Southeast Asia GPU Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

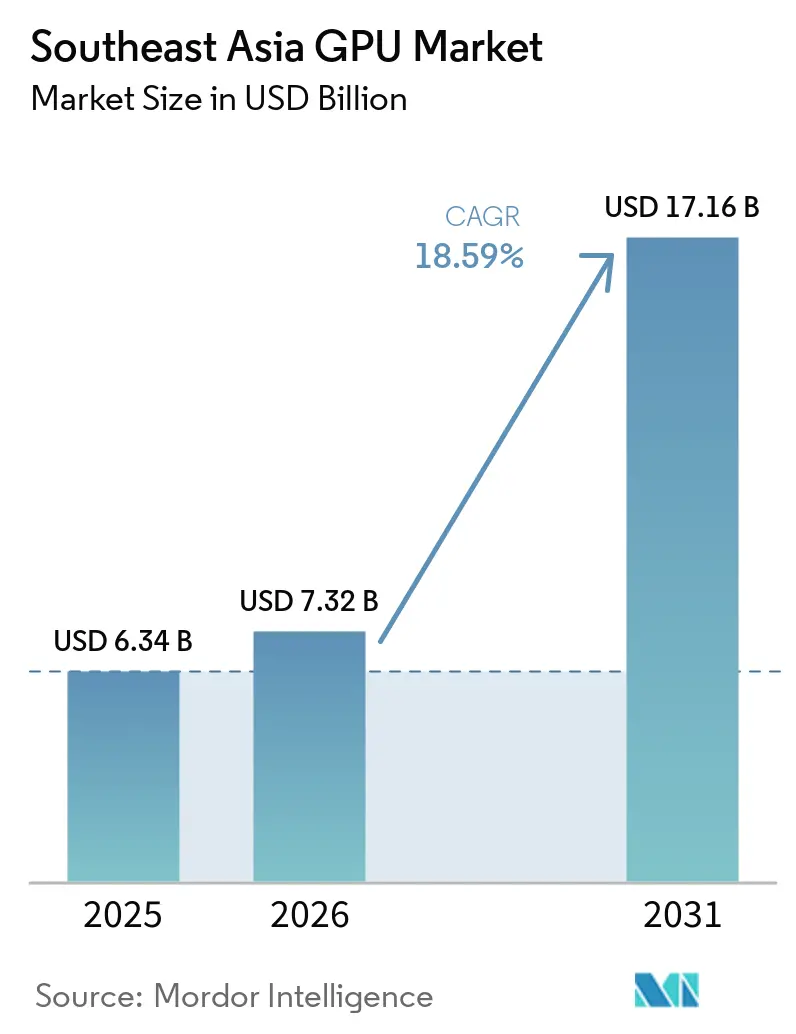

| Base Year Market Size (2025) | USD 6.34 Billion |

| Market Size (2026) | USD 7.32 Billion |

| Market Size (2031) | USD 17.16 Billion |

| Growth Rate (2026 - 2031) | 18.59% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Southeast Asia GPU Market Analysis by Mordor Intelligence

The Southeast Asia GPU market size is expected to increase from USD 7.32 billion in 2026 to USD 17.16 billion by 2031, growing at a CAGR of 18.59% over 2026-2031. The market’s near-term momentum reflects hyperscaler investment in regional availability zones, rising adoption of GPU-accelerated AI workloads, and government incentives directed at semiconductor packaging and testing. Discrete accelerators for inference and training continue to anchor demand, while integrated GPUs in smartphones and PCs expand the total addressable user base. Energy-efficiency regulations, supply-chain volatility, and export quotas shape deployment choices but have not derailed capital-expenditure plans across Singapore, Malaysia, Indonesia, and Thailand.

Key Report Takeaways

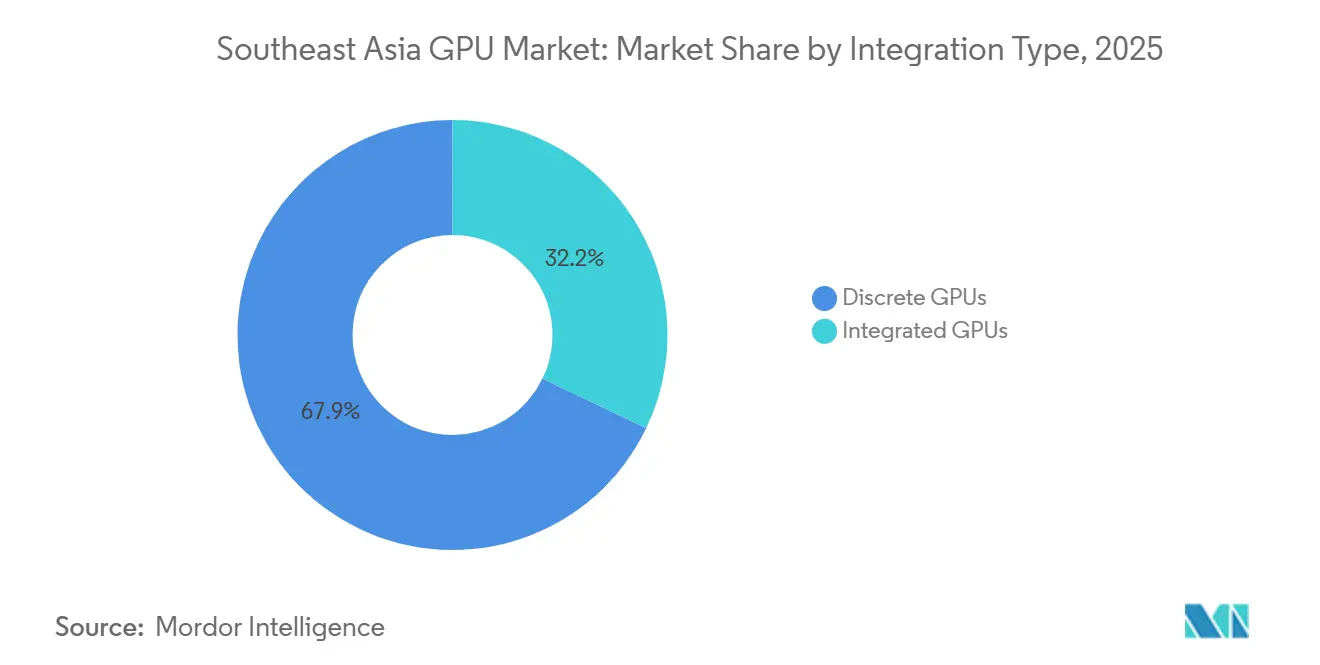

- By integration type, discrete GPUs led with 67.85% of the Southeast Asia GPU market share in 2025 and are projected to expand at a 19.11% CAGR through 2031.

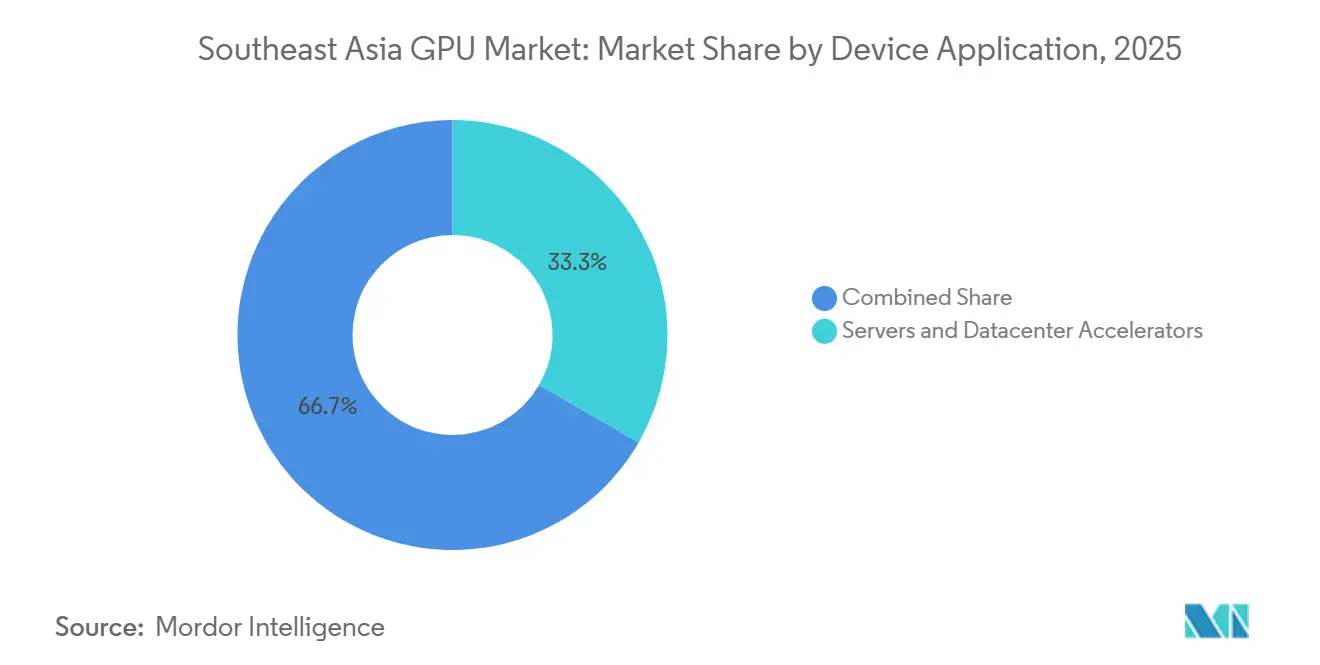

- By device application, servers and datacenter accelerators captured 33.34% of the Southeast Asia GPU market in 2025 and are expected to grow at a 19.23% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Southeast Asia GPU Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for High-Performance Computing in Data Centers | 5.80% | Singapore, Malaysia, Indonesia, Thailand, Vietnam | Medium term (2-4 years) |

| Rapid Adoption of Cloud Gaming and Online Esports | 3.20% | Singapore, Thailand, Indonesia, Philippines | Short term (≤ 2 years) |

| Expansion of AI-Powered Content Creation for Social Commerce | 3.50% | Indonesia, Thailand, Vietnam, Philippines, Singapore | Medium term (2-4 years) |

| Growth of Mobile Gaming Ecosystem in Southeast Asia | 2.40% | Indonesia, Philippines, Vietnam, Thailand, Malaysia | Short term (≤ 2 years) |

| Government Incentives for Local Semiconductor Packaging and Testing | 2.10% | Singapore, Malaysia, Vietnam, Indonesia | Long term (≥ 4 years) |

| Increasing Graphics Requirements for AAA PC and Console Titles | 1.60% | Singapore, Malaysia, Thailand | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Demand for High-Performance Computing in Data Centers

Hyperscalers have started localizing compute clusters to satisfy data-residency mandates and reduce latency for generative AI inference. Microsoft Azure rolled out ND GB200-v6 instances in Malaysia and Indonesia in 2025, while Google Cloud launched a Bangkok region with A3 nodes powered by H100 GPUs the same year.[1]Google LLC, “Google Cloud Opens Bangkok Region,” cloud.google.com YTL Power International broke ground on a 500 MW AI campus in Johor, scheduled for 2027 completion, and regional colocation providers are retrofitting halls with liquid cooling. These moves establish Southeast Asia as a first-tier inference hub rather than a spoke served out of Singapore.

Rapid Adoption of Cloud Gaming and Online Esports

Fiber-to-the-home penetration and nationwide 5G coverage have enabled sub-20 ms gameplay for subscription-based cloud gaming services. Radian Arc and Singtel-Razer pilots moved from trial to commercial launch during 2024-2025, with monthly pricing under USD 10 proving critical for scale.[2]Radian Arc, “Launching Southeast Asia Cloud Gaming Platform,” radianarc.io Esports’ inclusion as a medal event in the Southeast Asian Games 2025 triggered public-sector investment in GPU-equipped training centers, spurring near-term purchases of workstation-class cards across Thailand and the Philippines.

Expansion of AI-Powered Content Creation for Social Commerce

Retailers on platforms such as TikTok Shop and Shopee are adopting GPU-accelerated generative AI tools to automate imagery, copy, and recommendation flows. ByteDance allocated USD 23 billion to AI infrastructure in 2025, deploying H200 GPUs across Southeast Asian data centers.[3]ByteDance Ltd., “ByteDance Invests USD 23 Billion in AI Infrastructure,” bytedance.com True Corporation used GTC 2026 to highlight real-time multilingual translation at the network edge, indicating telecom operators’ entry into GPU provisioning for enterprise clients.

Growth of Mobile Gaming Ecosystem in Southeast Asia

MediaTek’s Dimensity 9500s introduces hardware ray tracing to sub-USD 400 smartphones, while the Dimensity 8500 delivers 25% higher graphics throughput at 20% lower power draw.[4]MediaTek Inc., “MediaTek Dimensity 9500s Product Brief,” mediatek.com Sustained frame rates above 110 fps in 35 °C outdoor conditions make these devices viable for esports tournaments in Indonesia and the Philippines, markets where installment plans dominate handset purchases.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Global GPU Supply Chain Disruptions and Chip Shortages | -3.40% | Global, acute in Singapore, Malaysia, Indonesia | Short term (≤ 2 years) |

| Rising Average Selling Prices Limiting Entry-Level Adoption | -2.80% | Indonesia, Philippines, Vietnam, Thailand | Short term (≤ 2 years) |

| Energy Cost Sensitivity of Emerging Country Data Centers | -1.60% | Indonesia, Philippines, Vietnam, Myanmar | Medium term (2-4 years) |

| Regulatory Scrutiny on Cryptocurrency Mining in Key Markets | -1.20% | Malaysia, Thailand, Vietnam, Laos | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Global GPU Supply Chain Disruptions and Chip Shortages

HBM3E memory remained constrained through 2025, compelling NVIDIA and AMD to ration flagship accelerators to hyperscalers on multi-year contracts. Lead times for regional cloud providers stretched beyond six months, and CoWoS packaging capacity at TSMC exceeded 90% utilization. U.S. export controls imposed a 50,000-unit ceiling on datacenter GPUs shipped to Indonesia for 2025-2027, forcing enterprises to emphasize inference over training.

Rising Average Selling Prices Limiting Entry-Level Adoption

Between 2024 and 2025, retail premiums ranged from 20% to 90% above MSRP across major e-commerce sites. A USD 399 RTX 4060 Ti is listed at USD 550-650 in Indonesia, while AMD’s RX 7600 XT carries 30-40% markups in Vietnam. These premiums extended refresh cycles for SMEs by up to 18 months, limiting penetration in creative studios and indie game developers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Integration Type: Discrete GPUs Extend Performance Advantage

Discrete units controlled 67.85% of the Southeast Asia GPU market in 2025, a position amplified by datacenter clusters built around NVIDIA H200 and AMD MI325X accelerators. The Southeast Asia GPU market size for discrete units is on track to expand at a 19.11% CAGR through 2031 as hyperscalers lock in multi-year supply agreements. YTL Power International’s 500 MW Johor facility alone plans to host tens of thousands of cards, while automotive OEMs such as Volvo integrate dual Drive AGX Orin boards that deliver 254 TOPS per vehicle.

Smaller but rising, integrated GPUs ride smartphone and AI PC shipments. MediaTek’s 9500s embeds an Immortalis-G925 core with hardware ray tracing, trimming the gap with entry-level discrete boards. Qualcomm’s Snapdragon 8 Gen 3 and MediaTek’s 8500 sustain 60 fps on popular mobile titles, underscoring that integrated silicon now handles workloads once reserved for add-in cards.

By Device Application: Servers and Datacenter Accelerators Propel Revenue

Servers and accelerators accounted for 33.34% of the Southeast Asia GPU market share in 2025 and exhibit the highest growth trajectory, with a 19.23% CAGR out to 2031. Azure’s ND GB200-v6 and Google Cloud’s A3 instances anchor this uptrend, delivering 1.4 exaFLOPS per rack and enabling sub-10 ms inference for trillion-parameter models. Equinix SG6, opened in 2025, features liquid-cooled colocation bays specifically designed for multi-GPU clusters, illustrating colocation demand beyond hyperscalers.

Desktop and workstation refreshes remain steady as content creators embrace real-time ray tracing in RTX 50-series and Radeon RX 9070 XT boards. Meanwhile, mobile devices dominate shipment volumes but contribute less to revenue because integrated GPUs command lower average selling prices. Automotive ADAS and edge appliances are emerging as niche yet strategic domains, driven by export quotas that push compute closer to the data source.

Geography Analysis

Singapore leads the Southeast Asia GPU market, benefiting from mature colocation ecosystems and the USD 28.5 billion Research, Innovation and Enterprise 2025 program. Equinix SG6, inaugurated in 2025, offers 400 Gbps interconnects and liquid cooling, meeting stringent latency and thermal requirements for GPU clusters. Imminent Minimum Energy Performance Standards, effective July 2026, will require import registration and labeling, potentially favoring energy-efficient architectures over high-wattage accelerators.

Malaysia registers the fastest CAGR thanks to YTL Power International’s 500 MW AI campus and GIBO Malaysia’s 14,000-GPU build-out, both slated for 2027 completion. The National Semiconductor Strategy earmarks USD 5.3 billion for packaging and testing, positioning Malaysia as a supply-chain complement to Singapore’s colocation dominance. Microsoft Azure’s ND GB200-v6 rollout in 2025 further cements Malaysia as a regional AI node.

Indonesia follows closely, buoyed by the February 2026 semiconductor roadmap and the Indonesia Chip Design Collaborative Center. Microsoft Azure’s local ND GB200-v6 availability and NVIDIA’s AI Center of Excellence enrich the developer ecosystem. Nevertheless, the 50,000-unit datacenter GPU quota for 2025-2027 encourages enterprises to prioritize inference-optimized GPUs and edge deployments to circumvent supply constraints.

Thailand and Vietnam form the mid-tier. Google Cloud’s Bangkok region, operational since 2025, and Telehouse’s Bangkok expansion enhance Thailand’s latency profile for cloud gaming and AI workloads. Vietnam attracts GPU-centric R&D, with NVIDIA inaugurating an AI software center in 2025. Although industrial electricity rates hover near USD 0.08 per kWh, operators still weigh energy costs when sizing GPU clusters. The Philippines and Myanmar represent emerging opportunities centered on integrated GPUs in mobile gaming, supported by carrier subsidies and rising smartphone penetration.

Competitive Landscape

Datacenter accelerators are concentrated, with NVIDIA controlling roughly 80% share, while consumer graphics and mobile GPUs remain fragmented among AMD, Intel, MediaTek, and Qualcomm. NVIDIA deepened its moat by aligning CUDA software with regional language models and sealing a multi-year supply and co-development pact with YTL Power International in 2025. AMD answers with value-priced Radeon RX 9070 XT cards that undercut NVIDIA equivalents by USD 200, targeting cost-sensitive creators and gamers.

Intel straddles both integrated and discrete arenas. Its partnership with NVIDIA on AI PC platforms, announced in 2025, signals a collaborative stance even as Arc discrete GPUs and Xe iGPUs pursue standalone mindshare. MediaTek’s tie-up with NVIDIA embeds RTX features into AI PC chipsets, illustrating convergence between laptop and desktop graphics. Qualcomm counters with Snapdragon 8 Gen 3, tuned for sustained ray-traced gaming without active cooling.

Regulation shapes competitive tactics. The 50,000-unit cap for Indonesia elevates vendors that can supply mid-range inference accelerators or power-efficient integrated GPUs. Automotive ADAS emerges as a white-space battleground, where NVIDIA’s dual Drive AGX Orin design-win in Volvo’s EX90 in 2025 showcases the blend of infotainment and autonomous compute poised for replication across EV models in Southeast Asia.

Southeast Asia GPU Industry Leaders

NVIDIA Corporation

Advanced Micro Devices, Inc.

Intel Corporation

Qualcomm Technologies, Inc.

Samsung Electronics Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: The U.S. Department of Commerce proposed export rules requiring pre-approval for projects exceeding 200,000 GPUs, potentially slowing mega-scale Southeast Asian builds.

- February 2026: Indonesia’s Ministry of Industry finalized the Indonesia Chip Design Collaborative Center with Polytron and 13 universities to nurture local design talent.

- January 2026: Singapore’s National Environment Agency concluded consultation on extending Minimum Energy Performance Standards to GPUs, effective July 2026.

- January 2026: MediaTek unveiled the Dimensity 9500s and 8500 SoCs, bringing hardware ray tracing and improved power efficiency to midrange and flagship smartphones.

Southeast Asia GPU Market Report Scope

The Southeast Asia GPU Market Report is Segmented by Integration Type (Integrated GPUs, Discrete GPUs), and Device Application (Mobile Devices and Tablets, PCs and Workstations, Servers and Datacenter Accelerators, Gaming Consoles and Handhelds, Automotive and ADAS, Other Embedded and Edge Devices). The Market Forecasts are Provided in Terms of Value (USD).

| Integrated GPUs (iGPU) |

| Discrete GPUs (dGPU) |

| Mobile Devices and Tablets |

| PCs and Workstations |

| Servers and Datacenter Accelerators |

| Gaming Consoles and Handhelds |

| Automotive / ADAS |

| Other Embedded and Edge Devices |

| By Integration Type | Integrated GPUs (iGPU) |

| Discrete GPUs (dGPU) | |

| By Device Application | Mobile Devices and Tablets |

| PCs and Workstations | |

| Servers and Datacenter Accelerators | |

| Gaming Consoles and Handhelds | |

| Automotive / ADAS | |

| Other Embedded and Edge Devices |

Key Questions Answered in the Report

How large will the Southeast Asia GPU market be by 2031?

It is projected to reach USD 17.16 billion by 2031, expanding at an 18.59% CAGR from 2026.

Which segment grows fastest within regional GPU demand?

Servers and datacenter accelerators post the highest forecast CAGR at 19.23% through 2031.

Which country shows the quickest growth in large-scale GPU deployments?

Malaysia leads growth, supported by a 500 MW AI campus in Johor and a USD 5.3 billion semiconductor strategy.

How do export controls affect Indonesia’s access to datacenter GPUs?

A 50,000-unit ceiling for 2025-2027 forces local firms to prioritize inference GPUs and edge architectures.

What role do mobile GPUs play in overall demand?

Integrated GPUs in smartphones and AI PCs widen the user base, although they contribute less revenue than discrete accelerators.

Why are energy regulations relevant for GPU vendors?

Singapores mandatory energy labeling starting July 2026 will push vendors to highlight power-efficiency to avoid compliance penalties.

Page last updated on: