuited for single-tenant clouds within the Spain artificial intelligence data center market.

A third growth locus lies in enterprise/on-premises/edge facilities. Vodafone intends to reach 100 edge sites by the end of 2025, bringing inference capabilities closer to users and shaving milliseconds from application response times. Industrial and telecom verticals adopt micro-modular designs that slot into factories and cell-tower compounds, leveraging existing power and fiber. Although each installation is sub-megawatt, the aggregated footprint lifts demand for AI-tuned monitoring software, remote-hands services and regional interconnects. As a result, cloud, colocation and edge form a complementary stack that collectively defines the Spain artificial intelligence data center market landscape through 2030.

By Component: Software Dominance Meets Hardware Acceleration

Software generated 45.20% of 2025 spending as organizations prioritized AI model orchestration, natural-language processing and computer-vision frameworks on top of containerized environments. Deep-learning libraries such as PyTorch and TensorFlow require frequent updates and specialist tuning, creating annuity-like revenue streams for managed-service providers. Nevertheless, the hardware segment is where the fastest value growth emerges, with a 15.47% CAGR driven by GPU clusters and custom inference ASICs. Operators like EDGNEX design data halls around direct-to-chip liquid cooling, enabling rack densities of up to 120 kW, and thereby unlocking new colocation pricing tiers tied to power draw rather than floor area.

Power and cooling infrastructure investments also swell as facilities integrate 2N electrical feeds, lithium-ion battery storage and outside-air economizers to meet sustainability targets. These subsystems now account for more than one-third of total build cost, reflecting both regulatory pressure and investor due-diligence criteria tied to environmental, social and governance (ESG) metrics. In tandem, service overlays ranging from predictive maintenance to cybersecurity continue to monetize the deployed base, ensuring that the Spain artificial intelligence data center market size for services keeps pace with physical capacity growth.

By Tier Standard: Tier IV Reliability Meets Edge Flexibility

Tier IV facilities represented 61.05% of Spain artificial intelligence data center market size in 2025 as banking, healthcare and government buyers insisted on concurrently maintainable sites and fault-tolerant design. Redundant utility feeds, dual transformer yards and hot-aisle containment remain non-negotiable for AI workloads that drive real-time fraud detection or medical imaging diagnostics. These attributes command premium pricing and sustain higher revenue per square foot, reinforcing a reliability-based competitive moat for incumbent operators in major metros.

Tier III deployments, in contrast, are forecast to pace the market at 15.86% CAGR as edge nodes and cost-sensitive enterprise workloads accept slightly lower redundancy in exchange for accelerated delivery. The Nokia-backed 400 G IXP upgrade equips Tier III sites with network-level resilience that closes much of the perceived reliability gap. In rural Aragón, fast-track Tier III shells can be erected in under 12 months, catering to hyperscalers that capex-stage large campuses. Taken together, the dual-track trajectory in tier preferences underscores how the Spain artificial intelligence data center market balances uptime imperatives with capital efficiency.

By End-User Industry: IT Sector Leads Digital Transformation

IT and ITES enterprises captured 33.40% of 2025 revenue as software vendors and system integrators sought low-latency AI development sandboxes. Many adopt dedicated cages inside multi-tenant facilities to satisfy client compliance audits yet still benefit from cloud-like elasticity. Internet and Digital Media companies, spanning streaming, social networks and gaming, will record the highest 15.74% CAGR through 2031, propelled by recommendation engines and generative-content pipelines that thrive on massive GPU clusters. These firms gravitate toward Madrid and Barcelona, tapping into Spain’s sub-30 ms round-trip latency to Western Europe’s densest internet exchanges, thus elevating the Spain artificial intelligence data center market’s profile among content distributors.

BFSI players ramp AI-enabled risk scoring and algorithmic trading, with BBVA’s Google Cloud Spain deployment serving as proof of concept for regulated multi-cloud. Healthcare and life-science stakeholders invest in diagnostic imaging AI, leveraging MareNostrum 5’s supercomputing nodes for complex simulations. Manufacturing and industrial IoT users demand edge-embedded inference for quality assurance and predictive maintenance, while government and defense initiate sovereign AI projects covering language translation and border-security analytics. Telecom operators, finally, underpin network-wide 5G optimization and customer chatbots, thereby diversifying the Spain artificial intelligence data center industry revenue pool.

Geography Analysis

Madrid towers above all domestic peers, projecting 792 MW of installed IT power by 2030 as AWS, Microsoft and Oracle deepen capital commitments and the national AI strategy channels public funds into local research clusters. A dense fiber mesh, well-developed grid sub-stations and a growing talent pipeline foster a positive feedback loop that attracts secondary providers and niche service firms alike. Power-purchase agreements tied to solar plants in Castilla-La Mancha further enhance sustainability credentials, advantages that buoy the Spain artificial intelligence data center market visibility among foreign investors.

Barcelona, although trailing in grid headroom, expands colocation white space by 68% year-to-date and is on track to reach EUR 124.8 million in revenue by 2025. The city benefits from cross-border fiber to Marseille and Frankfurt, positioning it as a Mediterranean gateway for pan-European AI traffic. Developers are offsetting power constraints through onsite sub-stations and district-cooling partnerships that slash water consumption. These improvements unlock incremental capacity, keeping Barcelona relevant within the Spain artificial intelligence data center market map despite structural bottlenecks.

Aragón has emerged as Europe’s largest hyperscaler cluster outside Ireland, with over 1,800 MW in the pipeline including Microsoft’s multi-campus build and QTS’s 300 MW Calatorao project. Liberal land-use policies, abundant wind-solar resources and low population density simplify permitting and mitigate community opposition. Neighboring regions such as Cantabria and Extremadura absorb overflow demand spurred by Barcelona and Valencia grid saturation, yet their aggregate impact remains supplemental to the Madrid-Barcelona-Aragón corridor that accounts for the overwhelming bulk of Spain artificial intelligence data center market capacity.

Mordor Intelligence evaluates the artificial intelligence (ai) data center market across all key regional markets, including Europe, North America, and South America, with deeper country-level insights covering Germany, France, Canada, Chile, United Kingdom, and China.

Competitive Landscape

The Spain artificial intelligence data center market tilts toward moderate consolidation: AWS, Microsoft and Oracle control an estimated 60% of projected capacity additions through 2030, leveraging first-mover advantage in sovereign cloud contracts and hyperscale economics. Traditional colocation specialists such as Equinix, Digital Realty and Global Switch differentiate through metro-connectivity fabrics, cross-connect ecosystems and specialized compliance offerings for AI workloads. Nabiax and EDGNEX chase high-density, GPU-ready suites, carving niches inside Tier III shells that support faster time-to-market for enterprise tenants.

Spanish infrastructure giants are entering forcefully. ACS has announced intentions to invest between EUR 6 billion and EUR 12 billion in data center assets, while Iberdrola is scouting partners to co-develop renewable-backed campuses. These moves inject long-dated infrastructure capital and engineering know-how, intensifying competition and potentially compressing yields. Technology rivalry focuses on cooling efficiency: liquid-immersion, rear-door heat exchangers and waste-heat reuse are now table stakes for bids targeting AI clusters.

Regulatory hurdles shape strategy. Royal Decree-Law 8/2023 introduces competitive bidding for new grid connections, implicitly favoring operators with strong balance sheets and proven construction discipline. Sustainability metrics, notably 100% renewable PPAs and low Water Usage Effectiveness (WUE) scores, are becoming decisive factors in public and enterprise RFPs. Against this backdrop, M&A activity, exemplified by the Nabiax sales process involving Goldman Sachs Asset Management and international funds, is poised to rise as investors seek scale and geographic diversification, consolidating the Spain artificial intelligence data center industry.

Spain Artificial Intelligence (AI) Data Center Industry Leaders

IBM Corporation

Amazon Web Services Inc.

Microsoft Ireland Operations Ltd.

Alphabet Inc. (Google Cloud Spain SL)

Meta Platforms Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Spanish telecom carriers deploy backup generators during nationwide outages, with Vodafone operating at 70% capacity, spotlighting grid reliability issues for data centers.

- March 2025: Microsoft announced that it is expanding its data center operations in Spain. The Aragon government announced that Microsoft will invest an additional USD 3 billion to build a new data center campus in Zaragoza, near Puerto Venecia. The company also plans to invest USD 2.1 billion in cloud computing and AI infrastructure in Spain over the next two years.

- March 2025: Microsoft unveils an additional campus in Zaragoza within its EUR 10 billion Aragón program, reinforcing Spain’s largest hyperscaler cluster.

- March 2025: Google signs a 35 MW wind PPA with Exus Renewables, its third Spanish renewable agreement of 2025.

Spain Artificial Intelligence (AI) Data Center Market Report Scope

The research encompasses the full spectrum of AI applications in data centers, covering hyperscale, colocation, enterprise, and edge facilities. The analysis is segmented by component, distinguishing between hardware and software. Hardware considerations include power, cooling, networking, IT equipment, and more. Software technologies under scrutiny encompass machine learning, deep learning, natural language processing, and computer vision. The study also evaluates the geographical distribution of these applications. Additionally, it assesses AI's influence on sustainability and carbon neutrality objectives. A comprehensive competitive landscape is presented, detailing market players engaged in AI-supportive infrastructure, encompassing both hardware and software utilized across various AI data center types. Market size is calculated in terms of revenue generated by products and solutions providers in the market and forecasts are presented in USD Million for each segment.

| Cloud Service Providers |

| Colocation Data Centers |

| Enterprise / On-Premises / Edge |

| Hardware | Power Infrastructure |

| Cooling Infrastructure | |

| IT Equipment | |

| Racks and Other Hardware | |

| Software | Technology |

| Machine Learning | |

| Deep Learning | |

| Natural Language Processing | |

| Computer Vision | |

| Services | Managed Services |

| Professional Services |

| Tier III |

| Tier IV |

| IT and ITES |

| Internet and Digital Media |

| Telecom Operators |

| Banking, Financial Services and Insurance (BFSI) |

| Healthcare and Life Sciences |

| Manufacturing and Industrial IoT |

| Government and Defense |

| By Data Center Type | Cloud Service Providers | |

| Colocation Data Centers | ||

| Enterprise / On-Premises / Edge | ||

| By Component | Hardware | Power Infrastructure |

| Cooling Infrastructure | ||

| IT Equipment | ||

| Racks and Other Hardware | ||

| Software | Technology | |

| Machine Learning | ||

| Deep Learning | ||

| Natural Language Processing | ||

| Computer Vision | ||

| Services | Managed Services | |

| Professional Services | ||

| By Tier Standard | Tier III | |

| Tier IV | ||

| By End-user Industry | IT and ITES | |

| Internet and Digital Media | ||

| Telecom Operators | ||

| Banking, Financial Services and Insurance (BFSI) | ||

| Healthcare and Life Sciences | ||

| Manufacturing and Industrial IoT | ||

| Government and Defense | ||

Key Questions Answered in the Report

What is the current value of the Spain artificial intelligence data center market?

The market is valued at USD 2.24 billion in 2026 and is on course to hit USD 4.09 billion by 2031.

Which segment holds the largest Spain artificial intelligence data center market share?

Cloud service providers lead with 55.10% share based on 2025 figures.

Which Spanish region houses the biggest pipeline of hyperscaler capacity?

Aragón hosts more than 1,800 MW of planned IT power, the largest concentration outside Ireland.

What CAGR is forecast for hardware spending within Spain’s AI data centers?

Hardware revenue is set to grow at 15.47% CAGR through 2031.

Why are Tier III facilities expanding faster than Tier IV in Spain?

Edge computing needs and lower build costs drive a 15.86% CAGR for Tier III, while network upgrades offset most reliability gaps.

Page last updated on: