South Korea Discrete GPU Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

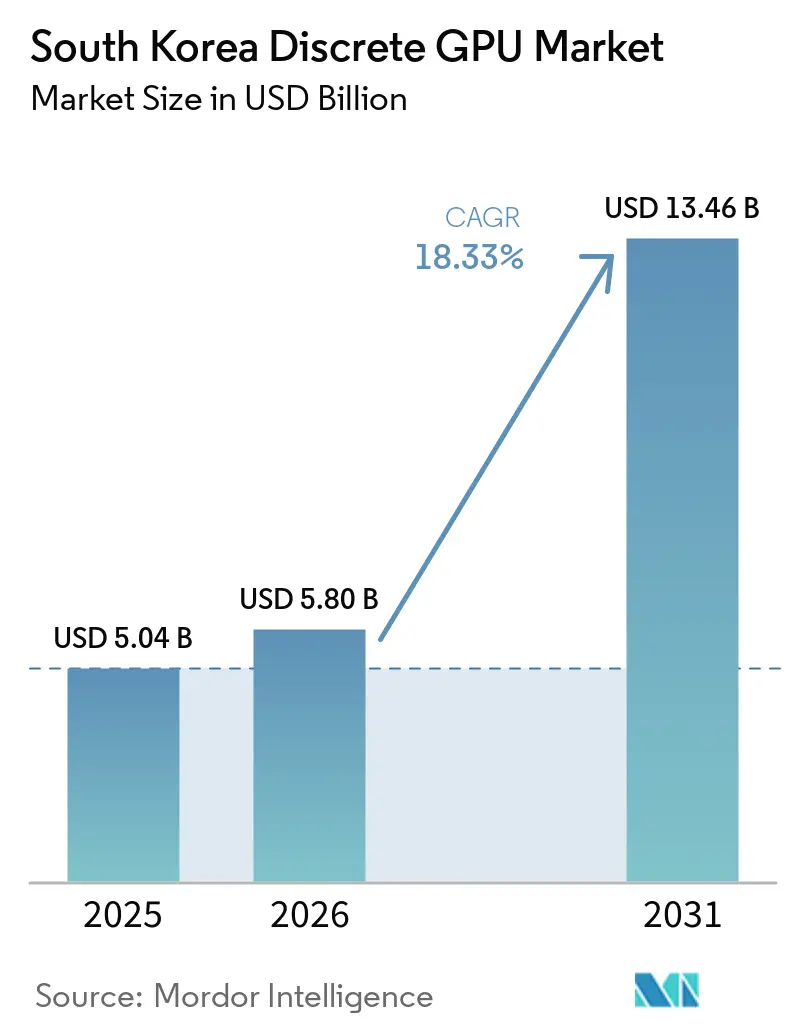

| Base Year Market Size (2025) | USD 5.04 Billion |

| Market Size (2026) | USD 5.80 Billion |

| Market Size (2031) | USD 13.46 Billion |

| Growth Rate (2026 - 2031) | 18.33% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Korea Discrete GPU Market Analysis by Mordor Intelligence

The South Korea discrete GPU market size is projected to be USD 5.04 billion in 2025, USD 5.80 billion in 2026, and reach USD 13.46 billion by 2031, growing at a CAGR of 18.33% from 2026 to 2031. A sovereign-AI push, anchored in the government’s KRW 21 trillion – KRW 30 trillion (USD 16.0 billion – USD 22.8 billion)1 semiconductor and AI stimulus, is accelerating hyperscale deployments and bolstering long-term demand. Servers and datacenter accelerators already dominate the discrete GPU market as enterprises migrate from proof-of-concept pilots to production-grade GPU farms, while gaming culture sustains a sizeable consumer hardware base. Memory innovation is redefining performance ceilings, with domestic HBM4 production positioning Korean suppliers at the center of high-bandwidth AI workloads. Competitive intensity remains elevated: Nvidia retains overwhelming add-in-board share, yet local NPU start-ups are attracting nine-figure funding as policymakers seek to localize critical compute IP.

Key Report Takeaways

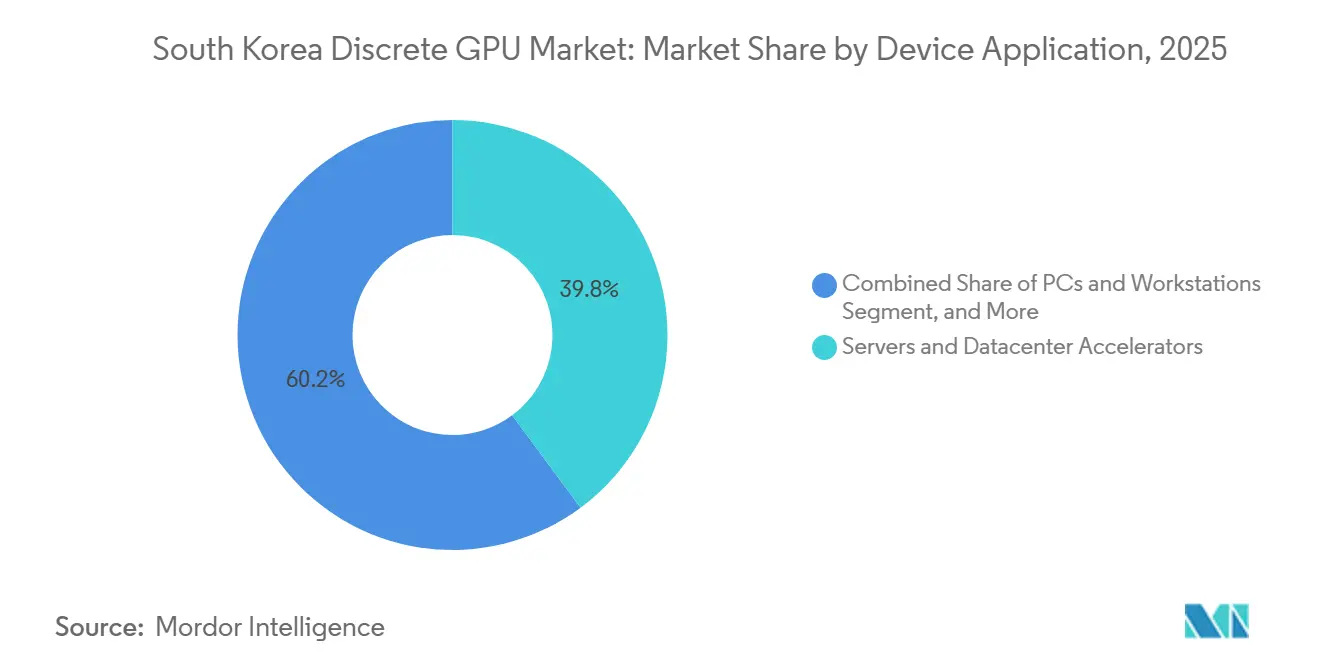

- By device application, servers and datacenter accelerators commanded 39.84% of the discrete GPU market share in 2025 and are advancing at an 18.92% CAGR to 2031.

- By memory type, GDDR-based products led with 71.28% of the discrete GPU market share in 2025, whereas HBM-based GPUs posted the fastest growth at an 18.88% CAGR through 2031.

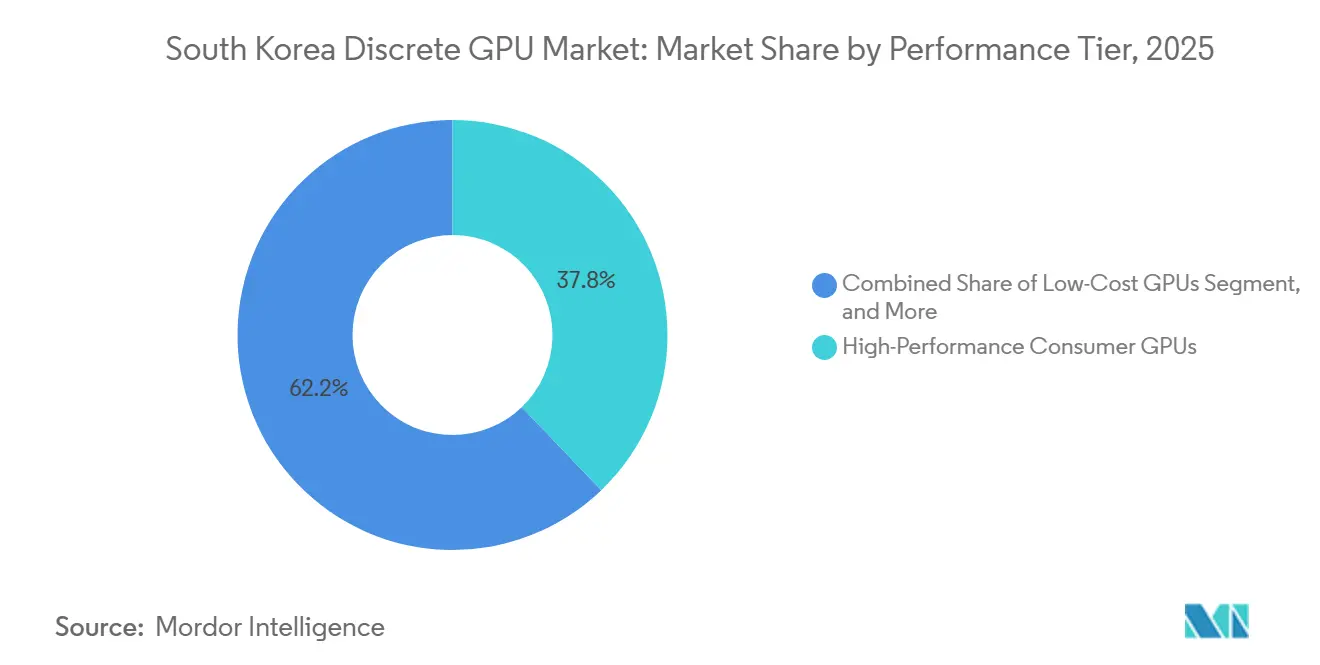

- By performance tier, high-performance consumer GPUs captured 37.83% of the discrete GPU market in 2025, but datacenter and AI accelerators priced above USD 1,200 are progressing at an 18.75% CAGR over the same horizon.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

South Korea Discrete GPU Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Surge in AI and HPC workloads requiring high-performance GPUs | +5.2% | Seoul, Gyeonggi, Busan hubs | Medium term (2–4 years) |

| Growing popularity of PC gaming and esports in South Korea | +2.8% | Seoul, Busan, Incheon metros | Short term (≤ 2 years) |

| Rapid expansion of cloud gaming services | +2.1% | Seoul and Gyeonggi | Medium term (2–4 years) |

| Government incentives for domestic semiconductor design start-ups targeting GPU IP | +3.4% | Pangyo, Seongnam, Pyeongtaek clusters | Long term (≥ 4 years) |

| Adoption of discrete GPUs in next-generation automotive HUDs and cockpit domain controllers | +1.9% | Ulsan and Hwaseong plants | Medium term (2–4 years) |

| Integration of discrete GPUs into edge AI appliances for smart factories | +1.7% | Jeonbuk, Gyeongnam, Chungnam zones | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in AI and HPC Workloads Requiring High-Performance GPUs

Government and enterprise commitments are reshaping procurement behavior, with 13,000 Nvidia Blackwell B200 units already distributed in 2025 and a target of 50,000 GPUs by 2028. Kakao installed 2,040 B200 GPUs across 255 nodes, enabling public beta access in January 2026. Samsung and SK Group are each designing AI factories with more than 50,000 GPUs to automate chip manufacturing and semiconductor R&D. Krafton’s 1,000-unit Blackwell Ultra cluster, equipped with XDR-800G InfiniBand, illustrates private-sector enthusiasm for large language models. These multi-tenant farms use Kubernetes and Slurm to maximize utilization and shift the South Korean discrete GPU market toward hyperscale consumption.[1]Tech-Critter Editorial, “Samsung Plans AI Factory With 50,000 GPUs,” tech-critter.com

Growing Popularity of PC Gaming and Esports in South Korea

NVIDIA launched its RTX 5060 family, priced between USD 299 and USD 429, catering to gamers eager for high refresh rates in titles like Valorant. In its most recent reporting year, the domestic PC gaming sector generated KRW 5.8 trillion (approximately USD 4.4 billion). Meanwhile, as esports activities grow, cafes are upgrading their rigs with ray-tracing GPUs. Additionally, studios such as Krafton are harnessing GPU clusters to accelerate AI-driven content creation, underscoring the growing synergy between gaming and AI infrastructure demands.

Rapid Expansion of Cloud Gaming Services

SK Telecom debuted a subscription GPUaaS platform in January 2025 inside a 44 kW-per-rack Gasan facility, nearly ten times the domestic density norm. Naver Cloud targets more than 60,000 GPUs, allowing idle capacity to stream cloud games at low latency. A National AI Computing Resource Support Portal stitches providers together, lowering barriers for indie developers who can rent discrete GPUs on demand. This shared-infrastructure model reinforces cloud migration and sustains growth in the South Korea discrete GPU market.

Government Incentives for Domestic Semiconductor Design Start-Ups Targeting GPU IP

The Advanced Strategic Industry Fund injected KRW 250 billion (USD 166 million) into Rebellions in March 2026, complementing the firm’s USD 400 million Series D. FuriosaAI closed USD 125 million in July 2025 and is preparing a USD 500 million pre-IPO raise. Policy support de-risks R&D, subsidizes access to foundries, and guarantees early adoption through procurement mandates, encouraging domestic challengers to Nvidia’s dominance.[2]BusinessKorea Correspondents, “Advanced Strategic Industry Fund Invests in Rebellions,” businesskorea.co.kr

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Global supply-demand imbalance in advanced node foundry capacity | -2.4% | Global, acute for Korean board partners | Medium term (2–4 years) |

| Intensifying price competition from integrated graphics in entry-level systems | -1.8% | Consumer notebooks and tablets | Short term (≤ 2 years) |

| Escalating GPU power density challenging data center cooling infrastructure | -1.3% | Seoul, Gyeonggi, Busan data centers | Medium term (2–4 years) |

| Limited domestic expertise in GPU software stack optimization | -1.1% | Enterprise IT teams nationwide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Global Supply-Demand Imbalance in Advanced Node Foundry Capacity

TSMC has fully booked its 3 nm lines through 2027. Meanwhile, Samsung's 2 nm process is only achieving a 70% yield. This has led board partners to secure wafer allocations 18 months in advance, often at the cost of margin-eroding premiums. Samsung has successfully secured the order for xAI's Grok3 chip. However, with a yield gap of 10 to 15 points compared to TSMC, concerns about supply risks loom large. If Chinese demand rebounds, it could reroute high-end wafers from Korean distributors. This shift might result in spot-price surges and prolonged lead times in the discrete GPU market.

Intensifying Price Competition from Integrated Graphics in Entry-Level Systems

Intel Core Ultra 200V and AMD Ryzen AI 300 reach a significant share of GTX 1650-class performance while cutting component costs by up to USD 50 per notebook. OEMs are pivoting mainstream laptops toward integrated solutions, relegating discrete GPUs to gaming or workstation niches. Mobile discrete shipments are declining, nudging vendors to focus on higher-margin tiers above USD 400, where integrated silicon still lags in sustained compute workloads.[3]Seoul Economic Daily Journalists, “Government Allocates 50,000 GPUs for Sovereign AI,” sedaily.com

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Application: Datacenter Accelerators Dominate AI Infrastructure Build-Out

Servers and datacenter accelerators controlled 39.84% of the discrete GPU market share in 2025. Government orders for 13,000 Blackwell B200 units and enterprise clusters like Krafton’s 1,000-GPU farm underscore a pivot from pilot to production environments. PCs and workstations remain substantial, yet integrated graphics erode entry-level demand, concentrating discrete upgrades among esports enthusiasts and creators. Handheld gaming consoles contribute modest volumes, while automotive and ADAS deployments emerge as premium growth areas, driven by Hyundai’s 50,000-unit commitment to Level 4 robotaxis.

Datacenter momentum rests on economics: SK Telecom’s GPUaaS racks deliver 44 kW of density, shaving idle capacity and monetizing mixed AI and HPC workloads. Naver Cloud’s prospective 60,000-GPU footprint offers data-sovereign infrastructure that attracts multinational tenants. These deployments expand the discrete GPU market for ancillary products such as HBM, immersion cooling, and 800G networking.

By Memory Type: HBM Adoption Accelerates as AI Workloads Demand Bandwidth

GDDR-based GPUs dominated at 71.28% in 2025, but HBM-equipped accelerators grow 18.88% annually as Samsung and SK Hynix ramped HBM4. Samsung’s 4 nm logic base die drives 13 Gbps pin speeds, while SK Hynix demonstrates 16 Gbps throughput, aligning with Nvidia Vera Rubin and AMD Instinct MI455X needs. GDDR persists in cost-sensitive gaming SKUs where bandwidth ceilings are lower and discrete GPU industry margins are tight.

The supply shift sparks ecosystem realignment: Samsung’s March 2026 MOU with AMD bundles HBM4, DDR5, and prospective foundry access, while SK Hynix funnels HBM wafers into its new M15X fab. HBM’s trajectory reinforces Korea’s upstream leverage in the discrete GPU market.

By Performance Tier: AI Accelerators Above USD 1,200 Lead Growth

High-performance consumer cards (USD 400-USD 1,200) accounted for 37.83% in 2025, yet datacenter accelerators priced above USD 1,200 posted the highest 18.75% CAGR to 2031. NVIDIA’s CUDA ecosystem secures a 94% add-in-board grip, though AMD’s MI455X and domestic NPUs emphasize performance-per-watt to win inference workloads. Mainstream (USD 100-USD 400) discrete GPUs face cannibalization from integrated silicon, and sub-USD 100 boards retreat to niche usage.

Consumer vendors differentiate through custom cooling and factory overclocks, whereas cloud operators invest USD 10,000-USD 40,000 per accelerator and adopt liquid cooling to achieve 600 kW racks. Start-ups like Rebellions claim 2.7× tokens-per-watt over Nvidia H100, but software-stack gaps temper adoption, illustrating how ecosystem maturity, not silicon alone, dictates South Korea discrete GPU market success.

Geography Analysis

Gyeonggi Province anchors the discrete GPU market, hosting Kakao’s 2,040-unit B200 cluster, NHN Cloud’s Pangyo NCC, and SK Telecom’s Gasan AI center. Pyeongtaek’s semiconductor corridor gains prominence as Samsung fabs xAI’s Grok3 chips and plans an AI factory exceeding 50,000 GPUs. Seoul drives consumer demand through dense PC-cafe networks that upgrade rigs every 2 years, reinforcing the city’s role as the retail heartbeat of the South Korea discrete GPU market.

Jeonbuk’s KRW 1 trillion (USD 760 million)3 Physical AI Manufacturing Initiative installs GPU-accelerated robotics across fabs and shipyards, broadening adoption beyond core metros. Ulsan and Hwaseong integrate discrete GPUs into automotive HUDs and cockpit controllers as Hyundai scales a USD 3 billion AI infrastructure rollout. Busan’s port logistics hub leverages GPUs for real-time defect detection in shipbuilding, while Cheongju supports upstream memory production at SK Hynix’s M15X HBM line.

The Ministry of Science and ICT’s sovereign AI strategy links compute clusters via a national portal, but power-grid headroom and cooling-water availability keep most hyperscale capacity in the Seoul Capital Area. Nonetheless, regional initiatives encourage balanced growth, cementing South Korea’s status as a data-sovereign AI hub that lures multinationals seeking latency-sensitive Korean language models.

Competitive Landscape

NVIDIA highlights a highly concentrated discrete GPU market, with AMD and Intel holding smaller portions. Foundry scarcity gives Nvidia leverage, with North American and European hyperscalers often receiving priority shipments over Korean buyers. Board partners Asus, MSI, and Gigabyte compete on thermal design and aesthetics rather than silicon. Samsung and SK Hynix exploit HBM4 leadership to forge vertical alliances, with Samsung expanding into foundry and advanced packaging for AMD’s MI455X.

Start-ups, Rebellions, and FuriosaAI pursue inference-optimized NPUs, buoyed by significant government and venture infusions. Adoption hurdles persist because enterprises must retool MLOps pipelines, delaying deployment. Liquid cooling adoption creates operational moats: KT Cloud’s immersion setup cuts power consumption and reaches 600 kW per rack, capabilities that smaller colocation providers cannot easily replicate. Automotive OEMs emerge as captive offtakers, internalizing discrete GPUs for Level 4 autonomy, and further diversifying buyer profiles in the South Korea discrete GPU market.[4]NewstheAI Analysts, “Liquid Cooling Hits 38% of Data Centers,” newstheai.com

South Korea Discrete GPU Industry Leaders

Nvidia Corporation

Advanced Micro Devices Inc.

Intel Corporation

AsusTek Computer Inc.

Micro-Star International Co. Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Samsung Electronics and AMD signed an MOU to position Samsung as the primary HBM4 supplier for Instinct MI455X and explore foundry synergies for future GPUs.

- March 2026: South Korea’s Financial Services Commission approved KRW 250 billion (USD 166 million) for Rebellions under the K-NVIDIA program, marking the initiative’s first direct equity investment.

- February 2026: NHN Cloud agreed to build Krafton’s 1,000-GPU Blackwell Ultra cluster at Pangyo NCC, scheduled for completion in July 2026, with XDR 800G InfiniBand networking.

- January 2026: Samsung commenced HBM4 mass production, targeting shipments to Nvidia and AMD after passing qualification in February 2026.

South Korea Discrete GPU Market Report Scope

The South Korea Discrete GPU Market Report is Segmented by Device Application (Mobile Devices and Tablets, PCs and Workstations, Servers and Datacenter Accelerators, Gaming Consoles and Handhelds, Automotive/ADAS, and Other Embedded and Edge Devices), Memory Type (GDDR-Based GPUs and HBM-Based GPUs), and Performance Tier (Low-Cost GPUs, Mainstream GPUs, High-Performance Consumer GPUs, and Data Center/AI Accelerator GPUs). The Market Forecasts are Provided in Terms of Value (USD).

| Mobile Devices and Tablets |

| PCs and Workstations |

| Servers and Datacenter Accelerators |

| Gaming Consoles and Handhelds |

| Automotive / ADAS |

| Other Embedded and Edge Devices |

| GDDR-Based GPUs |

| HBM-Based GPUs |

| Low-Cost GPUs (Less than USD 100) |

| Mainstream GPUs (USD 100-USD 400) |

| High-Performance Consumer GPUs (USD 400-USD 1,200) |

| Data Center / AI Accelerator GPUs (Greater than USD 1,200) |

| By Device Application | Mobile Devices and Tablets |

| PCs and Workstations | |

| Servers and Datacenter Accelerators | |

| Gaming Consoles and Handhelds | |

| Automotive / ADAS | |

| Other Embedded and Edge Devices | |

| By Memory Type | GDDR-Based GPUs |

| HBM-Based GPUs | |

| By Performance Tier | Low-Cost GPUs (Less than USD 100) |

| Mainstream GPUs (USD 100-USD 400) | |

| High-Performance Consumer GPUs (USD 400-USD 1,200) | |

| Data Center / AI Accelerator GPUs (Greater than USD 1,200) |

Key Questions Answered in the Report

How large will South Korea’s discrete GPU market be by 2031?

It is forecast to reach USD 13.46 billion, up from USD 5.80 billion in 2026, with a 18.33% CAGR.

Which application segment holds the largest share today?

Servers and datacenter accelerators led with 39.84% of the 2025 South Korea discrete GPU market share.

Why is HBM memory gaining traction against GDDR?

AI training workloads require less than 2 Tbps of bandwidth, and HBM4 delivers up to 3.3 Tbps, driving an 18.88% CAGR for HBM-based GPUs.

What risks threaten supply continuity?

Foundry bottlenecks at advanced nodes could add 6-12 months to lead times, potentially trimming market growth.

Will integrated graphics eliminate low-end discrete GPUs?

Integrated GPUs now match 80%-90% of entry-level card performance, prompting OEMs to drop sub-USD 100 boards from mainstream laptops.

Page last updated on: