Chile Artificial Intelligence (AI) Data Center Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

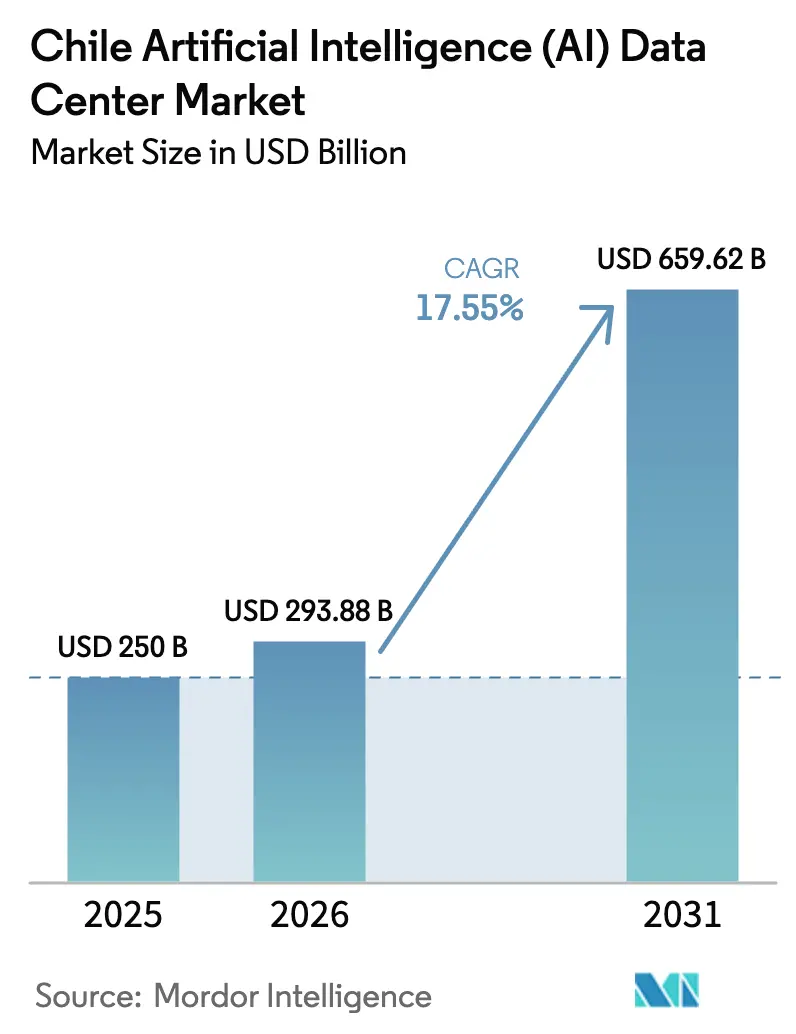

| Base Year Market Size (2025) | USD 250 Billion |

| Market Size (2026) | USD 293.88 Billion |

| Market Size (2031) | USD 659.62 Billion |

| Growth Rate (2026 - 2031) | 17.55% CAGR |

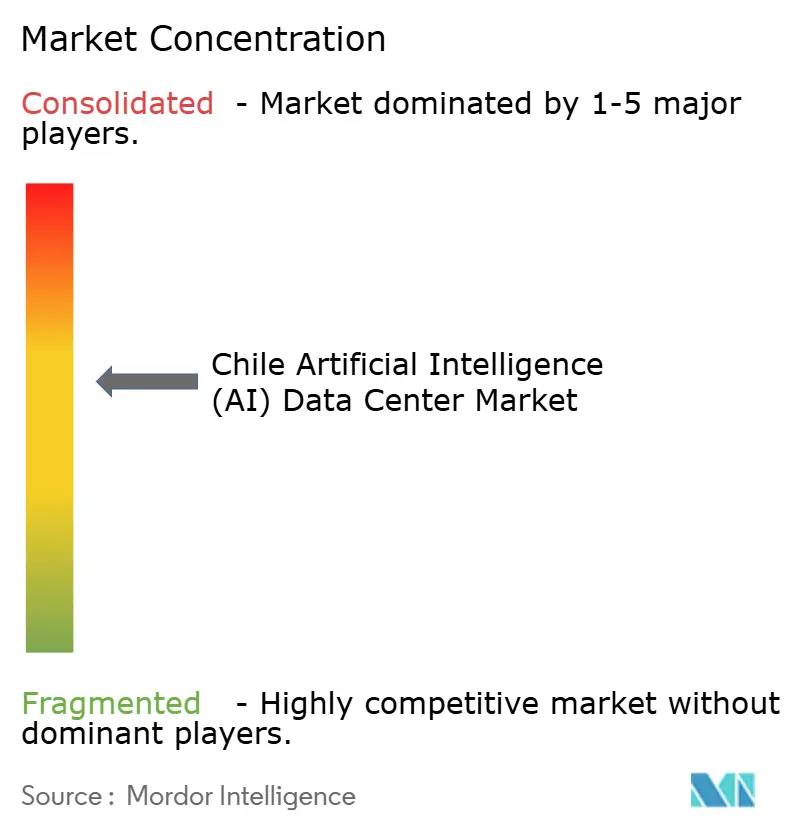

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Chile Artificial Intelligence (AI) Data Center Market Analysis by Mordor Intelligence

The Chile artificial intelligence data center market size is expected to grow from USD 250 million in 2025 to USD 293.88 million in 2026 and is forecast to reach USD 659.62 million by 2031 at 17.55% CAGR over 2026-2031. Continued hyperscaler capital inflows, the government’s USD 4 billion National Data Centers Plan, and Chile’s renewable-energy advantage are combining to accelerate project pipelines. Policy measures that reduce permitting times, combined with direct Asia-Pacific links via the Humboldt submarine cable, enhance Chile’s position as a low-latency hub for AI workloads. Investments in liquid-cooled halls, seismic-resilient designs, and 100% clean power procurement strengthen competitive moats, while headline risks around water availability and skilled labor shortages are prompting innovation in dry cooling and talent development programs. With cloud regions already live from Microsoft and Amazon, early-stage adopters are securing power and land, anticipating a second wave of demand as enterprises operationalize their generative AI roadmaps.

Key Report Takeaways

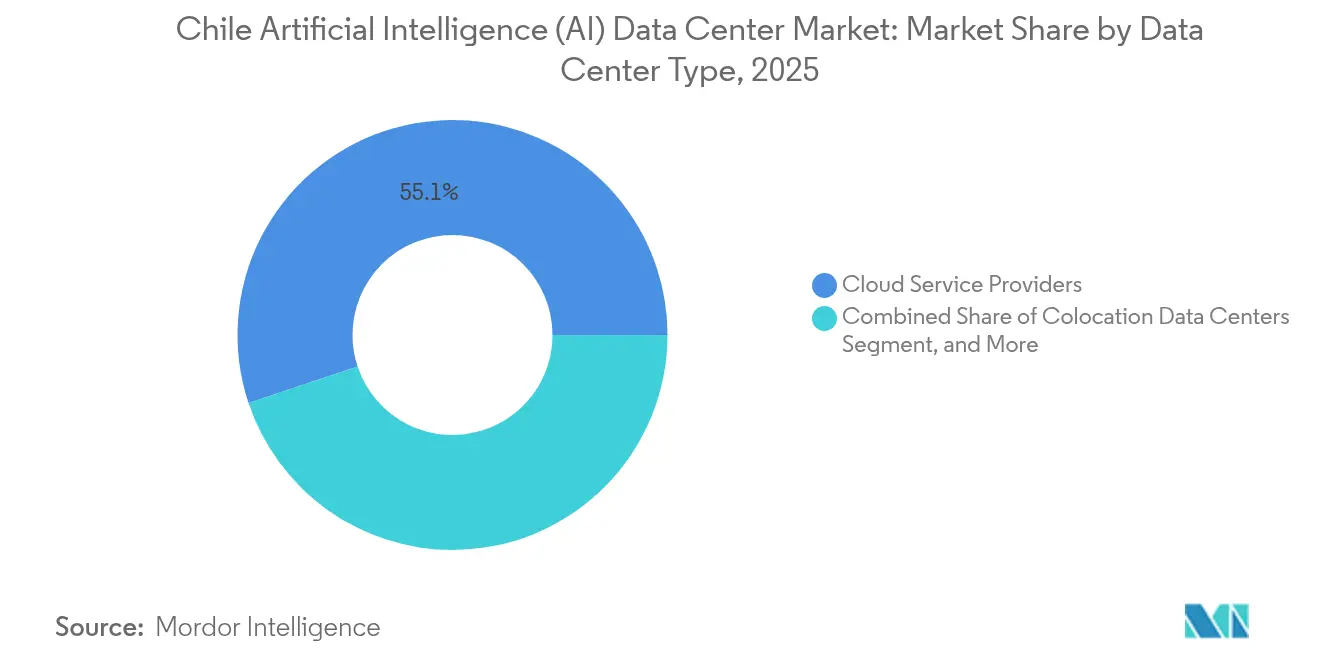

- By data center type, cloud service providers led with 55.12% of Chile's artificial intelligence data center market share in 2025, whereas colocation facilities are projected to expand at a 19.08% CAGR through 2031.

- By component, software accounted for 45.12% of the Chilean artificial intelligence data center market size in 2025, while hardware is forecast to grow at a 19.42% annual rate to 2031.

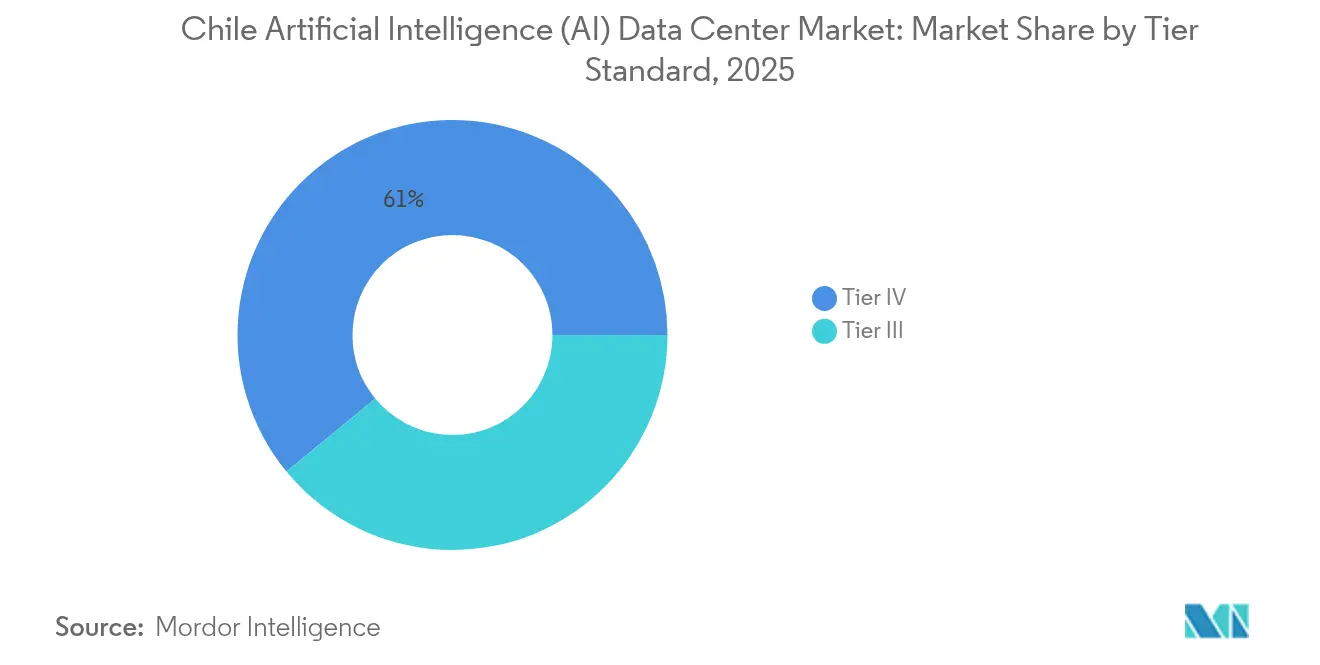

- By tier standard, Tier IV facilities held 60.95% share of the Chile artificial intelligence data center market size in 2025, whereas Tier III builds are advancing at an 18.61% CAGR.

- By end user, IT and ITES captured 33.15% of the Chile artificial intelligence data center market size in 2025, while internet and digital media workloads are scaling at a 20.02% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market participation spans countries and regions, making Chile competition one layer within a larger international field. In its global artificial intelligence (ai) data center industry statistics, Mordor Intelligence maps that multi-region structure.

Chile Artificial Intelligence (AI) Data Center Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing AI-driven compute demand | +4.2% | National, concentrated in Santiago and Quilicura | Medium term (2-4 years) |

| Expansion of cloud hyperscalers into Chile | +3.8% | Santiago Metropolitan Region | Short term (≤ 2 years) |

| Government digital transformation incentives | +2.9% | National, with priority to Antofagasta and Atacama | Long term (≥ 4 years) |

| Abundant renewable energy potential in Patagonia | +2.1% | Southern grid-connected regions | Long term (≥ 4 years) |

| Humboldt and other submarine cables lowering latency | +1.7% | Coastal landing points, Santiago hubs | Medium term (2-4 years) |

| Seismically resilient construction standards attracting investors | +1.4% | Earthquake-prone central belt | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing AI-driven compute demand

Chile reports that 64% of firms store more than 75% of data in the cloud, yet only 10% have executed over 40% of planned generative-AI projects, leaving a sizable capacity gap.[1]BNamericas Staff, “Datacenters, AI and education reform key to Chile's global competitiveness,” BNamericas, bnamericas.com Equinix’s 425-cabinet ST2 addition in April 2025, purpose-built for liquid-cooled GPUs, signals infrastructure-led growth outpacing application rollouts. Early entrants are therefore positioned to capture a disproportionate share as generative AI adoption accelerates. Rising compute density is also lifting power-draw requirements, prompting operators to secure large renewable-energy PPAs and redesign power distribution for 100 kW racks. The market’s trajectory reflects a virtuous circle: more AI deployments require more optimized halls, and those halls in turn make advanced AI economically feasible for enterprises.

Expansion of cloud hyperscalers into Chile

Amazon’s USD 4 billion and Microsoft’s USD 500 million rollouts establish multi-availability zones that meet locality and redundancy rules for regulated sectors.[2]Microsoft News Center, “Microsoft anuncia inversión de US$317 millones para establecer región de Azure en Chile,” microsoft.com Hyperscaler entry catalyzes the ecosystem by attracting fiber expansions, specialist contractors, and new colocation builds seeking to land spillover workloads. Scala’s USD 145.2 million Huechuraba campus and Cirion’s Santiago node highlight follow-on investments clustering near cloud zones. Local integrators such as TECfusions are partnering with developers to assemble 100 MW campuses, leveraging hyperscaler design templates and procurement volumes. As more regions go live, service-provider alliances deepen, stimulating domestic SaaS vendors targeting export markets.

Government digital transformation incentives

The 2025 economic growth pact pledges accelerated permitting windows and automatic tax credit eligibility for digital economy projects. Streamlined processes reduce schedule risk, a critical variable for investors facing multi-billion-dollar commitments. The state also assigns priority transmission-line upgrades to data-center corridors, ensuring renewable generation reaches load centers. Policy coordination among environmental, energy, and telecom agencies now occurs through a single-window mechanism, cutting red tape that previously deterred international operators. These measures reinforce Chile’s strategic agenda to become Latin America’s export base for AI-driven digital services.

Abundant renewable energy potential in Patagonia

Patagonia’s high-capacity factors for wind and solar enable 100% clean energy sourcing, as demonstrated by Microsoft’s Quilicura site, powered by AES Andes PPAs. Transmission projects, such as Kimal-Lo Aguirre, unlock surplus generation for data-center corridors, thereby mitigating curtailment risk. Operators combine grid power with on-site battery storage to manage intermittency, and some evaluate behind-the-meter hydrogen pilots as a backup generation source. Renewable abundance becomes strategic because AI workloads drive sharp power-density jumps; liquid-cooling pumps alone can add megawatts per hall. Facilities marketed as zero-carbon gain are being given procurement preference by cloud buyers with net-zero pledges.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High electricity prices in metropolitan zones | -2.3% | Santiago industrial belts | Short term (≤ 2 years) |

| Water scarcity challenges for liquid cooling | -1.8% | Central regions | Medium term (2-4 years) |

| Shortage of specialized AI and DC workforce | -1.5% | Nationwide metros | Long term (≥ 4 years) |

| Elevated capex for earthquake-resistant facilities | -1.2% | National high-seismic zones | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Water scarcity challenges for liquid cooling

The Supreme Court’s halt of Google’s Cerrillos build, which planned to draw 7.6 million L/day, underscores escalating scrutiny of industrial water use.[3]BNamericas Staff, “Google data center water-use dispute,” BNamericas, bnamericas.com Operators are now trialing adiabatic-free or air-cooled chillers, marketed by WIKA Chile, that reduce consumption by up to 90%. Some projects are situated outside water-stressed basins and connect to desalinated industrial water pipelines serving mining clusters. These strategies add cost and engineering complexity but are becoming prerequisites for environmental approvals.

Shortage of specialized AI and data-center workforce

OECD surveys show that cybersecurity and DC operations skills remain clustered in Santiago, leaving regional talent constrained. The Talento Digital program aims to target 50,000 new graduates by 2028, while Inacap’s didactic data center offers practical training. In the meantime, firms rely on expatriate engineers and remote operations tooling. Labor scarcity lengthens ramp-up timetables and raises salary pressure, slightly eroding operating margins.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Data Center Type: Hyperscaler dominance with colocation surge

Cloud providers accounted for 55.12% of the 2025 revenues in the Chile artificial intelligence data center market, translating to USD 137.8 million of the market size. Their presence standardizes next-generation design, such as 30 MW halls and on-site 100 kV substations. Hyperscalers’ appetite for multi-availability-zone redundancy pushes parcel aggregation near urban fiber rings, raising land valuations in Quilicura by double digits. Colocation operators respond by leasing ready-to-build plots and offering shell-and-core frameworks that align with hyperscaler specifications yet retain carrier neutrality.

Looking ahead, colocation’s 19.08% CAGR implies incremental USD 123.7 million inflows by 2031, reflecting enterprises' adoption of hybrid models and the movement of AI training off-premises once data-governance concerns are addressed. Edge micro-DCs along mining corridors and coastal cable landings are emerging as a niche, aiming for sub-10 ms latency for computer vision analytics and autonomous equipment control.

By Component: Hardware acceleration phase

Software retained 45.12% in 2025, yet hardware spending now outpaces as GPU clusters, power gear, and liquid-cooling plants dominate capex. The Chile artificial intelligence data center market size for hardware is expected to increase from USD 111.5 million in 2026 to USD 271.4 million by 2031, representing a 19.42% CAGR. Power infrastructure commands the largest ticket, as evident in Data Hall Quilicura’s 97,500 kVA diesel array, which offers 38-hour autonomy. Cooling outlays intensify as operators transition to warm-water loops and rear-door heat exchangers capable of 100 kW per rack.

Software value migrates toward orchestration layers, integrating AI-optimized scheduling, energy-aware workload placement, and predictive maintenance analytics. Service revenues trail hardware but climb steadily through managed-AI platforms, remote hands, and compliance consulting that de-risk enterprise migration.

By Tier Standard: Balancing uptime and cost

Tier IV sites controlled 60.95% of 2025 billings, equal to USD 152.4 million of the Chile artificial intelligence data center market size. Their 99.995% availability is indispensable for AI model training runs that cost millions in cloud credits. However, Tier III’s 18.61% CAGR reveals customer willingness to accept 1-hour annual downtime for lower rents, especially for development and test, and regional edge nodes. GTD’s 8 MW Tier III build, which is fully renewable, proves that Tier III can satisfy sustainability mandates while maintaining performance.

Certification paths are increasingly incorporating Tier III Gold Operational Sustainability, which combines lower redundancy with procedural rigor. Earthquake resilience remains non-negotiable, so both tiers invest in base isolation and active-mass-damping systems. As workloads diversify, a mixed-tier portfolio lets operators optimize capital while matching SLA tiers to application criticality.

By End-user Industry: Digital media outpaces traditional IT

IT and ITES held a 33.15% share in 2025, accounting for USD 82.9 million of the Chilean artificial intelligence data center market size. They retain dominance due to cloud-native SaaS vendors scaling across Spanish-speaking markets. Yet, internet and digital-media workloads, including over-the-top video, social feeds, and ad-tech inference, will grow fastest at a 20.02% CAGR, doubling revenue by 2031.

Financial services uptake accelerates as regulators clarify cloud outsourcing frameworks. Healthcare pilots AI-assisted diagnostics that require encrypted, low-latency GPU fabric, driving the need for specialized colocation suites near teaching hospitals. Mining majors deploy edge pods for predictive maintenance, linking remote sites to Santiago cores over private 5G backbones funded by Entel’s USD 330 million modernization push.

Geography Analysis

Santiago controls well over half of the operational megawatts, supported by dense fiber, existing substations, and its metropolitan proximity to enterprises. Microsoft’s USD 317 million investment in the Quilicura zone underscores the pull of the capital’s infrastructure and talent pools. Yet water-stress events and peak-hour power tariffs introduce cost pressure, nudging developers toward peripheral industrial parks.

Quilicura’s clustering effect deepens as Equinix, Amazon, and Data Hall build co-locate, leveraging shared logistics and grid upgrades. Parcels exceed 54,000 m², and backup generation surpasses 97 MVA, illustrating the scale landlords now market to hyperscalers. Renewable-energy PPAs tied to dedicated feeders reduce Scope-2 emissions, a procurement prerequisite for global tech tenants.

Government policy encourages north-and-south diversification. Antofagasta and Atacama boast abundant solar PV capacity and subsea cable landings. WOM’s 7,500 km national fiber rollout under the FON program provides remote locations with dual-path connectivity, making edge deployment a viable option. Humboldt’s 2027 go-live will enable coastal data centers to function as Asia-Pacific latency gateways, distributing workloads beyond the Santiago basin.

Coverage of the artificial intelligence (ai) data center market by Mordor Intelligence spans a wide geographic footprint, with regional analysis available for North America, South America, and Europe, alongside detailed country-level intelligence for Brazil, United States, United Kingdom, Malaysia, Indonesia, and Singapore, each shaped by local operating conditions.

Competitive Landscape

The top three cloud providers, along with two leading colocation firms, account for roughly 56% of billed revenue, indicating moderate concentration. Amazon’s USD 4 billion multi-region plan and Microsoft’s fully renewable campus set a capital threshold that deters smaller entrants. Equinix leverages its neutral-carrier status to capitalize on hyperscaler overflow, while Scala and Ascenty expedite fast-track environmental approvals to pre-lease shells. Local telcos Entel and ClaroVTR bundle fiber and hosting to defend enterprise accounts.

Strategic plays revolve around (1) green-energy hedges, (2) seismic-resilience branding, and (3) edge extensions into mining corridors. Liquid-cooling vendors partner with builders to embed rear-door and immersion systems at the shell stage, creating vendor-lock opportunities. Start-ups like NotCo and Suncast raise demand for AI as a service, spurring managed-platform offerings from incumbents. Horizontal consolidation remains possible as telcos divest DC real estate to fund 5G rollouts.

Chile Artificial Intelligence (AI) Data Center Industry Leaders

Amazon Web Services Chile SpA

Google Chile SpA

Microsoft Chile S.A.

Oracle Corporation Chile Ltd.

Huawei Technologies Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Microsoft launched its Azure Chile region after investing USD 500 million, opening three availability zones in Santiago.

- May 2025: Amazon Web Services has confirmed a USD 4 billion commitment for a Chile cloud region, marking its largest capital investment in Latin America.

- May 2025: TECfusions and Baeza Group unveiled plans for a 100 MW campus in Puente Alto.

- May 2025: Equinix secured environmental clearance for its USD 130 million ST5 build in Santiago.

- April 2025: Equinix completed a USD 50 million ST2 expansion, adding 425 liquid-cooled cabinets.

- April 2025: Chile inaugurated its first didactic data center at Inacap to develop AI operations talent.

Chile Artificial Intelligence (AI) Data Center Market Report Scope

The research encompasses the full spectrum of AI applications in data centers, covering hyperscale, colocation, enterprise, and edge facilities. The analysis is segmented by component, distinguishing between hardware and software. Hardware considerations include power, cooling, networking, IT equipment, and more. Software technologies under scrutiny encompass machine learning, deep learning, natural language processing, and computer vision. The study also evaluates the geographical distribution of these applications.

Additionally, it assesses AI's influence on sustainability and carbon neutrality objectives. A comprehensive competitive landscape is presented, detailing market players engaged in AI-supportive infrastructure, encompassing both hardware and software utilized across various AI data center types. Market size is calculated in terms of revenue generated by products and solutions providers in the market, and forecasts are presented in USD Billion for each segment.

| Cloud Service Providers |

| Colocation Data Centers |

| Enterprise / On-Premises / Edge |

| Hardware | Power Infrastructure |

| Cooling Infrastructure | |

| IT Equipment | |

| Racks and Other Hardware | |

| Software | Technology |

| Machine Learning | |

| Deep Learning | |

| Natural Language Processing | |

| Computer Vision | |

| Services | Managed Services |

| Professional Services |

| Tier III |

| Tier IV |

| IT and ITES |

| Internet and Digital Media |

| Telecom Operators |

| Banking, Financial Services and Insurance (BFSI) |

| Healthcare and Life Sciences |

| Manufacturing and Industrial IoT |

| Government and Defense |

| By Data Center Type | Cloud Service Providers | |

| Colocation Data Centers | ||

| Enterprise / On-Premises / Edge | ||

| By Component | Hardware | Power Infrastructure |

| Cooling Infrastructure | ||

| IT Equipment | ||

| Racks and Other Hardware | ||

| Software | Technology | |

| Machine Learning | ||

| Deep Learning | ||

| Natural Language Processing | ||

| Computer Vision | ||

| Services | Managed Services | |

| Professional Services | ||

| By Tier Standard | Tier III | |

| Tier IV | ||

| By End-user Industry | IT and ITES | |

| Internet and Digital Media | ||

| Telecom Operators | ||

| Banking, Financial Services and Insurance (BFSI) | ||

| Healthcare and Life Sciences | ||

| Manufacturing and Industrial IoT | ||

| Government and Defense | ||

Key Questions Answered in the Report

What is the current value of the Chile AI data center sector?

The Chile artificial intelligence data center market size stands at USD 293.88 million in 2026.

How fast is the sector growing?

The market is forecast to grow at a 17.55% CAGR, reaching USD 659.62 million by 2031.

Which data center type leads spending?

Cloud service providers hold 55.12% of 2025 revenue.

What segment is expanding the quickest?

Colocation facilities show the fastest trajectory, at a 19.08% CAGR to 2031.

How important is renewable energy to future builds?

Renewables are critical, with flagship campuses such as Microsoft Quilicura sourcing 100% clean power from AES Andes contracts.

What regional advantages does Chile offer for AI workloads?

Direct Asia-Pacific submarine cable links via the Humboldt system will lower latency and enhance Chile’s role as a trans-Pacific digital hub.

Page last updated on: