Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

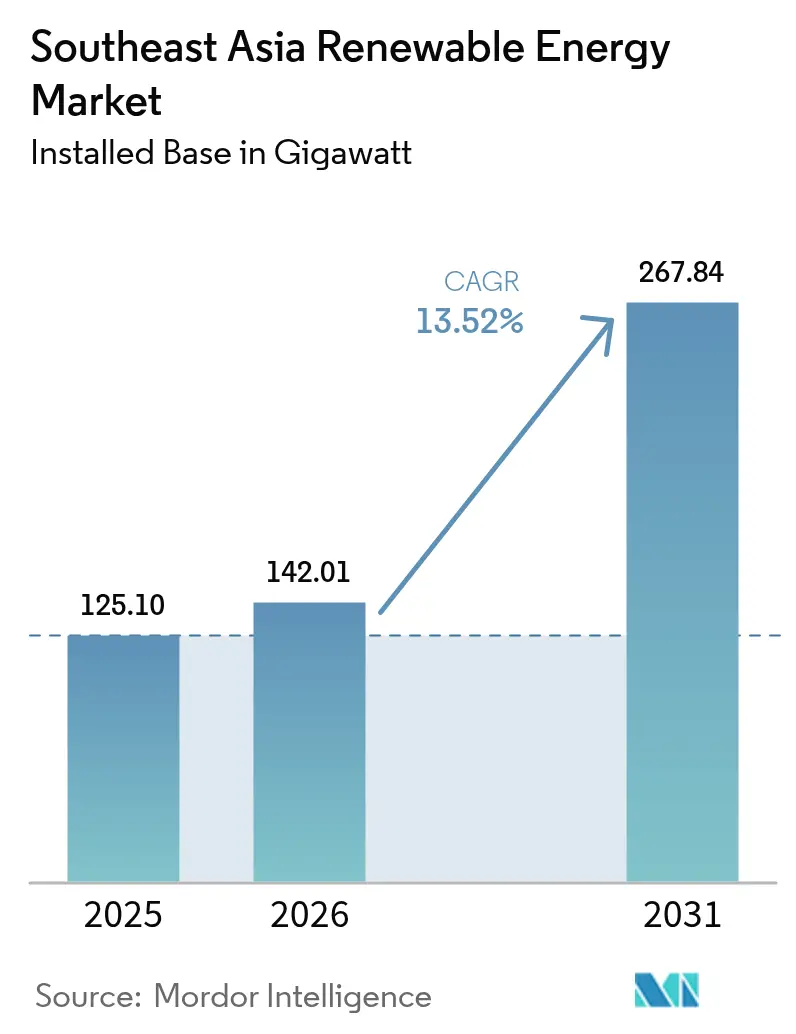

| Base Year Market Size (2025) | 125.10 gigawatt |

| Market Volume (2026) | 142.01 gigawatt |

| Market Volume (2031) | 267.84 gigawatt |

| Growth Rate (2026 - 2031) | 13.52% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Southeast Asia Renewable Energy Market Analysis by Mordor Intelligence

The Southeast Asia Renewable Energy Market size was valued at 125.10 gigawatt in 2025 and estimated to grow from 142.01 gigawatt in 2026 to reach 267.84 gigawatt by 2031, at a CAGR of 13.52% during the forecast period (2026-2031).

Rapid policy alignment with net-zero targets across eight ASEAN states has accelerated investment, while persistent LNG price volatility has improved the cost-competitiveness of solar-plus-storage solutions compared to gas-fired power.[1]International Energy Agency, “2024 South-East Asia Energy Update,” iea.org Solar retains the largest slice of capacity, aided by declining module costs and mature supply chains, while wind energy is the fastest growing, following large offshore concessions in the Philippines and onshore pipeline expansion in Vietnam. Corporate RE100 programs in export-oriented sectors are spurring commercial and industrial (C&I) demand, especially in Thailand’s automotive clusters and Vietnam’s electronics parks. The region’s competitive landscape remains moderately fragmented, with local developers such as ACEN and Gulf Energy competing against global players like Ørsted and Vena Energy for gigawatt-scale auctions.

Key Report Takeaways

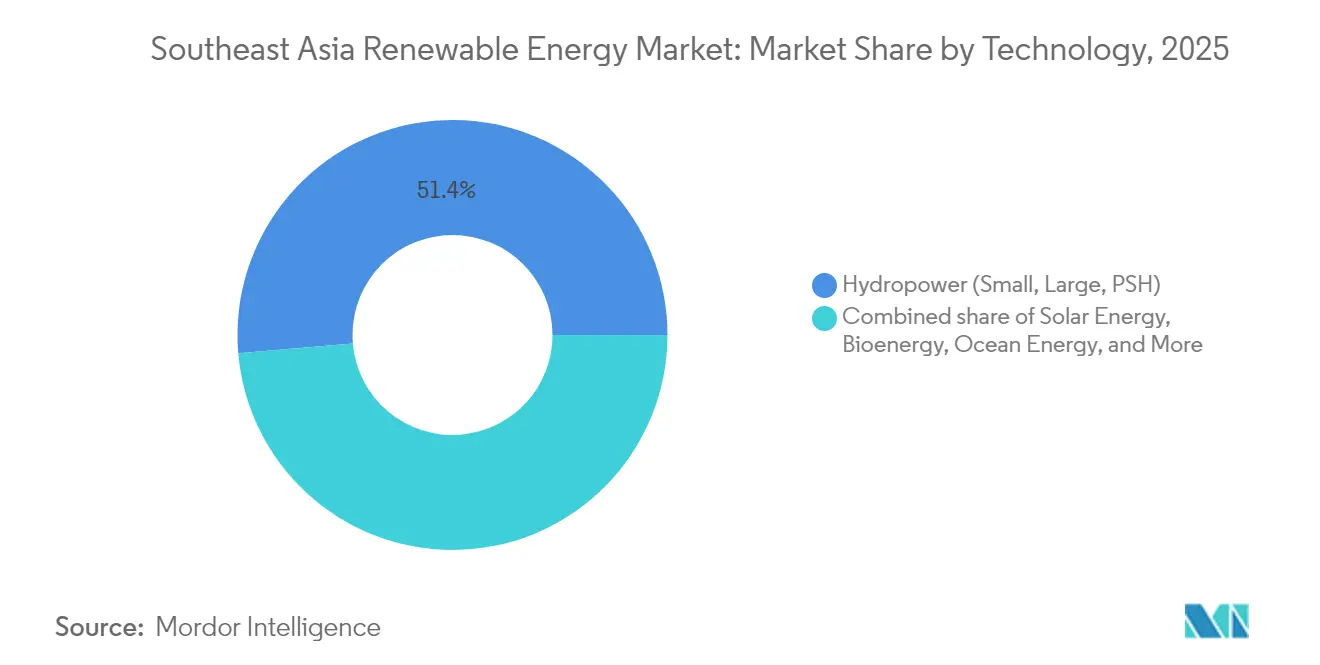

- By type, hydropower led with 51.35% of the Southeast Asia renewable energy market share in 2025; ocean energy is forecast to expand at a 134.85% CAGR to 2031.

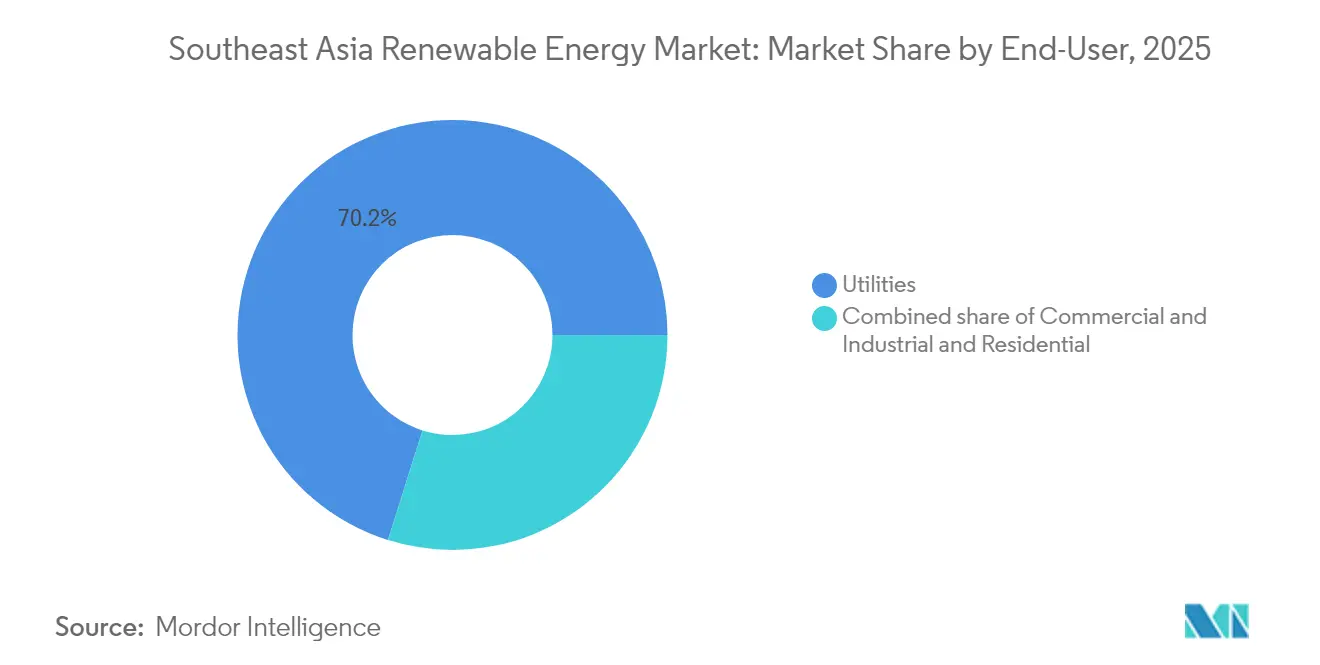

- By end-use sector, the utility segment accounted for 70.15% of the Southeast Asia renewable energy market size in 2025, while commercial and industrial PPAs are projected to advance at a 16.14% CAGR through 2031.

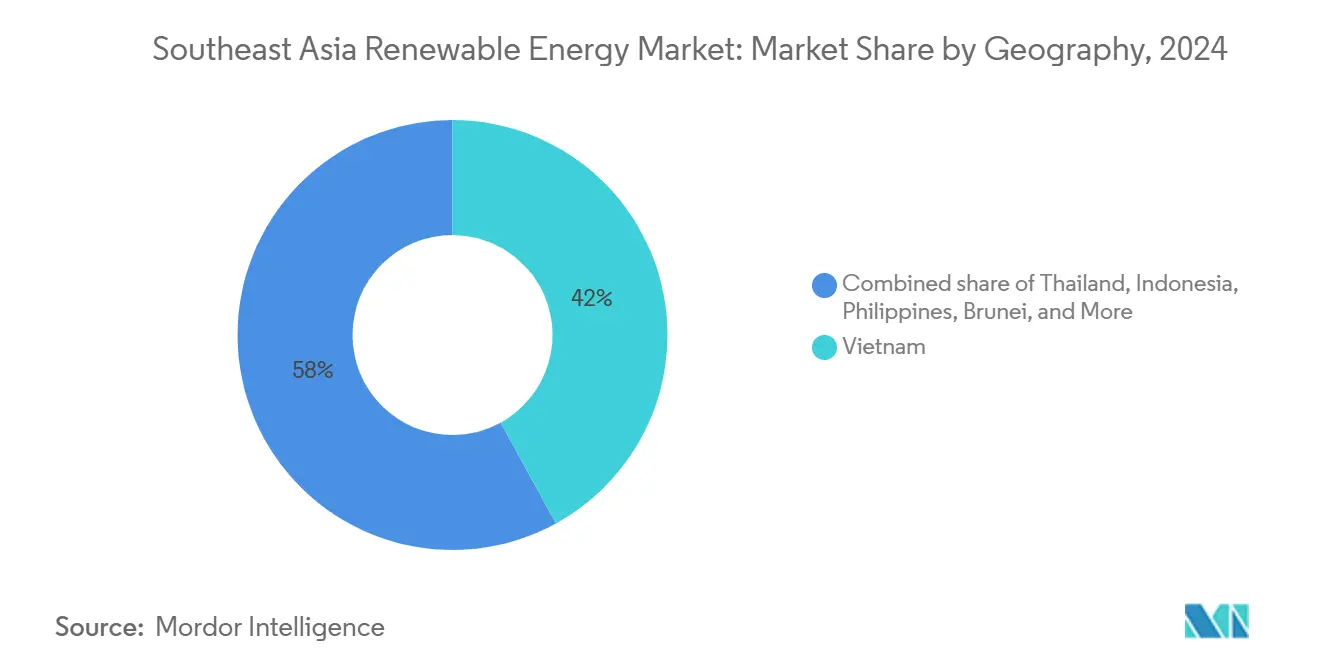

- By geography, Vietnam commanded 41.55% capacity share in 2025, yet Brunei is poised for a 101.32% CAGR between 2026-2031.

- ACEN, B.Grimm Power, and Gulf Energy, together, controlled less than 10% of regional capacity in 2025, underscoring a fragmented competitive field.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Southeast Asia Renewable Energy Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| ASEAN Green-Energy Financing Booms | +2.80% | Regional (SG, VN, ID, PH) | Medium term (2-4 yrs) |

| Rapid Corporate RE100 Procurement | +2.30% | VN, TH, MY | Short term (≤ 2 yrs) |

| LNG Price Volatility Favoring Solar-Storage | +2.10% | ID, TH, PH | Medium term (2-4 yrs) |

| Cross-Border Power-Trade Initiatives | +1.90% | LA, TH, MY, SG | Long term (≥ 4 yrs) |

| Net-Zero-Driven Gigawatt Auctions | +2.50% | ID, PH | Medium term (2-4 yrs) |

| Grid-Connected Floating Solar Pilots | +1.20% | ID, TH, PH | Long term (≥ 4 yrs) |

| Source: Mordor Intelligence | |||

Green-energy financing booms led by Singapore-based funds

Singapore’s Green Bond Framework aims to target SGD 35 billion of sustainable issuance by 2030, catalyzing cross-border capital flows into renewable projects across ASEAN.[2]Norfund, “Norfund invests in Xurya,” norfund.no Sovereign investment vehicles, such as Temasek, partnering with BlackRock’s USD 1.4 billion climate fund, are steering private capital toward distributed solar developers, unlocking commercial and industrial (C&I) rooftops that were previously underserved. The Norwegian Climate Investment Fund’s USD 55 million equity investment in Indonesia’s Xurya demonstrates that foreign investors favor smaller, scalable arrays that match industrial electricity profiles. Local banks follow suit, DBS’s RE100 pledge signals that financiers are embedding green-sourcing clauses in corporate loans, creating an ecosystem where renewable procurement becomes a baseline requirement.

Rapid corporate RE100 procurement across export-led industries in Vietnam & Thailand

Vietnam has lifted its 2030 solar target to 73 GW after multinationals relocating from China indicated demand that outstrips earlier forecasts. Thailand mirrors this push: its 5 GW feed-in-tariff round explicitly earmarks industrial zones where auto and electronics producers need verified clean electricity. The Asian Development Bank’s USD 820 million loan for 12 Thai solar-plus-storage projects underscores storage moving from pilot to prerequisite for round-the-clock supply. Long-term corporate PPAs, often spanning 15 to 20 years, now price below volatile LNG-indexed tariffs, providing exporters with both cost certainty and compliance with supplier codes of conduct.

Accelerating LNG price volatility improving LCOE competitiveness of solar-plus-storage

Spot LNG prices averaged more than double their 10-year mean throughout 2024, lifting the levelized cost of gas generation above that of comparable solar-plus-storage projects in Indonesia and Thailand. Indonesia's PLN absorbed USD 8 billion in subsidies to shield retail tariffs, sharpening the government's resolve to cut fossil exposure. Industrial buyers respond by locking in renewables to hedge energy price risk; this has made solar paired with four-hour batteries bankable, as project finance models can tap grid-service revenues and energy sales. In Thailand, energy-intensive exporters prioritize renewables for budget stability, thereby pushing commercial and industrial (C&I) demand beyond the earlier utility-scale bias.

Cross-border power-trade initiatives (Lao-PDR-Thailand-Malaysia-Singapore) scaling regional demand

The LTMS-PIP’s 300 MW pilot validated the technical feasibility of a multi-country, asynchronous grid trade.[3]Ember-Climate, “LTMS-PIP Pilot Analysis,” ember-climate.org Singapore, a land-constrained yet affluent nation, has committed to importing 4 GW of renewables by 2035, effectively underwriting large hydro and solar projects in neighboring economies. Sarawak Energy is positioning Malaysia’s hydro-rich state as a clean-power exporter, while Laos intends to monetize surplus hydro by sending electrons south. Harmonized wheeling rules under the broader ASEAN Power Grid initiative reduce investor risk, letting developers size projects to a multi-market offtake instead of a single national demand curve.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Grid Congestion & Curtailment in Southern VN | −1.8% | VN (Ninh Thuan, Binh Thuan) | Short term (≤ 2 yrs) |

| Auction Transition Uncertainty in Indonesia | −1.5% | ID | Medium term (2-4 yrs) |

| Land-Banking & Right-of-Way Issues in PH | −1.2% | PH | Medium term (2-4 yrs) |

| Limited Wind-Turbine Manufacturing Base | −1.0% | Regional (VN, PH, TH) | Long term (≥ 4 yrs) |

| Source: Mordor Intelligence | |||

Grid congestion & curtailment risks in Vietnam’s southern corridor

Vietnam’s renewable energy rollout has outpaced its 500 kV backbone, forcing solar farms in Ninh Thuan and Binh Thuan to curtail output as demand lies hundreds of kilometers to the north. The eighth Power Development Plan acknowledges this bottleneck, but timelines for new lines remain vague. Developers are incorporating 5 to 10% curtailment assumptions into their cash flows, which increases the required tariffs or returns. The government has floated direct-wire PPAs to local industry as an interim relief, yet that would shift rather than solve congestion. Until transmission catches up, financiers may favor regions with excess evacuation capacity.

Land-banking & right-of-way challenges for utility-scale projects in the Philippines

Complex land titles and smallholder plots delay site aggregation, raising soft costs and elongating financial close timelines. Aboitiz Power lists land issues alongside grid access as its top development risks; more than 1,000 awarded service contracts remain inactive, illustrating the gridlock. To reach the 50% solar capacity generation goal by 2040, 46,140 ha would be required, intensifying competition with agriculture. Green Lanes streamline paperwork but cannot resolve overlapping tenure; deeper cadastral reforms are required.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Hydropower Anchors Capacity, Ocean Energy Surges from Near-Zero Base

Hydropower accounted for 51.35% of installed capacity in 2025, underpinned by large dams in Laos and Malaysia’s Sarawak region that export surplus electricity to neighbors. Solar photovoltaics supplied roughly 35% of Vietnam’s energy after its 2019-2020 boom, benefiting from a module oversupply that pushed prices below USD 0.15 per watt. Onshore wind contributed 8-10%, concentrated in Vietnam’s central highlands, while offshore wind remained in pre-construction despite multi-gigawatt concessions. Ocean energy is poised for significant growth, with a projected 134.85% CAGR through 2031 for tidal and wave pilots in the Philippines and Indonesia.

Ocean technologies currently total less than 10 MW, so even modest additions will result in triple-digit growth. Capital expenditure per megawatt remains 3-4 times that of offshore wind, and regional supply chains for subsea cables are lacking, which temper near-term commercialization. Bioenergy supplied 4-5%, mainly from palm oil mill effluent in Indonesia and rice husk combustion in Thailand, whereas geothermal, classified under “Other”, delivered roughly 2 GW, mostly in Indonesia and the Philippines.

By End-Use Sector: Utilities Dominate, Corporate PPAs Reshape Procurement

Utilities owned 70.15% of capacity in 2025 and are forecast to grow at a 15.92% CAGR on the back of gigawatt-scale auctions in Indonesia and the Philippines. Competitive bidding compressed tariffs by 20-30% relative to legacy incentives, driving developers to streamline engineering, procurement, and construction costs. Commercial and industrial rooftop solar captured 20-25% of the market, powered by Vietnam’s Decree 80/2024 and Thailand’s Direct PPA rules, which allow export manufacturers to lock in 10-15-year contracts at fixed prices.

Residential rooftop systems remain marginal at 5-8% because Philippine and Thai caps restrict system size, and bank financing for small owners is scarce. Singapore differs: more than 1,500 HDB blocks host panels under mandated solar-ready roofs, illustrating the policy’s role in demand creation.

Geography Analysis

Vietnam’s 41.55% share of the Southeast Asia renewable energy market in 2025 stemmed from a 16 GW solar surge during 2019-2020; however, 30-40% midday curtailment now stifles returns. EVN’s USD 3 billion grid upgrade, due in 2027, should alleviate congestion, while Decree 80/2024 opens up 1 GW of corporate PPA demand, partly offsetting auction delays. Offshore wind, including La Gan’s 3.5 GW, could diversify generation post-2027, although typhoon-proof turbines raise capital expenditures by 15-20% over European benchmarks.

Indonesia and the Philippines rely on auctions to fulfill net-zero pledges. Indonesia’s USD 20 billion Just Energy Transition Partnership is experiencing slow disbursement, and PPA negotiations typically last 9-12 months. The Philippines’ 3.6 GW 2024 auction faces land-banking bottlenecks, yet low solar and wind tariffs signal improving competitiveness. Indonesia’s 145 MW Cirata floating solar project reveals reservoir potential, offering 30-40% interconnection savings compared to ground-mount projects. Thailand and Malaysia present mature regulatory landscapes. Thailand’s Direct PPA law and Malaysia’s Corporate Renewable Energy Supply Scheme attract multinational manufacturers seeking green power hedges. Thailand is also studying pumped storage to buffer variable renewable energy sources, while Malaysia’s Sarawak exports hydroelectric surpluses to the Peninsular grids. Singapore compensates for land scarcity with a 4 GW import target and mandatory rooftop solar on public housing, whereas Brunei, from near-zero renewables in 2024, expects a 101.32% CAGR through 2031, anchored by its first 54 MW solar plant.

Competitive Landscape

Competition in the Southeast Asia renewable energy market is moderate and intensifying, with no single developer exceeding 10% of installed capacity. Regional champions, such as ACEN in the Philippines, Gulf Energy in Thailand, and B.Grimm in Thailand, leverage their domestic relationships to secure land and permits quickly. International majors such as Ørsted and Vena Energy bring project finance expertise and offshore wind experience, often teaming with local partners to navigate licensing. Technology focus is a key differentiator: Sunseap concentrates on commercial and industrial (C&I) solar rooftops, Nexif Energy on multi-country wind, and Masdar on floating solar, as evidenced by its PLN joint projects.

Joint ventures are becoming the norm. BuhaWind Energy, a joint venture between Copenhagen Energy and PetroGreen, invests PHP 330 billion in Ilocos Norte’s first 1 GW offshore wind farm, illustrating how risk sharing unlocks large-scale projects. Supply-chain localization provides a cost edge: CS Wind’s tower factory in Vietnam and potential nacelle assembly lines in Indonesia reduce lead times and import duties. However, turbine shortages persist region-wide, exposing projects to price spikes and schedule risks until local manufacturing scales.

Southeast Asia Renewable Energy Industry Leaders

B.Grimm Power PCL

Gulf Energy Development PCL

ACEN Corp (Ayala Group)

Vena Energy

BCPG PCL

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: ACWA Power and the Malaysian Investment Development Authority (MIDA) have signed a Memorandum of Understanding (MoU) to potentially develop up to 12.5 GW of power generation capacity by 2040.

- April 2025: Masdar and PLN sign two floating-PV agreements in Indonesia, scaling the technology beyond Cirat. These agreements include a Memorandum of Understanding (MoU) for a floating PV project at the Jatigede Dam reservoir in West Java.

- November 2024: Nexif Ratch Energy inks MoU for a 102 MW wind farm in Khanh Hoa, Vietnam, investing USD 155 million. The company signed a Memorandum of Understanding (MoU) for the project with the planning department of Vietnam’s Khanh Hoa province,

- September 2024: Under its "Green Lane" initiative, the Philippine Board of Investments (BOI) fast-tracked approvals for strategic investments, endorsing renewable energy projects worth a total of PHP 4.13 trillion (around USD 72 billion). Notably, offshore wind energy projects have received a substantial allocation of approximately PHP 600 billion.

Southeast Asia Renewable Energy Market Report Scope

Renewable energy is the energy produced from sources such as the sun and wind, which are abundant and replenishable. Renewable energy is commonly used for electricity generation, space and water heating and cooling, as well as transportation. Biomass, geothermal resources, sunlight, water, and wind are some of the energy sources that can be converted into clean and usable energy.

The Southeast Asian renewable energy market is segmented by technology, end-user. By technology, the market is segmented into Solar Energy (PV and CSP), Wind Energy (Onshore and Offshore), Hydropower (Small, Large, and PSH), Bioenergy, Geothermal, and Ocean Energy (Tidal and Wave). By end user, the market is segmented into Utilities, Commercial and Industrial, and Residential.

The report also covers the market size and forecasts for the renewable energy market across the major countries in the region. For each segment, market sizing and forecasts were made based on installed capacity (GW).

By Technology

| Solar Energy (PV and CSP) |

| Wind Energy (Onshore and Offshore) |

| Hydropower (Small, Large, PSH) |

| Bioenergy |

| Geothermal |

| Ocean Energy (Tidal and Wave) |

By End-User

| Utilities |

| Commercial and Industrial |

| Residential |

By Geography

| Vietnam |

| Indonesia |

| Philippines |

| Thailand |

| Malaysia |

| Singapore |

| Rest of Southeast Asia |

| By Technology | Solar Energy (PV and CSP) |

| Wind Energy (Onshore and Offshore) | |

| Hydropower (Small, Large, PSH) | |

| Bioenergy | |

| Geothermal | |

| Ocean Energy (Tidal and Wave) | |

| By End-User | Utilities |

| Commercial and Industrial | |

| Residential | |

| By Geography | Vietnam |

| Indonesia | |

| Philippines | |

| Thailand | |

| Malaysia | |

| Singapore | |

| Rest of Southeast Asia |

Key Questions Answered in the Report

What is the projected capacity of renewables in Southeast Asia by 2031?

The Southeast Asia Renewable Energy Market is forecast to reach 267.84 GW by 2031, growing at a 13.52% CAGR.

Which country currently leads Southeast Asia in installed renewable capacity?

Vietnam held 41.55% of regional capacity in 2025, largely due to its 2019-2020 solar boom.

Why are corporate PPAs gaining popularity in Southeast Asia?

Decree 80/2024 in Vietnam and similar rules in Thailand allow export manufacturers to secure long-term renewable supply, helping them avoid future EU carbon border taxes.

How does floating solar benefit Indonesia’s grid expansion plans?

Projects like the 145 MW Cirata plant leverage existing hydropower reservoirs, cutting interconnection costs by up to 40% and avoiding costly land acquisition.

What are the main bottlenecks facing offshore wind in the region?

Limited local turbine manufacturing, localization mandates, and typhoon-resistant design requirements raise cap-ex and extend procurement timelines.

Page last updated on: