Japan Data Center GPU Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

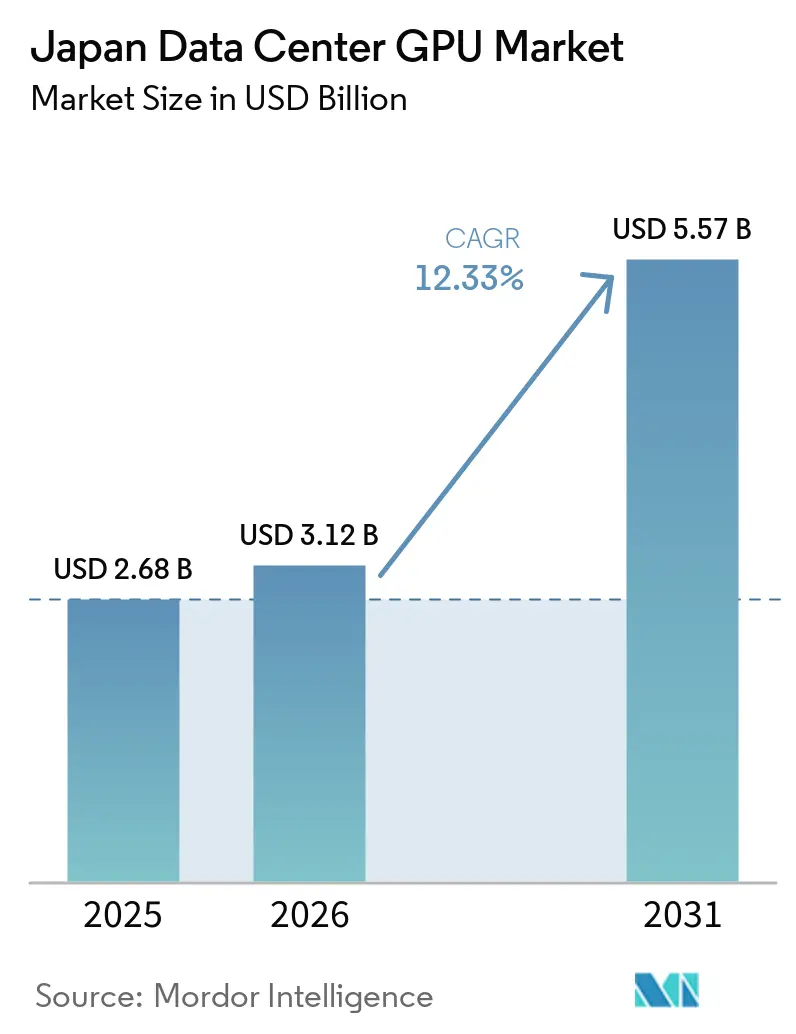

| Base Year Market Size (2025) | USD 2.68 Billion |

| Market Size (2026) | USD 3.12 Billion |

| Market Size (2031) | USD 5.57 Billion |

| Growth Rate (2026 - 2031) | 12.33% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Japan Data Center GPU Market Analysis by Mordor Intelligence

The Japan data center GPU market size is expected to increase from USD 2.68 billion in 2025 to USD 3.12 billion in 2026 and reach USD 5.57 billion by 2031, growing at a CAGR of 12.33% over 2026-2031. Robust sovereign-AI spending by hyperscalers and the Ministry of Economy, Trade and Industry (METI) anchors capital inflows, while enterprises race to embed generative AI into core workflows, pushing demand for training and inference accelerators. Liquid-cooled GPU racks that achieve power usage effectiveness (PUE) of 1.02 in immersion configurations are replacing air-cooled systems, lowering operating costs despite Japan’s high electricity tariffs. Supply-side diversification, led by AMD Instinct and Intel Gaudi accelerators, introduces competitive pricing pressure on NVIDIA and propels the adoption of Ethernet-based scale-out architectures. However, constrained grid capacity in Tokyo and seismic compliance costs keep build-out economics under scrutiny, encouraging brownfield conversions and secondary-city deployments.

Key Report Takeaways

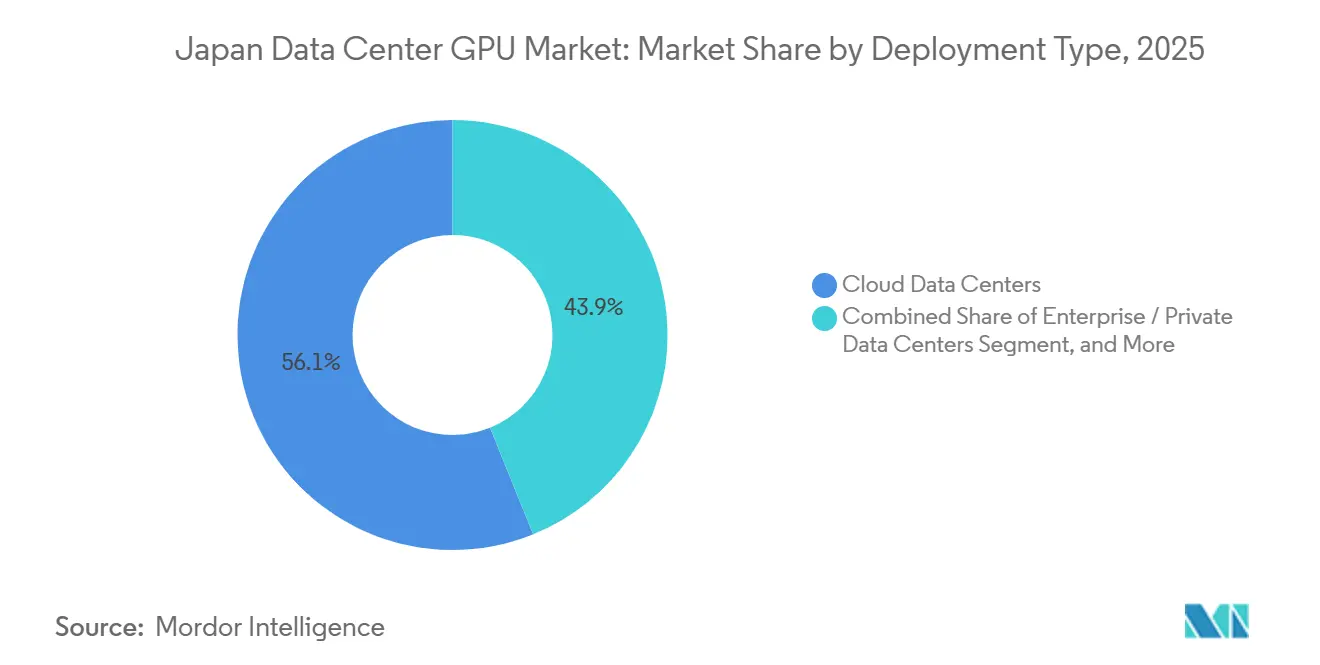

- By deployment type, cloud data centers led with 56.13% revenue share in 2025, while edge facilities are projected to post the fastest CAGR through 2031.

- By GPU type, training GPUs captured 54.68% of the Japan data center GPU market share in 2025; inference GPUs are forecast to expand at the highest CAGR during 2026-2031.

- By interconnect, PCIe-based accelerators accounted for 68.74% share of the Japan data center GPU market size in 2025, whereas high-bandwidth NVLink and InfiniBand GPUs are advancing at the fastest pace.

- By workload, artificial intelligence and machine learning held 55.26% share in 2025; graphics and visualization workloads are expected to register the strongest growth to 2031.

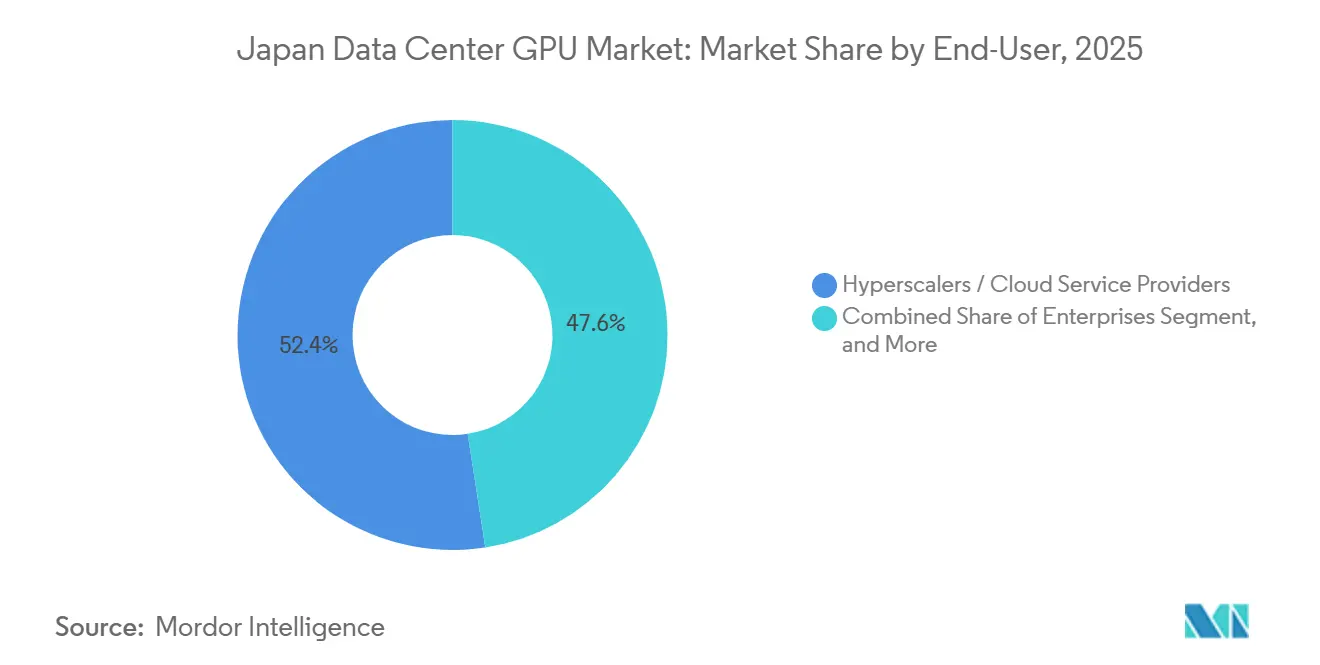

- By end user, enterprises commanded 52.43% of revenue in 2025 and continue to outpace hyperscalers and public-sector buyers in incremental GPU procurement.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Japan Data Center GPU Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating AI and ML Adoption Across Japanese Enterprises | +4.2% | National, concentrated in Tokyo, Osaka, Nagoya metropolitan areas | Medium term (2-4 years) |

| Government's Society 5.0 Initiatives Driving HPC Infrastructure | +3.1% | National, with emphasis on RIKEN, AIST, university consortia | Long term (≥4 years) |

| Expansion of Hyperscale Cloud Capacity in Japan | +2.8% | National, focused on Tokyo, Osaka, Hokkaido regions | Short term (≤2 years) |

| Growing Demand for Cloud Gaming and Streaming Services | +0.9% | National, urban centers with high broadband penetration | Medium term (2-4 years) |

| Corporate Decarbonization Targets Catalyzing Energy-Efficient GPUs | +0.7% | National, led by large enterprises in manufacturing and finance | Long term (≥4 years) |

| Emergence of Regional Edge Data Centers Near Manufacturing Clusters | +0.6% | Regional, concentrated in Aichi, Shizuoka, Kanagawa prefectures | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Accelerating AI and ML Adoption Across Japanese Enterprises

Japanese banks, manufacturers, and professional-services firms are embedding generative AI into daily operations, fueling outsized demand for on-premises and hybrid GPU clusters. Sakura Internet expanded its inventory to 10,800 NVIDIA HGX B200 accelerators, supported by a JPY 50.1 billion (USD 334 million) METI subsidy, to satisfy enterprises unwilling to deploy proprietary models in multi-tenant clouds. Microsoft’s USD 2.9 billion commitment to train 1 million workers in AI skills underscores the talent gap that Japanese companies must bridge to operationalize new workloads.[1]Microsoft Corp., “USD 2.9 Billion Japan AI Investment,” news.microsoft.comGMO Internet’s August 2025 rollout of 200 NVIDIA B300 GPUs demonstrated that multi-instance partitioning can cut per-query inference costs by 40%, accelerating production deployments. As proof-of-concept pilots morph into revenue-bearing services, the Japan data center GPU market benefits from sustained enterprise-led refresh cycles. Financial institutions now run retrieval-augmented generation models for compliance automation, while automotive suppliers apply vision transformers for defect detection with sub-millisecond latency.

Government's Society 5.0 Initiatives Driving HPC Infrastructure

Public-sector investment anchors long-term demand visibility. RIKEN’s FugakuNEXT roadmap integrates 2,140 NVIDIA Blackwell GPUs into exascale systems scheduled for spring 2026, advancing national climate and drug-discovery research.[2]RIKEN, “Blackwell Deployment for FugakuNEXT,” riken.jp AIST’s ABCI 3.0, live since January 2025 with NVIDIA H200 GPUs and Quantum-2 InfiniBand, offers subsidized compute at up to 70% below commercial cloud rates, democratizing access for startups and universities. These flagship programs de-risk GPU adoption by demonstrating sustained performance at scale and building a domestic talent pipeline. NEC’s November 2024 contract to deliver a 40.4 petaflops supercomputer combining Intel Xeon 6900P CPUs with AMD Instinct MI300A GPUs showcases multi-vendor heterogeneity in national research infrastructure. The Society 5.0 agenda, therefore, stimulates both public and private spending and reinforces long-term confidence in the Japanese data center GPU market.

Expansion of Hyperscale Cloud Capacity in Japan

Amazon Web Services, Microsoft, and Oracle have earmarked a combined USD 28 billion through 2029 to expand their presence in the Tokyo and Osaka regions with liquid-cooled GPU clusters.[3]Amazon Web Services, “USD 15 Billion Japan Expansion,” press.aboutamazon.comOracle’s 50,000-unit AMD MI450 and MI355X deployment, starting Q3 2026, represents one of the world’s largest non-NVIDIA GPU installations and tests price elasticity in training workloads. Cloud providers shorten procurement lead times from 12-18 months to minutes, letting mid-market firms experiment with large language models without capital outlays. NTT aims to double global capacity to 4 GW by 2028, channeling sizeable GPU power toward domestic tenants. Together, these projects improve availability, reduce latency, and introduce competitive pricing to democratize high-end accelerators.

Emergence of Regional Edge Data Centers Near Manufacturing Clusters

Automotive and electronics manufacturers deploy edge facilities within or adjacent to factories to maintain sub-5-millisecond inference latency. Ubitus announced a JPY 17 billion (USD 113 million) program in December 2025 to build GPU nodes across Aichi, Shizuoka, and Kanagawa, targeting real-time quality control workflows.[4]Ubitus, “Regional GPU Infrastructure Announcement,” strainer.jp HiRezo’s March 2026 GPU center in Kagawa, equipped with NVIDIA A4000 and H100 GPUs, illustrates demand arising from regional industrial bases. Edge facilities also sidestep Tokyo’s grid connection queue, as utilities in Hokkaido and other secondary regions grant faster approvals and charge lower tariffs, trimming operating costs by up to 30%. NEC’s ExpEther solution, launched in January 2026, disaggregates GPUs across buildings over 100 Gbps Ethernet, allowing manufacturers to place accelerators in thermally optimized enclosures while retaining microsecond latency.

Restraints Impact Analysis*

| High Capital Expenditure and Long ROI Cycles | -2.4% | National, most acute in Tokyo and Osaka metropolitan areas | Short term (≤2 years) |

|---|---|---|---|

| Semiconductor Supply Constraints for Advanced Nodes | -1.7% | National, with spillover effects from Taiwan and South Korea supply chains | Medium term (2-4 years) |

| Skills Shortage in GPU Cluster Management | -0.8% | National, concentrated in enterprises outside Tokyo metropolitan area | Long term (≥4 years) |

| Stricter Earthquake-Resilience Standards Inflating Build Costs | -0.6% | National, most severe in Pacific coastal zones (Tokyo, Osaka, Shizuoka) | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

High Capital Expenditure and Long ROI Cycles

Japan’s seismic engineering codes lift greenfield Tier IV cost to USD 8-12 per watt of IT load, equal to USD 800 million-1.2 billion for a 100 MW campus, 30-40% above global norms. Electricity averaging USD 0.09-0.13 per kWh further erodes margins, with a 100 MW facility incurring roughly USD 44.7 million in annual power expense. Cloud GPUs, available at USD 1.50-2.50 per hour, outcompete on-premises clusters that amortize at USD 1.70 per hour over three years, extending payback to as long as four years. Brownfield conversions like KDDI’s Osaka Sakai project save JPY 10 billion (USD 67 million) and compress timelines to under one year, yet suitable sites remain scarce. Grid connection queues of up to ten years in Tokyo magnify ROI uncertainty.

Semiconductor Supply Constraints for Advanced Nodes

HBM3 and HBM3e scarcity caps NVIDIA H100 and Blackwell shipments, leaving demand 20-30% ahead of supply into 2027. Small and medium enterprises struggle to secure GPUs as vendors favor hyperscalers, echoing the 2025 retail shortage of RTX 5060 Ti boards in Japan. Japan depends on TSMC’s leading-edge nodes; the 2024 Hualien earthquake, which cut wafer starts by up to 7%, spotlights geopolitical supply risks. AMD Instinct and Intel Gaudi provide modest diversification, yet AMD holds under 5% share, and Gaudi remains niche within IBM Cloud. Consequently, operators extend refresh cycles and hedge build schedules, moderating near-term capacity additions in the Japan data center GPU market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Type: Cloud Dominates, Edge Accelerates

Cloud data centers generated 56.13% of 2025 revenue in the Japan data center GPU market, reflecting hyperscalers’ ability to amortize billion-dollar campuses across thousands of tenants while offering on-demand H100 instances that bypass 18-month procurement cycles. Enterprises embrace cloud for burst training, yet edge data centers are the fastest-growing slice as manufacturers demand sub-5 millisecond latency on machine-vision tasks. Ubitus’s USD 113 million rollout places GPU nodes within 10-20 kilometers of production lines, eliminating wide-area round-trip delay and boosting quality-inspection throughput by up to 25%.

The edge surge is underpinned by lower power tariffs in secondary cities, available land, and looser grid queues. HiRezo’s Kagawa facility leverages provincial incentives to reduce energy costs by roughly 20%, while NEC’s ExpEther infrastructures enable GPU disaggregation, trimming capital intensity by 30% versus fixed clusters. Brownfield conversions such as KDDI’s Osaka Sakai site underscore a strategic pivot toward adaptive reuse that shortens time-to-market and spreads the Japan data center GPU market footprint beyond the Tokyo-Osaka axis.

By GPU Type: Training Retains Majority While Inference Surges

Training GPUs held 54.68% of 2025 spending, anchored by national supercomputing procurements like RIKEN’s 2,140 Blackwell units for exascale simulations. Nevertheless, inference accelerators are scaling faster as enterprises shift to production LLM deployment; GMO Internet partitions each NVIDIA B300 into seven inference slices, trimming query costs by 40% and elevating device utilization.

With fine-tuning replacing pre-training for most companies, the Japan data center GPU market size for inference is on a steeper trajectory. NVIDIA’s H200 boosts FP8 throughput threefold, while Intel Gaudi 3 claims 50% higher inference/sec versus H100 on select tasks, tempting cost-sensitive buyers. The performance-per-watt gains reinforce a pivot toward multi-instance, low-latency serving.

By Interconnect: PCIe Leads, NVLink Gains Ground

PCIe cards comprised 68.74% of 2025 installations, favored by enterprise and edge sites that rely on air-cooled 10-15 kW racks. In hyperscale campuses, however, NVLink and InfiniBand are rapidly expanding their share as training runs span hundreds of GPUs. KDDI’s GB200 NVL72 racks deliver 260 TB/s of bandwidth, reducing all-reduce times for trillion-parameter models by 14× compared to PCIe clusters.

RIKEN and AIST mirror the trend, pairing H200 GPUs with Quantum-2 InfiniBand to sustain exascale throughput. AMD’s MI300A uses high-bandwidth Infinity Fabric, introducing vendor diversity at national labs. For enterprises, the cost premium of liquid cooling and proprietary fabrics preserves PCIe’s dominance, yet rising model sizes continue to shift share toward high-bandwidth interconnects in the overall Japan data center GPU market share.

By Workload Type: AI Dominates, Visualization Accelerates

AI and ML workloads commanded 55.26% of 2025 expenditure, but graphics and visualization now record the fastest expansion as digital-twin platforms proliferate. NTT PC Communications uses NVIDIA Omniverse with multi-vGPU licensing to support remote design collaboration at 60 fps, replacing high-end workstations and cutting software maintenance overhead.

Enterprises increasingly view AI training as periodic, whereas inference, rendering, and simulation drive day-to-day utilization. Ureru Net’s April 2026 immersion-cooled data center integrates 1,000 NVIDIA B200 GPUs to service mixed AI-plus-rendering queues, achieving PUE as low as 1.02 and validating ultra-dense deployments in seismic zones. The evolution of the workload mix underpins steady diversification in the Japan data center GPU market.

By End-User: Enterprise First, Cloud Closing In

Enterprises held 52.43% share in 2025, diverging from global norms where hyperscalers dominate GPU purchases. Sakura Internet’s domestic build, subsidized by METI, addresses sovereignty concerns that deter Japanese firms from sharing silicon with competitors. Financial services groups deploy retrieval-augmented generation models on dedicated clusters to satisfy stringent data-handling rules, while automotive suppliers co-locate GPUs near assembly lines for instant defect detection.

Cloud providers race to narrow the cost gap: Oracle’s mass AMD rollout and IBM Cloud’s Gaudi-backed instances promise lower hourly rates, potentially enticing conservative enterprises into hybrid arrangements. Government and research bodies maintain a steady demand through multi-year programs, stabilizing baseline volumes in the Japan data center GPU market.

Geography Analysis

Tokyo and Osaka anchor demand thanks to fiber density and proximity to corporate headquarters, yet grid congestion and land premiums squeeze expansion. TEPCO’s 5-10 year connection queue forced KDDI to convert Sharp’s Sakai LCD plant in Osaka, slashing build schedules to under one year and saving USD 67 million by reusing infrastructure. Operators now weigh Osaka’s lower land prices and Kansai’s industrial base when allocating future capacity.

Hokkaido attracts colder-climate builds, offering tariffs of USD 0.06-0.07 per kWh that cut operating expense by up to 30% for the Japan data center GPU market. Regional cities, including Kagawa and Aichi, host edge projects that position GPUs within minutes of factory floors, a pattern exemplified by HiRezo’s March 2026 launch. This dispersion mitigates seismic clustering risk and aligns with METI’s JPY 114.6 billion subsidy program that spreads sovereign-AI capacity nationwide.

Seismic standards influence site economics: coastal zones that adhere to the Japan Data Center Council Tier IV add 24-27% to structural budgets. Consequently, some operators pivot inland, trading network proximity for lower capex. Collectively, the geographic mosaic balances latency, cost, and resiliency, shaping the forward distribution of the Japan data center GPU market share.

Competitive Landscape

The landscape remains moderately concentrated: NVIDIA controls high-end training and inference, yet AMD and Intel inject heterogeneity. Oracle’s 50,000-unit MI450 and MI355X deployment signals scale that could compress NVIDIA premiums, while IBM Cloud’s April 2025 Gaudi 3 launch offers an Ethernet-based alternative that avoids proprietary fabrics.

Japanese vendors leverage sovereignty differentiators. Fujitsu began domestic production of HGX B300 and Blackwell servers in March 2026, ensuring local supply and seismic compliance. NEC’s ExpEther disaggregation cuts over-provisioning, resonating with enterprises guarding capital budgets.

Hardware competition now extends to cooling and integration. Supermicro’s alliance with KDDI and Foxconn deploys liquid-cooled racks delivering a PUE of 1.15, while Ureru Net’s immersion design pushes PUE to 1.02 and demonstrates feasibility in quake-prone regions. As pricing converges, software ecosystems and total cost of ownership become decisive, positioning the Japan data center GPU market for increased vendor diversity.

Japan Data Center GPU Industry Leaders

NVIDIA Corporation

Advanced Micro Devices Inc.

Intel Corporation

Amazon Web Services Inc.

Fujitsu Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Ureru Net established BCDC.Ai.GPU Data Center with 1,000 NVIDIA B200 GPUs using immersion cooling, achieving PUE 1.02-1.04 and 200 kW per rack density.

- March 2026: Fujitsu began local manufacture of HGX B300 and Blackwell servers compliant with JDCC Tier IV seismic norms.

- March 2026: HiRezo opened a Kagawa GPU center featuring NVIDIA A4000 and H100 accelerators to serve Shikoku manufacturers.

Japan Data Center GPU Market Report Scope

The Japan Data Center GPU Market Report is Segmented by Deployment Type (Cloud Data Centers, Enterprise/Private Data Centers, Edge Data Centers), GPU Type (Training GPUs, Inference GPUs), Interconnect (PCIe-Based GPUs, High-Bandwidth Interconnect GPUs), Workload Type (AI and ML, HPC, Data Analytics, Graphics and Visualization), and End-User (Hyperscalers/CSPs, Enterprises, Government and Research Institutions). Market Forecasts are Provided in Terms of Value (USD).

| Cloud Data Centers |

| Enterprise / Private Data Centers |

| Edge Data Centers |

| Training GPUs |

| Inference GPUs |

| PCIe-Based GPUs |

| High-Bandwidth Interconnect GPUs |

| Artificial Intelligence (AI) & Machine Learning (ML) |

| High-Performance Computing (HPC) (non-AI scientific computing) |

| Data Analytics (database acceleration, query processing) |

| Graphics & Visualization (VDI, rendering, digital twins) |

| Hyperscalers / Cloud Service Providers |

| Enterprises |

| Government & Research Institutions |

| By Deployment Type | Cloud Data Centers |

| Enterprise / Private Data Centers | |

| Edge Data Centers | |

| By GPU Type | Training GPUs |

| Inference GPUs | |

| By Interconnect | PCIe-Based GPUs |

| High-Bandwidth Interconnect GPUs | |

| By Workload Type | Artificial Intelligence (AI) & Machine Learning (ML) |

| High-Performance Computing (HPC) (non-AI scientific computing) | |

| Data Analytics (database acceleration, query processing) | |

| Graphics & Visualization (VDI, rendering, digital twins) | |

| By End-User | Hyperscalers / Cloud Service Providers |

| Enterprises | |

| Government & Research Institutions |

Key Questions Answered in the Report

What is the projected value of the Japan data center GPU market by 2031?

The market is forecast to reach USD 5.57 billion by 2031, expanding at a 12.33% CAGR over 2026-2031.

Which deployment type is growing fastest in Japan?

Edge data centers record the steepest growth as manufacturers need sub-5 ms latency for real-time quality inspection near production lines.

Why are enterprises ahead of hyperscalers in Japan’s GPU demand?

Data sovereignty concerns and hybrid-IT preferences drive Japanese firms to build or lease dedicated clusters rather than rely solely on multi-tenant clouds.

How are seismic standards affecting data center economics?

Tier IV quake-resilient designs add 24-27% to structural budgets, pushing greenfield cost to USD 8-12 per watt of IT load.

Page last updated on: