South Korea GPU Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

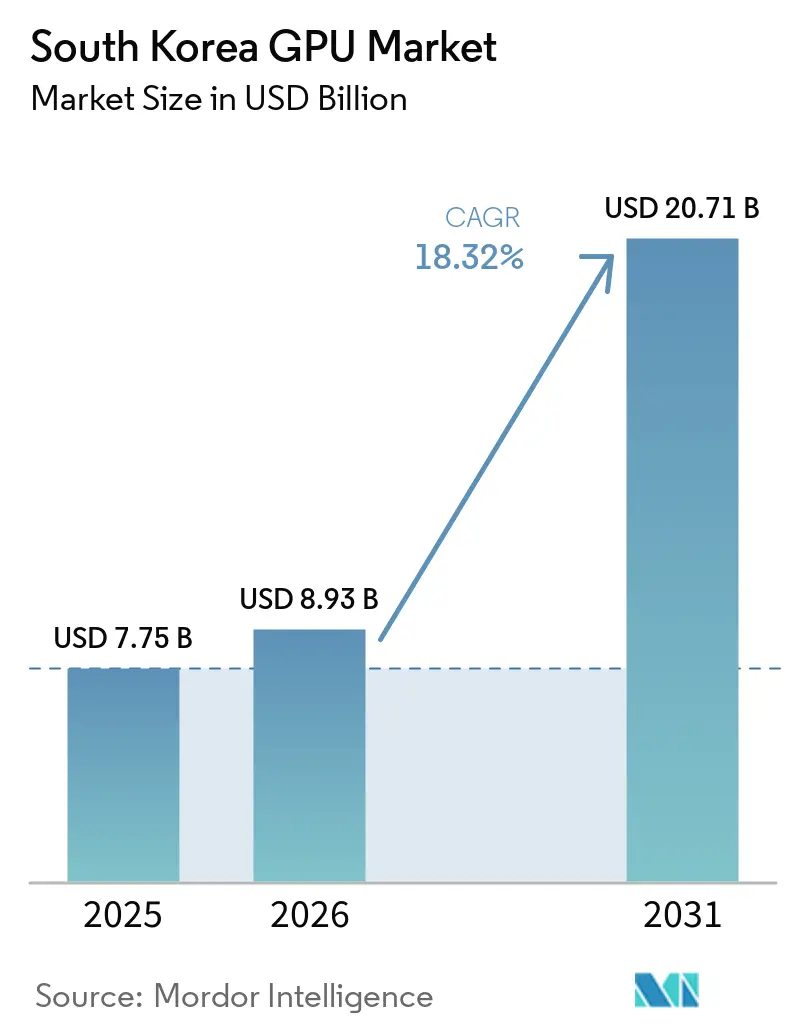

| Base Year Market Size (2025) | USD 7.75 Billion |

| Market Size (2026) | USD 8.93 Billion |

| Market Size (2031) | USD 20.71 Billion |

| Growth Rate (2026 - 2031) | 18.32% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Korea GPU Market Analysis by Mordor Intelligence

The South Korea GPU market size was valued at USD 7.75 billion in 2025 and is estimated to grow from USD 8.93 billion in 2026 to USD 20.71 billion by 2031, at a CAGR of 18.32% during the forecast period (2026-2031). Buoyant demand from hyperscale data centers, ongoing automotive digitalization, and government-backed semiconductor programs keep expenditure on graphic processors at a sustained double-digit trajectory. Domestic conglomerates are investing in sovereign AI infrastructure to reduce external dependency, while policy incentives lower capital hurdles for fabless start-ups. Growth is further amplified by Korea’s vibrant PC-gaming culture and widening adoption of high-refresh OLED displays, both of which nudge consumers toward premium GPUs. At the same time, supply-side partnerships between memory vendors and GPU designers are tightening, signaling a future where access to high-bandwidth memory will define competitive advantage.

Key Report Takeaways

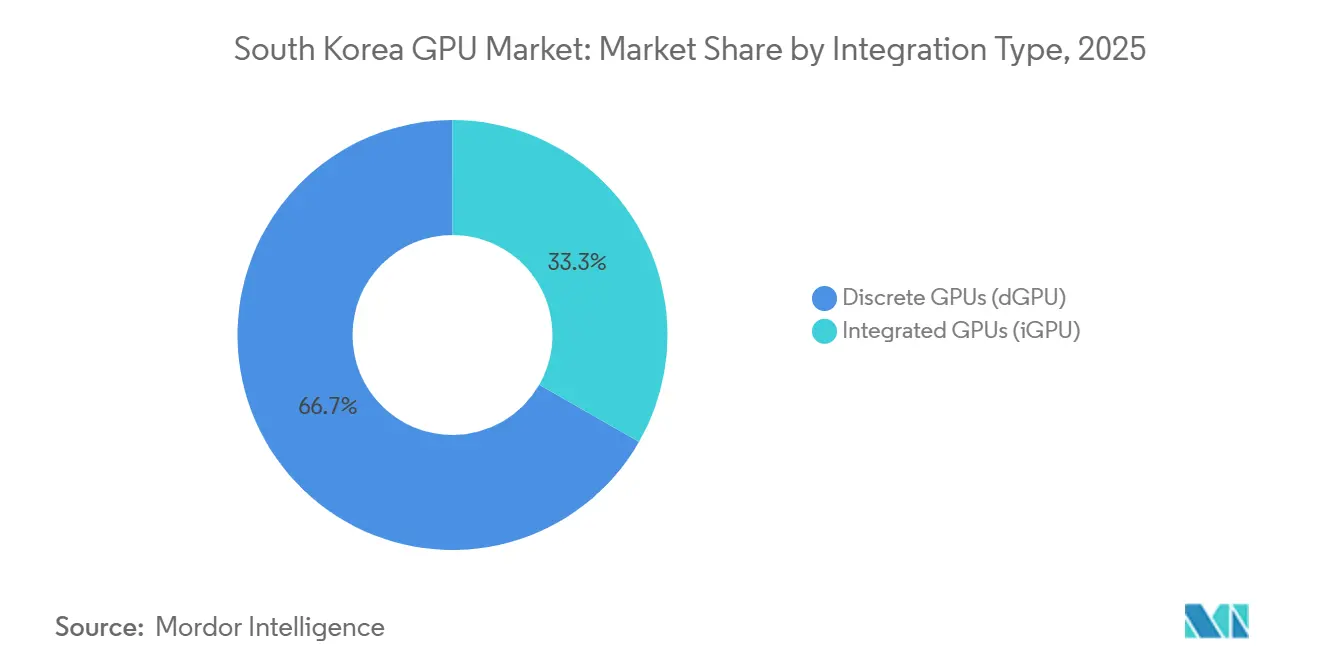

- By integration type, discrete GPUs commanded 66.73% of the South Korea GPU market share in 2025 and are forecast to expand at an 18.92% CAGR through 2031.

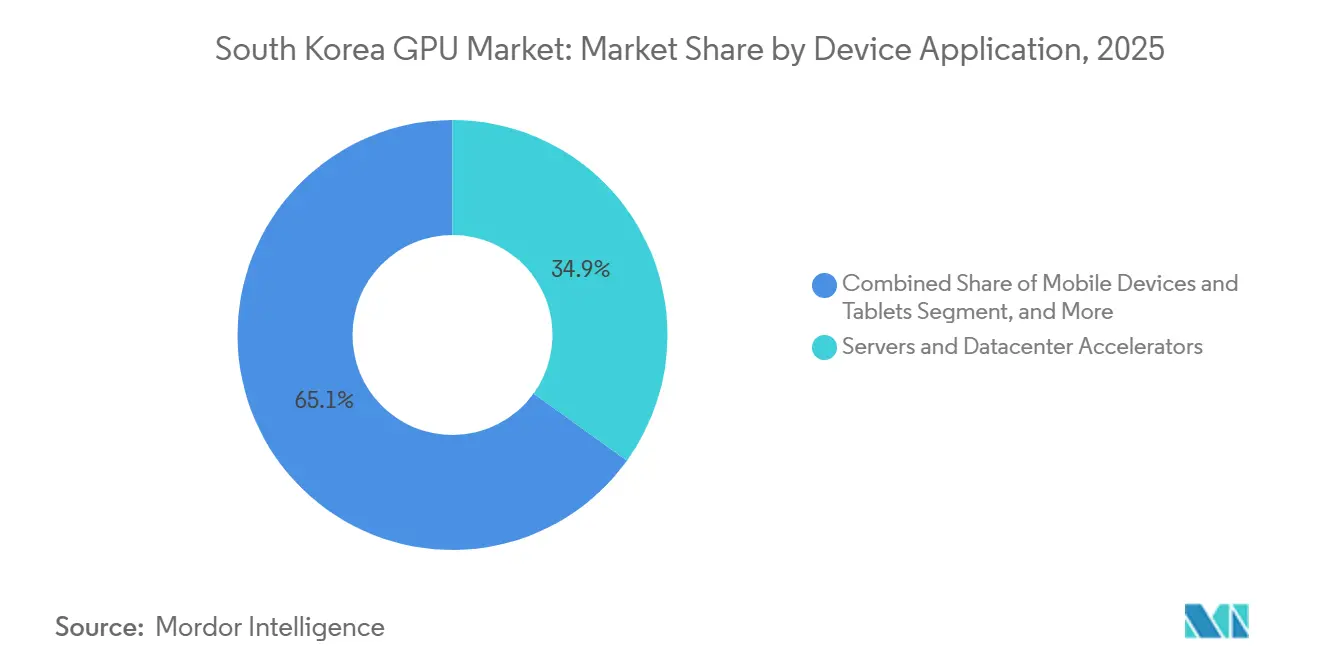

- By device application, servers and data-center accelerators accounted for 34.94% of revenue in 2025 and are projected to grow at an 18.79% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

South Korea GPU Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Explosive Growth of AI Workloads in Domestic Data Centres | +6.2% | National, concentrated in Seoul Capital Area and Busan | Medium term (2–4 years) |

| Rising Popularity of AAA PC Gaming Titles Requiring High-End GPUs | +2.8% | National, urban clusters in Seoul, Busan, Incheon | Short term (≤ 2 years) |

| Government Subsidies for Fabless Chip Start-ups Focused on GPUs | +3.1% | National, Pangyo, Seongnam, Daejeon tech clusters | Long term (≥ 4 years) |

| Shift to OLED / High-Refresh Mobile Displays Necessitating Stronger iGPUs | +2.4% | National, Samsung and LG Display hubs | Medium term (2–4 years) |

| Integration of GPUs in Advanced Driver-Assistance Systems Mandated for 2027 | +2.6% | National, Ulsan and Gwangju automotive corridors | Medium term (2–4 years) |

| Growing Demand for Low-Power Edge GPUs in Smart Factories | +1.5% | National, Gyeonggi and Chungcheong industrial zones | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Explosive Growth of AI Workloads in Domestic Data Centers

Seoul’s goal of hosting country-specific large-language-model services is driving unprecedented GPU procurement. Operators are colocating new halls next to existing generation assets to offset the energy draw of 260,000 NVIDIA accelerators earmarked by the government, a scale equivalent to the load of a large nuclear reactor.[1]Jeong-ho Lee, “Seoul’s AI Ambition Requires Power Equal to Nuclear Reactor,” Korea JoongAng Daily, joongang.co.kr Shinsegae’s 250-megawatt complex in Yongin, slated for late 2026, will become the nation's largest private AI facility. Samsung SDS plans to produce 50,000 units for its National AI Computing Center, enabling smaller enterprises to rent time on domestic clusters rather than rely on foreign clouds.[2]Samsung SDS, “National AI Computing Center Investor Briefing,” samsungsds.com Demand already outpaces government quotas four-to-one, pointing to tight capacity over the medium term. The result is a winner-takes-most environment that favors groups that can secure land, power, and early preferential memory allocations.

Rising Popularity of AAA PC Gaming Titles Requiring High-End GPUs

The country’s esports heritage now coexists with an enthusiast niche that demands 4K ray tracing at triple-digit frame rates. NVIDIA cards captured three-quarters of the do-it-yourself channel in late 2025, while premium models such as the GeForce RTX 5090 sold at 1.8 times suggested retail due to constrained supply. Samsung and LG Display, which account for a significant share of global OLED gaming monitor output, raised refresh rates to 480 hertz, forcing GPUs to sustain higher throughput.[3]LG Display, “Next-Gen OLED Gaming Monitors Exceed 480Hz,” lgdisplaynewsroom.com Compliance with VESA DisplayHDR 1400 and ISO/IEC 23003-5 further raises performance thresholds, indirectly boosting discrete attach rates. Retail spending on gaming rigs, therefore, rises in lock-step with every display specification leap.

Government Subsidies for Fabless Chip Start-ups Focused on GPUs

To balance its historical bias toward memory fabs, Korea is funneling capital into design-only firms. The Ministry of Trade, Industry, and Energy spent KRW 49.4 billion (USD 34.2 million) in 2025 to commercialize AI semiconductors, while Rebellions alone drew KRW 250 billion (USD 173 million) from the National Growth Fund. SiliconArts closed a Series B round to refine its ray-tracing core for automotive and metaverse workloads.[4]SiliconArts, “Series B Funding Announcement,” siliconarts.co.kr Sapeon, spun out of SK Telecom, markets a lower-cost inference accelerator for edge telecom racks.[5]Sapeon, “X330 Edge Accelerator Overview,” sapeon.com Subsidies come with domestic-manufacturing clauses that feed a talent pipeline with university partners. Even so, long design cycles and tight wafer availability at Samsung Foundry or TSMC remain execution risks.

Integration of GPUs in Advanced Driver-Assistance Systems Mandated for 2027

A regulation coming into force in 2027 obliges all new passenger vehicles to include at least Level 2+ driver assistance. Hyundai Motor Group locked in 50,000 NVIDIA Blackwell units for simulation and in-vehicle compute, aiming to achieve Level 4 autonomy by 2028. Kia’s EV9 and Hyundai’s Ioniq 7 will rely on NVIDIA Drive Orin chips capable of 254 TOPS for sensor fusion. SiliconArts is concurrently piloting a low-latency ray-tracing core for real-time environment rendering, with trials slated for late 2026. Certification under ISO 26262 and UN Regulation 157 adds validation complexity, pushing OEMs toward suppliers with proven automotive-grade roadmaps.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Memory Supply-Chain Bottlenecks Affecting HBM Availability | -2.1% | Icheon and Pyeongtaek HBM fabs | Short term (≤ 2 years) |

| High Import Tariffs on Discrete GPU Boards | -1.3% | National consumer and enterprise channels | Medium term (2–4 years) |

| Domestic Talent Shortage in GPU Architecture Design | -1.8% | Seoul Capital Area, Daejeon, Pangyo | Long term (≥ 4 years) |

| Volatility in Cryptocurrency Mining Demand | -0.6% | National resale markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Memory Supply-Chain Bottlenecks Affecting HBM Availability

High-bandwidth memory now sets the throughput ceiling for AI accelerators. SK hynix began HBM4 production in January 2026 and captured a significant share of NVIDIA’s early allocation, while Samsung’s ramp lagged after thermal-management hurdles. A single Blackwell GPU requires up to eight HBM3e stacks and even more under HBM4, making wafer allocation a zero-sum game. Samsung earmarked more than half of its SOCAMM2 output, roughly 100 billion Gb, for NVIDIA in 2026. Each wafer diverted to HBM squeezes DDR5 supply, lifting costs across the memory spectrum.

Domestic Talent Shortage in GPU Architecture Design

Brain drain undermines Korea’s ambition to create home-grown GPU intellectual property. The industry will be short 54,000 semiconductor specialists by 2031, and Samsung alone lost 515 engineers to NVIDIA in the year to June 2024. Global players pay base salaries exceeding USD 250,000 for HBM expertise, dwarfing domestic norms. SK hynix attempted to bridge the gap by awarding bonuses worth 29.6 months of base pay in 2024, yet such largesse is hard to repeat. A significant portion of advanced AI talent educated locally now works abroad, and government programs to train specialists over five years cannot offset annual attrition. Start-ups, therefore, struggle to hire senior architects, who are vital for competitive tape-outs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Integration Type: Discrete GPUs Anchor Datacenter Buildouts

Discrete accelerators held 66.73% of the South Korea GPU market share in 2025 after hyperscale buyers prioritized plug-and-play scalability. Samsung SDS, Shinsegae, and Hyundai collectively reserved more than 150,000 add-in boards through 2029, most of them NVIDIA Blackwell units. Such orders lock in PCIe Gen5 backplanes and liquid-cooling loops for at least two refresh cycles, ensuring long revenue tails for board vendors. Import levies at 10% and episodic reciprocal tariffs briefly at 25% raise the total cost of ownership, yet buyers still choose discrete cards because integrated alternatives lack the raw tensor throughput needed for generative AI.

In consumer channels, the escalation in esports prize pools and OLED monitor refresh rates reinforces the premium halo around high-end discrete cards. Integrated GPUs, by contrast, ride mobile and automotive demand where thermal envelopes and value-added tax exemptions for locally fabbed SoCs create cost advantages. Samsung’s Exynos 2600 illustrates this pivot, bundling an RDNA 4 graphics block that handles hardware ray tracing in a handset. Over the forecast horizon, the South Korean GPU market for integrated solutions will grow, yet discrete silicon remains the revenue anchor for data-center and workstation workloads.

By Device Application: Servers Dominate, Automotive Accelerates

Servers and data-center accelerators accounted for 34.94% of 2025 revenue and are projected to grow at an 18.79% CAGR, keeping the South Korean GPU market for rack-mounted hardware on a steep incline. Government quotas for sovereign AI infrastructure allocate 260,000 NVIDIA boards to national champions, resulting in recurring replacement cycles every 24-30 months. PCs and workstations stay relevant as the nation’s gaming culture migrates to 4K ray tracing at 144 frames per second, a threshold only high-end desktops can currently meet. Mobile devices are catching up: Exynos 2600 brings console-grade graphics plus on-device generative AI that bypasses cloud round-trips, pushing handset ASPs higher.

Automotive is the standout. Korea’s 2027 Level 2+ mandate compels OEMs to integrate GPUs for sensor fusion, and Hyundai’s order for 50,000 Blackwell units sets a procurement template likely to be emulated by Kia and GM Korea. Industrial edge deployments round out demand, as SK Group installed 2,000 RTX Pro 6000 cards for predictive maintenance while POSCO DX pilots Mobilint NPUs to displace GPUs in inference-only tasks. Collective momentum across these verticals ensures broad-based growth for the South Korea GPU market.

Geography Analysis

Seoul Capital Area absorbs the lion’s share of GPU spending because hyperscale campuses cluster near Yongin, Pyeongtaek, and Ansan. Government land-zoning incentives and proximity to 765-kilovolt substations shorten project lead times. Busan is next in line, leveraging its port infrastructure to handle inbound GPU boards and power modules without cross-peninsula trucking delays. The South Korean GPU market, attributable to Busan, gained further impetus when local authorities cleared 60 hectares for a greenfield data center corridor linked to LNG-fired peaker plants.

Gwangju and Ulsan form the automotive corridor that anchors GPU-rich ADAS simulation farms. Hyundai Motor’s research hub in Ulsan partners with local universities, creating a feedback loop that keeps algorithm training onshore. The upcoming Level 2+ regulation has already nudged supplier parks to upgrade test benches with GPU clusters capable of physics-based digital twins. Jeolla and Chungcheong provinces, while less urbanized, attract smart-factory pilots that install low-power edge GPUs for machine-vision defect detection.

Jeju Island hosts a smaller, renewable-powered data-center segment. Although its contribution to overall revenue is modest, the region acts as a testbed for immersion-cooled GPUs that can operate within tight thermal margins. Over the forecast period, power-grid upgrades and submarine cable redundancy projects will allow Jeju to punch above its current weight. Across all regions, public-sector co-funding for AI training resources ensures that rural start-ups can access compute credits without relocating, spreads GPU adoption beyond traditional metropolitan strongholds, and keeps the South Korean GPU market on a geographically diversified growth path.

Competitive Landscape

NVIDIA maintains a strong position in data-center accelerators, buoyed by its CUDA ecosystem and early co-design deals with SK hynix and Samsung on HBM4. The two memory giants together control a significant share of HBM supply, granting partners preferential bandwidth lanes. Samsung Electronics pursues a dual approach: licensing AMD’s RDNA cores for mobile Exynos chips while incubating proprietary accelerators tied to its memory roadmaps. By capturing a substantial share of NVIDIA’s SOCAMM2 orders for 2026, Samsung improved its bargaining leverage in negotiations over future die-to-memory interposers.

Fabless challengers such as Rebellions, SiliconArts, and Sapeon are carving niches where lower power budgets and telecom-grade latency are prioritized over brute-force FLOPS. Rebellions’ ATOM neural-processing unit targets 5-to-20-watt edge routers, an arena where traditional GPUs cannot achieve favorable power efficiency. SiliconArts focuses on automotive ray tracing, hoping that its deterministic timing advantages will satisfy ISO 26262 certification faster than chiplet-based competitors. Sapeon, under the SK Telecom umbrella, exploits colocation rights at base-station shelters to deploy inference accelerators that sidestep cloud bandwidth costs.

Patent trends reveal diverging priorities. NVIDIA and AMD file aggressively around chiplet interconnects to stack more SMs under one package footprint, whereas Samsung and SK Hynix patent schemes that move HBM dies closer to logic to shave nanoseconds of latency. POSCO DX’s pilot to replace GPUs with Mobilint NPUs for welding-defect detection underscores a broader shift toward specialized silicon for narrow workloads. Despite these incursions, ecosystem inertia, software lock-in, and superior memory access keep NVIDIA at the apex of the South Korea GPU market for the medium term.

South Korea GPU Industry Leaders

NVIDIA Corporation

Samsung Electronics Co., Ltd.

Advanced Micro Devices, Inc.

Intel Corporation

Qualcomm Technologies, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: SK hynix commenced mass production of HBM4 at its Icheon fab, securing approximately 70% of NVIDIA’s initial allocation for Blackwell accelerators.

- December 2025: Samsung Electronics unveiled the Exynos 2600 with an AMD RDNA 4-based Xclipse 960 GPU, positioning it for Galaxy S26 devices.

- November 2025: Hyundai Motor Group and NVIDIA agreed on a multi-year deal for 50,000 Blackwell GPUs to support Level 4 autonomous driving.

- October 2025: Samsung SDS confirmed plans to operate 50,000 GPUs by 2029 in its National AI Computing Center.

South Korea GPU Market Report Scope

The South Korea GPU Market Report is Segmented by Integration Type (Integrated GPUs and Discrete GPUs), and Device Application (Mobile Devices and Tablets, PCs and Workstations, Servers and Datacenter Accelerators, Gaming Consoles and Handhelds, Automotive and ADAS, and Other Embedded and Edge Devices). The Market Forecasts are Provided in Terms of Value (USD).

| Integrated GPUs (iGPU) |

| Discrete GPUs (dGPU) |

| Mobile Devices and Tablets |

| PCs and Workstations |

| Servers and Datacenter Accelerators |

| Gaming Consoles and Handhelds |

| Automotive / ADAS |

| Other Embedded and Edge Devices |

| By Integration Type | Integrated GPUs (iGPU) |

| Discrete GPUs (dGPU) | |

| By Device Application | Mobile Devices and Tablets |

| PCs and Workstations | |

| Servers and Datacenter Accelerators | |

| Gaming Consoles and Handhelds | |

| Automotive / ADAS | |

| Other Embedded and Edge Devices |

Key Questions Answered in the Report

What growth outlook is projected for the South Korea GPU market through 2031?

Revenue is forecast to rise from USD 8.93 billion in 2026 to USD 20.71 billion by 2031, reflecting an 18.32% CAGR over 2026-2031.

Which integration type leads to spending?

Discrete accelerators accounted for 66.73% of the market in 2025 and should remain the primary revenue driver as hyperscalers expand sovereign AI capacity.

How will the 2027 ADAS mandate affect GPU demand?

Automotive OEMs must install Level 2+ systems on every new car, prompting multi-year GPU procurement agreements that accelerate unit adoption.

What restrains near-term supply?

Limited availability of HBM3e and initial HBM4 stacks at SK hynix and Samsung creates a bottleneck that curtails accelerator shipments.

Are start-ups competitive against NVIDIA?

Fabless firms target niche workloads such as low-power edge inference and automotive ray tracing, but ecosystem and talent gaps limit broad displacement of incumbent platforms.

Page last updated on: