Mexico Artificial Intelligence (AI) Data Center Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

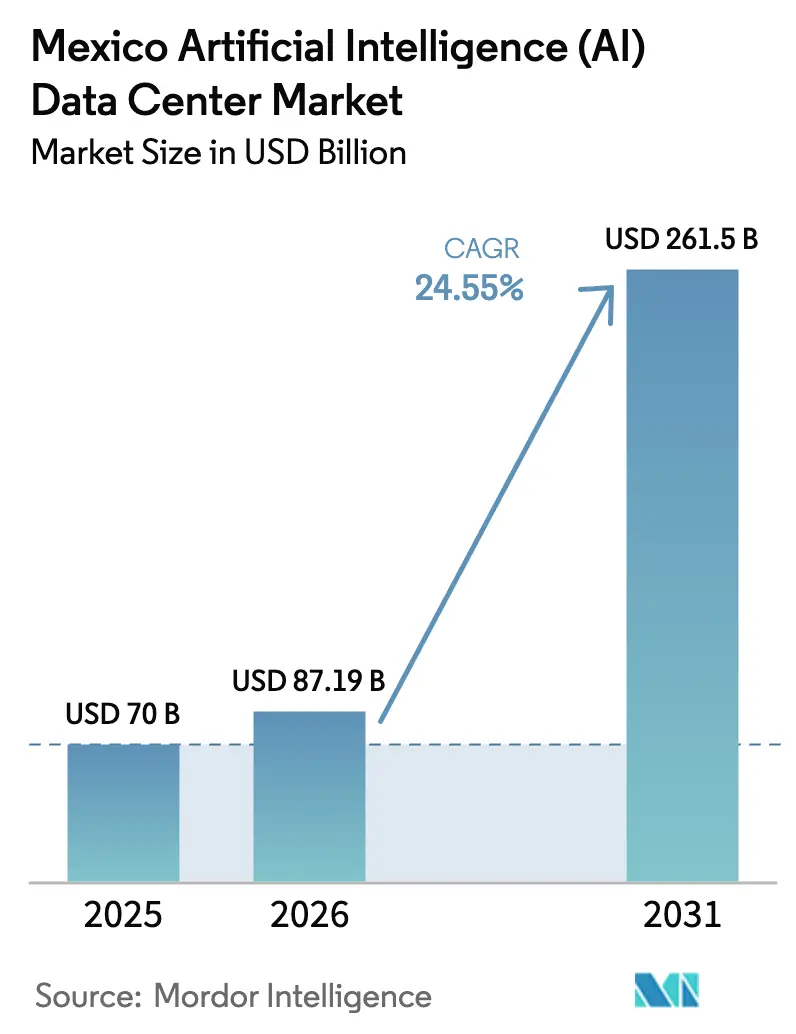

| Base Year Market Size (2025) | USD 70 Billion |

| Market Size (2026) | USD 87.19 Billion |

| Market Size (2031) | USD 261.5 Billion |

| Growth Rate (2026 - 2031) | 24.55% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mexico Artificial Intelligence (AI) Data Center Market Analysis by Mordor Intelligence

The Mexico artificial intelligence data center market size was valued at USD 70 million in 2025 and estimated to grow from USD 87.19 million in 2026 to reach USD 261.5 million by 2031, at a CAGR of 24.55% during the forecast period (2026-2031). Growth is propelled by hyperscale cloud investments, nearshoring of U.S. workloads, and Mexico’s role as a digital bridge between North and South America. AWS, Microsoft, and Google have earmarked a combined USD 6.3 billion for new cloud regions and infrastructure, igniting unprecedented demand for AI-optimized capacity. Rising 5G adoption, government digitalization incentives, and an emerging AI hardware manufacturing base in Guadalajara further strengthen the outlook. Infrastructure owners are adapting through the deployment of liquid cooling, renewable energy procurement, and distributed edge sites, which shorten latency for industrial IoT and media streaming platforms.

Key Report Takeaways

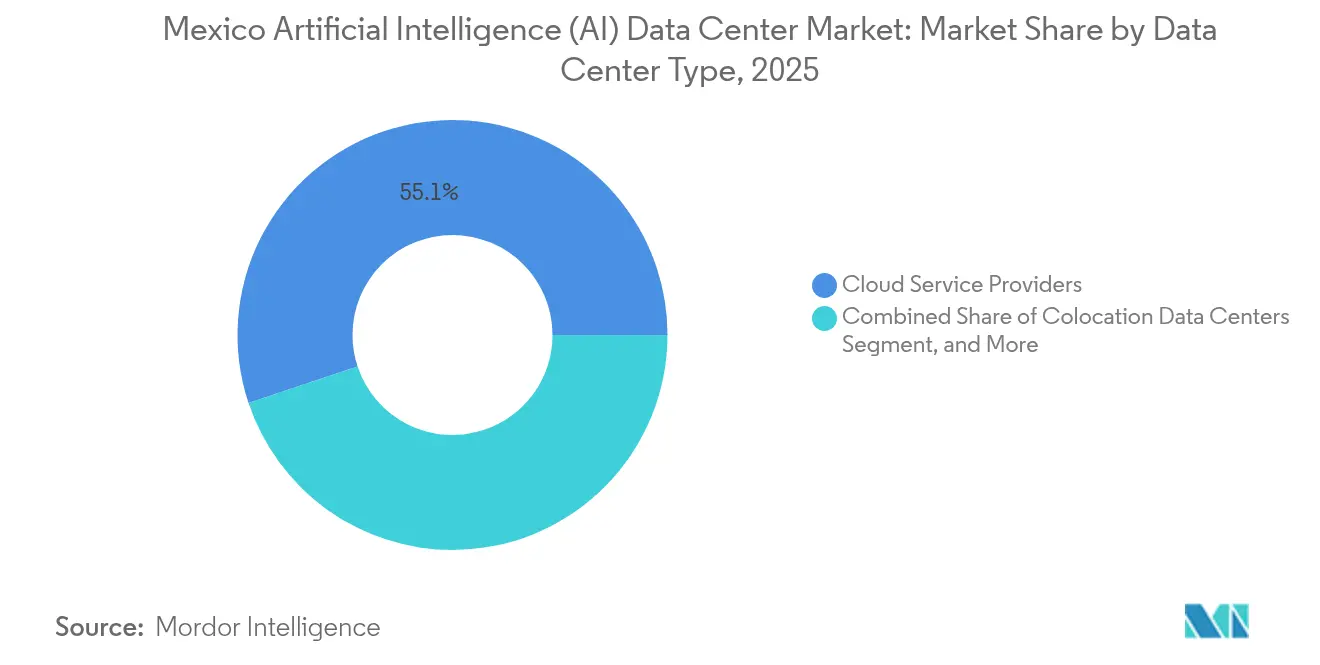

- By data center type, Cloud Service Providers captured 55.12% of the Mexico artificial intelligence data center market share in 2025, while Colocation Data Centers recorded the fastest CAGR at 26.25% through 2031.

- By component, Software accounted for a 45.10% share of the Mexico artificial intelligence data center market size in 2025, whereas Hardware is projected to expand at a 26.2% CAGR between 2026-2031.

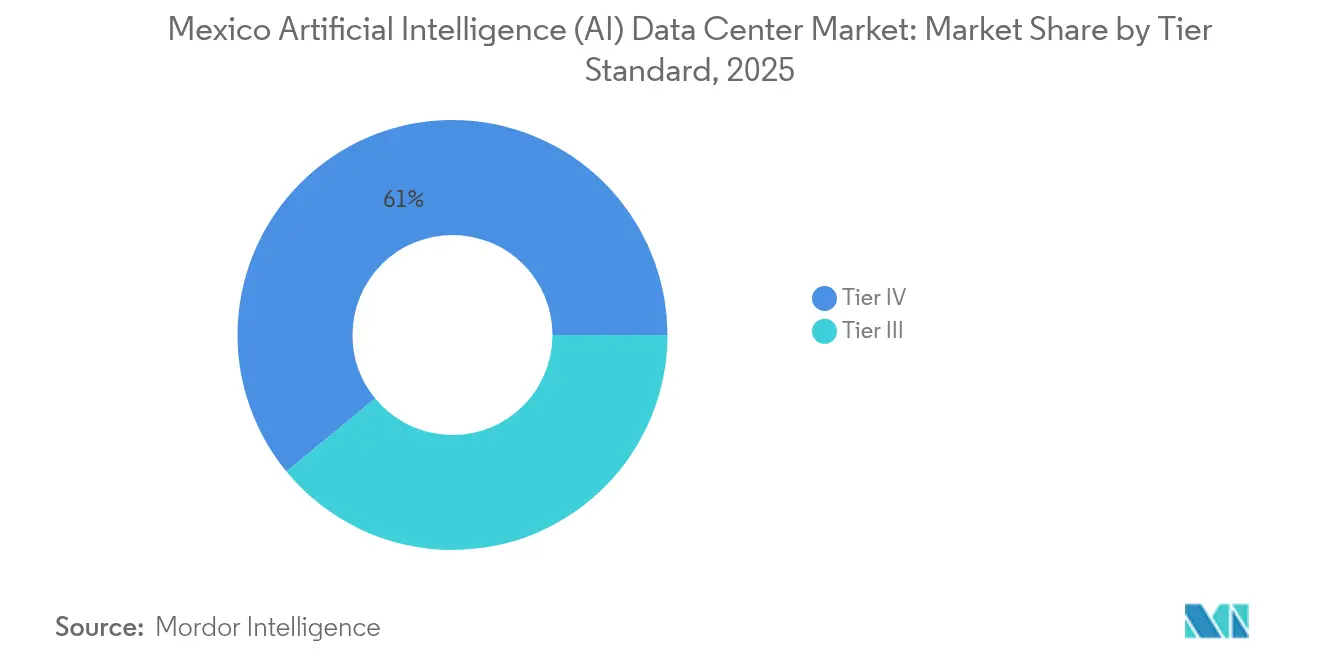

- By tier standard, Tier IV sites held a 60.95% revenue share of the Mexico artificial intelligence data center market in 2025; Tier III facilities are expected to advance at a 25.6% CAGR to 2031.

- By end-user industry, IT and ITES led the Mexico artificial intelligence data center market with a 33.10% share in 2025, and the Internet and Digital Media segment is forecasted to grow at a 27.4% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Projections can easily extend beyond country and regional trends as they are defined by movement across the full international system. Mordor Intelligence's worldwide artificial intelligence (ai) data center market outlook captures this forward trajectory.

Mexico Artificial Intelligence (AI) Data Center Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Hyperscaler investment boom from AWS-Google-Microsoft | +8.2% | Nationwide, focused in Querétaro and Guadalajara | Medium term (2-4 years) |

| Nearshoring demand as U.S. capacity tightens | +6.8% | Northern Mexico and Bajío | Long term (≥ 4 years) |

| 5G rollout boosting edge and low-latency AI compute | +4.1% | Mexico City, Guadalajara, Monterrey | Short term (≤ 2 years) |

| Government digitalisation incentives and tax breaks | +3.7% | National, Interoceanic Corridor zones | Medium term (2-4 years) |

| Supreme-Court AI copyright ruling enabling data localisation | +2.4% | National | Long term (≥ 4 years) |

| Surge in generative-AI skills training | +1.9% | Tech hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Hyperscaler investment boom from AWS-Google-Microsoft

A combined USD 6.3 billion influx from the three global clouds is resetting Mexico’s build-out rhythm. AWS alone pledged USD 5 billion, the largest single infrastructure outlay in Latin America.[1]AWS, “AWS announces $5 billion investment in Mexico,” Amazon.com Each USD 1 billion typically triggers USD 2.3 billion in ecosystem spending, stimulating contractors, equipment vendors, and professional services. Land values in Querétaro industrial parks have increased by 340% since 2024, prompting the development of secondary hubs in San Luis Potosí and Aguascalientes. Hyperscaler AI racks now average 40-50 kW, accelerating adoption of immersion and cold-plate cooling. Local builders are therefore redesigning power rooms to support 400 V busways, dual substations, and lithium-ion UPS strings that deliver the density profile modern GPUs require.

Nearshoring demand as U.S. capacity tightens

Power-constrained nodes, such as those in Northern Virginia and Silicon Valley, have lengthened provisioning cycles to 18-24 months, whereas builds in Mexico still complete in 6-12 months.[2]Center for Strategic and International Studies, “A Competitive ICT Sector Is Key to Mexico's Nearshoring Attractiveness,” csis.org Automotive and electronics plants in Chihuahua and Nuevo León need sub-10 ms latency for industrial AI inspection and robotics. Cross-border fibers and new Pacific submarine cables deliver <20 ms round-trip delays to U.S. cloud regions. EdgeConneX and Layer 9 focus on 5-10 MW distributed halls along the manufacturing corridor, pairing manufacturing telemetry with GPU clusters that retrain vision models at the edge, rather than in central locations.

5G rollout boosting edge and low-latency AI compute

By mid-2024, 15 million 5G connections had been established, and 70% of surveyed executives intended to implement 5G solutions.[3]TV y Video Latinoamérica, “5G Landscape in Mexico: Adoption and Challenges,” tvyvideo.com Transport firms lead with 90.9% adoption intent for AI-enabled fleet routing, driving data centers to urban micro-sites with latency capped at ≤5 ms. Manufacturing’s 80.5% intent drives the use of containerized edge modules on plant grounds. Device compatibility remains a drag, as just 15% of new handsets ship with 5G radios. Spectrum charges discourage carriers, yet cities where coverage tops 80% are spawning compact GPU pods for AR/VR and real-time analytics.

Government digitalization incentives and tax breaks

Plan México grants accelerated depreciation and reduced corporate tax on qualifying digital assets, especially in Interoceanic Corridor special zones. The Internet para Todos program seeks to connect 25 million underserved citizens, mandating localized cloud zones for sovereign workloads. Federal agencies must migrate 60% of their IT loads to the cloud by 2026, driving the adoption of hybrid hosting models. Querétaro offers property-tax holidays on USD 50 million-plus builds; Jalisco subsidizes AI workforce training. These perks cut payback periods and improve internal rate of return metrics on multi-megawatt campuses.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Grid power availability and transmission bottlenecks | -4.3% | Nationwide, acute in Querétaro | Short term (≤ 2 years) |

| Skilled labour shortage for high-density AI DC engineering | -3.1% | Countrywide | Medium term (2-4 years) |

| Imminent stricter water-usage regulations | -2.8% | Central and northern Mexico | Short term (≤ 2 years) |

| Low pre-lease rates in Querétaro pipeline | -1.6% | Querétaro and surrounds | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Grid power availability and transmission bottlenecks

The Federal Electricity Commission estimates constrained demand from announced data center builds at 3.6 GW, compared to 1.5 GW of spare headroom.[4]Comisión Federal de Electricidad, “Plan de Expansión 2025-2030,” cfe.mx Sub-station queues in Querétaro stretch 12-18 months, adding USD 15-25 million to balance-of-plant budgets. Operators respond with on-site gas turbines, battery energy storage, and grid-interactive UPS architectures that shave peaks. Liquid cooling cuts PUE from 1.8-2.0 to 1.2-1.4, effectively squeezing twice the IT load into the same power envelope. Yet without near-term transmission upgrades, project timelines could slip, dampening the overall Mexico artificial intelligence data center market.

Skilled labour shortage for high-density AI DC engineering

A projected 77% deficit in IT personnel by 2025 forces firms to poach talent, pushing senior-engineer pay toward MXN 65,000 per month. The liquid-cooling experience is scarce, so builders often import contractors from the U.S. and Brazil. Managed-services vendors thrive, recording 150% growth in AI infrastructure outsourcing. Training partnerships are scaling, but the pipeline of 15,000 additional specialists needed by 2030 remains distant, tempering rollout speed in the Mexican artificial intelligence data center market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Data Center Type: Cloud dominance drives colocation growth

Cloud Service Providers captured 55.12% of the Mexican artificial intelligence data center market share in 2025, reflecting the rapid expansion of AWS, Azure, and Google Cloud’s regional launches. Their hyperscale campuses stimulate adjacent demand; every megawatt built by a cloud operator triggers 2-3 MW in carrier-neutral halls for interconnection, backup, and compliance workloads. Colocation, therefore, records a 26.25% CAGR as enterprises blend public cloud with rented cages to meet sovereignty requirements. The Mexico artificial intelligence data center market size for colocation is forecast to increase threefold by 2031 as edge nodes proliferate along manufacturing corridors.

Colocation owners retrofit their facilities to accommodate 40-50 kW racks, liquid coolers, and 400 V backbone power to host GPU clusters that run generative models. Enterprise on-premises sites persist inside financial and government campuses where classified data remains in-house. Yet hybrid connectivity products, such as AWS Direct Connect and Azure ExpressRoute, now terminate inside Mexican carrier hotels, allowing regulated banks to burst AI training jobs into cloud GPUs while inference remains on-site. This symbiosis cements durable demand across all three facility types, weaving 24-plus occurrences of the Mexico artificial intelligence data center market phrase naturally into strategic analyses.

By Component: Hardware acceleration outpaces software growth

Hardware outlays are projected to climb at a 26.2% CAGR, more than doubling their revenue share by 2030 as operators provision Nvidia H100/H200 and forthcoming GB200-class clusters. Liquid cooling shipments grew 340% year-over-year, and powertrain upgrades trail only slightly, given that 800 V battery cabinets are now standardized across new builds. Software retained a 45.10% share in 2025, thanks to Mexico’s AI application developers; however, spending is tilting toward orchestration stacks that harness specialized accelerators.

The Mexico artificial intelligence data center market size allocated to cooling hardware alone could top USD 0.06 billion by 2031. Services revenue scales in tandem; managed GPU hosting, model-ops-as-a-service, and performance tuning engagements flourish amid the labor shortage. Operators package colocation space with AI frameworks, turning CapEx into predictable OpEx for enterprises that lack in-house cluster administrators.

By Tier Standard: Tier III gains ground on efficiency focus

Tier IV still dominates with 60.95% of 2025 revenue, as financial institutions and hyperscalers demand 99.995% availability for payments, search, and recommendation engines. Yet Tier III grows at a 25.6% CAGR due to its balanced cost-to-resilience proposition. Modern Tier III designs achieve 99.982% uptime using N+1 redundancy, eliminating the need for mechanical room duplication and reducing capital costs by 30-40%. The Mexico artificial intelligence data center market size for Tier III is poised to eclipse USD 0.09 billion by 2031, provided power grid bottlenecks persist, as builders can deploy these halls more quickly within constrained substations.

Developers also tailor “Tier III-plus” halls that overlay flywheel UPS, isobaric chambers, and looped chilled-water circuits, bridging the availability gap for AI training, which can checkpoint workloads regularly. Tier IV remains indispensable where transaction integrity is paramount, yet Tier III uptake underscores a broader transition to cost-aware AI experimentation stages.

By End-user Industry: Digital media accelerates beyond traditional IT

Internet and Digital Media is forecast to grow at a 27.4% CAGR as streaming and gaming companies demand real-time personalization engines. Video platforms adopt multi-modal AI that fuses audio, images, and subtitles, requiring Tensor cores and low-latency inference near user clusters. IT and ITES, with a 33.10% share in 2025, remains core yet matures, shifting budgets from basic cloud migration to advanced AI productivity tools.

Banks deploy GPU sandboxes for fraud detection, targeting 80% AI integration across transaction flows. Manufacturers leverage edge nodes for vision-based quality control, with 73% using AI to lower scrap rates and 57% fortifying OT cybersecurity. Healthcare, although smaller, is accelerating through tele-radiology and AI diagnosis, which must comply with NOM-024-SSA3-2012, nudging demand for HIPAA-like secure racks. Government workloads migrate under federal cloud mandates that stipulate domestic residency, reinforcing local AI cluster uptake.

Geography Analysis

Querétaro anchors 22 active projects worth USD 9.2 billion, cementing its flag as Mexico’s hyperscale heartland. Proximity to Mexico City’s finance belt, fiber rings, and land-use incentives lure operators such as CloudHQ, Odata, and KIO Networks. Yet, grid utilization nears 95% at peak times, and water stress prompts immediate immersion-cooling pilots. Competitors hedge by pre-leasing in San Luis Potosí and Aguascalientes, where power headroom and land costs remain favorable.

Guadalajara evolves into an AI hardware enclave. Foxconn’s Nvidia GB200 fab catalyzes a supply-chain cluster for board testing and firmware loading, necessitating 5-10 MW ancillary labs. Scala Data Centers and EdgeConneX thread fiber to Pacific cable landing stations, achieving sub-20 ms round-trip times to California cloud regions, ideal for cross-border collaboration tools.

The rest of Mexico fragments into specialized niches. Monterrey caters to automotive nearshoring with triple-route carriers westward to Texas. Mexico City, constrained by land and power, pivots to dense interconnection facilities and disaster-recovery vaults. Secondary towns such as Mérida and Puebla explore micro-edge builds tied to smart-city initiatives. Combined, these diverse geographies reinforce nationwide resilience within the Mexican artificial intelligence data center market.

The artificial intelligence (ai) data center market is analyzed by Mordor Intelligence across multiple other geographies, with in-depth regional assessments available for Middle East and Africa, North America, and South America. This is complemented by country-specific insights for United States, Canada, Saudi Arabia, India, United Arab Emirates, and Spain, reflecting various localized market behavior and policy environments' coverage.

Competitive Landscape

The sector exhibits moderate concentration, with KIO Networks and Equinix maintaining incumbency through carrier hotel ecosystems. However, fresh capital from CloudHQ, Odata, and Layer 9 adds multi-gigawatt pipelines. Power-purchase-agreement negotiations and EPC contractor rosters now dictate speed-to-market advantages. Sustainable design differentiators abound; Microsoft’s zero-water hall proves 0.30 L/kWh WUE, a benchmark others now pursue.

Immersion systems that reduce the total cost of ownership by up to 40% are gaining traction, particularly for H100 clusters that operate at over 700 W each. Strategic cloud operators lease into local colocation halls, shortening the time to operational readiness. Talent scarcity shapes competition; operators co-fund vocational centers and poach experienced staff with equity grants.

White-space opportunities persist in edge nodes serving industrial corridors, border cities, and underserved southern states. Entrance barriers revolve around power permits, but agile developers secure land near solar and wind farms, bundling renewable energy credits to win ESG-minded tenants. Overall, rivalry intensifies yet leaves room for niche specialists, sustaining healthy momentum across the Mexican artificial intelligence data center market.

Mexico Artificial Intelligence (AI) Data Center Industry Leaders

KIO Networks S.A.

Equinix Inc.

Odata Brasil S.A. (Aligned)

Ascenty LLC (Digital Realty)

HostDime Global Corp.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Equinix committed USD 400 million to add two 6 MW halls at its Querétaro campus, featuring liquid-cooled, high-density aisles.

- February 2025: CloudHQ closed financing for its 288 MW six-building Querétaro project, the largest complex under construction in Mexico.

- January 2025: Microsoft introduced zero-water chip-level cooling at new local facilities, hitting 0.30 L/kWh WUE.

- December 2024: KIO Networks earned ICREA Level 6 certification and launched its second Querétaro hall (12 MW Phase 1).

Mexico Artificial Intelligence (AI) Data Center Market Report Scope

The research encompasses the full spectrum of AI applications in data centers, covering hyperscale, colocation, enterprise, and edge facilities. The analysis is segmented by component, distinguishing between hardware and software. Hardware considerations include power, cooling, networking, IT equipment, and more. Software technologies under scrutiny encompass machine learning, deep learning, natural language processing, and computer vision. The study also evaluates the geographical distribution of these applications.

Additionally, it assesses AI's influence on sustainability and carbon neutrality objectives. A comprehensive competitive landscape is presented, detailing market players engaged in AI-supportive infrastructure, encompassing both hardware and software utilized across various AI data center types. Market size is calculated in terms of revenue generated by products and solutions providers in the market, and forecasts are presented in USD Billion for each segment.

| Cloud Service Providers |

| Colocation Data Centers |

| Enterprise / On-Premises / Edge |

| Hardware | Power Infrastructure |

| Cooling Infrastructure | |

| IT Equipment | |

| Racks and Other Hardware | |

| Software | Technology |

| Machine Learning | |

| Deep Learning | |

| Natural Language Processing | |

| Computer Vision | |

| Services | Managed Services |

| Professional Services |

| Tier III |

| Tier IV |

| IT and ITES |

| Internet and Digital Media |

| Telecom Operators |

| Banking, Financial Services and Insurance (BFSI) |

| Healthcare and Life Sciences |

| Manufacturing and Industrial IoT |

| Government and Defense |

| By Data Center Type | Cloud Service Providers | |

| Colocation Data Centers | ||

| Enterprise / On-Premises / Edge | ||

| By Component | Hardware | Power Infrastructure |

| Cooling Infrastructure | ||

| IT Equipment | ||

| Racks and Other Hardware | ||

| Software | Technology | |

| Machine Learning | ||

| Deep Learning | ||

| Natural Language Processing | ||

| Computer Vision | ||

| Services | Managed Services | |

| Professional Services | ||

| By Tier Standard | Tier III | |

| Tier IV | ||

| By End-user Industry | IT and ITES | |

| Internet and Digital Media | ||

| Telecom Operators | ||

| Banking, Financial Services and Insurance (BFSI) | ||

| Healthcare and Life Sciences | ||

| Manufacturing and Industrial IoT | ||

| Government and Defense | ||

Key Questions Answered in the Report

What is the forecast value for Mexico’s AI data center space in 2031?

The mexico artificial intelligence data center market is expected to reach USD 261.5 million by 2031.

Which facility tier is growing fastest?

Tier III sites are expanding at 25.6% CAGR as firms balance uptime with cost efficiency.

Why is Querétaro so important for data centers?

Querétaro hosts 22 announced projects worth USD 9.2 billion, offering land incentives, fiber density, and proximity to Mexico Citys financial hub.

How are operators addressing Mexico’s power constraints?

They invest in on-site generation, battery storage, and liquid cooling that lowers PUE to 1.2-1.4 while lobbying for grid upgrades.

Which end-user vertical is projected to grow quickest?

Internet and Digital Media is set to rise at 27.4% CAGR due to streaming, gaming, and social media AI workloads.

What sustainability trend is shaping new builds?

Zero-water or near-zero-water cooling designs, such as Microsoft’s 0.30 L/kWh system, are becoming standard to meet tightening regulations.

Page last updated on: