Magnesium Compounds Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

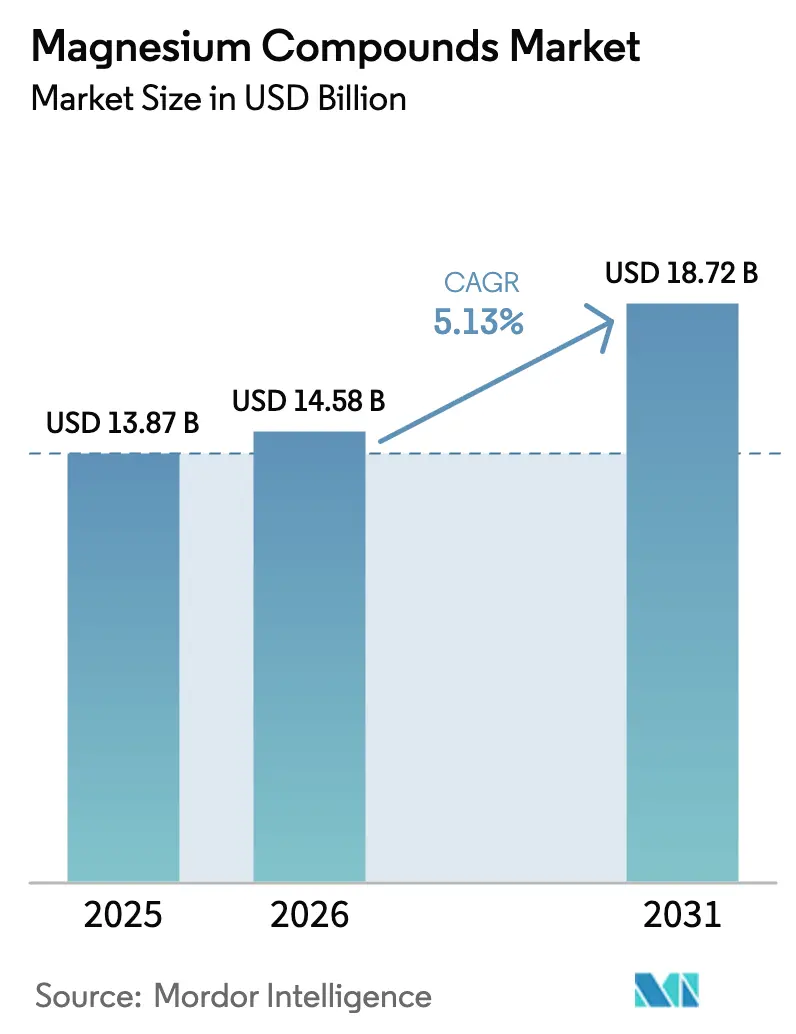

| Market Size (2026) | USD 14.58 Billion |

| Market Size (2031) | USD 18.72 Billion |

| Growth Rate (2026 - 2031) | 5.13% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Magnesium Compounds Market Analysis by Mordor Intelligence

The Magnesium Compounds Market size is projected to expand from USD 13.87 billion in 2025 and USD 14.58 billion in 2026 to USD 18.72 billion by 2031, registering a CAGR of 5.13% between 2026 to 2031. Refractory demand still drives volume, yet higher growth now comes from electrical and electronics applications because fire-safety rules and battery thermal-management needs boost magnesium hydroxide usage. Desalination-brine valorization is trimming feedstock costs below USD 200 per tonne in the Middle East and Australia, giving seawater-sourced material a 6.18% growth path that challenges the dominance of natural brines. Supply security has risen on executive agendas since the March 2024 bankruptcy of US Magnesium, which eliminated the only United States primary producer and widened dependence on Chinese exports. Low-carbon electrolysis projects in Europe and North America are attracting premium contracts from auto and electronics buyers eager to decarbonize.

Key Report Takeaways

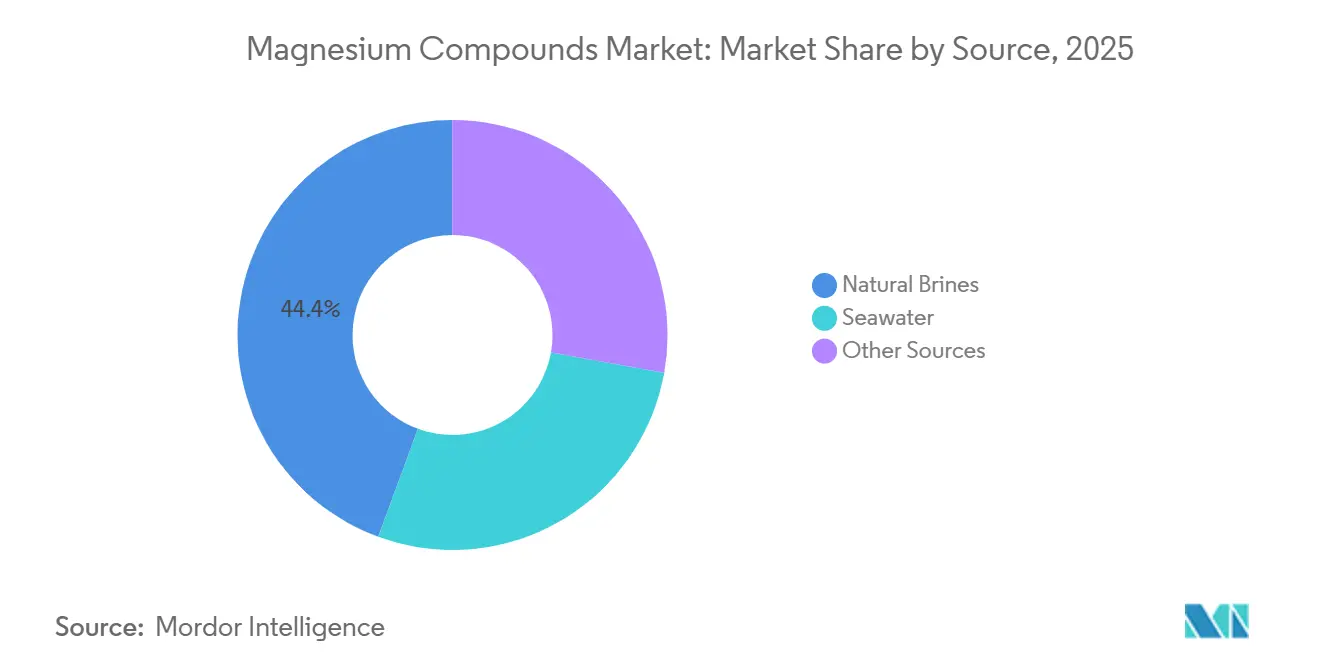

- By source, natural brines accounted for 44.38% of the magnesium compounds market share in 2025, while seawater-based production is the fastest-growing source at a 6.18% CAGR through 2031.

- By product type, inorganic chemicals led with 71.46% revenue share in 2025; organic magnesium salts record the highest projected CAGR at 6.24% to 2031.

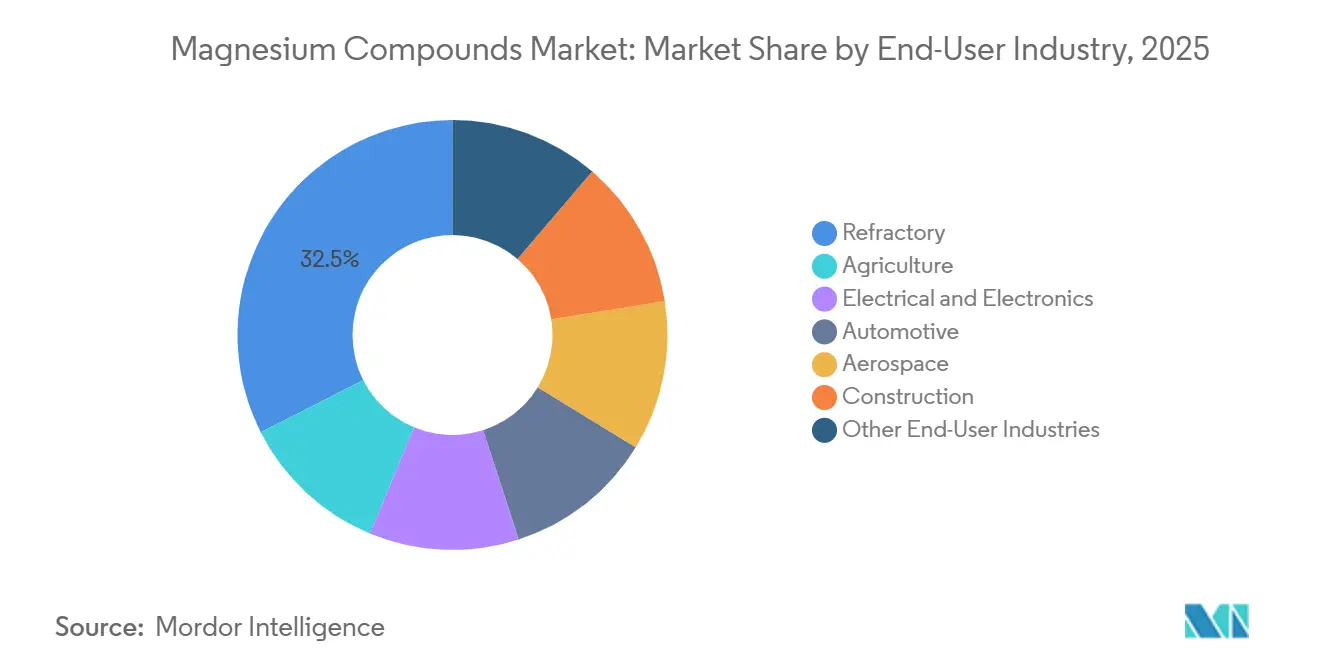

- By end-user industry, refractories held 32.47% of the magnesium compounds market size in 2025, whereas electrical and electronics is advancing at a 6.31% CAGR to 2031.

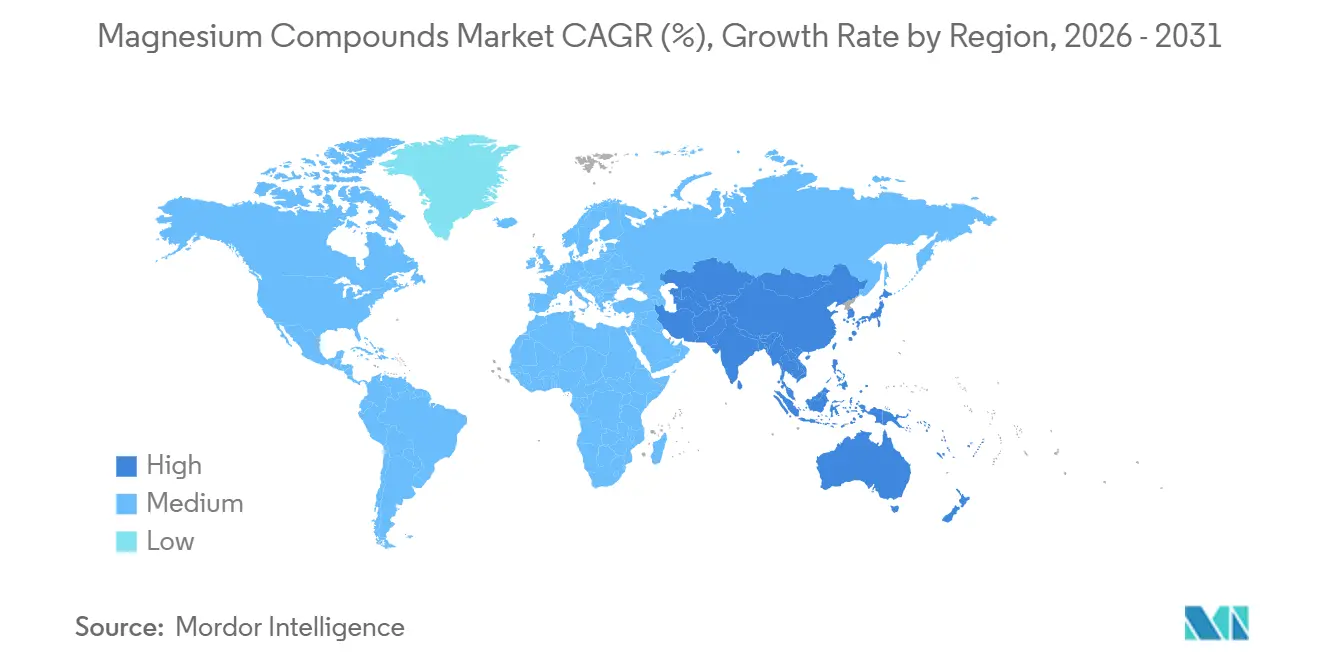

- By geography, Asia-Pacific commanded 53.28% of the 2025 value, and at 5.94% it remains the fastest expanding regional segment to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Magnesium Compounds Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Booming refractory demand from reviving global steel output | +1.2% | Asia-Pacific core, spill-over to Europe and Middle East | Medium term (2-4 years) |

| Stringent wastewater and flue-gas norms spurring Mg-based environmental reagents | +0.9% | Global, early enforcement in North America and EU | Short term (≤ 2 years) |

| Soil-magnesium depletion accelerating fertilizer-grade Mg salts usage | +0.7% | North America, South America, Asia-Pacific | Long term (≥ 4 years) |

| Desalination-brine valorization unlocking ultra-low-cost Mg feedstocks | +0.6% | Middle East, Australia, California | Medium term (2-4 years) |

| Rapid adoption of low-carbon magnesium-phosphate cements | +0.5% | Europe, Asia-Pacific, North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Booming Refractory Demand from Reviving Global Steel Output

In early 2025, crude steel production saw a year-on-year increase. However, in 2024, prices for refractory-grade magnesia dipped, a decline attributed to persistently high inventories in Liaoning. While Indian capacity additions received approval in 2024, they are expected to start influencing refractory orders after the typical 18-to-24-month delay. Electric-arc furnaces, accounting for a significant portion of global steel output, are known to shorten lining life, consequently increasing the frequency of brick replacements. RHI Magnesita reported an uptick in Asian refractory consumption, contrasting with stagnant volumes in Europe. The magnesium compounds market stands to gain, as magnesia bricks are crucial for withstanding the heightened thermal shocks associated with EAF operations.

Stringent Wastewater and Flue-Gas Norms Spurring Mg-Based Environmental Reagents

In April 2024, the U.S. EPA mandated a sulfur-dioxide capture rule for primary magnesium refiners, compelling plants to adopt magnesium-oxide scrubbers that also function as product-recovery systems[1]U.S. Environmental Protection Agency, “National Emission Standards for Hazardous Air Pollutants,” EPA.GOV. In 2025, Europe imposed stricter phosphorus discharge limits on municipal wastewater, favoring magnesium hydroxide over lime due to its ability to reduce sludge volumes. In 2025, Israel Chemicals announced increased sales of magnesium hydroxide slurry to EU utilities, attributing the success to their ISO 14001-certified output. With similar policies emerging in Asia, there's a growing expectation that environmental-grade magnesium compounds will command premium prices and capture additional market volumes.

Soil-Magnesium Depletion Accelerating Fertilizer-Grade Mg Salts Usage

In 2024, USDA field work revealed that maize and soybean yields declined when soil magnesium levels dipped below 50 ppm. The issue worsened with high-potassium fertilizer regimens, leading agronomists to advocate for magnesium sulfate side-dress applications. In 2025, TIMAB Magnesium introduced a coated oxide granule that boosted nutrient-use efficiency in trials with Brazilian soybeans. While fertilizer buyers remain sensitive to prices, the market penetration of magnesium compounds is poised to rise, driven by the increasing prevalence of remote sensing and soil-testing services.

Desalination-Brine Valorization Unlocking Ultra-Low-Cost Mg Feedstocks

In 2024, global desalination plants released brine daily, containing magnesium. Magrathea Metals, leveraging coastal wind power, extracts magnesium hydroxide from Pacific seawater through colocated electrolysis. Verde Magnesium is investing in a Romanian venture, aiming to launch a plant by 2027. This facility is designed to comply with EU Carbon Border regulations, boasting a low carbon footprint. Collectively, these initiatives expand the raw material landscape for the magnesium compounds sector and help stabilize feedstock costs.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price-sensitive substitution by Ca or Al compounds | -0.8% | Global, acute in South Asia and Africa | Short term (≤ 2 years) |

| Supply-chain volatility driven by China-centric production | -0.7% | North America and Europe | Medium term (2-4 years) |

| ESG scrutiny of Pidgeon-route carbon footprint | -0.5% | Asia-Pacific, Europe, North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Price-Sensitive Substitution by Ca or Al Compounds in Several End-Uses

Calcium carbonate is about half the cost of light-burned magnesia and is the go-to filler when flame retardancy isn't a priority[2]U.S. Geological Survey, “Mineral Commodity Summaries 2025,” USGS.GOV. In 2025, aluminum hydroxide commanded a dominant share of the global flame-retardant market, bolstered by longstanding certifications. While construction budgets in India and Southeast Asia lean towards locally sourced lime for water treatment, opting for it over imported magnesium hydroxide, there are noted performance trade-offs. These economic choices result in a deduction from the baseline CAGR.

Supply-Chain Volatility Driven by China-Centric Production and Energy Costs

In 2024, coal prices at Qinhuangdao fluctuated, impacting production costs, even as Liaoning province accounted for a significant share of Europe's magnesia imports. Following the bankruptcy of US Magnesium, buyers turned to imports, now subject to tariffs until 2026. Late in 2024, freight costs from Dalian to Rotterdam surged, doubling in price, as container availability was compromised by diversions in the Red Sea. Such market volatility undermines buyer confidence, leading to delays in long-term contracts and a consequent growth restraint.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source: Natural Brine Scale vs. Seawater Disruption

Natural brines held 44.38% of the 2025 volume and remain the low-cost base for commodity magnesia, anchored by Dead Sea operations. Seawater-derived output, while a mid-teen share today, is set for 6.18% annual growth as electrolysis costs fall and ESG audits favor its lower carbon footprint.

The magnesium compounds market benefits from this dual structure because high-purity products can be sourced from seawater without displacing large-scale brine evaporation assets. Magrathea Metals showed that seawater operating costs already undercut Great Salt Lake brine in pilot runs. If coastal projects replicate at scale, commodity suppliers may pivot excess brine capacity toward refractory grades while seawater plants serve electronics and pharma buyers.

By Product Type: Organics Move Up the Value Chain

Inorganic chemicals commanded 71.46% of revenue in 2025, supported by refractory bricks, environmental reagents, and fertilizers. Organic magnesium compounds expanded 6.24% per year because FDA-cleared drugs rely on magnesium stearate, while nutraceutical brands market chelated forms at premium prices.

The magnesium compounds market size linked to organic grades is small but profitable. In 2025, pharmaceutical-grade stearate prices remain high, largely due to the entry hurdles posed by GMP certification. TIMAB’s controlled-release oxide blurs the inorganic-organic divide by adding coating technology that raises nutrient-use efficiency.

By End-User Industry: Electronics Outpace Refractories

Refractories took 32.47% of 2025 demand, tied to steel and cement cycles. Electrical and electronics applications now grow at 6.31% a year, fueled by halogen-free fire standards in EV battery packs and the thermal conductivity needs of 5G equipment.

The magnesium compounds market share for flame-retardant hydroxide will broaden as regulators tighten rules on brominated additives. In 2025, Japanese fabs boosted their purchases of semiconductor-grade MgO, highlighting a shift towards sourcing high-purity supplies.

Geography Analysis

Asia-Pacific supplied 53.28% of the 2025 value and should grow 5.94% to 2031 despite Liaoning’s capacity freeze. India’s new steel projects and Japan’s specialty-grade exports offset slower Chinese construction.

After the shutdown at the Great Salt Lake, North America faced tighter supply but maintained a significant market share. Despite facing tariffs on imports, buyers are still willing to pay a premium for non-Chinese supplies. This scenario is paving the way for seawater ventures to flourish along the Pacific coast.

Europe's market share largely hinges on Nedmag’s operations in the Netherlands and the upcoming Verde Magnesium plant. Set to launch in the coming years, this plant is poised to reduce Europe's import dependency. Meanwhile, South America and the Middle East, driven by Brazilian fertilizer needs and brine projects in the Gulf Cooperation Council (GCC), together account for a notable portion of the market.

Competitive Landscape

The magnesium compounds market is fragmented in nature. Low-carbon entrants are making significant strides. Verde Magnesium has secured funding for a sub-5 kg CO₂ electrolysis route in Romania. In California, Magrathea Metals is running a pilot project powered by coastal wind energy. Tateho Chemical and Ube Industries have established dominance in semiconductor-grade oxides, thanks to their ability to consistently meet impurity specifications of less than 10 ppm. Patents related to brine valorization and electrodialysis have increased. Chinese firms are at the forefront of bulk extraction methods, while Japanese entities are honing in on high-purity oxide synthesis. These developments suggest a magnesium compounds market that's split: commodity volumes are benefiting from scale, while specialty grades are leaning towards process innovation.

Magnesium Compounds Industry Leaders

RHI Magnesita

Magnezit Group

Grecian Magnesite

Martin Marietta Magnesia Specialties

Israel Chemicals Ltd. (ICL)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Verde Magnesium, a strategic initiative under the EU's CRM Act, is set to mark Europe's return to magnesium production after a 25-year hiatus, championing a sustainable and low-carbon extraction method. The Verde Magnesium project inches closer to reviving Europe's magnesium metal production.

- April 2024: PMAP Mine Water Corp and Baymag Inc. signed a letter of intent to co-develop AI-controlled magnesium-oxide systems for mine wastewater treatment, targeting compliance with new EPA pollutant caps.

Global Magnesium Compounds Market Report Scope

Magnesium forms a number of useful compounds in industry and biology, such as magnesium carbonate, magnesium chloride, magnesium citrate, magnesium hydroxide, and others. Magnesium and magnesium compounds are produced from saltwater, well brines, lake brines, bitterns, and minerals. Magnesium compounds have a wide range of applications in agriculture, healthcare, chemicals, construction, and other industries.

The magnesium compounds market is segmented by source, product type, end-user industry, and geography. By Source, the market is segmented into seawater, natural brines, and other sources. By Product Type, the market is segmented into inorganic chemicals and organic chemicals. By End-User Industry, the market is segmented into agriculture, electrical and electronics, automotive, aerospace, construction, refractory, and other end-user industries. The report also covers the market size and forecasts in 16 countries across major regions. For each segment, market sizing and forecasts have been done on the basis of revenue (USD).

| Seawater |

| Natural Brines |

| Other Sources |

| Inorganic Chemicals |

| Organic Chemicals |

| Agriculture |

| Electrical and Electronics |

| Automotive |

| Aerospace |

| Construction |

| Refractory |

| Other End-User Industries |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN | |

| Oceania | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Source | Seawater | |

| Natural Brines | ||

| Other Sources | ||

| By Product Type | Inorganic Chemicals | |

| Organic Chemicals | ||

| By End-User Industry | Agriculture | |

| Electrical and Electronics | ||

| Automotive | ||

| Aerospace | ||

| Construction | ||

| Refractory | ||

| Other End-User Industries | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN | ||

| Oceania | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

How large is the magnesium compounds market in 2026?

The magnesium compounds market size is USD 14.58 billion in 2026 and is forecast to reach USD 18.72 billion by 2031, registering a CAGR of 5.13%.

Which segment is growing fastest within magnesium compounds?

Electrical and electronics end uses show the highest growth at a 6.31% CAGR, driven by flame-retardant and battery applications.

What share do natural brines hold in the global supply?

Natural brines contributed 44.38% of global production in 2025.

What regulatory trends affect magnesium hydroxide demand?

Tougher wastewater and flue-gas rules, such as the U.S. EPA mandate for 99.5% SO₂ capture, accelerate magnesium hydroxide adoption in environmental applications.

Page last updated on: