South America Artificial Intelligence (AI) Data Center Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

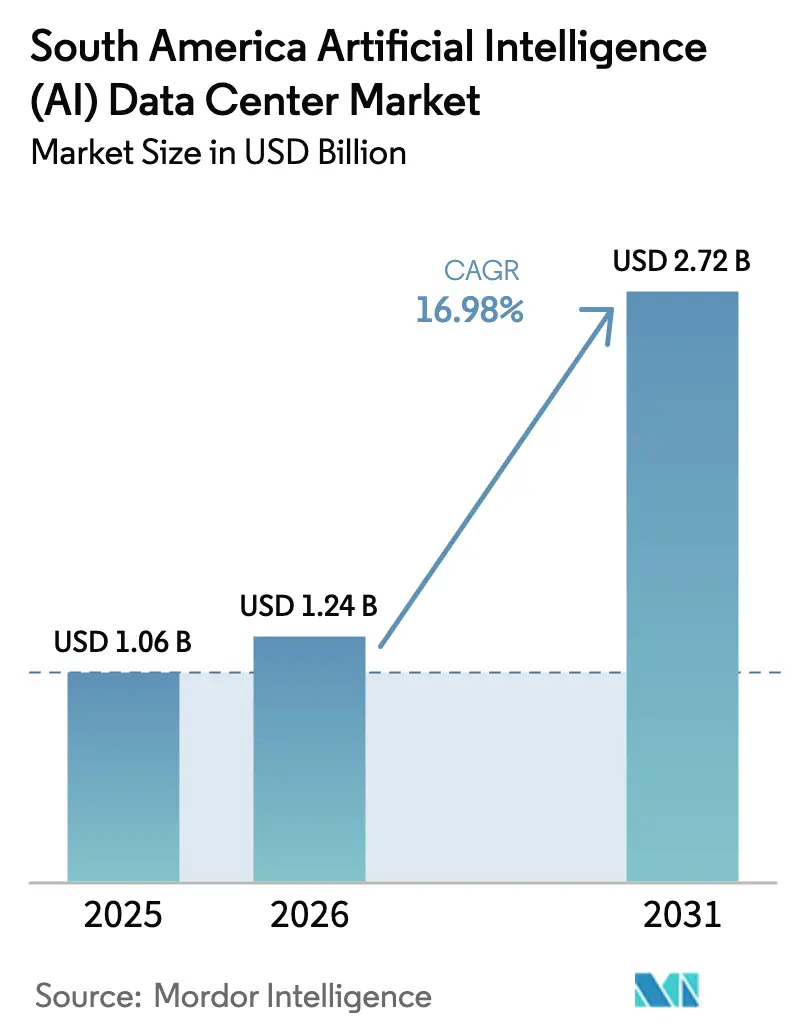

| Base Year Market Size (2025) | USD 1.06 Billion |

| Market Size (2026) | USD 1.24 Billion |

| Market Size (2031) | USD 2.72 Billion |

| Growth Rate (2026 - 2031) | 16.98% CAGR |

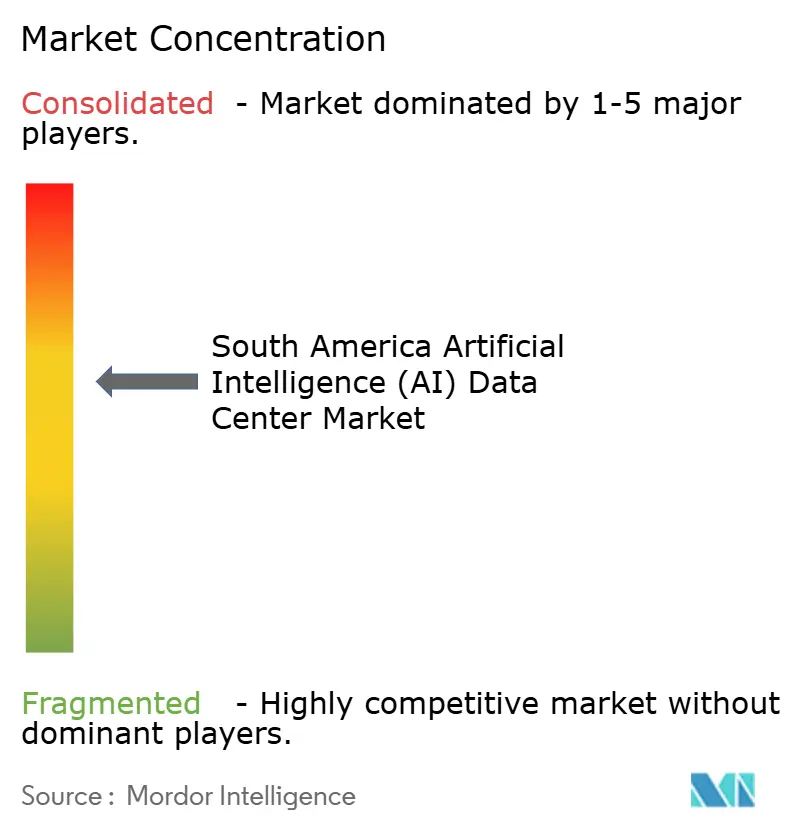

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

South America Artificial Intelligence (AI) Data Center Market Analysis by Mordor Intelligence

The South America artificial intelligence data center market size in 2026 is estimated at USD 1.24 billion, growing from 2025 value of USD 1.06 billion with 2031 projections showing USD 2.72 billion, growing at 16.98% CAGR over 2026-2031. Continued hyperscale cloud commitments, rapid enterprise digitalization, and increasing access to renewable energy are key drivers of this trajectory. The South America artificial intelligence data center market benefits from Brazil’s dominant hosting base, Chile’s sustainable campus build-outs, and Argentina’s fintech-led demand, which collectively attract global capital. Heightened GPU density prompts operators to reassess power delivery and liquid cooling, while hybrid architectures drive growth in colocation. Strategic tax incentives linked to clean energy, coupled with submarine cable upgrades, further reinforce the South America artificial intelligence data center market as a preferred regional hub.[1]Natália Flach, “Tecto invests R$550m in data center in Ceará,” Valor International, valorinternational.globo.com

Key Report Takeaways

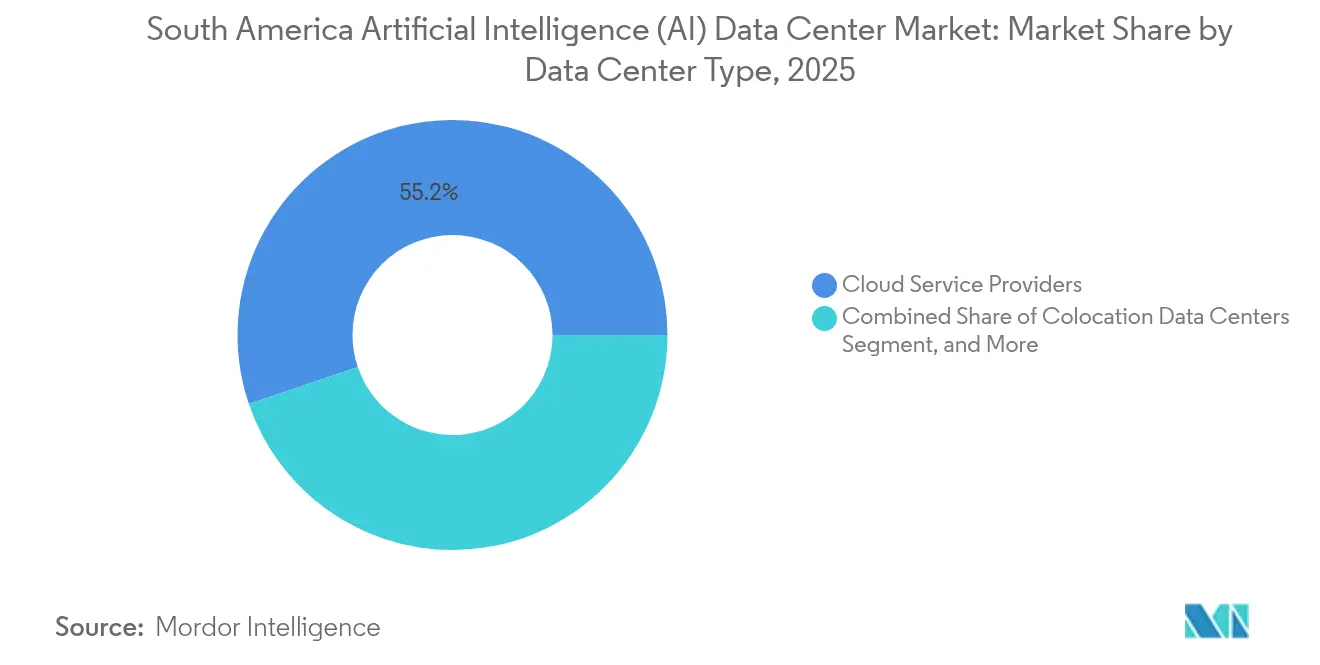

- By data center type, Cloud Service Providers led the South America artificial intelligence data center market with a 55.20% revenue share in 2025; Colocation Data Centers are expected to advance at a 18.55% CAGR through 2031.

- By component, software held 45.10% of the South America artificial intelligence data center market share in 2025, while hardware is projected to grow at an 18.24% CAGR to 2031.

- By tier standard, Tier IV captured 61.05% share of the South America artificial intelligence data center market size in 2025, and Tier III is forecast to expand at a 18.60% CAGR.

- By end-user industry, IT and ITES accounted for a 33.40% share of the South America artificial intelligence data center market size in 2025, and the Internet and Digital Media sector is set to post an 17.90% CAGR.

- By country, Brazil held a 56.70% market share of the South America artificial intelligence data center market in 2025; Argentina recorded the fastest growth at an 18.05% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Understanding the full system requires moving beyond South america boundaries into a wider international view. Mordor Intelligence captures the global artificial intelligence (ai) data center market scope in its worldwide coverage.

South America Artificial Intelligence (AI) Data Center Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Hyperscale cloud investments across Brazil and Chile | +4.2% | Brazil, Chile, Argentina | Medium term (2-4 years) |

| Low-latency AI demand from fintech and e-commerce | +3.8% | Brazil, Argentina, Colombia | Short term (≤ 2 years) |

| Renewable-energy incentives for data centers | +2.9% | Brazil, Chile, Uruguay | Long term (≥ 4 years) |

| Expansion of AI edge micro data centers along 5G corridors | +2.1% | São Paulo, Santiago, Buenos Aires | Medium term (2-4 years) |

| Under-utilized hydroelectric assets enabling green clusters | +1.8% | Paraguay, Brazil, Chile | Long term (≥ 4 years) |

| Heat-reuse partnerships in Santiago | +0.7% | Chile, Argentina | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in hyperscale cloud investments across Brazil and Chile

Massive multiyear allocations by Amazon Web Services (USD 1.8 billion) and Microsoft (USD 14.7 billion) anchor new sovereign-cloud zones that comply with looming data-localization statutes. The facilities emphasize high-density GPU halls engineered for sub-10 millisecond latency serving algorithmic trading, instant payments, and autonomous systems. Local regulators accelerate approvals when projects couple renewable power contracts with community fiber expansion. Santiago’s growing role as a trans-Pacific landing point further cements the South America artificial intelligence data center market as a conduit for Asian data flows.

Growing demand for low-latency AI workloads from fintech and e-commerce

Brazil’s PIX rails now clear 29 billion transactions yearly, producing data streams that fuel fraud-detection and credit-scoring models running in regional GPU clusters. E-commerce marketplaces integrate dynamic pricing and recommendation engines that must respond within single-digit milliseconds to protect checkout conversions. Similar latency imperatives materialize in Argentina, where sandboxed fintech pilots process peso-denominated microloans and NLP chatbots tuned to local dialects. These applications accelerate enterprise migration toward colocation and edge nodes in the South America artificial intelligence data center market.[2]Center for Data Innovation, “How Generative AI Is Changing the Global South's IT Services Sector,” datainnovation.org

Government incentives for renewable-energy-backed data centers

Brazil’s ANEEL discounts transmission fees for operators sourcing over 70% of their power from renewable sources, and Chile expedites permits when facilities interconnect with solar or hydroelectric plants. Such policies dovetail with corporate carbon-neutral mandates, making long-term power purchase agreements a competitive differentiator. Operators also monetize grid-balancing services by modulating AI training cycles during peak demand, creating additional revenue streams that sustain the profitability of the South America artificial intelligence data center market.

Rapid expansion of AI-focused edge micro data centers along 5G corridors

Specialists like EdgeUno deploy 1-5 MW pods within 20 km of population centers, exploiting telco fiber to guarantee <10 ms round-trip. These nodes support real-time traffic optimization in São Paulo, AR shopping trials in Santiago, and predictive maintenance in Chile’s mining belts. Telcos view the architecture as an avenue to monetize idle ducts and lock in enterprise clients, thereby widening the South America artificial intelligence data center market footprint.[3]BNamericas Staff, “Atlas Renewable to announce first contracts with LatAm datacenters," BNamericas, bnamericas.com

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Inadequate regional power grid reliability | -2.8% | Argentina, secondary Brazilian and Chilean cities | Short term (≤ 2 years) |

| High capital expenditure and lengthy permitting | -2.1% | Argentina, Colombia | Medium term (2-4 years) |

| Skilled-workforce scarcity outside Brazil | -1.9% | Argentina, Chile, Colombia | Medium term (2-4 years) |

| Water-stress rules limiting evaporative cooling | -1.4% | Chile, Uruguay, southern Brazil | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Inadequate regional power grid reliability

Voltage fluctuations and frequency swings in Argentina’s grid increase the risk of unscheduled GPU shutdowns, which can reset multiday model-training runs. Operators over-spec backup diesel arrays and double-conversion UPS systems, inflating total project costs and eroding returns. Similar reliability gaps in secondary Brazilian and Chilean markets slow greenfield build-outs until transmission upgrades arrive, tempering near-term growth for the South America artificial intelligence data center market.

Water-stress regulations limiting evaporative cooling

Chile bars new evaporative towers in drought-prone regions, compelling operators to adopt air-cooled chillers or immersion baths that lift capex by USD 2-3 million per site. Uruguay demands closed-loop recycling, adding system complexity. GPU racks dissipate more than 30 kW each, raising the stakes for efficient thermal designs. Compliance costs slow deployments yet also spur innovation in heat-reuse agreements with district-energy operators, subtly reshaping the South America artificial intelligence data center market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Data Center Type: Cloud Dominance Meets Colocation Momentum

Cloud Service Providers claimed 55.20% of 2025 revenue as hyperscalers embedded sovereign zones in São Paulo and Santiago. The colocation sub-segment is forecasted to deliver the fastest 18.55% CAGR, as enterprises adopt hybrid strategies that balance latency, cost, and data sovereignty needs. The South America artificial intelligence data center market size for colocation solutions is projected to hit USD 1.06 billion by 2031, reflecting rising demand for shared GPU suites and compliance-ready whitespace. Edge nodes, although currently niche, attract industrial operators seeking local inference and disaster recovery options.

Hybrid deployments meld self-hosted training clusters with cloud burst capacity, sidestepping egress fees. AWS Outposts and Microsoft Azure Stack form anchor tenants inside regional colocation halls, validating the model’s viability. Over the forecast period, improved metro fiber and 5G densification will further entrench colocation’s role within the South America artificial intelligence data center market.

By Component: Software Leads, Hardware Accelerates

Software retained 45.10% revenue in 2025 on the back of recurring licenses for ML frameworks and MLOps pipelines. Yet hardware is slated to climb at an 18.24% CAGR as GPU scarcity inflates prices and operators invest in liquid-cooling manifolds and 20 kV substations. Power and cooling infrastructure accounts for the bulk of incremental spending, while services contribute steady single-digit growth through consulting and compliance management.

GPU shortages prompt buyers to reserve capacity years in advance, securing hardware revenue. Scala’s 560 MW switchyard and Ascenty’s modular substation program illustrate the capex scale required to host AI clusters, reinforcing the hardware uptrend within the South America artificial intelligence data center market.

By Tier Standard: Tier IV Strength Faces Tier III Speed

Tier IV governed 61.05% of the 2025 share, prized for its 99.995% availability, vital to week-long training runs. However, Tier III is on course for a 18.60% CAGR as edge inference tolerates short outages in exchange for locality and cost. Operators weigh duplicated feeds and fault-tolerant software to decide between standards. The South America artificial intelligence data center market share for Tier III is expected to expand most in secondary metros, where land and energy costs favor lower redundancy.

Urban edge nodes prioritize latency over uptime, deploying modular Tier III shells adjacent to 5G towers. These installations often co-locate with telco shelters, integrating battery racks but omitting dual generators, illustrating architectural diversity across the South America artificial intelligence data center market.

By End-user Industry: IT Leadership With Media Uptick

IT and ITES entities commanded 33.40% 2025 revenue, leveraging AI sandboxes for code generation, test automation, and managed-service delivery. Banking, Financial Services, and Insurance followed closely, buoyed by real-time fraud filters on PIX and open-banking APIs.

The Internet and Digital Media sector is forecasted to grow at an 17.90% CAGR, driven by the rollouts of streaming CDNs and the personalization of generative AI content. Healthcare pilots radiology triage algorithms, while manufacturing firms deploy predictive maintenance on conveyor lines. This industry mix underpins diversified demand in the South America artificial intelligence data center market.

Geography Analysis

Brazil captured 56.70% 2025 revenue, sustained by robust power grids, submarine cables, and pro-investment statutes such as REIDI tax exemptions for ICT infrastructure. The South America artificial intelligence data center market size within Brazil is projected to surpass USD 1.55 billion by 2031. São Paulo clusters concentrate >500 MW of commissioned AI capacity, yet operators are expanding into Ceará and Rio Grande do Sul to access renewable portfolios and reduce land costs.

Argentina posts the swiftest 18.05% CAGR, driven by the National AI Plan, central bank fintech sandboxes, and a deep STEM talent pool. Buenos Aires campuses anchor most projects, but Mendoza targets edge nodes serving western corridors. Currency volatility increases hedging costs, yet demand for colocation from near-shore BPO firms offsets risk. Consequently, the South America artificial intelligence data center market share in Argentina is poised to expand steadily through 2031.

The rest of South America, comprising Chile, Paraguay, Colombia, and Uruguay, offers a differentiated appeal. Chile couples 100% renewable grids with Pacific subsea links, positioning Santiago as a strategic redundancy zone. Paraguay’s surplus hydroelectric power enables low-cost, 100 MW-scale campuses, such as HIVE Digital’s Itaipu-adjacent project. Colombia’s Bogotá-Medellín axis lures edge builds servicing Andean e-commerce. Collectively, these geographies diversify risk and spread the South America artificial intelligence data center market footprint across varied regulatory and resource contexts.

Mordor Intelligence examines the artificial intelligence (ai) data center market across diverse other regional markets as well, including Middle East and Africa, North America, and Europe, while also offering granular country-level perspectives for Brazil, Chile, United Arab Emirates, Spain, Netherlands, and Canada and more.

Competitive Landscape

Moderate concentration defines the arena, with regional champions Scala Data Centers and Ascenty leveraging land banks and utility pacts, while hyperscalers such as AWS and Microsoft inject scale and technology leadership. Equinix and Digital Realty import global design standards and interconnection fabrics. V.tal’s spin-off of Tecto underscores telco ambitions to monetize fiber backbones through colocation, intensifying rivalry in the South America artificial intelligence data center market.

Sustainability credentials surface as a key battleground. ODATA’s ISO 14001 certification secures multinationals with stringent ESG targets, while Scala’s planned AI City touts 4.7 GW of potential green-powered IT capacity. Investment funds eye consolidation; IFX Networks catalogs 25 potential takeovers, indicating an impending roll-up cycle that may lift the combined top-five share toward 60% in the South America artificial intelligence data center market.

Strategic moves illustrate momentum. Cirion earmarked USD 300 million for 2024 Latin American builds, targeting expansions in Rio de Janeiro and Bogotá. Elea Digital added 120 MW near São Paulo to service the hyperscale pipeline overflow. Atlas Renewable is finalizing PPAs linking solar farms to new Chilean campuses, signaling power-sourcing innovation that further differentiates players within the South America artificial intelligence data center market.

South America Artificial Intelligence (AI) Data Center Industry Leaders

-

Ascenty Data Centers e Telecommunicações Ltda.

-

Scala Data Centers S.A.

-

ODATA Brasil S.A.

-

Equinix Inc.

-

Amazon Web Services Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Scala Data Centers, along with several other big Latin American operators, trimmed payrolls as part of a move from fixed to more flexible cost models. Scala’s headcount fell from around 1,200 to just under 1,000 people. Managers pointed to ongoing shortages of GPUs and racks as the trigger, and said that more design and build work will now be allocated to local contractors as regional supply chains mature.

- February 2025: A study in the journal Globalizations examined more than 900 data-labeling workers in Argentina, Brazil, and Venezuela, finding widespread job insecurity and skills gaps. Uneven education levels and informal work arrangements are making it harder for AI data center operators to hire and retain qualified staff.

- October 2024: Telecom carrier V.tal set up a new subsidiary, Tecto, to pull its colocation sites under one roof and chase the growing demand for hybrid-cloud space in Brazil. By leveraging its fiber network and existing enterprise ties, V.tal aims to compete with the country’s established data-center heavyweights.

- September 2024: Scala Data Centers unveiled “Scala AI City,” a proposed USD 50 billion campus in Brazil that could eventually host up to 4.7 GW of IT load. If built, the project would rank among the world’s largest purpose-built hubs for AI workloads, underscoring just how much infrastructure the region now requires for digital transformation programs.

South America Artificial Intelligence (AI) Data Center Market Report Scope

The research encompasses the full spectrum of AI applications in data centers, covering hyperscale, colocation, enterprise, and edge facilities. The analysis is segmented by component, distinguishing between hardware and software. Hardware considerations include power, cooling, networking, IT equipment, and more. Software technologies under scrutiny encompass machine learning, deep learning, natural language processing, and computer vision. The study also evaluates the geographical distribution of these applications.

Additionally, it assesses AI's influence on sustainability and carbon neutrality objectives. A comprehensive competitive landscape is presented, detailing market players engaged in AI-supportive infrastructure, encompassing both hardware and software utilized across various AI data center types. Market size is calculated in terms of revenue generated by products and solutions providers in the market, and forecasts are presented in USD Billion for each segment.

| Cloud Service Providers |

| Colocation Data Centers |

| Enterprise / On-Premises / Edge |

| Hardware | Power Infrastructure |

| Cooling Infrastructure | |

| IT Equipment | |

| Racks and Other Hardware | |

| Software | Technology |

| Machine Learning | |

| Deep Learning | |

| Natural Language Processing | |

| Computer Vision | |

| Services | Managed Services |

| Professional Services |

| Tier III |

| Tier IV |

| IT and ITES |

| Internet and Digital Media |

| Telecom Operators |

| Banking, Financial Services and Insurance (BFSI) |

| Healthcare and Life Sciences |

| Manufacturing and Industrial IoT |

| Government and Defense |

| Brazil |

| Argentina |

| Chile |

| Rest of South America |

| By Data Center Type | Cloud Service Providers | |

| Colocation Data Centers | ||

| Enterprise / On-Premises / Edge | ||

| By Component | Hardware | Power Infrastructure |

| Cooling Infrastructure | ||

| IT Equipment | ||

| Racks and Other Hardware | ||

| Software | Technology | |

| Machine Learning | ||

| Deep Learning | ||

| Natural Language Processing | ||

| Computer Vision | ||

| Services | Managed Services | |

| Professional Services | ||

| By Tier Standard | Tier III | |

| Tier IV | ||

| By End-user Industry | IT and ITES | |

| Internet and Digital Media | ||

| Telecom Operators | ||

| Banking, Financial Services and Insurance (BFSI) | ||

| Healthcare and Life Sciences | ||

| Manufacturing and Industrial IoT | ||

| Government and Defense | ||

| By Country | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

Key Questions Answered in the Report

What drives South America's AI data center growth?

The market is propelled by hyperscale cloud investments (USD 1.8 billion from AWS, USD 14.7 billion from Microsoft), fintech's need for low-latency processing, and renewable energy incentives that reduce operational costs. Brazil leads with 56.70% market share, while Argentina shows the fastest growth at 18.05% CAGR through 2031.

How do power challenges affect AI deployments in South America?

Power grid reliability issues in Argentina and secondary markets create risks for GPU clusters that require continuous operation. This forces operators to invest in oversized backup systems, increasing costs by 15-20%. Meanwhile, Chile and Uruguay restrict water usage for cooling, pushing operators toward air-cooled or immersion technologies that add USD 2-3 million to typical construction budgets.

Which companies lead the South American AI data center market?

The market shows moderate concentration with regional specialists (Scala Data Centers, Ascenty), global hyperscalers (AWS, Microsoft), and telecommunications operators (V.tal/Tecto) holding significant positions. Scala's planned USD 50 billion AI City campus with 4.7 GW potential capacity exemplifies the scale of investments underway.

Why is colocation growing faster than cloud in South America?

Colocation data centers are growing at 18.55% CAGR (versus 16.98% market average) as enterprises adopt hybrid architectures that balance cloud scalability with on-premises control. This model enables companies to maintain direct oversight of sensitive AI training data while sharing infrastructure costs, particularly appealing for financial and healthcare sectors with strict compliance requirements.

How are sustainability concerns shaping the market?

Environmental factors significantly influence deployments, with Brazil's ANEEL offering reduced transmission charges for facilities sourcing over 70% renewable power. Chile expedites permits for solar/hydro integration, while ODATA's ISO 14001 certification attracts multinationals with ESG mandates. Paraguay's abundant hydropower enables projects like HIVE Digital's 100 MW facility at competitive rates.

What role does edge computing play in South America's AI landscape?

Edge micro data centers (1-5 MW) are expanding along 5G corridors to support applications requiring sub-10 millisecond latency, including traffic management in São Paulo, augmented reality in Santiago, and industrial IoT in mining regions. While currently a smaller segment, edge deployments are strategic for telecommunications operators monetizing fiber investments through AI infrastructure.

Page last updated on: