Singapore Data Center GPU Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

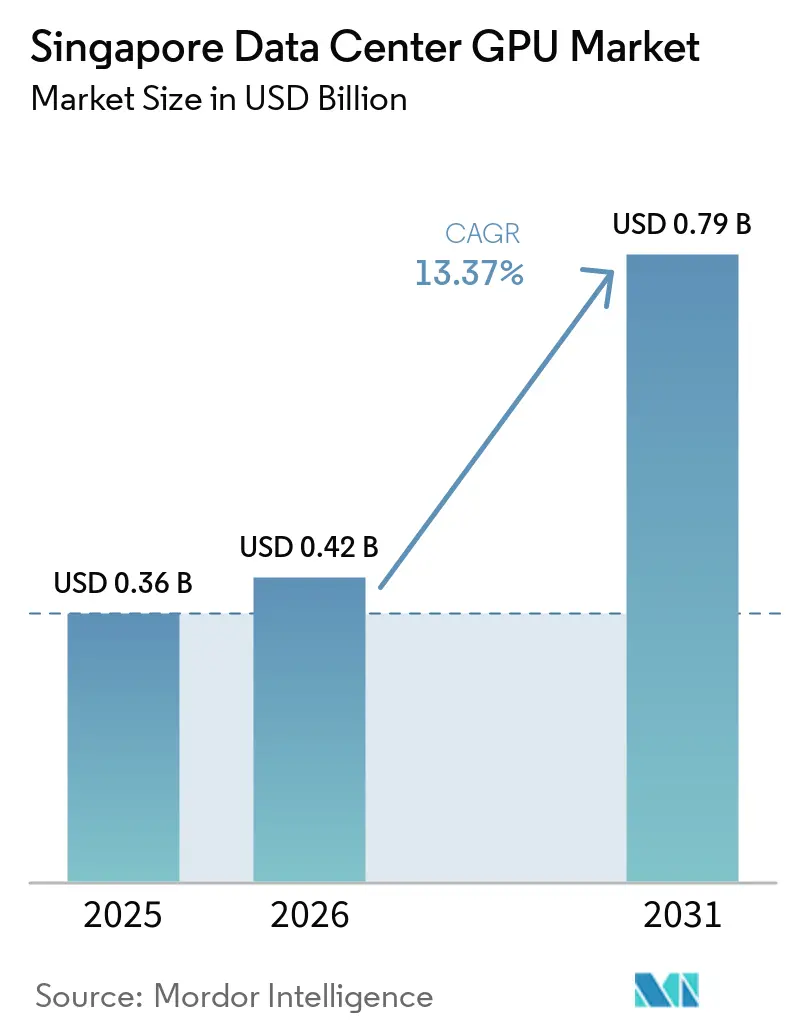

| Base Year Market Size (2025) | USD 0.36 Billion |

| Market Size (2026) | USD 0.42 Billion |

| Market Size (2031) | USD 0.79 Billion |

| Growth Rate (2026 - 2031) | 13.37% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Singapore Data Center GPU Market Analysis by Mordor Intelligence

The Singapore data center GPU market size was valued at USD 0.42 billion in 2026 and is estimated to grow from USD 0.36 billion in 2025 to reach USD 0.79 billion by 2031, advancing at a 13.37% CAGR over 2026-2031. Hyperscalers continue to anchor construction pipelines, but enterprise and public-sector demand is expanding the customer base, accelerating the pivot to liquid-cooled, high-density racks, and making sovereign AI capacity a national priority. Operators are racing to secure renewable energy allocations before the next Data Center-Call for Application window, while GPU vendors face binding high-bandwidth memory and CoWoS packaging constraints that keep pricing elevated. Tight land and power caps are forcing rack densities above 40 kilowatts, pushing immersion and direct-to-chip cooling into mainstream deployment. The policy-driven emphasis on efficiency, combined with premium colocation rates, is sustaining investor appetite for new builds even as the supply chain remains volatile.

Key Report Takeaways

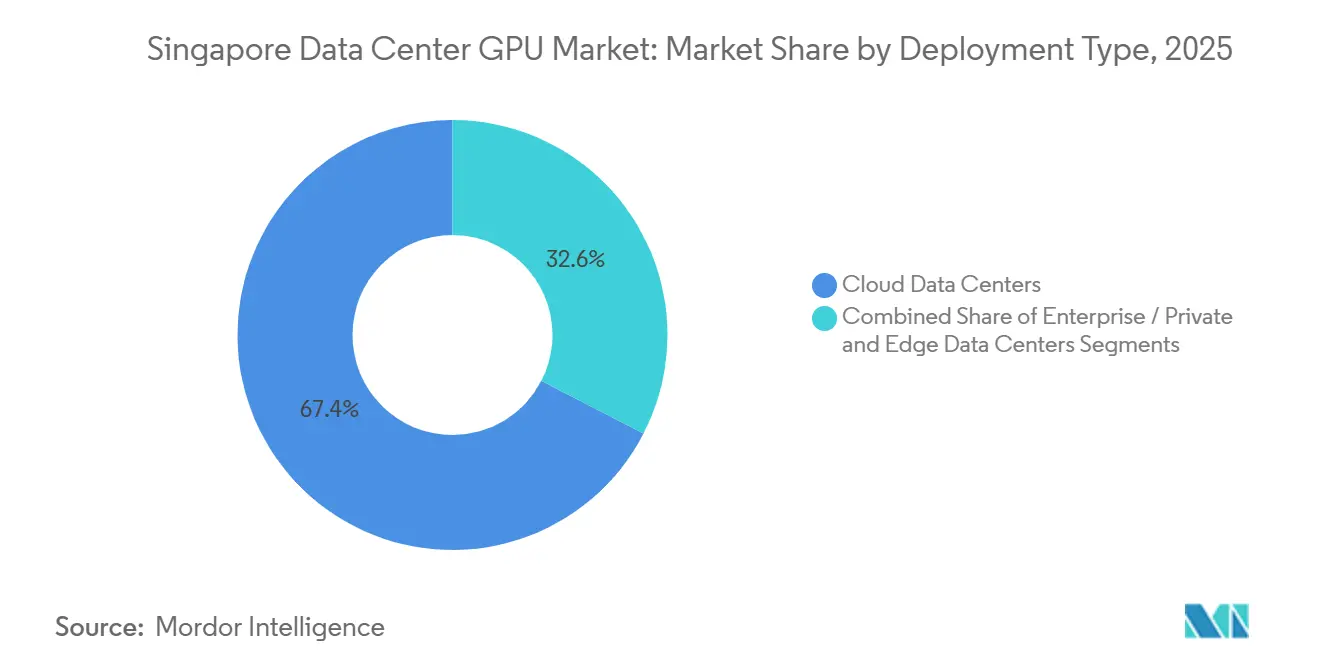

- By deployment type, cloud data centers led with 67.42% share of the Singapore data center GPU market in 2025, while edge data centers were identified as the fastest-growing segment through at 16.94% CAGR through 2031.

- By GPU type, inference devices accounted for 56.93% share of the Singapore data center GPU market in 2025, whereas training GPUs are registering the highest growth at 17.45% CAGR through 2031 momentum across the forecast window.

- By interconnect, PCIe solutions commanded 77.28% of the Singapore data center GPU market size in 2025; however, high-bandwidth interconnect GPUs are expected to post the quickest expansion as larger language models become commonplace at 16.89% CAGR through 2031.

- By workload, artificial intelligence and machine learning captured 53.81% share of the Singapore data center GPU market size in 2025, with data analytics overtaking all other use cases as the fastest climber at 17.58% CAGR through 2031.

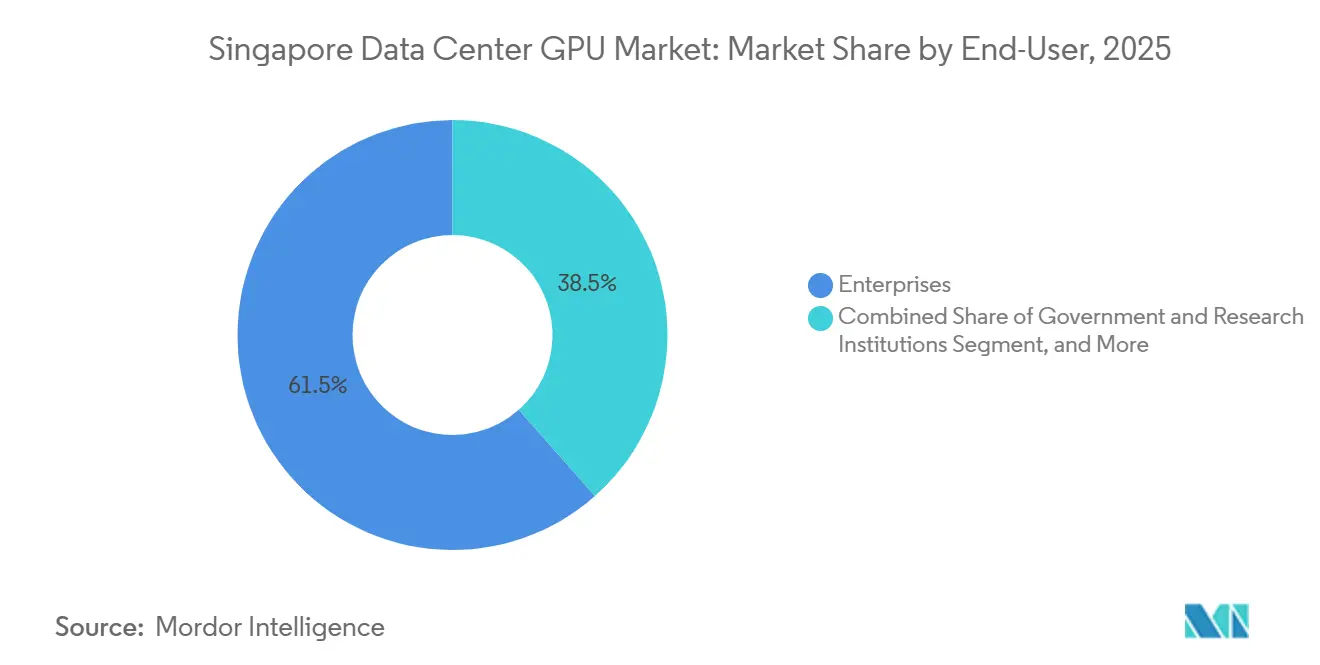

- By end-user, hyperscalers and cloud service providers held 61.54% of the Singapore data center GPU market share in 2025, while hyperscalers remain the fastest-expanding customer group at 17.02% CAGR through 2031 as they continue multibillion-dollar build-outs across India.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Singapore Data Center GPU Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in Generative AI and LLM Training Demand | +4.2% | National with spillover to ASEAN | Medium term (2-4 years) |

| Hyperscaler Expansion and Pre-Committed Capacity in Singapore | +3.8% | Jurong and Tuas industrial zones | Short term (≤ 2 years) |

| Rapid Enterprise Adoption of AI Workloads | +2.6% | Finance and logistics corridors | Short term (≤ 2 years) |

| Government Incentives for Green Data Centers | +2.1% | DC-CFA2 allocated sites | Medium term (2-4 years) |

| Decentralized GPUaaS Platforms Filling Capacity Gaps | +0.9% | National and regional edge nodes | Long term (≥ 4 years) |

| Integrated Cable-Landing Data Centers Lowering Latency | +0.7% | Tuas and Changi CLS clusters | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge in Generative AI and LLM Training Demand

Large language model training has become the single biggest catalyst for new GPU clusters. The ASPIRE 2A+ supercomputer’s 320 NVIDIA H100 GPUs cut the MERaLiON model’s training time from 340 days to under 6 days, proving the productivity leap enabled by dense accelerators. Sovereign AI initiatives now require on-premises capacity to maintain data residency, prompting agencies to deploy B200 DGX SuperPODs for frontier workloads. Regional model builders such as Firmus AI reserve hundreds of H200 GPUs for months, a demand pattern spot markets cannot match.[1]National Supercomputing Centre Singapore, “NSCC Singapore’s ASPIRE 2A+ Ranks 90 on TOP500 Supercomputers List,” nscc.sgUniversity clusters support video generative AI, surgical intelligence, and materials science, broadening use cases beyond natural language processing. As model sizes swell, interconnect bandwidth and memory capacity dictate architectural choices, reinforcing the shift to InfiniBand fabrics.

Hyperscaler Expansion and Pre-Committed Capacity in Singapore

Microsoft, Amazon Web Services, and Google have collectively earmarked more than USD 19 billion for Singapore builds between 2024 and 2029, with a disproportionate share targeting GPU-dense availability zones. Keppel DC REIT’s hyperscaler rent climbed to 69.3% of revenue in fiscal 2025, and rental reversions reached 45%, signaling that cloud giants will pay premiums for liquid-cooled halls. The DC-CFA2 program’s 200-megawatt cap, coupled with a March 2026 build deadline, triggered a land rush that locked hyperscalers into multi-year commitments. Asset-backed conversions of legacy halls into GPU rooms accelerated, highlighted by KDC Singapore 7 and 8’s SGD 1.4 billion purchase. These moves cement Singapore as the region’s AI gravity center despite more affordable capacity in neighboring Malaysia.

Government Incentives for Green Data Centers

Policy now shapes design choices as much as customer demand. The Green Data Center Roadmap imposes a 1.3 PUE ceiling and compulsory liquid cooling for builds above 30 megawatts, effectively retiring air-cooled blueprints. SS 715:2025 targets a 30% cut in IT energy use, steering operators toward direct-to-chip systems that handle 700-watt H100 and 1,000-watt Blackwell GPUs. Nxera’s DC Tuas debuted in 2026 with a 1.25 PUE and the country’s largest commercial liquid loop, setting a benchmark for future projects. Grants covering up to 70% of retrofit costs lower barriers for midsize operators, while integrated cable-landing stations cut latency for real-time AI. Together, efficiency rules and subsidies accelerate the migration to power-dense GPU halls.

Rapid Enterprise Adoption of AI Workloads

Enterprises are moving production AI in-house, pushing demand past hyperscaler footprints. Singtel’s Applied AI Center runs GB200 racks at 200 kilowatts, a 20-fold jump over legacy servers. Financial services, logistics, and telecom firms seek sub-second inference latency for customer service bots, supply-chain optimizers, and digital twins. Data residency rules favor hybrid and private clouds, prompting banks to lease GPU containers inside secure colocation suites. Managed GPU services abstract cluster complexity for firms lacking deep AI ops talent. Skills shortages and compliance hurdles remain barriers, but turnkey offerings shorten deployment cycles and amplify overall infrastructure demand.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Land and Power Caps Limiting New Facilities | -2.3% | Jurong and Tuas development corridors | Short term (≤ 2 years) |

| Global GPU Supply Constraints and Price Volatility | -1.8% | Worldwide, with premium pricing in Singapore | Medium term (2-4 years) |

| Skilled Workforce Shortage in Liquid-Cooling Operations | -0.6% | National talent pool | Medium term (2-4 years) |

| Water-Use Scrutiny Impacting Facility Permits | -0.4% | National, enforcement on 30 MW+ sites | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Land and Power Caps Limiting New Facilities

Singapore’s moratorium, lifted only partially through the DC-CFA2 call, restricts expansion to 200 megawatts and mandates 50% renewable energy, forcing rack densities up to 120 kilowatts.[2]Huawei Digital Power, “FusionDC1000A Prefabricated All-in-One Data Center,” digitalpower.huawei.com Space scarcity drives cooling, electrical, and structural complexities that lengthen project timelines. Operators hedge by securing capacity in Malaysia and Australia, but latency-sensitive AI inference still gravitates to Singapore. Cross-border renewable imports remain uncertain, and solar yield is capped by limited rooftop real estate, sustaining the constraint beyond 2026.

Global GPU Supply Constraints and Price Volatility

High-bandwidth memory shortages lifted GPU prices 30% in late 2025 and another 20% in early 2026, while TSMC’s CoWoS lines remain the throughput bottleneck, with NVIDIA claiming roughly 60% of available slots.[3]Silicon Analysts, “NVIDIA AI Accelerator Market Share 2024-2026,” siliconanalysts.com H100 cloud instances now cost USD 2.50-4.00 per hour in Singapore, a 25-33% premium over pre-shortage rates. Lead times diverge: Supermicro delivers in under a month, but tier-one vendors can take up to 10 weeks, complicating enterprise roadmaps. As Blackwell racks climb to USD 4 million each, capital planning grows more complex, and smaller buyers often resort to spot markets with unpredictable availability.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Type: Cloud Dominance Matched by Edge Momentum

Cloud data centers captured 67.42% of the Singapore data center GPU market size in 2025, reflecting hyperscaler scale economics and their ability to sign multi-year renewable power purchase agreements, while edge data centers were identified as the fastest-growing segment through at 16.94% CAGR through 2031. The concentration deepened as Microsoft and AWS reserved GPU halls years in advance, pushing colocation rates toward the upper end of USD 480 per kilowatt per month. Enterprise-class private clouds mounted a comeback once data residency clauses tightened in financial services, leading banks to carve out on-premises GPU zones inside Tier 4 facilities. Edge builds recorded the sharpest growth, driven by autonomous vehicle testing tracks in Tuas and live-stream analytics at the port, where sub-10-millisecond latency is mandatory.

In 2026, the Singapore data center GPU market sees cloud operators retrofit existing halls with immersion tanks while edge specialists deploy prefabricated 6-kilowatt pods near 5G base stations. Nxera’s cable-landing integration model further blurs lines between core and edge by offering regional inference at cloud-class throughput. Universities and government labs continue to build in-country clusters for sovereign workloads, ensuring that the cloud’s share edges down slightly even as absolute capacity rises.

By GPU Type: Inference Leadership under Training Upswing

Inference devices led the segment with 56.93% share of the Singapore data center GPU market in 2025 as customer-facing chatbots, fraud detectors, and digital twins demanded low-latency responses, whereas training GPUs are registering the highest growth at 17.45% CAGR through 2031 momentum across the forecast window. Banks opted for H100 NVL cards configured for 60-watt power caps to fit within legacy air corridors, while logistics firms standardized on L40S boards for computer vision. Training-class accelerators, however, posted the quickest growth as large language model developers locked in H200 and early Blackwell allocations.

The Singapore data center GPU market share tilted toward training when public-sector buyers ordered DGX SuperPODs for national security language models. Multi-tenancy constraints limited private clouds to inference-only racks, but new isolation features in GB200-class systems will allow mixed-workload clusters from 2027 onward. Training demand also spurred the adoption of unified memory clusters, ensuring that the two GPU types increasingly coexist rather than compete.

By Interconnect: PCIe Installed Base, InfiniBand Growth Curve

PCIe links accounted for 77.28% of the Singapore data center GPU market in 2025 due to their ubiquity in single-server deployments. High-bandwidth interconnect GPUs are expected to post the quickest expansion as larger language models become commonplace at 16.89% CAGR through 2031. Small clusters in engineering firms and video studios continue to favor PCIe for cost reasons, but limitations emerge once node counts exceed 8. Training labs now default to 400 Gbit s-1 InfiniBand, and early adopters are testing 800 Gbit s-1 Quantum-X800 fabrics for 10-trillion-parameter models.

High-bandwidth interconnect GPUs have become the fastest-expanding slice of the Singapore data center GPU market. The ASPIRE 2A+ cluster demonstrates that time-to-solution improvements justify a 20% capital premium, slashing simulation runtimes from months to days. Vendors now bundle liquid loops and busbars designed for 96-GPU trays, foregrounding interconnect choice as a core design variable.

By Workload Type: AI Dominant, Analytics Surging

Artificial intelligence and machine learning tasks held 53.81% of the Singapore data center GPU market in 2025, covering recommendation engines, vision pipelines, and speech synthesis, with data analytics overtaking all other use cases as the fastest climber at 17.58% CAGR through 2031. Yet GPU-accelerated data analytics logged the steepest climb, as vector search and SQL push-downs re-wrote ETL economics. Financial houses report 44% faster query runtimes using GPU-based data warehouses, enabling intraday risk recalculations.

High-performance computing remains significant in public labs, where molecular dynamics and weather models demand double-precision throughput. Graphics workloads such as digital twins now merge with AI inference to render 3D factories in real time for predictive maintenance. The Singapore data center GPU industry is therefore converging on hybrid workloads that require both tensor and raster pipelines, reinforcing the need for versatile accelerators.

By End-User: Hyperscaler Weight, Enterprise Upshift

Hyperscalers and cloud service providers represented 61.54% of the Singapore data center GPU market share in 2025, absorbing nearly every Blackwell slot available in the first allocation round, while hyperscalers remain the fastest-expanding customer group at 17.02% CAGR through 2031 as they continue multibillion-dollar build-outs across India. Colocation landlords report that single tenants now reserve entire 30-megawatt blocks, leaving little swing capacity for smaller buyers.

Enterprise buyers, however, are scaling fastest, spurred by data residency mandates and rising inference traffic. Telecom operators deploy GB200 racks for customer analytics, while ports bring inference nodes quayside to orchestrate autonomous cranes. Government and research arms expand national supercomputing fleets with GPU-only partitions to attain world-top-100 rankings. The Singapore data center GPU market, therefore, broadens even as vendor concentration at the silicon layer stays high.

Geography Analysis

Singapore remains Southeast Asia’s unmistakable GPU nexus thanks to policy clarity, dense submarine cable nodes, and investor confidence. Colocation charges of USD 420-480 per kilowatt per month rank among the world’s highest, yet operators continue to add capacity because integrated cable-landing data centers cut regional latency below 10 milliseconds, a critical threshold for real-time AI. The Green Data Center Roadmap’s 1.3 PUE ceiling positions Singapore as an early adopter of immersion cooling, while the 50% renewable mandate spurs development of solar imports from Malaysia and Indonesia. Cross-border competition is nevertheless intensifying. Malaysia markets 3x lower power costs, prompting some firms to place training clusters in Johor and inference clusters in Singapore. Keppel DC REIT’s 720-megawatt reserve in Melbourne shows operators diversifying beyond the city-state’s scarce land bank. Even so, the Singapore data center GPU market retains a first-mover advantage in talent, regulation, and network reach. Sustainability constraints will shape future builds. The Public Utilities Board now requires 50% water recycling for high-density halls, a rule that mirrors wafer-fab targets and raises capex for cooling towers. Power imports via the Laos-Thailand-Malaysia-Singapore line add renewable headroom after 2027, but until then, operators optimize per-rack density, ensuring the city continues to deliver more compute per square meter than any global peer.

Competitive Landscape

NVIDIA controls roughly 80% of the global AI accelerator market, a dominance that translates directly into Singapore's procurement patterns. AMD’s MI300 ramps slowly, and Intel’s Gaudi remains niche. Supply, therefore, hinges on TSMC’s CoWoS packaging capacity, which NVIDIA secures ahead of rivals, turning allocation decisions into a gating factor for local projects.

At the operator tier, competition revolves around speed-to-market and cooling IP. Supermicro claims 70% of the direct-liquid-cooling server segment, delivering nodes in weeks and courting hyperscalers facing build deadlines. Dell and Hewlett Packard Enterprise differentiate on managed-service layers, promising turnkey clusters with integrated MLOps stacks. Nxera sets the latency bar by pairing cable landings with 1.25 PUE halls, while Digital Realty commits USD 5.2 billion to preserve scale leadership.

Disruptors emerge as decentralized GPU-as-a-service platforms that aggregate idle silicon across the region. They pitch 40-90% cost savings but still lack enterprise-grade SLAs. Edge specialists field prefab micro-data centers rated at 9 kilowatts for roadside AI boxes, expanding addressable demand. The Singapore data center GPU market, therefore, juxtaposes silicon concentration with operator diversity, fostering innovation in power, cooling, and service tiers.

Singapore Data Center GPU Industry Leaders

NVIDIA Corporation

Advanced Micro Devices, Inc.

Intel Corporation

Super Micro Computer, Inc.

Dell Technologies Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Digital Realty set a USD 5.2 billion investment target for new GPU-ready campuses in Singapore.

- April 2026: Firmus AI reached a USD 5.5 billion valuation after fresh funding led by NVIDIA.

- April 2026: Microsoft confirmed a USD 5.5 billion program to expand GPU zones through 2029.

Singapore Data Center GPU Market Report Scope

Data Center GPU refers to a specialized graphics processing unit engineered for large-scale computing environments, such as enterprise data centers and cloud platforms, rather than for personal computers or gaming.

The Singapore Data Center GPU Market Report is Segmented by Deployment Type (Cloud Data Centers, Enterprise/Private Data Centers, and Edge Data Centers), GPU Type (Training GPUs, Inference GPUs), Interconnect (PCIe-Based GPUs, and High-Bandwidth Interconnect GPUs), Workload Type (Artificial Intelligence (AI) and Machine Learning (ML), High-Performance Computing (HPC) (non-AI scientific computing), Data Analytics (database acceleration, query processing), and Graphics and Visualization (VDI, rendering, digital twins)), and End-User (Hyperscalers/Cloud Service Providers, Enterprises, and Government and Research Institutions). The Market Forecasts are Provided in Terms of Value (USD).

| Cloud Data Centers |

| Enterprise / Private Data Centers |

| Edge Data Centers |

| Training GPUs |

| Inference GPUs |

| PCIe-Based GPUs |

| High-Bandwidth Interconnect GPUs |

| Artificial Intelligence and Machine Learning |

| High-Performance Computing (non-AI scientific computing) |

| Data Analytics (database acceleration, query processing) |

| Graphics and Visualization (VDI, rendering, digital twins) |

| Hyperscalers / Cloud Service Providers |

| Enterprises |

| Government and Research Institutions |

| By Deployment Type | Cloud Data Centers |

| Enterprise / Private Data Centers | |

| Edge Data Centers | |

| By GPU Type | Training GPUs |

| Inference GPUs | |

| By Interconnect | PCIe-Based GPUs |

| High-Bandwidth Interconnect GPUs | |

| By Workload Type | Artificial Intelligence and Machine Learning |

| High-Performance Computing (non-AI scientific computing) | |

| Data Analytics (database acceleration, query processing) | |

| Graphics and Visualization (VDI, rendering, digital twins) | |

| By End-User | Hyperscalers / Cloud Service Providers |

| Enterprises | |

| Government and Research Institutions |

Key Questions Answered in the Report

How large is the Singapore data center GPU market in 2026?

It is valued at USD 0.42 billion and is on track to reach USD 0.79 billion by 2031 at a 13.37% CAGR.

Which deployment model adds the most new GPU capacity?

Cloud data centers dominate because hyperscalers pre-committed power-dense halls ahead of the DC-CFA2 deadline.

Why is liquid cooling becoming standard in Singapore builds?

Policies cap PUE at 1.3 and land-power limits drive rack densities above 40 kilowatts, making immersion or direct-to-chip cooling necessary.

What is driving demand for high-bandwidth interconnects?

Large language model training and multi-node inference need all-to-all communication that PCIe cannot deliver efficiently.

How are enterprises securing GPU resources amid supply constraints?

Many lease turnkey GPUaaS stacks from telecom operators or colocate private clusters in facilities that meet data residency rules.

Does Malaysia’s lower colocation cost threaten Singapore’s position?

Some training clusters move across the border, but Singapore retains the latency, talent, and regulatory advantages for mission-critical inference.

Page last updated on: