Asia-Pacific GPU Cooling Solutions Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

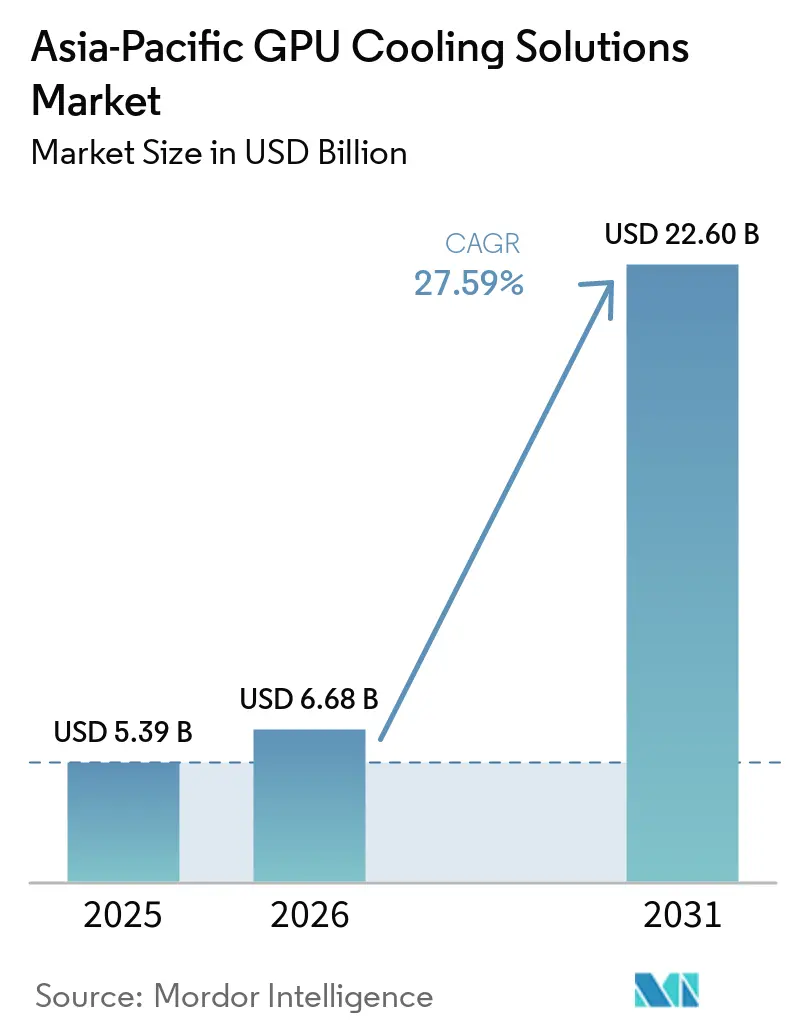

| Base Year Market Size (2025) | USD 5.39 Billion |

| Market Size (2026) | USD 6.68 Billion |

| Market Size (2031) | USD 22.60 Billion |

| Growth Rate (2026 - 2031) | 27.59% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific GPU Cooling Solutions Market Analysis by Mordor Intelligence

The Asia-Pacific GPU cooling solutions market size is expected to grow from USD 5.39 billion in 2025 to USD 6.68 billion in 2026 and is forecast to reach USD 22.60 billion by 2031 at 27.59% CAGR over 2026-2031. The Asia-Pacific GPU cooling solutions market is moving into a phase where GPU power density, rack density, and facility design are changing at the same time, which is making liquid-based systems more central to new AI infrastructure. NVIDIA’s move from 700W-class GPUs toward 1,000W and higher-power platforms has made air cooling less practical for AI-dense racks, especially in hyperscale and sovereign compute settings. Government-backed AI compute programs in South Korea, Japan, China, and India are also pulling demand forward because new facilities are increasingly being designed for high-density thermal loads from the start. Competition is expanding beyond consumer thermal hardware vendors, as industrial manufacturers and precision cooling specialists add module capacity, coolant distribution systems, and enterprise-grade designs. Near-term growth is still shaped by retrofit cost and coolant fluid constraints, which is why direct-to-chip systems are gaining ground faster than full immersion in many deployments.

Key Report Takeaways

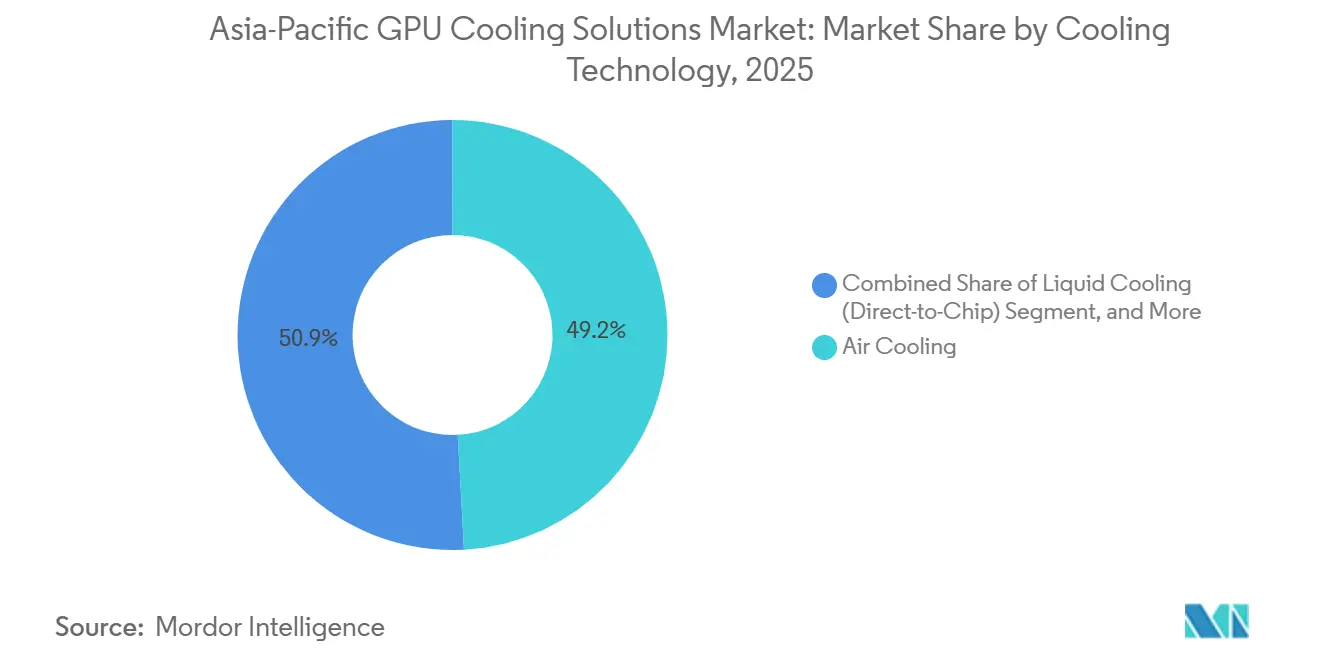

- By cooling technology, the Asia-Pacific GPU cooling solutions market had air cooling as the largest segment, with a 49.15% share in 2025, while immersion cooling is projected to expand at a 24.12% CAGR through 2031.

- By cooling level, server-rack-level cooling accounted for 61.25% share of the Asia-Pacific GPU cooling solutions market in 2025, and the same segment is expected to record the fastest growth through 2031.

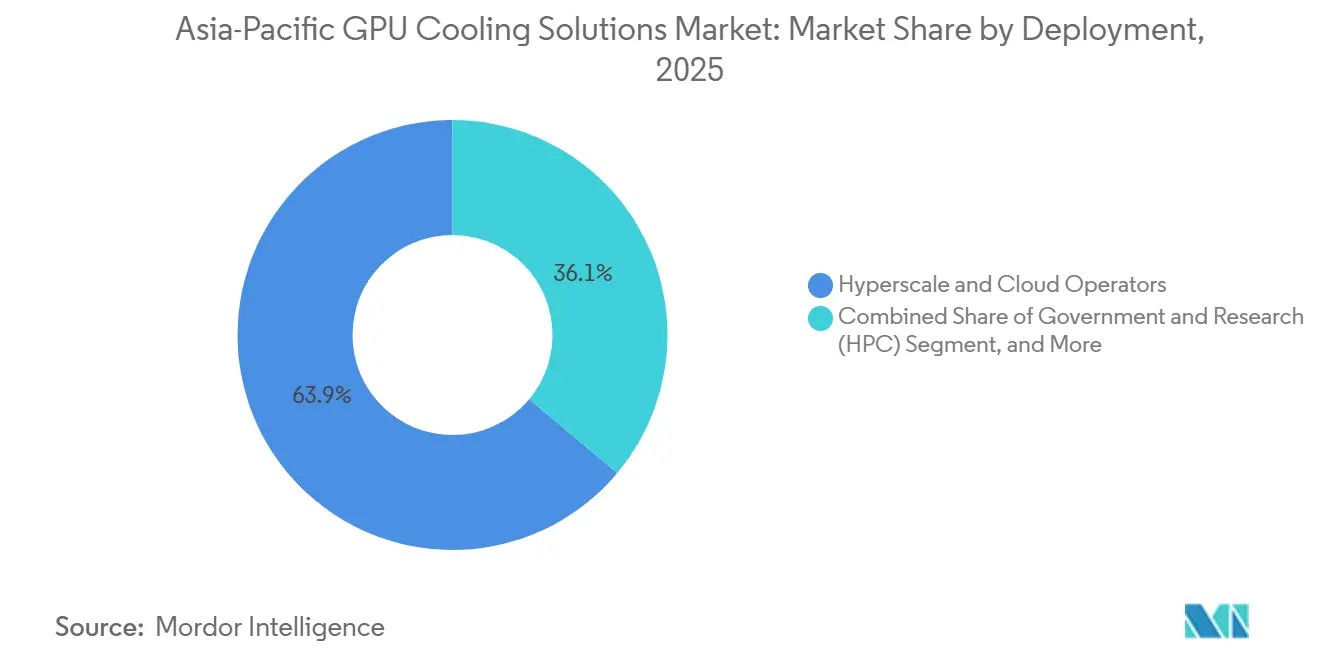

- By deployment, hyperscale-cloud held 63.90% share in 2025, while enterprise deployments are projected to post the 25.14% CAGR through 2031.

- By GPU power density, the 300W-700W band led with 51.60% share of the Asia-Pacific GPU cooling solutions market in 2025, while above-700 W systems are expected to expand at the 26.12% CAGR from 2026 to 2031.

- By geography, China held 47.55% of regional revenue in 2025, while India is projected to record the 29.20% CAGR growth through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Asia-Pacific GPU Cooling Solutions Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising GPU Thermal Design Power In AI Workloads | +7.5% | Global, with concentrated impact in China, Japan, and South Korea where AI compute density is highest | Short term (≤ 2 years) |

| Data-Center Energy Efficiency Mandates By Asia-Pacific Governments | +5.2% | China, Japan, and South Korea | Medium term (2-4 years) |

| Proliferation Of Liquid-Cooled High-Density Edge Micro-Data Centers | +4.0% | Japan, South Korea, Southeast Asia, and India | Medium term (2-4 years) |

| Tax Incentives For Green IT Infrastructure In China And Japan | +2.8% | China, Japan, and Singapore indirectly through green financing frameworks | Medium term (2-4 years) |

| Vertical Integration Of Hyperscalers Into Direct-To-Chip Cooling Hardware | +2.4% | China, Singapore, and Japan | Short term (≤ 2 years) |

| Emergence Of Immersion-Ready GPU Reference Designs From Semiconductor OEMs | +1.8% | Greenfield hyperscale campuses across Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Data-Center Energy Efficiency Mandates By Asia-Pacific Governments

The Asia-Pacific GPU cooling solutions market is also benefiting from policy frameworks that turn energy efficiency from a preference into a design requirement. China’s green data center framework under GB/T 44989-2024 and related energy efficiency rules is tightening the operating envelope for large data facilities, especially those that support dense compute deployments. Japan’s fiscal 2026 zero-emission data center commercialization program and its broader subsidy support for decarbonized facilities are reducing the payback period for advanced cooling investments. South Korea’s AI Data Center Special Act, cleared in May 2026, signaled that sovereign AI infrastructure will move forward with faster procurement and more direct policy support for high-density facilities. In practical terms, these frameworks favor cooling systems that can support lower PUE targets in GPU-heavy halls where legacy air designs struggle. For the Asia-Pacific GPU cooling solutions market, this means regulatory compliance is now reinforcing the same technology shift that GPU power density has already set in motion.

Proliferation Of Liquid-Cooled High-Density Edge Micro-Data Centers

A second layer of demand is coming from compact AI facilities that sit outside the hyperscale model and closer to end-use workloads. Preferred Networks, Internet Initiative Japan, and JAIST brought AImod into operation in Japan with a direct liquid cooling design, a 7:3 water-to-air ratio, a design PUE of 1.1, and a WUE of 0, which makes it an important reference point for dense urban AI infrastructure.[2]NVIDIA, “NVIDIA Blackwell Architecture,” NVIDIA, nvidia.com That type of architecture is relevant because many edge and modular sites cannot absorb the space, water, or mechanical plant footprint associated with larger conventional cooling systems. NHN Cloud’s 7,656-GPU cluster in Seoul also showed that liquid cooling can support dense deployment while improving energy performance compared with conventional air-cooled setups. As inference workloads move closer to factories, telecom sites, transport nodes, and city-edge facilities, the need for compact liquid cooling becomes more visible across Japan, South Korea, Singapore, and selected Southeast Asian markets. The Asia-Pacific GPU cooling solutions market is therefore widening beyond hyperscale campuses, which gives rack-integrated cooling vendors and compact CDU suppliers a broader customer base.

Tax Incentives For Green IT Infrastructure In China And Japan

Financial support is accelerating adoption in places where regulation alone would not move the market fast enough. Japan’s JPY 210 billion (USD 1.35 billion) program for decarbonized data centers and parallel regional support schemes are making high-efficiency cooling more affordable for operators that would otherwise delay major thermal upgrades. China’s national green data center recognition framework adds procurement and reputational value to facilities that exceed baseline efficiency requirements, which strengthens the business case for liquid cooling investment. AirTrunk’s JPY 191.6 billion green loan for its Tokyo campus showed that green finance is now directly linked to data center buildout and cooling efficiency in Japan. These incentives matter because cooling decisions are often deferred when operators must balance thermal upgrades against land, power, and IT equipment spending. In the Asia-Pacific GPU cooling solutions market, subsidy support and green finance are shortening decision cycles and helping advanced liquid architectures move beyond only the largest cloud buyers.

Rising GPU Thermal Design Power In AI Workloads

The Asia-Pacific GPU cooling solutions market is being pushed first by the steady rise in GPU thermal design power for AI training and inference systems. NVIDIA’s Blackwell architecture and GB200 NVL72 platform established a clear shift toward liquid-cooled rack design for high-density AI infrastructure, and that has changed how operators plan both greenfield and retrofit projects.[1]Furukawa Electric Co., Ltd., “Notice Regarding Capital Expenditure (Acquisition of Fixed Assets) for Production of Heat-Dissipation/Cooling Products for Data Centers,” Furukawa Electric Co., Ltd., furukawaelectric.comThe move from earlier 700W-class accelerators toward 1,000W-class systems and beyond is narrowing the range where conventional air cooling remains practical in production AI clusters. Rack-level power and thermal intensity now matter as much as per-chip wattage, because integrated AI systems are being deployed as tightly coupled domains instead of isolated servers. This is why operators in China, Japan, South Korea, and India are increasingly treating direct-to-chip and immersion architectures as infrastructure decisions rather than optional upgrades. In the Asia-Pacific GPU cooling solutions market, that shift creates durable demand for cold plates, coolant distribution units, pumps, heat exchangers, and facility-side liquid loops that align with new AI rack designs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital Expenditure Of Immersion Cooling Retrofits | -3.0% | Legacy air-cooled hyperscale and enterprise facilities in China, Japan, and India | Medium term (2-4 years) |

| Supply-Chain Volatility For Coolant Fluids | -2.0% | Import-dependent operators across Asia-Pacific, with spillover into Southeast Asia | Short term (≤ 2 years) |

| Limited Skilled Workforce For Liquid Loop Commissioning | -1.3% | India, Southeast Asia, and Rest of Asia-Pacific | Medium term (2-4 years) |

| Lack Of Common Open Standards Across Cooling Technologies | -0.8% | Multi-vendor hyperscale and enterprise deployments in China and Japan | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Supply-Chain Volatility For Coolant Fluids

The second major restraint is the tight and changing supply chain for specialty cooling fluids used in immersion deployments. The draft highlighted that dielectric fluid sourcing remains concentrated and import-dependent across much of the Asia-Pacific, which exposes operators to lead-time risk and qualification delays when supply conditions tighten. Regulatory pressure on PFAS-linked chemistries and the exit of 3M’s Novec line have added another layer of uncertainty for operators that need long-life fluid choices across multiple sites. In response, regional players have started to build local alternatives, including the May 2026 partnership between S-Oil and GST in South Korea to develop an immersion cooling solution around domestically linked fluid and equipment capabilities.[3]Preferred Networks, “PFN, IIJ and JAIST Deploy Direct Liquid-Cooled, High-Density AI Servers in Modular Data Center,” Preferred Networks, preferred.jp That is a useful first step, but regional capacity is still early relative to the expected rise in AI cluster deployment. In the Asia-Pacific GPU cooling solutions market, this keeps direct-to-chip systems attractive because they avoid part of the fluid dependency that still slows broader immersion adoption.

High Capital Expenditure Of Immersion Cooling Retrofits

The largest near-term constraint is the cost of converting existing air-cooled halls into environments that can support immersion or deep liquid-based architectures. The draft indicated that full retrofit readiness for advanced GPU deployments can require structural changes, liquid plumbing, and facility-level thermal redesign that materially raise capital intensity. This is one reason greenfield campuses are adopting native liquid cooling faster than older enterprise sites, because new builds can integrate thermal infrastructure from the first design stage. In legacy facilities, operators often prefer phased direct-to-chip upgrades because those projects can fit into existing rack and server layouts more easily than immersion tanks. That decision does not eliminate spending pressure, but it spreads the cost over a longer cycle and lowers disruption to installed workloads. For the Asia-Pacific GPU cooling solutions market, the result is not weaker demand, but a slower transition path for immersion in mid-tier enterprise and colocation environments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Cooling Technology: Air Cooling Leads, While Immersion Changes The Upgrade Path

Air cooling held 49.15% of the Asia-Pacific GPU cooling solutions market size in 2025, which kept it as the largest cooling technology segment, while immersion cooling is projected to expand at a 24.12% CAGR through 2031. That position came from the region’s large installed base of enterprise, public sector, and consumer GPU systems that were built around airflow-heavy thermal management and have not yet crossed the threshold for full liquid adoption. The Asia-Pacific GPU cooling solutions market still has meaningful air-cooled volume in gaming, workstation, and lower-density server environments, particularly where budgets or facility limitations delay major upgrades. At the same time, immersion cooling is the fastest-growing technology segment through 2031 because the newest AI hardware is pushing heat density beyond the comfortable operating range of traditional air designs.

Direct-to-chip liquid cooling is gaining ground as the most practical bridge between installed infrastructure and next-generation GPU power envelopes. It can often be introduced into existing server designs with less disruption than immersion, which makes it attractive for enterprise, colocation, and public sector buyers that need to support newer accelerators without rebuilding entire halls. Hybrid cooling is also gaining traction in dense urban deployments, especially where operators want liquid cooling for high-heat components and residual air support for the rest of the system. Japan’s AImod facility is a useful signal because it showed how a water-air hybrid model can achieve strong efficiency results in a compact AI deployment. Across the Asia-Pacific GPU cooling solutions industry, the technology mix is shifting toward liquid-based designs, but the transition path still differs by facility age, workload intensity, and available capital.

By Cooling Level: Rack-Scale Design Becomes The Main Thermal Unit

Server-rack-level cooling accounted for 61.25% share of the Asia-Pacific GPU cooling solutions market size in 2025, and it is also the fastest-growing cooling level over the forecast period. That combination reflects a clear architectural change in AI data centers, where the rack is now treated as a unified thermal and power domain rather than a collection of separate components. The Asia-Pacific GPU cooling solutions market is moving in this direction because integrated GPU systems are now deployed in tightly linked clusters with shared coolant routing, common monitoring, and coordinated fail-safe controls. Rack-level cooling, therefore, carries more value in AI factories and sovereign compute sites than isolated component-level solutions.

Component-level cooling still matters in consumer gaming, workstation systems, and lower-scale professional environments where thermal management remains card-specific, and the deployment unit is much smaller. Vendors based in Taiwan and China continue to benefit from that volume base, especially in aftermarket and prosumer channels. Even so, the revenue mix is migrating upward toward rack-scale platforms because dense AI clusters now require thermal management that is coordinated across the whole system. NHN Cloud’s liquid-cooled cluster in Seoul illustrated the operational case for this model, with rack-level management tied to pressure, flow, and temperature monitoring across a very large GPU environment. That shift gives rack-level vendors stronger pricing power and keeps R&D focused on distribution units, manifold systems, and coordinated rack cooling controls.

By Deployment: Hyperscale Holds The Lead, While Enterprise Picks Up Speed

Hyperscale cloud held 63.90% of the Asia-Pacific GPU cooling solutions market share in 2025, which made it the largest deployment segment by a wide margin, while enterprise deployments are projected to post the 25.14% CAGR through 2031. Large cloud campuses have been the earliest adopters of liquid cooling because they can design around high-density AI loads from the start and spread infrastructure cost over larger capacity programs. Vantage Data Centers’ USD 1.6 billion capital backing for its Asia-Pacific platform and Digital Edge’s USD 4.5 billion Indonesia campus both showed how new hyperscale projects in the region are being planned around AI-ready thermal systems rather than retrofitted later. That early lead means hyperscale buyers still anchor demand for high-value liquid loops, CDUs, manifolds, and rack-integrated systems across the Asia-Pacific GPU cooling solutions market. Enterprise is nevertheless the fastest-growing deployment segment because many organizations are now preparing for upgrades from H100-class hardware to more demanding platforms and cannot rely on legacy airflow designs indefinitely.

Government and research deployments are also rising as sovereign compute programs add national clusters, academic supercomputing projects, and public-private AI infrastructure. South Korea’s policy-backed AI computing expansion and NHN Cloud’s 7,656-GPU deployment showed how public programs are translating into liquid-cooled capacity in practice. Edge remains the smallest deployment segment by share, but it is attracting more interest in Japan, South Korea, and Singapore where low-latency inference is expanding. The spread of modular AI infrastructure means smaller deployments can still require sophisticated cooling when rack density is high. For vendors, that opens room to sell compact liquid systems outside the traditional hyperscale buying cycle.

By GPU Power Density: The 300W-700W Band Still Leads, But Higher Tiers Drive The Next Cycle

The 300W-700W range held 51.60% of the Asia-Pacific GPU cooling solutions market size in 2025, which reflects the large active base of GPUs installed over the last several procurement cycles, while above-700 W systems are expected to expand at the 26.12% CAGR from 2026 to 2031. This band includes hardware that can still operate across a mix of high-performance air and direct-to-chip cooling, depending on workload intensity and utilization pattern. It remains important because many enterprises, cloud providers, and research facilities are still extracting useful life from those installed systems before the next upgrade wave. In that sense, the 300W-700W category anchors current revenue even as the market’s center of gravity moves higher.

The above 700W segment is the fastest-growing category through 2031 because new AI deployments are increasingly based on hardware that pushes rack density and thermal load into a different operating regime. That change raises the importance of cold plate design, fluid flow control, manifold reliability, and facility-side heat rejection more than legacy GPU cycles did. The below 300W segment continues to serve gaming, workstation, and lighter inference use cases, but its growth profile is slower because the strongest spending is now centered on AI and HPC systems. Specialized component vendors are already adapting product lines to server-grade platforms, including water blocks and precision thermal components built for newer professional GPUs. For the Asia-Pacific GPU cooling solutions industry, that means the next product cycle is less about serving a broad mainstream power range and more about preparing for sustained demand at much higher thermal densities.

Geography Analysis

China held 47.55% of the Asia-Pacific GPU cooling solutions market share in 2025, which kept it as the largest country market in the region, while India is projected to record the 29.20% CAGR growth through 2031. The country’s lead came from its large installed AI compute base, a concentrated hyperscaler ecosystem, and policy support for domestic digital infrastructure buildout. China’s green data center framework is also reinforcing the move toward more efficient cooling because large facilities face tighter expectations around energy performance and renewable power usage. The vendor side is equally important because China and nearby supply centers are closely tied to the regional production of liquid cooling parts, enterprise water blocks, and server thermal modules. The Asia-Pacific GPU cooling solutions market, therefore, depends heavily on Chinese demand conditions, Chinese procurement cycles, and the broader manufacturing network linked to that ecosystem.

India is the fastest-growing geography in the Asia-Pacific GPU cooling solutions market because new data center capacity and AI infrastructure programs are arriving together rather than in separate waves. The draft noted that India’s data center base expanded to 1.5 GW, which gives the country a large platform for future GPU cooling demand as operators move toward denser AI deployments. Yotta’s USD 500 million raise for an India AI cluster and Reliance Industries’ INR 1.08 lakh crore (USD 12.86 billion) approved project in Andhra Pradesh both point to large-scale infrastructure that is being planned with liquid cooling economics in mind. Japan remained the third-largest geography, supported by decarbonized data center subsidies, urban AI infrastructure planning, and government-backed compute programs. AImod gave Japan a credible reference case for direct liquid cooling in a compact footprint with strong efficiency metrics, which matters in a market where land and facility design constraints are real.

South Korea is moving faster than its size would normally suggest because sovereign AI policy is translating into direct GPU cluster deployment and related cooling demand. The national AI fund, the AI Data Center Special Act, and the country’s large planned GPU rollout are making South Korea a critical market for liquid cooling adoption between 2026 and 2028. Southeast Asia is also emerging as a strong investment cluster, supported by AI-ready hyperscale projects in Indonesia and liquid cooling pilots in Singapore. The rest of Asia-Pacific, including Taiwan, Australia, and New Zealand, remains important because it includes technology suppliers, specialist thermal vendors, and production expansion linked to future liquid cooling demand. Taken together, the regional pattern shows a market where China anchors current scale, India drives the fastest expansion, and Japan, South Korea, and Southeast Asia shape the next phase of design adoption.

Competitive Landscape

The Asia-Pacific GPU cooling solutions market remained fragmented, with no single vendor holding a dominant position across cooling technologies, deployment tiers, and countries. The field included large Taiwan and China-based manufacturers such as Cooler Master, DeepCool, Gigabyte, ASUS, MSI, and Bykski, along with European precision cooling specialists such as Asetek, EKWB, and Alphacool, and a wider group of industrial and infrastructure players moving into enterprise liquid cooling. The Asia-Pacific GPU cooling solutions market is therefore not defined by one type of competitor, because consumer thermal brands, rack infrastructure vendors, and industrial manufacturers are all pursuing the same AI buildout. That mix keeps pricing pressure elevated in volume segments while rewarding vendors that can offer engineering performance, manufacturing scale, and after-sales support together. The strongest strategic moves in 2025 and 2026 came from companies that repositioned beyond traditional PC thermal hardware and toward data center-grade cooling platforms.

Cooler Master’s Computex 2025 presentation captured that shift clearly, because the company linked enterprise cold plates and rack-level coolant distribution systems with its broader thermal engineering base under the “One Cooler Master” strategy. Its disclosed plan to expand manufacturing in Vietnam around AI server cooling modules and precision thermal hardware showed that geographic diversification is now part of competitive strategy, not just a supply chain decision. Furukawa Electric’s JPY 55 billion (USD 345 million) capex plan for water-cooling module production across the Philippines, Thailand, and China showed that industrial suppliers are entering the segment at meaningful scale. Asetek also reinforced the value of OEM channels through its October 2025 long-term agreement with a minimum USD 35 million revenue commitment over 2 years, which confirmed continued demand for high-end liquid cooling through established hardware partnerships. These moves suggest that scale, channel access, and enterprise credibility are becoming just as important as component-level thermal performance.

White-space opportunities remain visible in service-heavy areas that many legacy hardware vendors do not fully address. Government and HPC deployments in South Korea, India, and Japan are creating demand for rack-level installation support, fluid qualification, maintenance, and long-term operating services alongside hardware supply. Edge AI deployments are opening a second gap, because urban and modular sites need compact liquid systems that can deliver high thermal performance in very small footprints. Keppel and Shell’s immersion cooling pilot in Singapore reflected this search for differentiated fluid-hardware combinations that can improve energy efficiency and computing density in advanced facilities. In the Asia-Pacific GPU cooling solutions market, vendors that can combine thermal engineering, field support, and regional manufacturing are likely to be better positioned than companies that compete only on standalone hardware.

Asia-Pacific GPU Cooling Solutions Industry Leaders

Cooler Master Technology Inc.

Deepcool Industries Co., Ltd.

Asetek A/S

Thermaltake Technology Co., Ltd.

EKWB d.o.o.

- *Disclaimer: Major Players sorted in no particular order

Asia-Pacific GPU Cooling Solutions Market Report Scope

GPU Cooling Solutions are integrated systems and technologies designed to dissipate heat generated by graphics processing units (GPUs) during operation, thereby maintaining optimal thermal performance, reliability, and longevity. These solutions encompass a range of methods, including air cooling, liquid cooling (direct-to-chip), immersion cooling, and hybrid approaches, and are implemented at various levels, such as component-level or server/rack-level architectures. They are critical in high-performance computing environments, data centers, hyperscale cloud platforms, and AI/ML workloads, where GPU power densities often exceed 300W, requiring efficient thermal management to prevent throttling and hardware failure and to ensure sustained computational throughput.

The Asia-Pacific GPU Cooling Solutions Market Report is Segmented by Cooling Technology (Air Cooling, Liquid Cooling (Direct-to-Chip), Immersion Cooling, and Hybrid Cooling), Cooling Level (Component-Level Cooling and Server / Rack-Level Cooling), Deployment (Hyperscale / Cloud, Enterprise, Government and Research (HPC), and Edge), GPU Power Density (Below 300W, 300W - 700W, and Above 700W), and Country (China, Japan, South Korea, India, Southeast Asia, Rest of Asia-Pacific). The Market Forecasts are Provided in Terms of Value (USD).

| Air Cooling |

| Liquid Cooling (Direct-to-Chip) |

| Immersion Cooling |

| Hybrid Cooling |

| Component-Level Cooling |

| Server / Rack-Level Cooling |

| Hyperscale / Cloud |

| Enterprise |

| Government and Research (HPC) |

| Edge |

| Below 300W |

| 300W - 700W |

| Above 700W |

| China |

| Japan |

| South Korea |

| India |

| Southeast Asia |

| Rest of Asia-Pacific |

| By Cooling Technology | Air Cooling |

| Liquid Cooling (Direct-to-Chip) | |

| Immersion Cooling | |

| Hybrid Cooling | |

| By Cooling Level | Component-Level Cooling |

| Server / Rack-Level Cooling | |

| By Deployment | Hyperscale / Cloud |

| Enterprise | |

| Government and Research (HPC) | |

| Edge | |

| By GPU Power Density | Below 300W |

| 300W - 700W | |

| Above 700W | |

| By Country | China |

| Japan | |

| South Korea | |

| India | |

| Southeast Asia | |

| Rest of Asia-Pacific |

Key Questions Answered in the Report

What is the Asia-Pacific GPU cooling solutions market size in 2026 and how large could it become by 2031?

The Asia-Pacific GPU cooling solutions market was valued at USD 6.68 billion in 2026 and is forecast to reach USD 22.60 billion by 2031, growing at a CAGR of 27.59% over 2026-2031.

Which cooling technology currently leads in Asia-Pacific GPU deployments?

Air cooling led in 2025 with 49.15% share because a large installed base still operates on legacy enterprise, government, and consumer GPU systems.

Why is liquid cooling gaining ground so quickly across AI infrastructure in Asia-Pacific?

Rising GPU power density, tighter rack design, and stronger energy efficiency requirements are making direct-to-chip and immersion systems more suitable for high-density AI environments.

Which deployment model drives the most demand for GPU cooling solutions in the region?

Hyperscale-cloud led with 63.90% share in 2025 because large cloud campuses are building AI-ready facilities with native liquid cooling infrastructure.

Which country is growing the fastest for GPU cooling solutions in Asia-Pacific?

India is the fastest-growing geography through 2031, supported by rapid data center capacity expansion, AI cluster funding, and policy-backed infrastructure development.

Page last updated on: