Brazil Artificial Intelligence (AI) Data Center Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

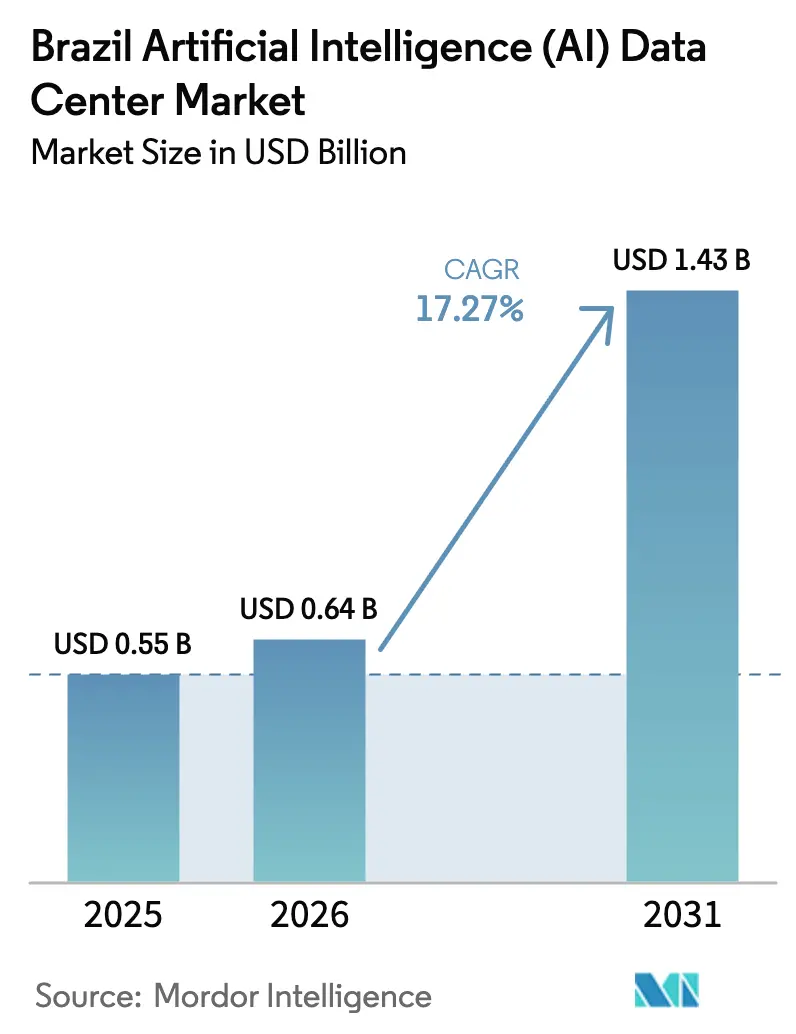

| Base Year Market Size (2025) | USD 0.55 Billion |

| Market Size (2026) | USD 0.64 Billion |

| Market Size (2031) | USD 1.43 Billion |

| Growth Rate (2026 - 2031) | 17.27% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Brazil Artificial Intelligence (AI) Data Center Market Analysis by Mordor Intelligence

The Brazil artificial intelligence data center market size is expected to grow from USD 0.55 billion in 2025 to USD 0.64 billion in 2026 and is forecast to reach USD 1.43 billion by 2031 at 17.27% CAGR over 2026-2031. Surging enterprise AI adoption, strong government incentives, abundant renewable energy, and rapid connectivity upgrades together fuel sustained capacity additions across both hyperscale and colocation facilities. The Brazil artificial intelligence data center market benefits from São Paulo’s mature fiber footprint, while rising Tier III builds in secondary metros reflect tenants’ growing appetite for lower-cost, quicker-to-deploy capacity. Hardware densification expands power demand per rack, prompting liquid-cooling retrofits and creative heat-reuse schemes. Competition centers on energy efficiency, sovereign cloud compliance, and sub-five-millisecond latency, giving operators with renewable power purchase agreements and edge nodes a clear advantage.

Key Report Takeaways

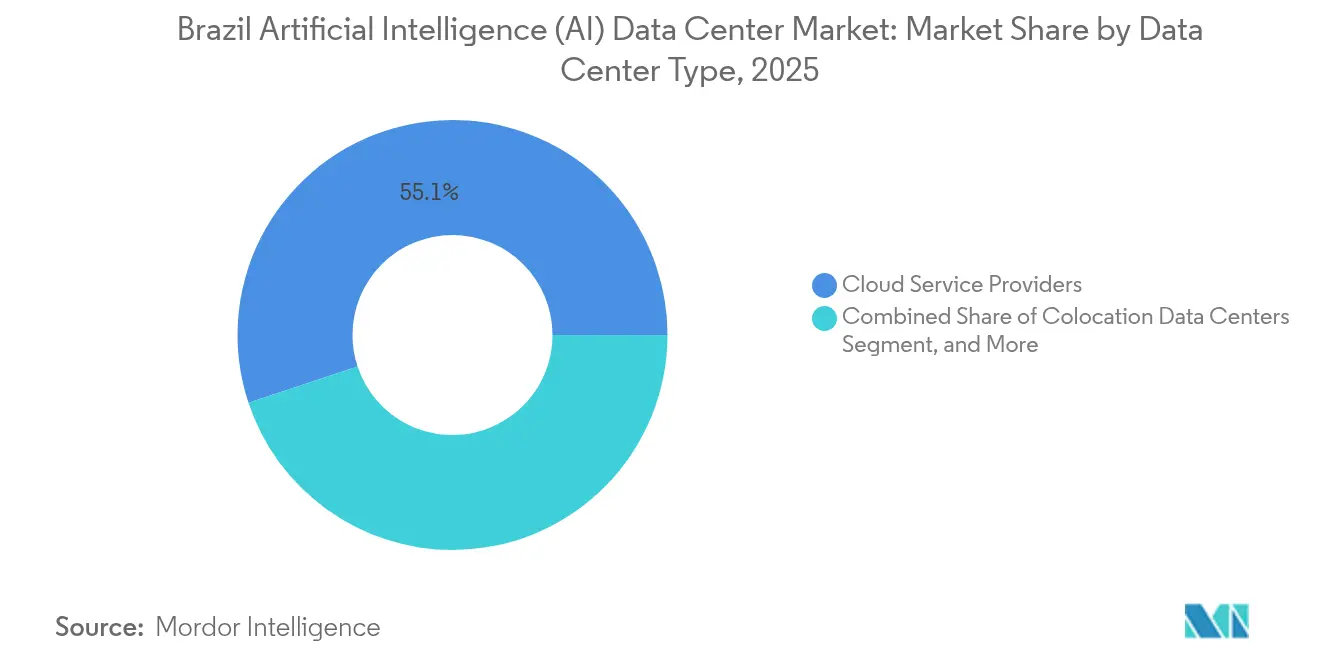

- By data center type, cloud service providers held 55.10% of the Brazilian artificial intelligence data center market share in 2025, whereas colocation facilities are forecast to post the fastest growth of 18.76% CAGR through 2031.

- By component, software platforms captured a 45.25% revenue share of the Brazilian artificial intelligence data center market in 2025, while hardware investments are projected to expand at a 19.05% CAGR through 2031, reflecting the escalating deployment of GPU clusters.

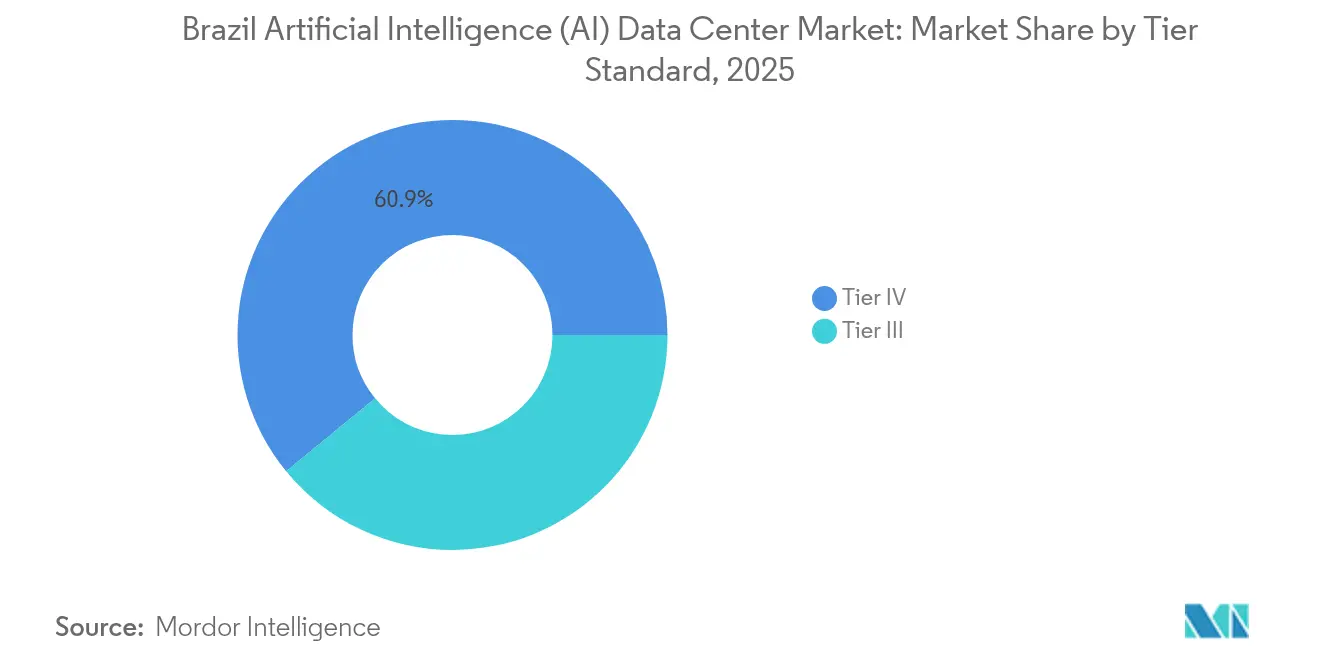

- By tier standard, Tier IV sites commanded 60.92% of the Brazilian artificial intelligence data center market size in 2025, yet Tier III projects are expected to exhibit an 18.35% CAGR through 2031.

- By end-user industry, IT and ITES accounted for 33.45% of the revenue in the Brazilian artificial intelligence data center market in 2025, while Internet and Digital Media services are projected to advance at a 19.62% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Dynamics observed within Brazil present a country level view when set against the broader international context. The artificial intelligence (ai) data center market analysis by Mordor Intelligence provides that expanded global perspective.

Brazil Artificial Intelligence (AI) Data Center Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government tax incentives for data center capex | +3.2% | National, with early gains in São Paulo, Rio de Janeiro, Ceará | Medium term (2-4 years) |

| Rapid cloud adoption among enterprises | +4.1% | National, concentrated in Southeast and South regions | Short term (≤ 2 years) |

| 5G rollout and submarine cable upgrades | +2.8% | National, with priority in São Paulo, Rio de Janeiro, Fortaleza | Medium term (2-4 years) |

| Offshore wind-to-hydrogen PPAs for green power | +1.9% | Coastal regions, particularly Northeast and South | Long term (≥ 4 years) |

| Edge AI demand in agribusiness IoT | +2.4% | Interior regions, São Paulo, Mato Grosso, Rio Grande do Sul | Medium term (2-4 years) |

| Heat-reuse district energy schemes in São Paulo | +1.1% | São Paulo metropolitan region | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Government tax incentives for data center capex

Federal policy grants import-duty relief on non-domestic equipment, trimming upfront costs for generators, switchgear, and immersion-cooling tanks. Ministries coordinate with BNDES to streamline low-rate loans, making 15-year greenfield projects financially viable even outside São Paulo. Fiscal clarity reduces investor risk and accelerates permit approvals, which have historically taken over 18 months. Early adopters utilize additional depreciation allowances to refresh their GPU inventories on a three-year cycle, thereby maintaining competitive performance per watt. The measure attracts offshore capital that previously bypassed Brazil in favor of Chile or Mexico.

Rapid cloud adoption among enterprises

More than 150 large Brazilian corporations now run production-scale generative AI, creating immediate demand for high-density cages capable of 30 kW per rack.[1]Casa Civil, “Política Nacional de Data Centers,” planalto.gov.br Banks allocate dedicated pods for fraud-detection models that retrain hourly, while retailers deploy computer-vision checkouts during weekend peaks. Government procurement for tax-processing platforms mandates NVMe storage and 400 GbE switching, pushing colocation providers to pre-install higher-tier power strips. The trend initially concentrates in São Paulo and Porto Alegre, but secondary cities see spillover effects once metro fiber routes mature. Cloud migration also drives the development of sovereign-cloud nodes that meet Brazilian data-residency laws.

5G rollout and submarine cable upgrades

Nationwide 5G coverage requires local cache nodes to ensure video buffering remains under 30 milliseconds, prompting micro-edge builds in Fortaleza and Brasília. New subsea cables landing in Rio de Janeiro and Santos halve round-trip latency to Lisbon, benefitting multi-region AI inference clusters. DE-CIX internet exchanges shorten hop counts to Frankfurt, lowering network costs for training workloads that synchronize across continents. Mobile operators shift traffic analytics from core to edge, unlocking colocation demand at 3 MW mini-hubs near radio-access networks. International cloud vendors secure dark-fiber IRUs to guarantee path diversity and comply with new cyber-resilience norms.

Edge AI demand in agribusiness IoT

Satellite-linked harvesters in Mato Grosso transmit 50 GB per day of imagery, which edge servers compress and label before backhauling summaries to São Paulo cores. Farms adopting autonomous drones require sub-second feedback loops to adjust pesticide spray patterns, spurring the build-to-suit containers cooled by evaporative towers. Telecom operators bundle private LTE and GPU edge nodes under revenue-sharing agreements with cooperatives managing over 1 million hectares. Commodity traders analyze truck-weight sensors en route to ports, reducing demurrage fees and boosting export margins. These use cases anchor smaller 500 kW facilities that feed regional aggregation hubs, expanding the Brazil artificial intelligence data center market beyond coastal metros.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Electricity cost volatility and shortages | -2.8% | National, acute in Northeast during drought periods | Short term (≤ 2 years) |

| Shortage of AI infrastructure engineers | -1.9% | National, concentrated in São Paulo, Rio de Janeiro | Medium term (2-4 years) |

| Water-scarcity regulations on cooling | -1.5% | Semi-arid regions, particularly Northeast and interior | Medium term (2-4 years) |

| Environmental licensing delays near protected biomes | -1.2% | Amazon region, Atlantic Forest, Cerrado boundaries | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Electricity cost volatility and shortages

Transmission queue requests ballooned from 2.5 GW in May 2024 to 9 GW four months later, exceeding available corridors and delaying energization of new halls.[2]Agência Nacional de Energia Elétrica, “Relatório de Acesso à Transmissão,” aneel.gov.br During El Niño droughts, hydro reservoirs fall, forcing thermal dispatch that lifts wholesale spot prices above BRL 750 per MWh, eroding operator margins. Developers hedge via ten-year solar PPAs in Minas Gerais, yet wheeling charges still fluctuate under regulatory reviews. Provisional Measure 1.307 obliges hyperscalers to contract only new-generation power, limiting the arbitrage of legacy hydroelectric output. Grid constraints spur the development of on-site battery farms, although lithium prices remain elevated, complicating payback calculations.

Water-scarcity regulations on cooling

Ceará authorities now cap groundwater draw for industrial users after multiyear deficits, compelling forthcoming campuses to adopt 100% air-cooled chillers or seawater desalination. Environmental review timelines lengthen near Caatinga preserves, adding up to 18 months of paperwork. Municipalities require proof of closed-loop systems achieving an IT load of under 0.2 L per kWh, pushing operators toward dielectric-fluid immersion and adiabatic walls. Water reuse projects tap sewage effluent; however, pipeline right-of-way costs are high in peri-urban zones. Stringent permitting tilts investment back toward São Paulo, where reclaimed-water infrastructure already serves semiconductor fabs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Data Center Type: Cloud hyperscale dominance meets agile colocation expansion

Cloud platforms controlled 55.10% of the Brazilian artificial intelligence data center market in 2025, driven by multi-availability-zone builds from AWS, Microsoft, and Google that underpin domestic sovereign cloud regions. These firms pre-lease entire campuses, enabling 200 MW pipelines that scale GPU clusters for large language model training. Capital intensity is mitigated through green debentures linked to rooftop solar arrays and on-site fuel cell pilots. Colocation providers, although smaller, post a 18.76% CAGR as enterprises adopt hybrid cloud, housing sensitive datasets in Tier III cages while bursting analytics to public regions.

Colocation incumbents like Scala interconnect their AI City campus to regional points-of-presence, offering 400 GbE cross-connects bundled with managed Kubernetes. Elea integrates liquid-cooling coolant distribution units, accommodating 100 kW racks for inference as-a-service startups. Edge specialists deploy 1 MW containers beside 5G base-band hotels, supporting media transcoding and multiplayer gaming. Enterprise on-premises nodes persist where latency-sensitive trading or proprietary ML models require ultra-low jitter. This mix sustains steady demand, ensuring the Brazil artificial intelligence data center market retains healthy diversification across service models.

By Component: Hardware acceleration reshapes investment priorities

Software stacks retained 45.25% revenue share in 2025, reflecting Brazil’s deep bench of AI developers building language localization models for Portuguese applications. However, hardware outlays now rise at a 19.05% CAGR as tenants install rack-scale systems that integrate HBM3 GPUs, silicon photonics interposers, and 800 GbE switching fabrics. Equipment import-tax exemptions lower landed costs by almost 12%, tilting budgets toward accelerated compute versus CPU-centric legacy nodes.

Cooling retrofits dominate capex; direct-to-chip water loops cut power usage effectiveness to 1.25, enabling sustainability certifications that unlock discounted green-loan rates. Storage spends escalate too, with tiered all-flash arrays supporting real-time inference and nearline HDD vaults archiving petabytes of sensor data from agribusiness deployments. Managed-services revenue grows as enterprises outsource model-ops, compliance, and patching to local integrators, yet its share remains modest relative to physical assets. This pivot confirms that the expansion of the Brazil artificial intelligence data center market size hinges on continuous silicon innovation and efficient thermal design.

By Tier Standard: Balancing uptime with time-to-market

Tier IV halls accounted for 60.92% of the Brazilian artificial intelligence data center market size in 2025, driven by financial institutions and government clouds that demand 2N+1 redundancy and 99.995% availability. Multiple diesel farms, dual utility feeds, and concurrent maintainability remain non-negotiable for mission-critical workloads such as instant-payment clearing and real-time risk analytics. Even so, Tier III projects deliver faster commissioning cycles, driving an 18.35% CAGR as AI startups accept limited downtime in exchange for price advantages.

Modular Tier III pods can be deployed within nine months on brownfield industrial sites, utilizing pre-fabricated switchgear skids and rooftop evaporative coolers. Operator playbooks incorporate cloud-native failover to other availability zones, mitigating risk from single-site outages. Brazilian standard NBR 16665 harmonizes cabling and grounding best practices, ensuring consistency regardless of tier. Over time, some Tier IV campuses convert unused 2N capacity into renewable-backed grid services, earning ancillary revenue and offsetting rising electricity tariffs. This evolution signals a nuanced risk-reward calculus that keeps the Brazil artificial intelligence data center market adaptive.

By End-User Industry: Digital incumbents widen AI spending gap

IT and ITES firms commanded 33.45% of the revenue in 2025, reflecting a heavy reliance on AI for software QA, conversational support, and DevOps automation. System integrators host training sandboxes alongside client-specific inference nodes, often within the same rack, to avoid data egress fees. Internet and Digital Media companies record the highest 19.62% CAGR thanks to recommendation engines driving video engagement and real-time language dubbing for e-sports streams.

Banks embed GPU clusters inside core transaction hubs, meeting strict security while harnessing deep-learning fraud models that scan millions of card swipes per second. Healthcare providers use cloud-based radiology inference, sending de-identified CT images to São Paulo inference farms that return triage flags in under two minutes. Manufacturers integrate machine-vision QC on assembly lines, with edge servers inside plant rooms syncing to central model repositories overnight. Government ministries are pursuing sovereign AI clouds for citizen services chatbots, further diversifying offtake. Jointly, these sectors ensure the Brazil artificial intelligence data center market maintains broad, resilient demand across economic cycles.

Geography Analysis

São Paulo hosts roughly 80% of the installed capacity, totaling 427.5 MW across the Barueri, Hortolândia, and Vinhedo clusters, owing to mature fiber rings, an abundance of talent, and proximity to national headquarters. Land prices are inching upward, so hyperscalers are acquiring outlying parcels in Sorocaba and Campinas, pairing low-cost acreage with 138 kV utility feeders. São Paulo state legislation fast-tracks environmental approvals for brownfield conversions, shortening lead times by nearly four months.

Rio de Janeiro ranks as the top secondary hub at 61 MW, leveraging 16 undersea cable landings and a robust utility grid that incorporates LNG-fired peakers for voltage stability. DE-CIX’s local internet exchange attracts content platforms seeking low-hop European peering, anchoring demand for multi-tenant halls in the downtown area. Edge builds in Niterói and Duque de Caxias service oil-and-gas analytics, streaming seismic data from offshore rigs to on-shore GPU accelerators.

The rest of Brazil encompasses Fortaleza’s carrier hotels, Porto Alegre’s southern manufacturing corridor, and interior agribusiness clusters. Fortaleza enjoys 17 subsea links and free-trade zone incentives, which cut import duties on chillers and switchgear. Porto Alegre benefits from a cooler climate, allowing for economizer-mode cooling for up to 2,200 hours per year. Mato Grosso sees 500 kW edge containers integrated with private-LTE farmlands, reducing latency for irrigation AI loops. Collectively, these diversifying nodes extend the reach of the Brazil artificial intelligence data center market and mitigate single-region concentration risks.

Coverage of the artificial intelligence (ai) data center market by Mordor Intelligence spans a wide geographic footprint, with regional analysis available for North America, South America, and Europe, alongside detailed country-level intelligence for Canada, Chile, Spain, United States, India, and United Arab Emirates, each shaped by local operating conditions.

Competitive Landscape

The Brazil artificial intelligence data center market features a moderate concentration, with the top five operators accounting for roughly 68% of the built-out IT load, leaving room for niche specialists. Equinix retains a lead through Network Edge services and over 400 connectivity partners, while Ascenty leverages Digital Realty’s global fabric for cross-border workloads. Scala’s AI City campus delivers water-side economization and 100 kW racks that appeal to foundation-model startups. New entrants such as 247 Data Centers adopt sale-leaseback financing, monetizing completed halls and recycling capital into land banking near future submarine-cable zones.

Competition increasingly revolves around sustainability. Operators sign 15-year solar and wind PPAs, add onsite fuel-cell pilots, and publish hourly carbon tracking dashboards to satisfy hyperscalers’ 24/7 matching requirements. Cooling innovation serves as a further differentiation; Elea deploys dual-phase immersion baths, achieving a density of 1,200 W per U, whereas Serpro’s government cloud attains a PUE of 1.4 via chilled-water aisles powered by reclaimed effluent.

Strategic moves underscore this rivalry. AWS committed USD 1.8 billion through 2034 for additional availability zones, stipulating 100% renewable coverage from day one. Microsoft opened paired builds in Hortolândia and Sumaré, gaining redundancy within a 50 km radius. Pátria’s USD 1 billion Omnia fund aggregates fiber routes with edge pods, offering bundled dark-fiber plus colocation contracts to OTT video clients. Collectively, these actions sustain a dynamic yet disciplined environment that propels the Brazil artificial intelligence data center market forward.

Brazil Artificial Intelligence (AI) Data Center Industry Leaders

Equinix Inc.

Ascenty LLC (Digital Realty)

Scala Data Centers S.A.

Odata Brasil S.A. (Aligned)

Microsoft Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Brasscom projects a USD 11.4 billion data-center investment by 2026, citing renewable leadership and favorable tax policy.

- September 2025: Dataspots unveils expansion plans while withholding site locations, signaling continued investor appetite despite grid constraints.

- June 2025: Government working group advises mandatory 100% clean-energy sourcing, prompting operators to accelerate renewable PPAs.

- May 2025: Pátria launches USD 1 billion Omnia platform to fund regional digital infrastructure, including hyperscale campuses.

- May 2025: ONS grants first Ceará grid connections for large data centers, unlocking the state’s technology corridor.

- May 2025: Communications Ministry rolls out National Submarine Cable Policy to diversify landing sites nationwide.

Brazil Artificial Intelligence (AI) Data Center Market Report Scope

The research encompasses the full spectrum of AI applications in data centers, covering hyperscale, colocation, enterprise, and edge facilities. The analysis is segmented by component, distinguishing between hardware and software. Hardware considerations include power, cooling, networking, IT equipment, and more. Software technologies under scrutiny encompass machine learning, deep learning, natural language processing, and computer vision. The study also evaluates the geographical distribution of these applications.

Additionally, it assesses AI's influence on sustainability and carbon neutrality objectives. A comprehensive competitive landscape is presented, detailing market players engaged in AI-supportive infrastructure, encompassing both hardware and software utilized across various AI data center types. Market size is calculated in terms of revenue generated by products and solutions providers in the market, and forecasts are presented in USD Billion for each segment.

| Cloud Service Providers |

| Colocation Data Centers |

| Enterprise / On-Premises / Edge |

| Hardware | Power Infrastructure |

| Cooling Infrastructure | |

| IT Equipment | |

| Racks and Other Hardware | |

| Software Technology | Machine Learning |

| Deep Learning | |

| Natural Language Processing | |

| Computer Vision | |

| Services | Managed Services |

| Professional Services |

| Tier III |

| Tier IV |

| IT and ITES |

| Internet and Digital Media |

| Telecom Operators |

| Banking, Financial Services and Insurance (BFSI) |

| Healthcare and Life Sciences |

| Manufacturing and Industrial IoT |

| Government and Defense |

| By Data Center Type | Cloud Service Providers | |

| Colocation Data Centers | ||

| Enterprise / On-Premises / Edge | ||

| By Component | Hardware | Power Infrastructure |

| Cooling Infrastructure | ||

| IT Equipment | ||

| Racks and Other Hardware | ||

| Software Technology | Machine Learning | |

| Deep Learning | ||

| Natural Language Processing | ||

| Computer Vision | ||

| Services | Managed Services | |

| Professional Services | ||

| By Tier Standard | Tier III | |

| Tier IV | ||

| By End-User Industry | IT and ITES | |

| Internet and Digital Media | ||

| Telecom Operators | ||

| Banking, Financial Services and Insurance (BFSI) | ||

| Healthcare and Life Sciences | ||

| Manufacturing and Industrial IoT | ||

| Government and Defense | ||

Key Questions Answered in the Report

What 2026 value does the Brazil artificial intelligence data center market reach?

The sector is valued at USD 0.64 billion in 2026.

How fast will capacity grow through 2031?

Market value is projected to expand to USD 1.43 billion by 2031 at a 17.27% CAGR.

Which segment shows the highest growth rate?

Colocation facilities record the fastest 18.76% CAGR by 2031.

Why is São Paulo the leading hub?

São Paulo offers robust fiber density, reliable power, skilled labor and proximity to corporate headquarters.

What main risk threatens new builds?

Transmission grid bottlenecks and electricity cost spikes present the most immediate challenges.

How are operators lowering environmental impact?

They adopt 15-year renewable PPAs, liquid-cooling systems and reclaimed-water use to cut carbon and water footprints.

Page last updated on: