Japan Discrete GPU Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

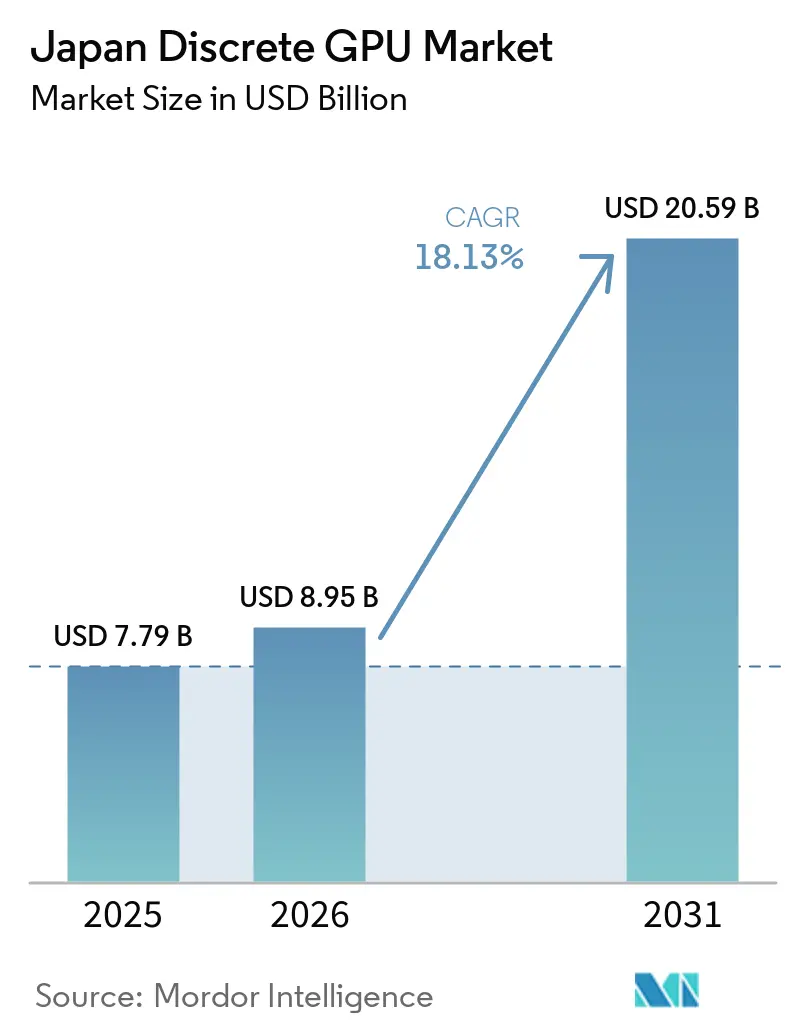

| Base Year Market Size (2025) | USD 7.79 Billion |

| Market Size (2026) | USD 8.95 Billion |

| Market Size (2031) | USD 20.59 Billion |

| Growth Rate (2026 - 2031) | 18.13% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Japan Discrete GPU Market Analysis by Mordor Intelligence

The Japan discrete GPU market size is expected to increase from USD 7.79 billion in 2025 to USD 8.95 billion in 2026 and reach USD 20.59 billion by 2031, growing at a CAGR of 18.13% over 2026-2031. Recent policy moves that steer sovereign AI development toward domestic infrastructure are accelerating capital outlays for high-bandwidth-memory accelerators that can remain inside Japan’s legal data perimeter. Public procurement programs, led by METI’s semiconductor subsidy package and RIKEN’s exascale roadmap, are underwriting multiyear demand that is decoupled from the global gaming cycle. At the same time, hyperscalers and telecom operators are racing to add GPU-rich regions near Tokyo and Osaka to eliminate the latency penalties that discourage enterprise AI adoption, while edge-gaming investments create a secondary pull for mid-tier cards. Currency volatility and grid-capacity ceilings introduce cost and deployment risk, yet they also encourage domestic assembly and liquid-cooling retrofits, which in turn expand service revenue opportunities for local OEMs. Competitive positioning, therefore, hinges as much on assured HBM supply and qualified system designs as on raw chip-level performance.

Key Report Takeaways

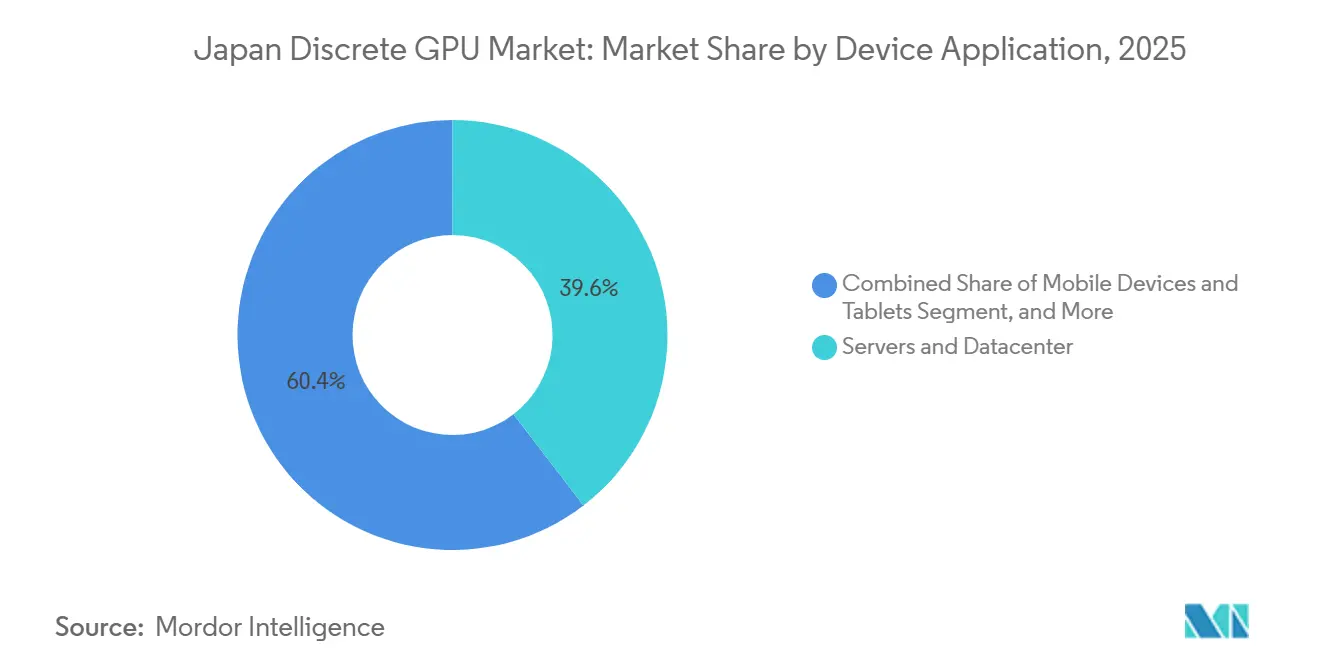

- By device application, servers and datacenter accelerators led with 39.58% of the Japan discrete GPU market share in 2025, and the segment is projected to expand at an 18.55% CAGR through 2031.

- By memory type, GDDR-based GPUs accounted for 69.91% share of the Japan discrete GPU market size in 2025, while HBM-based models are forecast to advance at an 18.73% CAGR over 2026-2031.

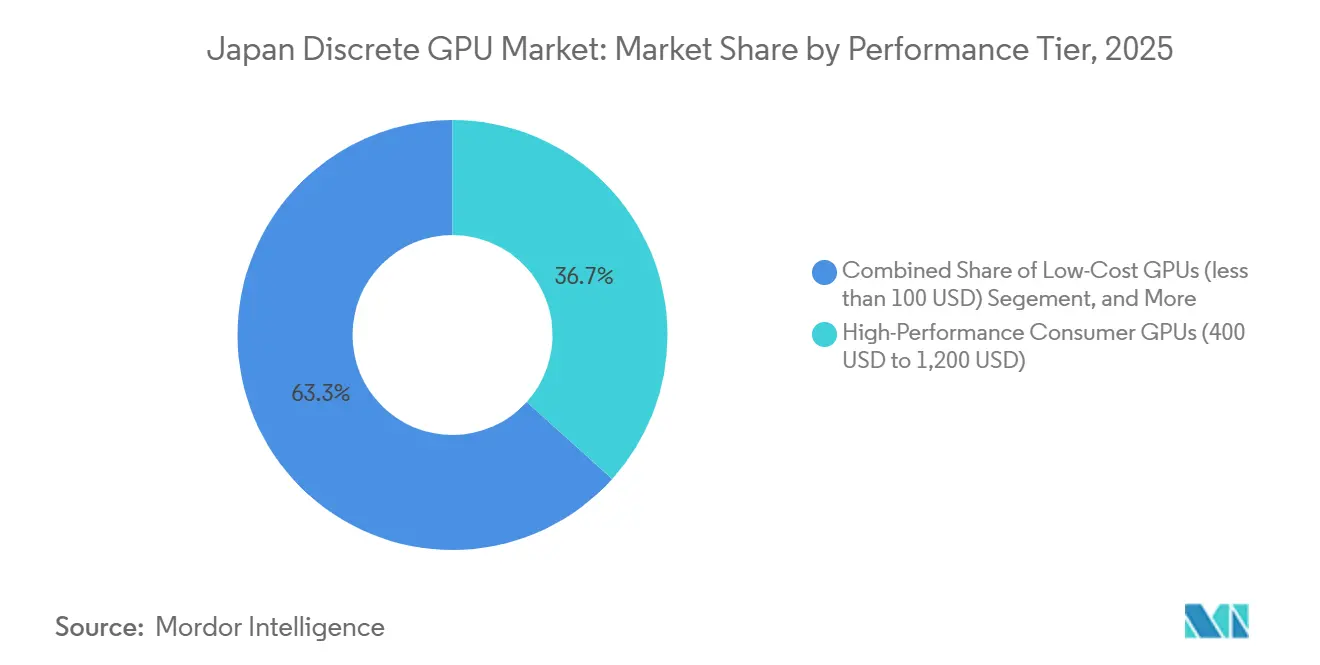

- By performance tier, high-performance consumer GPUs held 36.68% revenue share in 2025, whereas datacenter and AI accelerator GPUs are set to grow at an 18.66% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Japan Discrete GPU Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact |

|---|---|---|---|

| Growth in AI Workloads Driving High-End GPU Demand | +5.2% | National, concentrated in Tokyo, Osaka, Fukuoka datacenter hubs | Medium term (2-4 years) |

| Rising Popularity of PC Gaming and eSports in Japan | +2.8% | National, with urban concentration in Kanto and Kansai regions | Short term (≤ 2 years) |

| Expansion of Cloud Gaming Infrastructure | +2.1% | National, led by NTT, SoftBank, Sony infrastructure investments | Medium term (2-4 years) |

| Increased Adoption of GPUs in Automotive ADAS Systems | +3.4% | National, anchored by Toyota, Honda, Nissan development centers | Long term (≥ 4 years) |

| Government Incentives for Semiconductor Manufacturing in Japan | +2.9% | National, with early gains in Kumamoto, Hokkaido, Miyagi prefectures | Medium term (2-4 years) |

| Emergence of Edge AI Applications Requiring Discrete GPUs | +1.9% | National, industrial corridors in Aichi, Kanagawa, Shizuoka | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growth In AI Workloads Driving High-End GPU Demand

Sovereign-data mandates restrict the export of sensitive training corpora, so enterprises are building on-premises clusters with HBM3E-equipped accelerators that can tackle trillion-parameter models. SoftBank and OpenAI’s February 2026 agreement for an Osaka facility exemplifies the pivot toward local compute centers that displace offshore cloud options. RIKEN’s selection of 2,140 Blackwell GPUs for the FugakuNEXT system further underscores how public labs have become anchor tenants for bleeding-edge silicon.[1]RIKEN, “FugakuNEXT Exascale Roadmap,” riken.jpMicrosoft’s USD 10 billion Azure expansion adds private-sector heft, ensuring a steady pipeline of orders even if consumer demand cools. Validation of AMD’s MI325X by the National Institute of Advanced Industrial Science and Technology in February 2026 introduces price tension that could reallocate roughly USD 1.2 billion in annual public spending. The upshot is a procurement environment where assured HBM supply is more valuable than incremental teraflop gains, tightening the link between memory vendors and final GPU shipments.

Increased Adoption Of GPUs In Automotive ADAS Systems

Japanese automakers are embedding discrete GPUs into level-3 autonomy stacks, shifting inference workloads from CPUs to high-throughput accelerators. Toyota’s Arene software platform targets 2026 production vehicles with GPU-assisted sensor fusion, while Honda’s 2025 collaboration with NVIDIA extends discrete GPUs across its electric lineup. Long design-validation cycles mean that a single design win can translate into decade-long volume commitments, smoothing revenue profiles for vendors that meet automotive-grade reliability and ISO 26262 standards. The Ministry of Land, Infrastructure, Transport, and Tourism’s regulatory framework, which formalized functional-safety testing requirements in 2025, further entrenches vendors that can document field-failure rates compatible with automotive use. As electric-vehicle content per car rises, GPU makers also gain leverage to negotiate direct supply agreements, bypassing traditional tier-1 intermediaries and enhancing margin capture.[2]Ministry of Land, Infrastructure, Transport and Tourism, “Guidelines for Level-3 Automated Driving,” mlit.go.jp

Government Incentives For Semiconductor Manufacturing In Japan

METI’s seven-year, JPY 10 trillion (USD 67 billion) subsidy package reserves a dedicated tranche for AI compute infrastructure, effectively underwriting part of the bill for enterprises that install datacenter GPUs inside Japan’s borders. Early awards in Kumamoto, Hokkaido, and Miyagi are already funding clean-room construction and advanced-packaging lines, seeding domestic ecosystems that reduce dependence on overseas fabs. Subsidy rules favor applicants that source at least a portion of assembly locally, nudging OEMs to forge partnerships with Japanese EMS providers. Because payouts are tied to verified installation and utilization metrics, recipients are incentivized to maximize GPU rack densities and keep utilization high, a dynamic that supports recurring demand for mid-life upgrades. The incentive structure also shields early movers from currency swings by reimbursing a portion of dollar-denominated invoices, partially neutralizing yen depreciation risk.

Rising Popularity Of PC Gaming And eSports In Japan

Esports prize pools climbed past JPY 500 million (USD 3.4 million) in 2025, magnifying the incentive for competitive players to move from console to high-refresh-rate PCs. Gaming cafés in Tokyo and Osaka are refreshing rigs every 18 months to deliver 240 frames per second at 1440p, spurring volume for GPUs in the USD 100-USD 400 band where board partners compete on thermals rather than silicon. Pandemic-era remote-work habits persist, so households continue to buy multipurpose systems that double as gaming platforms during off-hours. Retail chains report that GPU attach rates for new PC builds outpaced CPU upgrades in 2025-2026, suggesting that graphics performance is now the chief differentiator in consumer purchase decisions. Local esports leagues broadcast on streaming platforms with sub-20 millisecond latency targets, which in turn lift demand for mid-tier cards that can encode AV1 streams in real time.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supply Chain Vulnerabilities and GPU Shortages | -2.7% | National, affecting all procurement channels | Short term (≤ 2 years) |

| High Power Consumption Limiting GPU Deployments in Datacenters | -1.8% | National, acute in Tokyo, Osaka grid-constrained zones | Medium term (2-4 years) |

| Competition from Integrated GPUs in Mainstream Laptops | -1.4% | National, concentrated in consumer and SMB segments | Short term (≤ 2 years) |

| Limited Domestic GPU IP Development in Japan | -1.1% | National, structural constraint on value capture | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Supply Chain Vulnerabilities And GPU Shortages

HBM production through 2025 is fully allocated, largely to hyperscalers that secured multiyear agreements, leaving spot buyers in Japan with six-to-nine-month wait times.[3]Reuters, “HBM Supply Constraints to Persist Through 2025,” reuters.com Because SK Hynix commands most HBM3E output, Japanese firms must either prepay to lock in slots or risk slipping project timelines. TSMC’s CoWoS advanced-packaging capacity remains oversubscribed, intensifying competition for substrates that marry logic dies to high-bandwidth stacks. Secondary markets have emerged in which refurbished H100 GPUs command 40% premiums over list price, distorting total cost of ownership calculations. These factors collectively delay AI rollouts at small and midsize enterprises, trimming near-term shipments even as pent-up demand grows.

High Power Consumption Limiting GPU Deployments In Datacenters

Many legacy Japanese colocation sites were designed for 300-watt CPUs and cannot dissipate the heat generated by 700-watt accelerators. Tokyo’s grid operator imposes summer peak-load caps, forcing datacenters to throttle draw or invest in on-site generation, both of which raise per-rack costs. Liquid-cooling retrofits can double permissible rack density but add USD 50,000-USD 100,000 per rack up front, a hurdle for operators still uncertain about AI workload persistence. Operators in cooler northern regions such as Hokkaido are building greenfield sites powered by hydro, but those facilities will not reach commercial service until 2028-2029. In the interim, enterprises may opt for inference-optimized GPUs with lower thermal-design power, narrowing the addressable market for flagship training cards.[4]Tokyo Electric Power Company, “Peak Load Management for Summer 2026,” tepco.co.jp

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Application: Datacenter Demand Outpaces Legacy Workloads

Servers and datacenter accelerators captured 39.58% of the Japan discrete GPU market share in 2025 as enterprises rushed to establish generative-AI clusters. This slice of the Japan discrete GPU market will rise fastest, advancing at an 18.55% CAGR, because each 24-GPU node can cost upward of USD 2 million, multiplying the revenue impact of every procurement cycle. Public institutions such as RIKEN and the National Institute of Advanced Industrial Science and Technology are anchoring multi-node purchases that guarantee baseline demand through 2031. PCs and workstations, once the volume backbone, now face cannibalization from integrated graphics that meet office-productivity needs, relegating discrete add-in cards to creative and CAD workloads where CUDA or ROCm acceleration remains indispensable.

Gaming consoles and handhelds, dominated by Sony’s system-on-chip strategy, offer limited upside for discrete GPUs because graphics silicon is integrated at manufacture. Automotive ADAS enters the forecast as an emerging yet strategic slice: Toyota and Honda design wins lock in volume over 10-year lifecycles, though near-term unit totals are modest. Edge devices in factories and security cameras are beginning to specify discrete GPUs for vision workloads, but these deployments remain pilot-stage and subject to integration budgets. Overall, the Japan discrete GPU market size tied to datacenter use is redefining channel economics, shifting emphasis toward enterprise-grade support contracts and away from retail sell-through velocity.

By Memory Type: HBM Growth Reconfigures Supply Chains

GDDR-based models held 69.91% revenue in 2025 thanks to entrenched gaming demand and mature cost structures. Yet the bandwidth ceilings of GDDR6X are already hindering AI training beyond 100 billion parameters, pushing hyperscalers to mandate HBM3E starting with NVIDIA’s Blackwell generation. Consequently, the HBM slice of the Japan discrete GPU market is projected to grow at an 18.73% CAGR. Supply risk remains the wild card; SK Hynix’s production booked through 2025 forces Japanese buyers to sign multiyear take-or-pay contracts that elevate inventory risk but preserve performance leadership. AMD’s MI325X and MI355X bring an alternate path, moderating NVIDIA’s bundle pricing and encouraging system integrators to qualify dual-vendor memory footprints. Board partners are redesigning thermal plates, as HBM’s stacked die footprint spreads heat differently than GDDR, spurring a mini-cycle of cooler innovation and margin recovery for premium cards.

By Performance Tier: Accelerators Outshine Enthusiast GPUs

Datacenter and AI accelerator cards, each priced above USD 1,200, will post the fastest expansion at 18.66% through the period, outpacing high-performance consumer GPUs that held 36.68% of revenue in 2025. Enterprise budgets, measured in millions of dollars per rack, make price elasticity far lower than in consumer segments, allowing vendors to pass through higher HBM and substrate costs without demand destruction. Mainstream cards in the USD 100-USD 400 band are squeezed between integrated graphics that now hit 1080p gaming thresholds and the willingness of enthusiasts to pay premiums for last-generation surplus stock. Low-cost GPUs under USD 100 are in secular decline, largely relegated to legacy office PCs and point-of-sale terminals. Merely matching frame rates is no longer sufficient; datacenter customers prioritize memory bandwidth and TDP envelopes, whereas gamers care about ray-tracing performance at 4K with frame-generation algorithms. That bifurcation allocates R&D budgets disproportionately to the high end, reinforcing existing performance hierarchies inside the Japan discrete GPU market.

Geography Analysis

Datacenter deployments in the Japan discrete GPU market remain clustered around Tokyo and Osaka, which together hosted roughly 60% of installed enterprise GPU capacity as of 2025. Proximity to headquarters in finance, e-commerce, and telecom keeps latency low and simplifies talent recruitment, but the metropolitan grid faces peak-load limitations that cap future rack densities. Operators are therefore pre-leasing space in peripheral prefectures such as Chiba and Saitama, betting on new transmission lines that will unlock additional megawatts after 2027. SoftBank’s greenfield campus in Tomakomai, Hokkaido, illustrates a northward migration pattern that taps surplus hydro power and cooler ambient temperatures, cutting chiller energy consumption during summer peaks. Microsoft’s multi-region Azure expansion follows a hub-and-spoke approach: new availability zones near Fukuoka and Nagoya aim to serve western Japan while providing disaster-recovery diversity against Tokyo’s earthquake risk.

Government incentives are also reshaping the map. METI subsidy criteria award extra points for projects in Hokkaido, Miyagi, and Kyushu, accelerating advanced-packaging investment in regions previously peripheral to semiconductor value chains. Kumamoto’s fast-growing ecosystem around the JASM fab could evolve into a mini-hub for GPU substrate and assembly by 2029, trimming logistical lead times for domestic system integrators. Fukuoka leverages undersea fiber to Seoul and Shanghai, pitching itself as a latency-optimized data waypoint for multinational AI workloads that must remain in-region for compliance reasons. Collectively, these shifts imply that the Japan discrete GPU market will decentralize over the forecast horizon, balancing disaster resilience, renewable energy access, and subsidy capture, rather than reflexively expanding inside traditional Tokyo-Osaka corridors.

Competitive Landscape

The Japan discrete GPU market operates as an oligopoly, with NVIDIA controlling roughly 80% of datacenter accelerator revenue, AMD securing near-15%, and the residual divided among Intel and niche FPGA or ASIC vendors. CUDA’s software moat locks many existing AI workflows to NVIDIA silicon, making migration costs a key deterrent. That said, AMD scored a breakthrough in February 2026 when government labs validated its MI325X for sovereign workloads, opening a path to divert as much as USD 1 billion in public purchases away from NVIDIA. Intel’s Arc Pro line, launched in December 2024, attacks workstation niches with AV1 encoding advantages but still grapples with driver maturity and limited deep-learning framework support. AIB partners such as ASUS, MSI, and Gigabyte compete chiefly on thermal solutions and factory overclocks, their gross margins compressing to single digits as chipmakers internalize more board-level value.

Supply-chain positioning now outweighs raw chip innovation. SK Hynix sold out HBM3E allocations through 2025, so board partners with early reservations enjoy a 12-18-month deployment lead that cannot be bridged by architectural tweaks alone. Government-backed installations, including RIKEN’s FugakuNEXT and the ABCI-Q supercomputer, reinforce incumbency by showcasing reference designs that private enterprises then copy. Domestic OEMs like Fujitsu and NEC seize value by bundling imported GPUs with Japanese-made server chassis, qualifying for METI subsidies that cover up to 40% of project costs and cushioning yen-dollar swings. Emerging white-space lies in edge inference and automotive ADAS, where smaller thermal budgets and functional-safety requirements dilute CUDA’s historic advantage, giving room for specialized accelerators or ASIC-based solutions to gain a foothold.

Japan Discrete GPU Industry Leaders

Nvidia Corporation

Advanced Micro Devices Inc.

Intel Corporation

ASUSTeK Computer Inc.

Micro-Star International Co. Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: AMD announced validation of its MI325X and MI355X datacenter GPUs by Japanese government agencies for sovereign AI workloads, opening public tenders to multi-vendor competition.

- February 2026: SoftBank and OpenAI unveiled plans for an Osaka AI data center that will prioritize on-premises compute in line with domestic privacy rules.

- January 2026: NVIDIA partnered with six Japanese cloud providers, including NTT and KDDI, to deploy sovereign AI infrastructure inside national borders.

Japan Discrete GPU Market Report Scope

The Japan Discrete GPU Market Report is Segmented by Device Application (Mobile Devices and Tablets, PCs and Workstations, Servers and Datacenter Accelerators, Gaming Consoles and Handhelds, Automotive/ADAS, Other Embedded and Edge Devices), Memory Type (GDDR-based GPUs, HBM-based GPUs), Performance Tier (Low-Cost GPUs, Mainstream GPUs, High-Performance Consumer GPUs, Data Center/AI Accelerator GPUs). The Market Forecasts are Provided in Terms of Value (USD).

| Mobile Devices and Tablets |

| PCs and Workstations |

| Servers and Datacenter Accelerators |

| Gaming Consoles and Handhelds |

| Automotive / ADAS |

| Other Embedded and Edge Devices |

| GDDR-based GPUs |

| HBM-based GPUs |

| Low-Cost GPUs (less than 100 USD) |

| Mainstream GPUs (100 USD to 400 USD) |

| High-Performance Consumer GPUs (400 USD to 1,200 USD) |

| Data Center / AI Accelerator GPUs (greater than 1,200 USD) |

| By Device Application | Mobile Devices and Tablets |

| PCs and Workstations | |

| Servers and Datacenter Accelerators | |

| Gaming Consoles and Handhelds | |

| Automotive / ADAS | |

| Other Embedded and Edge Devices | |

| By Memory Type | GDDR-based GPUs |

| HBM-based GPUs | |

| By Performance Tier | Low-Cost GPUs (less than 100 USD) |

| Mainstream GPUs (100 USD to 400 USD) | |

| High-Performance Consumer GPUs (400 USD to 1,200 USD) | |

| Data Center / AI Accelerator GPUs (greater than 1,200 USD) |

Key Questions Answered in the Report

What is the forecast value for discrete GPUs in Japan by 2031?

The Japan Discrete GPU market is projected to reach USD 20.59 billion by 2031.

Which application segment is expanding the fastest?

Servers and datacenter accelerators, supported by sovereign AI mandates, are advancing at an 18.55% CAGR.

How quickly is the HBM segment growing?

HBM-based GPUs are forecast to expand at an 18.73% CAGR between 2026 and 2031.

Which vendors dominate Japanese datacenter GPU sales?

NVIDIA holds about 80% share, while AMD commands near 15%, leaving the remainder to Intel and niche suppliers.

Page last updated on: