Banana Market Size and Share

Banana Market Analysis by Mordor Intelligence

The banana market size is expected to grow from USD 139.51 billion in 2025 to USD 145.97 billion in 2026 and is forecast to reach USD 183.43 billion by 2031 at 4.63% CAGR over 2026-2031. Robust demand in health-focused consumer segments, steady growth in functional snack formats, and widening cold-chain coverage underpin this expansion, giving the banana market resilience against regional income swings. Asia-Pacific remains the largest regional contributor due to strong production bases and rising intra-regional trade, while Africa posts the fastest growth as urban buyers shift toward convenient fresh produce. Large multinationals continue to drive innovation in sustainability and logistics efficiency, and supermarket private-label programs tighten requirements for verifiable social and environmental standards. Disease management costs, volatile freight rates, and stricter pesticide regulations temper growth but do not overturn the long-term bullish outlook for the banana market as a staple food and premium snack item.

Key Report Takeaways

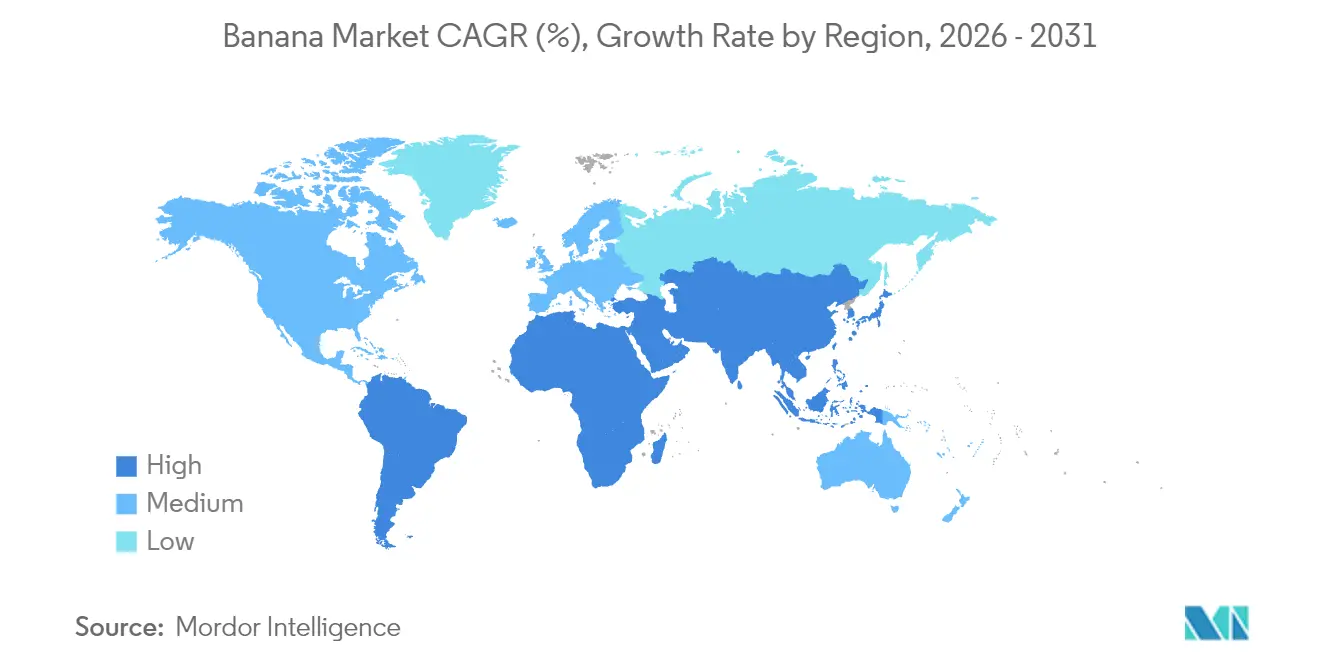

- By geography, Asia-Pacific led with 48.20% of the banana market share in 2025, while Africa is forecast to record a 5.63% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Banana Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating demand from health-conscious consumers | +0.8% | Global, with a concentration in North America and Europe | Medium term (2-4 years) |

| Trade liberalization in key importing nations | +0.6% | Asia-Pacific, the Middle East, and North America | Long term (≥ 4 years) |

| Rapid expansion of supermarket private labels | +0.5% | Europe, North America, and emerging Asia-Pacific markets | Medium term (2-4 years) |

| Emerging cold-chain hubs | +0.7% | Global, with emphasis on Africa and Southeast Asia | Long term (≥ 4 years) |

| Carbon-neutral banana initiatives by multinationals | +0.4% | Global, driven by regulatory requirements in Europe and North America | Long term (≥ 4 years) |

| Rise of functional banana-based snacks | +0.9% | North America, Europe, and urban Asia-Pacific centers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Escalating Demand from Health-Conscious Consumers

Premium banana consumption accelerates as fitness-oriented buyers focus on the fruit’s potassium, fiber, and natural-sugar attributes. Organic and fair-trade labels command 20–30% price premiums in North America and Europe, enabling growers to recover higher farming costs while funding soil-health projects. Brand collaborations such as Givaudan and Dole’s upcycled green banana powder showcase a circular-economy approach that turns culls into ingredients for bakery and beverage lines[1]Source: Press Office, “Givaudan and Dole partner to create upcycled green banana powder,” Givaudan, givaudan.com. Retail data indicate a 15–20% uptick in purchases when bananas appear in wellness merchandising sets alongside sports drinks and protein bars. Higher margins gained from health positioning encourage exporters to upgrade quality protocols, which in turn deepen supplier–retailer partnerships in premium supermarket channels.

Trade Liberalization in Key Importing Nations

Lower tariffs and streamlined customs rules expand market access for emerging exporters. Agreements such as the Economic Partnership pacts between the European Union and Caribbean producers remove most quota barriers, giving small islands wider access to large retail chains. Parallel reforms in selected Asia-Pacific economies open high-value niches for varietals that were previously unviable due to duties. Exporters that couple duty-free access with modern ripening facilities capture early-mover advantages, yet stringent phytosanitary standards still filter out growers who lack compliance certification. Over the long term, smoother trade channels reduce landed costs, stimulate origin diversification, and reinforce the banana market as one of the most globally traded produce segments.

Rapid Expansion of Supermarket Private Labels

European and North American grocers intensify their private-label banana programs to cement shopper loyalty and lift produce margins by 15–25% over national brands. Contractual volumes give mid-tier farms predictable revenue, spurring capital upgrades in irrigation and post-harvest handling. Private-label procurement emphasizes transparency through QR-based traceability, which pressures packers to digitize inventory data and pesticide logs. Retailers leverage exclusive labels to showcase ethical sourcing, organic, fair-trade, and Rainforest Alliance, shifting competition from price to purpose. As more volume migrates into private signatures, traditional spot-market distributors may lose share, further concentrating volumes into vertically integrated pipelines governed by retail specification scorecards.

Emerging Cold-Chain Hubs

Investments in temperature-controlled infrastructure, typified by Edeka’s Hamburg center with 50 state-of-the-art ripening rooms, cut shrink and extend shelf life. New African facilities backed by public-private financing target a 50–70% reduction in post-harvest losses. In Southeast Asia, modern packhouses integrate forced-air precoolers and TarpLess ripening technology to stabilize color stages, unlocking longer transit windows. Investments in Kenya, Tanzania, and Ghana aim to cut post-harvest loss rates by more than half through solar-powered packhouses and cluster-based consolidation hubs[2]Source: United Nations Development Programme, “Horticulture Storage and Transport Infrastructure,” undp.org. Advanced hubs not only boost export volumes but also upgrade domestic retail quality, thereby spurring in-country demand for class-one bananas and supporting broader growth in the banana market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Incidence of Panama Disease TR4 | -1.2% | Global, with a severe impact in Southeast Asia and spreading to South America | Long term (≥ 4 years) |

| Volatile freight rates and container shortages | -0.8% | Global, particularly affecting long-distance trade routes | Short term (≤ 2 years) |

| Stricter pesticide residue regulations in Europe | -0.6% | Europe and exporters to European markets | Medium term (2-4 years) |

| Rising labor activism in South American plantations | -0.4% | South America, with spillover effects on global supply | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Incidence of Panama Disease TR4

Tropical Race 4 poses an existential biological threat to Cavendish plantations across Asia, Australia, and, more recently, parts of North America. The pathogen remains latent in soil for decades, forcing farms to adopt quarantine trenches, disinfectant footbaths, and crop-rotation schemes. These biosecurity layers elevate unit costs and discourage greenfield expansion in high-risk zones. Breeders are trialing resistant cultivars, yet commercial roll-out remains years away, thereby holding back plantation investment and tempering growth in the banana market.

Volatile Freight Rates and Container Shortages

Spot freight quotes for refrigerated containers doubled in several key corridors during 2024 peaks, erasing thin exporter margins[3]Source: United Nations Conference on Trade and Development, “Freight rates remain elevated in first half of 2024,” unctad.org. Smallholders dependent on brokers could not hedge freight risk, triggering shipment postponements and spoilage. Although rates cooled in early 2025, forward contracts now carry surcharge clauses tied to fuel indexes, cementing higher baseline costs. Larger multinationals cushion volatility via long-term vessel charters, but ongoing uncertainty still weighs on the banana market’s profit profiles.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Geography Analysis

Asia-Pacific led with 48.20% of the banana market share in 2025, while Africa is forecast to record a 5.63% CAGR through 2031. Asia-Pacific retains primacy in both cultivation scale and local demand, delivering nearly half of global trade crates. While China scaled back imports, urban Indian households lifted fresh-fruit spend, and Indonesian supermarkets expanded controlled-temperature displays, muting the overall regional drag. India’s exporter INI Farms signed a direct farm-to-retail deal with LuLu Group to stock outlets across the Gulf, proving that outbound flows can coexist with robust domestic pull. Continuous growth in Vietnam’s shipments also reflects the low-land freight and tariff headroom available to regional producers, reinforcing the banana market’s strategic shift toward regional sourcing.

Africa’s growth narrative centers on untapped consumption and supply potential. Kenyan consumer-oriented food imports topped, underlining the appetite for ready-to-eat fruit. Tanzania plans to more than double horticulture output, backed by road and cold-store projects open to blended finance. Multinational retailers scout sourcing nodes in Uganda and Rwanda, encouraged by new packhouses and wider airline cargo links. These initiatives collectively sharpen Africa’s role from subsistence producer to competitive export origin, providing new depth to the banana market.

Europe and North America illustrate maturity and premiumization. Growth relies on higher-value organic, fair-trade, and functional spin-offs, not sheer volume. European Union policy updates on pesticides drive continuous agronomic innovation among South American exporters, who respond with integrated pest management and digital traceability. North American chains pilot carbon-footprint labels, giving suppliers with renewable energy credentials a clear advantage. The Middle East, led by the United Arab Emirates in banana imports, acts as a redistribution hub for North African and Gulf states. South America, despite disease and labor headwinds, leverages cost-efficient land, favorable weather, and established logistics to remain a crucial pillar of the banana market.

Recent Industry Developments

- November 2024: Edeka opened its new USD 65.4 million Fruchtkontor Nord distribution hub in Hamburg, featuring 50 banana-ripening rooms and capacity to handle over 240,000 pallets annually of imported tropical fruits.

- January 2024: INI Farms signed a memorandum of understanding with LuLu Group International to establish direct farm-to-retail partnerships for Indian Cavendish bananas, extending existing collaboration to include year-round supply from Maharashtra and Andhra Pradesh farmers.

- January 2024: THACO Agri launched an integrated agricultural project in Laos, encompassing 8,000 hectares for banana cultivation within a 27,384-hectare development that combines fruit farming, cattle operations, and processing facilities.

Global Banana Market Report Scope

Bananas are tropical fruits with soft pulpy flesh enclosed in a soft, usually yellow, rind with an elongated shape and tapering end. Bananas are produced by several kinds of large herbaceous flowering plants in the genus Musa, which grow in clusters hanging from the top of the plant.

The global banana market is segmented by geography (North America, Europe, Asia-Pacific, South America, and Africa). The study offers the market sizing in terms of volume in metric tons and value in USD thousand.

| North America | United States |

| Canada | |

| South America | Ecuador |

| Colombia | |

| Brazil | |

| Europe | Germany |

| Netherlands | |

| Russia | |

| Asia-Pacific | India |

| China | |

| Indonesia | |

| Philippines | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Africa | Egypt |

| Kenya |

| By Geography | North America | United States |

| Canada | ||

| South America | Ecuador | |

| Colombia | ||

| Brazil | ||

| Europe | Germany | |

| Netherlands | ||

| Russia | ||

| Asia-Pacific | India | |

| China | ||

| Indonesia | ||

| Philippines | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Africa | Egypt | |

| Kenya | ||

Key Questions Answered in the Report

What is the forecast value of the banana market by 2031?

The banana market is expected to reach USD 183.43 billion by 2031.

How fast is Africa's banana consumption growing?

Africa's segment is projected to rise at a 5.63% CAGR through 2031, driven by urbanization and better cold-chain access.

Why are supermarket private labels important for banana suppliers?

Private-label programs provide long-term volume contracts, higher retail margins, and strong incentives for growers to meet strict sustainability standards.

What is Panama Disease TR4 and why does it matter?

TR4 is a soil-borne fungus that can devastate Cavendish plantations, imposing costly biosecurity measures and threatening supply continuity.

Which region currently holds the largest banana market share?

Asia-Pacific leads with 48.20% share of the banana market due to high production and consumption levels.

Page last updated on: