Germany Artificial Intelligence (AI) Data Center Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

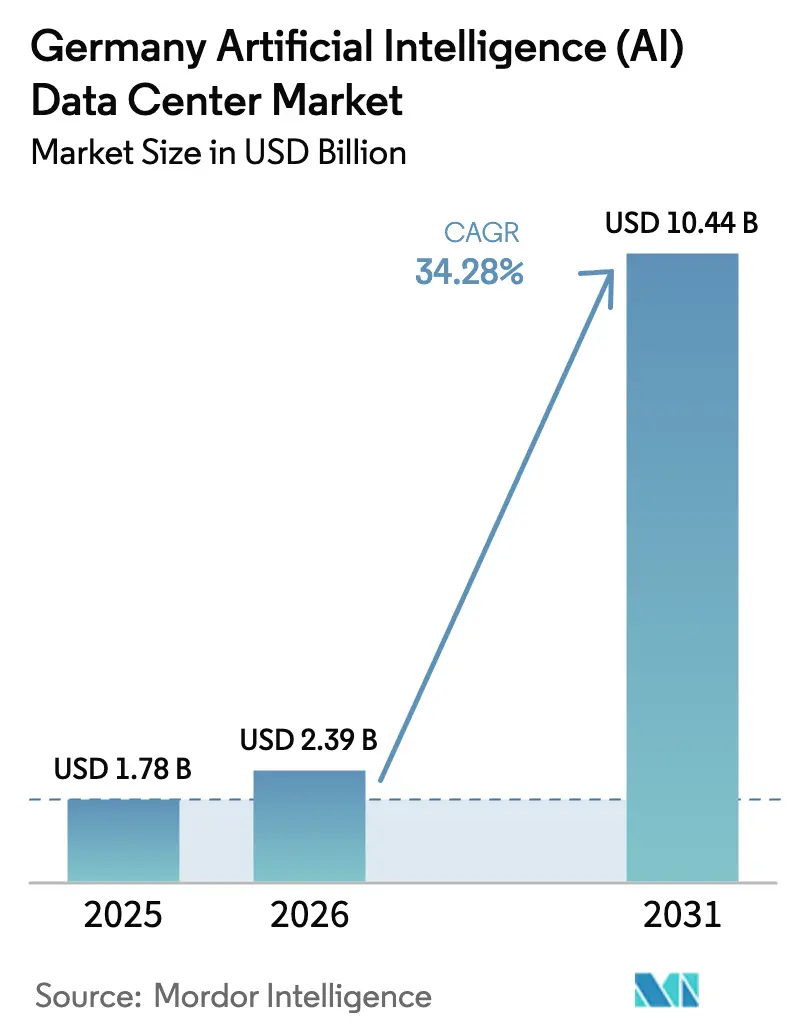

| Base Year Market Size (2025) | USD 1.78 Billion |

| Market Size (2026) | USD 2.39 Billion |

| Market Size (2031) | USD 10.44 Billion |

| Growth Rate (2026 - 2031) | 34.28% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany Artificial Intelligence (AI) Data Center Market Analysis by Mordor Intelligence

The Germany artificial intelligence data center market size was valued at USD 1.78 billion in 2025 and estimated to grow from USD 2.39 billion in 2026 to reach USD 10.44 billion by 2031, at a CAGR of 34.28% during the forecast period (2026-2031). Growing sovereign-cloud demand, rapid GPU cluster rollouts in Frankfurt-Rhein-Main, and favorable incentives embedded in the Energy Efficiency Act collectively propel the German artificial intelligence data center market. Meanwhile, energy-efficient cooling, district heat monetization, and renewable power purchase agreements are reshaping cost structures. Leading hyperscalers continue to invest at a multi-billion-euro scale; however, sovereign-cloud and GAIA-X frameworks divert a growing share of domestic AI workloads toward European providers that can demonstrate data-residency compliance. Hardware densification, combined with immersion cooling adoption, lifts power densities above 75 kW per rack, forcing operators to secure low-carbon electricity and implement advanced thermal management to maintain a PUE at or below 1.2. At the same time, grid congestion between the wind-rich North and industrial South complicates site selection, encouraging distributed builds that combine training clusters proximate to renewable energy sources with edge nodes embedded within automotive and manufacturing corridors.

Key Report Takeaways

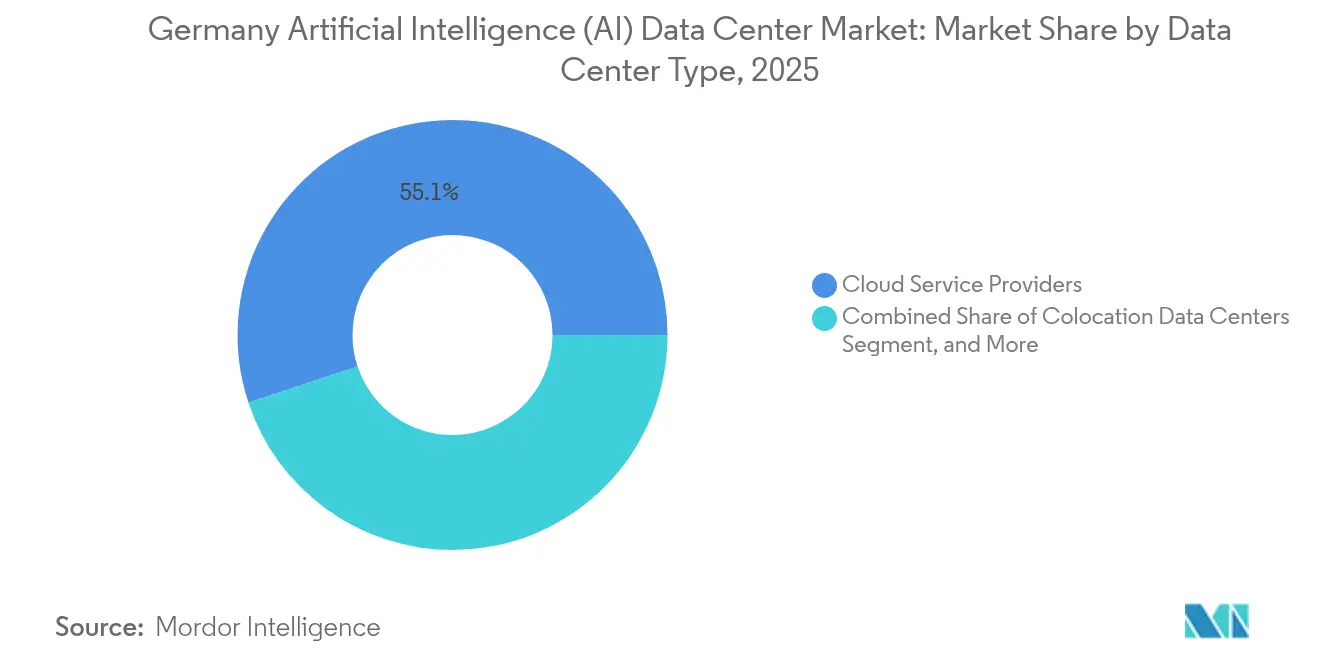

- By data center type, cloud service providers led with 55.10% revenue share of the German artificial intelligence data center market in 2025, while colocation data centers are projected to expand at a 36.02% CAGR through 2031.

- By component, software technologies accounted for 45.10% of the German artificial intelligence data center market share in 2025, while hardware is projected to advance at a 35.42% CAGR through 2031.

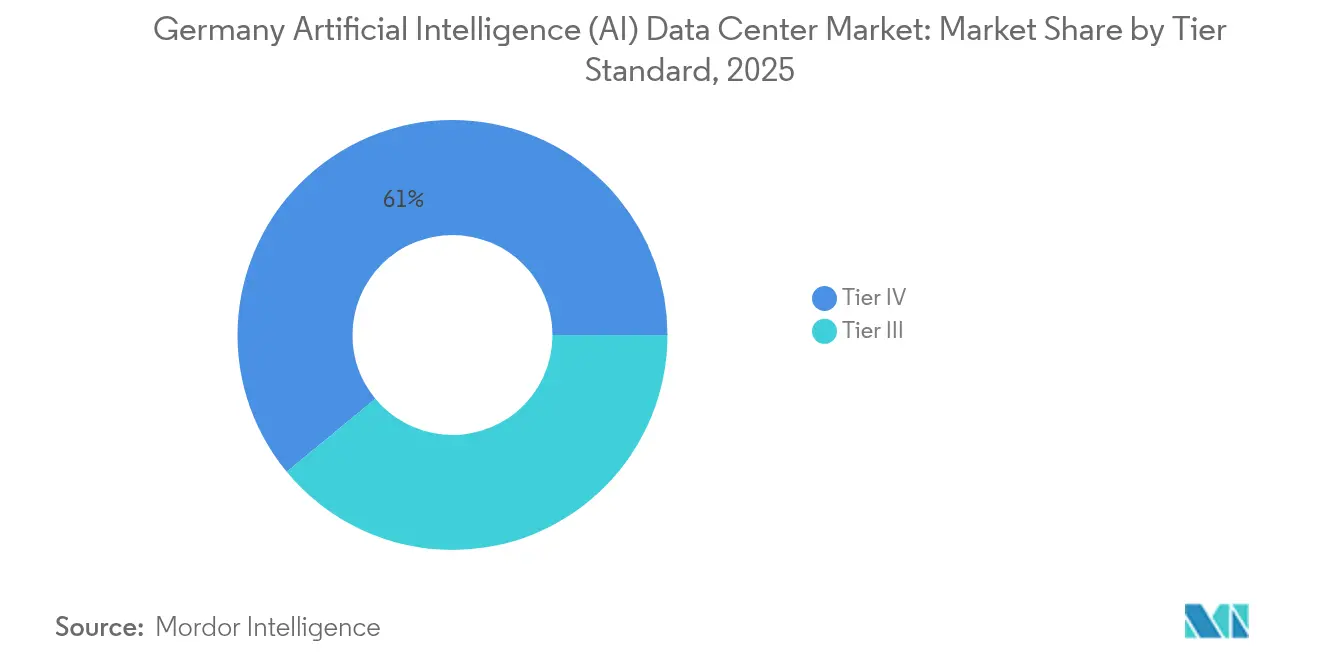

- By tier standard, tier IV facilities captured 60.98% share of the German artificial intelligence data center market size in 2025, whereas tier III is set to grow at 36.95% CAGR to 2031.

- By end-user vertical, IT and ITES accounted for a 33.40% share of the German artificial intelligence data center market in 2025, while the internet and digital media sector is forecast to grow at the fastest rate, with a 35.61% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

The contribution of Germany may read different when placed against the full pool of global outputs. The worldwide artificial intelligence (ai) data center market shares by Mordor Intelligence reflect that proportional balance.

Germany Artificial Intelligence (AI) Data Center Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Frankfurt-Rhein-Main GPU-dense hyperscale expansion | +8.2% | Frankfurt-Rhein-Main, Hesse | Medium term (2-4 years) |

| Surplus wind power enables carbon-free AI compute | +6.8% | Schleswig-Holstein, Lower Saxony | Long term (≥ 4 years) |

| Sovereign-cloud and GAIA-X-driven domestic AI loads | +7.5% | National with clusters in Frankfurt, Munich, Berlin | Medium term (2-4 years) |

| Automotive and Industry 4.0 digital-twin demand | +5.9% | Baden-Württemberg, Bavaria, NRW | Short term (≤ 2 years) |

| District-heat monetization for high-density clusters | +4.1% | Berlin, Munich, Hamburg | Long term (≥ 4 years) |

| Exascale public-HPC spill-over to commercial AI clouds | +3.5% | Jülich, Munich, Dresden | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Frankfurt-Rhein-Main GPU-Dense Hyperscale Expansion

Frankfurt is consolidating its position as Europe’s AI compute nexus as hyperscale operators deploy GPU-dense campuses engineered for sub-10 ms latency to major EU capitals.[1]CyrusOne, “Frankfurt expansion announcement,” cyrusone.com EUR 1.2 billion of new capacity from players such as CyrusOne and STACK deepens the region’s network externalities, drawing fintech and algorithmic-trading workloads that require proximity to the European Central Bank. Secondary cities Hanau and Offenbach benefit from land-price arbitrage while preserving fiber proximity, thereby extending the compute halo around Frankfurt. Regulatory certainty for financial AI use cases further cements investor confidence, accelerating speculative builds. Each additional AI-ready facility raises the density of interconnect providers, nudging total addressable demand upward as enterprises co-locate complementary functions.

Surplus Wind Power Enables Carbon-Free AI Compute

Northern Germany’s wind surplus routinely forces curtailment during high-generation intervals; GPU training farms absorb this oversupply, thereby lowering marginal electricity costs and reducing Scope 2 emissions under the EU CSRD.[2]Northern Data, “Renewable energy partnership,” northerndata.de Dynamic PPAs allow operators to schedule intensive model training jobs when wind peaks, while inference clusters remain closer to latency-sensitive users in the south. Northern Data’s Schleswig-Holstein campus illustrates how predictable offtake commitments stabilize renewable revenue and unlock price concessions that improve AI workload economics. Grid managers gain a buffer against volatility, creating political goodwill that accelerates permit approvals for new data center interconnects as more operators replicate the model, leading to increased renewable energy capture rates and advancement of Germany’s 80% green power target for 2030.

Sovereign-Cloud and GAIA-X-Driven Domestic AI Loads

GAIA-X federations move from pilot to production, steering regulated workloads toward providers that can prove compliance with BSI C5 and GDPR Article 44.[3]Federal Office for Information Security, “Cloud Computing Certification,” bsi.bund.de Automotive OEMs stipulate local model training to safeguard intellectual property, thereby expanding demand for redundant in-country clusters. Financial institutions adopt sovereign clouds to comply with BaFin supervision, accepting price premiums in exchange for risk mitigation. Duplicate deployments inflate capacity requirements because mirrored regions inside Germany cannot lean on distant EU sites for failover. Procurement teams are increasingly embedding data-residency clauses in tenders, raising entry barriers for non-compliant vendors and broadening the German artificial intelligence data center market.

Automotive and Industry 4.0 Digital-Twin Demand

BMW’s virtual factory streams over 500 TB of daily sensor data into AI simulations that fine-tune production lines in real time. Industry 4.0 projects under Manufacturing-X require hybrid clouds that connect edge nodes to centralized GPU training clusters, resulting in incremental rack demand both within plants and at regional hubs such as Stuttgart and Munich. IEC 62443 cybersecurity mandates are pushing enterprises toward certified facilities with micro-segmented networks, boosting the preference for AI-optimized colocation. Tier IV reliability is non-negotiable for mission-critical plant controls, whereas rapid-iteration twin models can run on lower-tier capacity, producing a dual-track infrastructure appetite. Early ROI proofs in the automotive industry spur replication across mechanical engineering, pharmaceuticals, and consumer goods manufacturing.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| BImSchG Noise and Heat-Emission Limits | -4.3% | Dense urban areas (Frankfurt, Munich, Berlin, Hamburg) | Short term (≤ 2 years) |

| North–South Grid Congestion | -3.7% | National, particularly affecting renewable energy integration | Medium term (2-4 years) |

| Urban Land Scarcity in FLAP-D Hubs | -2.8% | Frankfurt, London, Amsterdam, Paris, Dublin corridor markets | Medium term (2-4 years) |

| Chemical-Safety Permitting for Immersion Fluids | -1.9% | National, with stricter enforcement in industrial zones | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

BImSchG Noise and Heat-Emission Limits

Germany’s Federal Immission Control Act caps nighttime acoustic output at 35 dB(A) in mixed-use zones, requiring the installation of expensive acoustic louvers, buried chillers, or off-peak operation. GPU racks triple the heat density of conventional servers, so immersion cooling, an otherwise efficient option, faces additional permitting requirements under chemical regulations, potentially delaying go-lives by up to 12 months. Compliance overhead tilts the field toward large operators with specialized environmental teams, squeezing smaller entrants and nudging sector consolidation. CapEx creep of 15-20% raises breakeven leasing rates, slowing take-up among cost-sensitive tenants. Some projects pivot to suburban parcels where decibel thresholds are higher, but this increases fiber backhaul costs.

North–South Grid Congestion

Delayed SuedLink and SuedOstLink transmission lines keep renewable surpluses stranded in the North, while industrial clusters in Bavaria and Baden-Württemberg pay congestion surcharges of EUR 20-40 per MWh. AI-training sites located near wind farms enjoy lower energy costs but incur latency penalties when serving users in southern metropolitan areas. Conversely, inference nodes situated near demand centers face higher electricity tariffs that erode price competitiveness compared to neighboring EU markets, such as the Netherlands. Until 400 kV corridors go live in 2028, operators deploy mixed strategies: northern campuses for batch-training jobs and edge or colocation nodes in the South for real-time workloads. The split architecture increases operational complexity, tempering the growth of the German artificial intelligence data center market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Data Center Type: Cloud Dominance Faces Colocation Challenge

Cloud Service Providers are expected to command 55.10% of the German artificial intelligence data center market size in 2025, as hyperscalers leverage scale economies, proprietary AI services, and integrated global networks. Yet, colocation providers post the fastest growth of 36.02% because enterprises must reconcile data-sovereignty mandates with scalable GPU access. Banks, automakers, and telecom operators lease dedicated cages within AI-ready halls to maintain control over encryption keys while tapping burst capacity via cloud interconnects. This hybrid posture boosts cross-connect revenue and prompts multi-tenant operators to install liquid-cooling corridors and 48-inch-deep racks.

Colocation’s ascent also stems from Tier III edge builds in manufacturing corridors where Industry 4.0 sensors generate millisecond-sensitive traffic. Enterprises position inference clusters in colocation huts attached to 5G macro towers, shortening loop times for predictive-maintenance algorithms. Cloud incumbents counter by opening smaller availability zones in Düsseldorf and Leipzig, blurring lines between hyperscale and edge. Enterprise and on-premises facilities remain niche but vital for microsecond-latency trading and real-time factory controls. Their share declines in percentage terms, yet their absolute rack count grows as legacy halls retrofit for 30 kW racks.

By Component: Software Leadership Meets Hardware Acceleration

Software technologies held 45.10% of the German artificial intelligence data center market share in 2025, reflecting the dominance of AI orchestration stacks, MLOps pipelines, and federated learning frameworks. However, hardware spending grows at a 35.42% CAGR as every new GPU generation increases per-rack wattage, demanding upgraded busbars, switchgear, and dielectric fluid-based cooling. The German artificial intelligence data center market size is closely tied to hardware, thus surging whenever NVIDIA, AMD, or Intel release new accelerator SKUs accompanied by higher price points and power envelopes.

Managed services form the connective tissue between software and hardware; operators bundle DevOps, compliance dashboards, and SOC-2 audits with bare-metal GPU nodes, boosting ARPU and reducing churn. Professional services revenue spikes around migration projects from on-premises to sovereign cloud, integrating Kubernetes clusters with HSM-backed key management that is compliant with BSI C5. Competitive differentiation centers around vertically integrated offers, turnkey racks with pre-loaded AI frameworks, and performance SLAs that appeal to mid-market firms lacking in-house AI Operations talent.

By Tier Standard: Reliability Premium Drives Tier IV Dominance

Tier IV sites deliver 99.995% availability through 2N+1 redundancy and on-site substation loops, qualities prized by fintech and automotive OEMs operating zero-defect AI workflows. Consequently, these sites capture 60.98% of the German artificial intelligence data center market share in 2025, despite 20-30% higher rental premiums. Uptime-linked penalties embedded into OEM supply contracts reinforce the Tier IV bias.

Tier III growth, at a 36.95% CAGR, mirrors the proliferation of digital-twin pilots and AI-enabled quality-inspection workloads that can tolerate brief outages. Operators deploy battery-only UPS topologies and shared generator yards to cut capex, passing savings to tenants experimenting with edge AI. Demand for Tier II capacity remains marginal, generally limited to cold-storage DR nodes or AI training jobs that frequently checkpoint. The bifurcated pattern underscores a maturing Germany artificial intelligence data center market in which mission-critical lines pay for high resilience, while innovation workloads chase the lowest cost per FLOP.

By End-User Industry: Enterprise IT Leads Digital Media Surge

IT and ITES sectors maintain a 33.40% revenue share thanks to enterprise digitization projects that embed AI into ERP, CRM, and cybersecurity suites. These firms orchestrate multi-cloud footprints to optimize latency and compliance, thereby driving steady colocation rack uptake. Simultaneously, Internet and Digital Media bookings accelerate at a 35.61% CAGR as streaming platforms implement real-time recommendation engines and generative AI content assembly lines. Their throughput-heavy profiles persuade operators to reserve contiguous, high-density halls linked directly to DE-CIX Frankfurt, thereby trimming the hop count for consumers.

BFSI workloads grow on the back of PSD2-driven open-banking APIs and algorithmic fraud detection that necessitate sub-5 ms round-trip latency. Automotive digital twins continue to occupy large contiguous white-space blocks near Munich and Stuttgart, coupling GPU training labs with on-site battery farms to mitigate grid fluctuations. Healthcare, life sciences, and public-sector demand clusters are centered around Berlin and Bonn, leveraging sovereign-cloud certifications to train LLMs on patient or citizen records without violating the GDPR.

Geography Analysis

Frankfurt-Rhein-Main hosts approximately 39.60% of the national AI rack capacity, largely due to DE-CIX’s presence, pan-European fiber convergence, and proximity to the financial sector. GPU-dense builds, such as Equinix FR6 and Digital Realty FRA42, cement the locus; however, land scarcity and BImSchG noise curbs nudge spill-over into Hanau and Offenbach. Hessian energy subsidies for heat reuse further tip economics toward the metro.

Munich ranks second due to BMW, Audi, Infineon, and the Technical University of Munich, which drive AI twin simulations that require local training capacity. The city’s 100% renewable utility, Stadtwerke München, supplies competitively priced green power, appealing to corporates chasing CSRD metrics. Bavaria’s subsidy scheme for high-tech expansion adds EUR 200 million in grants through 2027, encouraging speculative land banking in Unterföhring and Unterschleißheim.

Berlin’s thriving startup scene and federal government presence fuel demand for agile, modular nodes that can spin up GPU pods within hours. Operators retrofit telecom switch sites into micro data centers, colocated with 5G edge, to support generative AI development and testing workloads. Hamburg leverages port logistics by deploying AI to orchestrate vessel traffic and warehouse robotics, thereby requiring inference clusters close to harbor operations. Northern states capture energy-intensive training farms that exploit wind surpluses, while southern industrial belts concentrate low-latency inference nodes. Upcoming federal gigabit corridors will bridge latency gaps, catalyzing further geographic dispersion before 2030.

The artificial intelligence (ai) data center market is analyzed by Mordor Intelligence across multiple other geographies, with in-depth regional assessments available for Europe, Middle East and Africa, and North America. This is complemented by country-specific insights for United Kingdom, Spain, Saudi Arabia, United States, Malaysia, and Indonesia, reflecting various localized market behavior and policy environments' coverage.

Competitive Landscape

The German artificial intelligence data center market displays moderate fragmentation. AWS allocates EUR 7.8 billion for Brandenburg, including 150 MW of liquid-cooled GPU halls that tap direct-wire wind farms.[4]Financial Times, “AWS Germany investment announcement,” ft.com Microsoft earmarks EUR 3.2 billion for Rhineland builds, partnering with SAP on co-developed AI clusters. Google scales its Hanau zone with geothermal-assisted cooling under trial. European challengers OVHcloud and Deutsche Telekom market sovereign-cloud SKUs carrying BSI C5 labels, targeting regulated workloads.

Specialists Northern Data and CloudandHeat pioneer immersion-cooled HPC clusters with PUE below 1.1 and waste-heat recovery proven at scale. They differentiate via carbon-adjusted SLAs, monetizing heat to district networks. Hardware ecosystem players Rittal and Schneider Electric are racing to patent modular coolant manifolds and AI-optimized busbars, embedding predictive maintenance sensors that flag voltage sag before thermal runaway occurs.

Strategic alliances emerge: Vantage pairs with RWE on 100 MW green power facilities; Equinix teams with Deutsche Börse to offer proximity hosting to algorithmic traders; STACK partners with municipalities to underwrite heat pipes serving 5,000 homes. Competitive intensity thus revolves around carbon credentials, cooling IP, and regulatory badges rather than solely on raw rack capacity.

Germany Artificial Intelligence (AI) Data Center Industry Leaders

NVIDIA Corporation

Intel Corporation

Advanced Micro Devices, Inc.

Arm Ltd.

Cisco Systems, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: AWS expanded its Brandenburg campus by EUR 2.1 billion, adding 150 MW liquid-cooled AI capacity wired to wind farms.

- February 2025: Microsoft and SAP launched joint AI clusters in the Rhineland to power RISE with SAP for German clients.

- February 2025: CloudandHeat secured ISO 50001 certification for its Dresden immersion-cooled facility, achieving 40% energy efficiency gains.

- January 2025: Digital Realty acquired 45 hectares in Frankfurt-Höchst for EUR 180 million, with plans for a 200 MW GPU megacampus.

- January 2025: Rittal unveiled modular coolant loops with predictive-failure analytics aimed at German operators.

Germany Artificial Intelligence (AI) Data Center Market Report Scope

The research encompasses the full spectrum of AI applications in data centers, covering hyperscale, colocation, enterprise, and edge facilities. The analysis is segmented by component, distinguishing between hardware and software. Hardware considerations include power, cooling, networking, IT equipment, and more. Software technologies under scrutiny encompass machine learning, deep learning, natural language processing, and computer vision.

The study also evaluates the geographical distribution of these applications. Additionally, it assesses AI's influence on sustainability and carbon neutrality objectives. A comprehensive competitive landscape is presented, detailing market players engaged in AI-supportive infrastructure, encompassing both hardware and software utilized across various AI data center types. Market size is calculated in terms of revenue generated by products and solutions providers in the market and forecasts are presented in USD Billion for each segment.

| Cloud Service Providers |

| Colocation Data Centers |

| Enterprise / On-Premises / Edge |

| Hardware | Power Infrastructure |

| Cooling Infrastructure | |

| IT Equipment | |

| Racks and Other Hardware | |

| Software Technology | Machine Learning |

| Deep Learning | |

| Natural Language Processing | |

| Computer Vision | |

| Services | Managed Services |

| Professional Services |

| Tier III |

| Tier IV |

| IT and ITES |

| Internet and Digital Media |

| Telecom Operators |

| Banking, Financial Services and Insurance (BFSI) |

| Healthcare and Life Sciences |

| Manufacturing and Industrial IoT |

| Government and Defense |

| By Data Center Type | Cloud Service Providers | |

| Colocation Data Centers | ||

| Enterprise / On-Premises / Edge | ||

| By Component | Hardware | Power Infrastructure |

| Cooling Infrastructure | ||

| IT Equipment | ||

| Racks and Other Hardware | ||

| Software Technology | Machine Learning | |

| Deep Learning | ||

| Natural Language Processing | ||

| Computer Vision | ||

| Services | Managed Services | |

| Professional Services | ||

| By Tier Standard | Tier III | |

| Tier IV | ||

| By End-user Industry | IT and ITES | |

| Internet and Digital Media | ||

| Telecom Operators | ||

| Banking, Financial Services and Insurance (BFSI) | ||

| Healthcare and Life Sciences | ||

| Manufacturing and Industrial IoT | ||

| Government and Defense | ||

Key Questions Answered in the Report

How fast is Germany’s AI data-center space expanding?

Capacity value grows from USD 2.39 billion in 2026 to USD 10.44 billion by 2031, posting a 34.28% CAGR driven by GPU deployments and sovereign-cloud mandates.

Which operators dominate German AI data-center spending?

Cloud Service Providers hold 55.10% revenue share in 2025, led by AWS, Microsoft, and Google, although colocation vendors grow fastest at 36.02% CAGR through 2031.

Why is Frankfurt central to German AI compute?

DE-CIX exchange density, financial-sector proximity, and multi-billion-euro GPU campuses make Frankfurt-Rhein-Main host about 39.60% of the nation’s AI rack footprint.

How do German regulations impact data-center design?

The Energy Efficiency Act enforces heat-reuse above 1 MW, while BImSchG imposes strict noise limits, collectively raising capex yet enabling thermal-revenue streams.

What cooling innovations are gaining traction?

Immersion and liquid-cooling corridors delivering PUE near 1.1 are spreading, with operators such as Northern Data and CloudandHeat pioneering large-scale deployments.

Which end-user vertical is growing quickest?

Internet and Digital Media workloads climb at 35.61% CAGR as streaming and real-time personalization engines require low-latency inference clusters across Germany.

Page last updated on: