China Data Center GPU Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

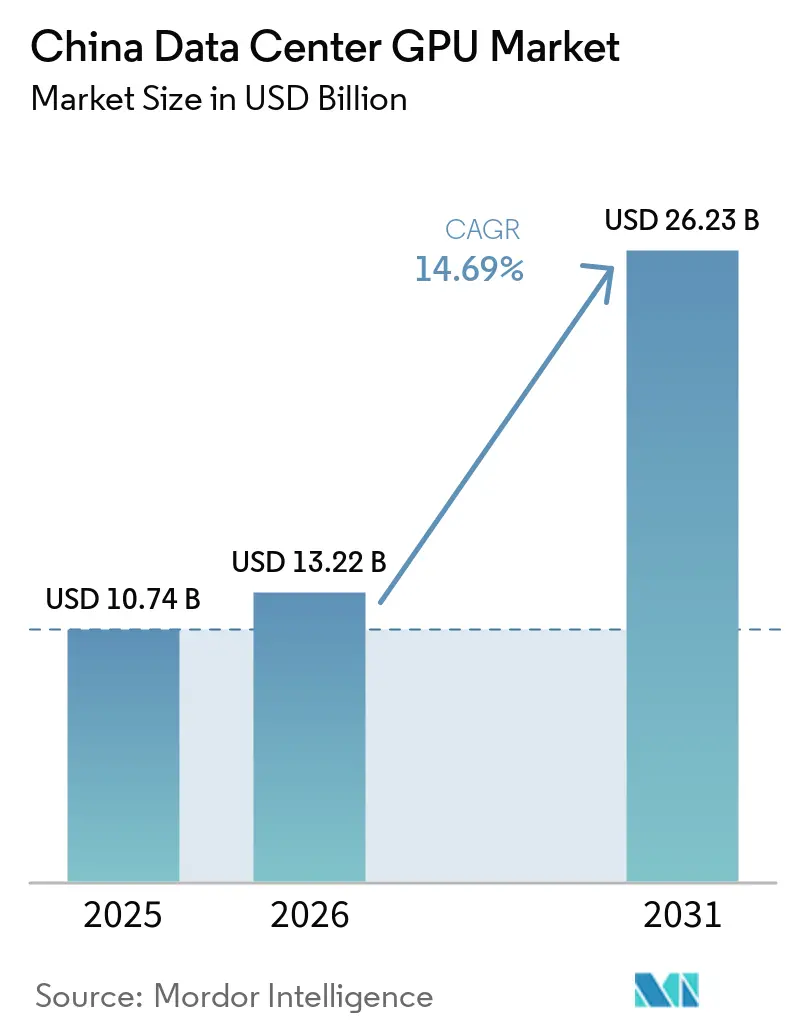

| Base Year Market Size (2025) | USD 10.74 Billion |

| Market Size (2026) | USD 13.22 Billion |

| Market Size (2031) | USD 26.23 Billion |

| Growth Rate (2026 - 2031) | 14.69% CAGR |

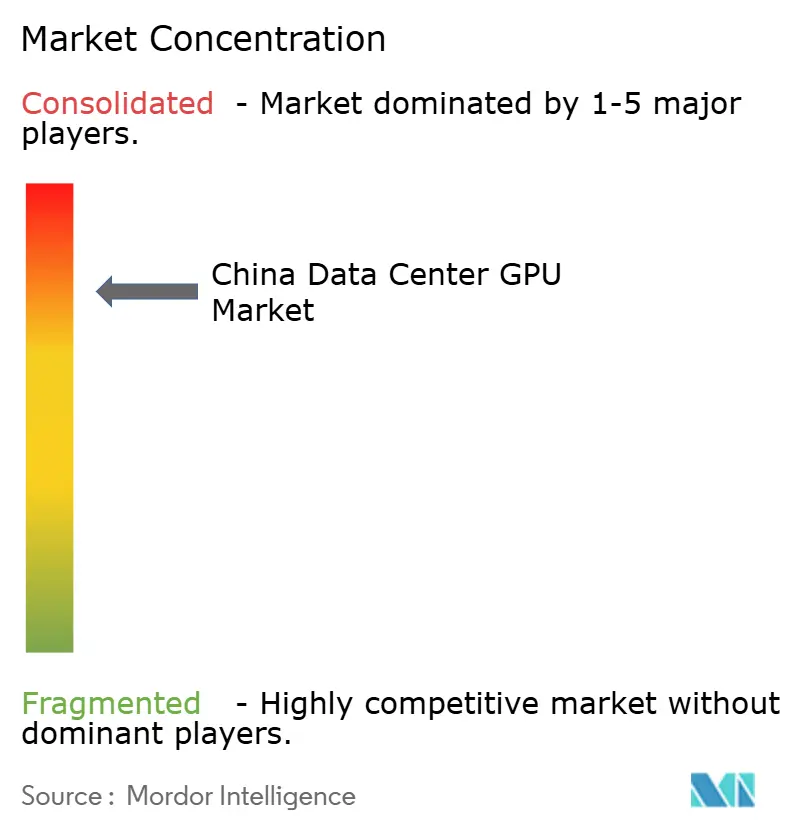

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Data Center GPU Market Analysis by Mordor Intelligence

The China data center GPU market size is projected to be USD 10.74 billion in 2025, USD 13.22 billion in 2026, and reach USD 26.23 billion by 2031, growing at a CAGR of 14.69% from 2026 to 2031. Spending by hyperscalers on 100,000-card clusters, a rapid shift toward domestic accelerators after United States export controls, and provincial voucher programs that cut computing costs by as much as 30% have become the main engines propelling the China data center GPU market. Liquid-cooling systems that keep rack power density below 1.3 PUE, together with hour-rate declines from more than RMB 90 to RMB 15-20 for H20 instances, are strengthening small-enterprise demand and expanding the addressable base for inference and analytics workloads. At the same time, CoWoS and HBM3e tightness limits high-end chip availability, and a younger domestic software stack forces code rewrites that temper full-scale migration from CUDA. Overall, the balance of accelerating capital expenditure, cost-down incentives, and technology bottlenecks explains why growth remains robust yet below the potential implied by announced spending totals.

Key Report Takeaways

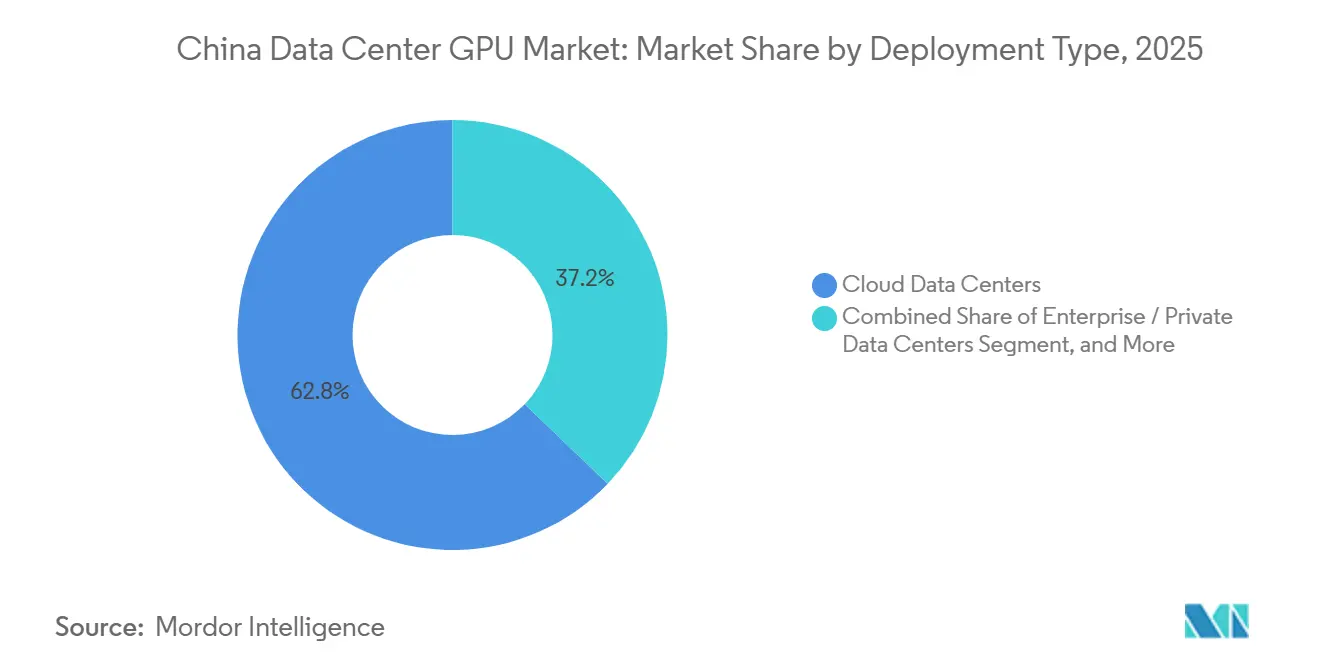

- Cloud data centers led with 62.84% of China data center GPU market share in 2025, while edge data centers are forecast to record the highest 2026-2031 CAGR at 20.3%.

- Inference GPUs accounted for 59.21% share of the China data center GPU market size in 2025 and are projected to expand at a 16.8% CAGR through 2031.

- High-bandwidth interconnect GPUs captured 56.37% share in 2025 and are advancing at a 17.4% CAGR over the forecast period.

- AI and machine-learning workloads dominated with a 73.55% share in 2025; data analytics is set to grow the fastest at a 19.1% CAGR to 2031.

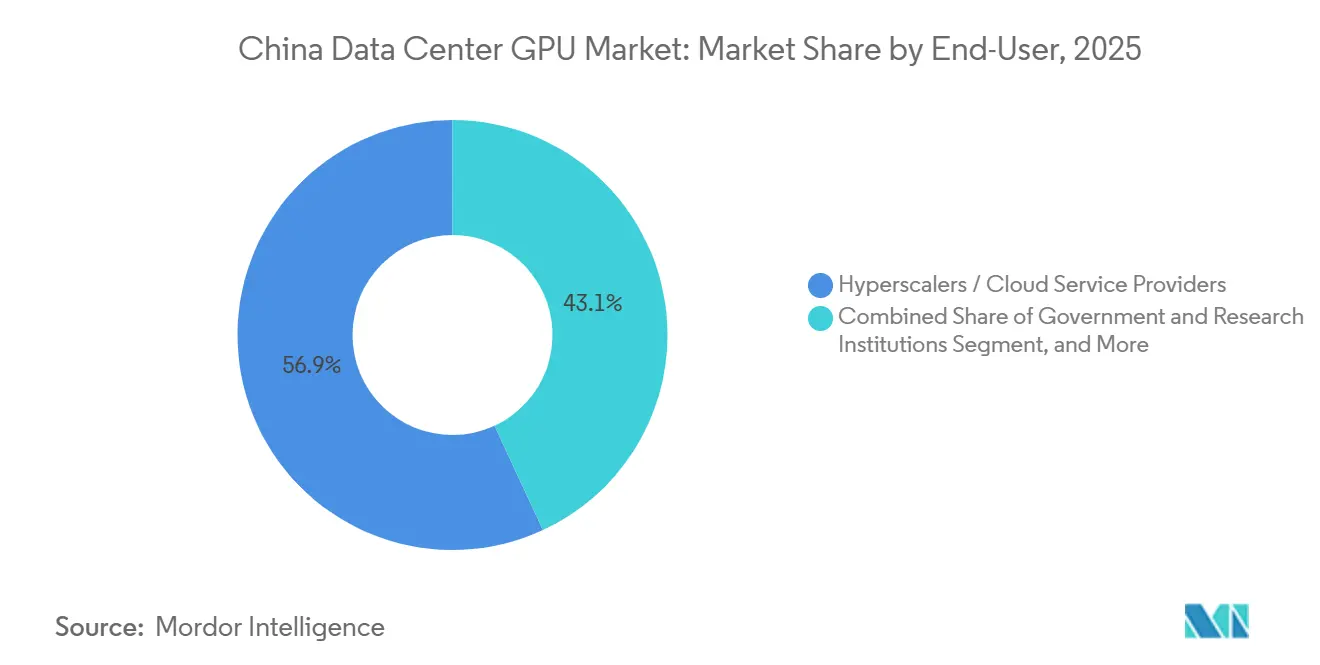

- Hyperscalers and cloud service providers held 56.91% of end-user demand in 2025, whereas enterprises are projected to post the strongest CAGR at 18.2% between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

China Data Center GPU Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Hyperscaler Capex for AI Clusters | +3.2% | National, concentrated in East and South-Central regions | Medium term (2-4 years) |

| Export-Control-Driven Substitution Toward Local GPUs | +2.8% | National, fastest in government and research deployments | Long term (≥ 4 years) |

| Government Vouchers Incentivizing Domestic AI Compute | +2.1% | Shanghai, Fujian, Guizhou, Beijing, Chengdu | Short term (≤ 2 years) |

| Liquid-Cooling Adoption Enabling 80 kW+ Racks | +1.5% | Beijing-Tianjin-Hebei, Yangtze River Delta | Medium term (2-4 years) |

| Rapid Price Declines in GPU Cloud Leasing | +1.3% | Nationwide SME segment | Short term (≤ 2 years) |

| East-Data West-Compute Policy Unlocking Low-Cost Power | +1.0% | Northwest and Southwest hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Hyperscaler Capex for AI Clusters

ByteDance set aside CNY 160 billion (USD 23 billion) for 2026 capital expenditure and devoted half of that sum to GPU purchases, while Alibaba discussed raising infrastructure investment to RMB 480 billion over three years.[2]Tencent Holdings, “Annual Report 2025,” tencent.comTencent doubled its annual AI budget to roughly USD 5 billion in 2026, although earlier supply tightness kept its 2025 spending to RMB 79.2 billion.[1]Wall Street Journal, “US Export Controls on H200 GPUs,” wsj.com Hangzhou’s USD 3.7 billion procurement package illustrates municipal co-investment that compounds corporate outlays. United States export licenses allowed limited H200 imports with a 25% tariff and 50% volume cap, nudging hyperscalers toward Huawei Ascend alternatives. Activity centers on the Yangtze River Delta and the Greater Bay Area, where sub-10-millisecond latency and 300 watts per rack of power headroom accommodate multi-card clusters.

Export-Control-Driven Substitution Toward Local GPUs

The block on advanced NVIDIA and AMD accelerators since mid-2025 stimulated Huawei shipments that topped 50,000 Ascend 910B units by year-end 2025 and planned 750,000 Ascend 950PR chips for 2026. The 910C and 950PR deliver 60-80% of H100 throughput and ride SMIC’s N+3 process, shrinking reliance on TSMC packaging capacity. Cambricon’s 2024 revenue surged 67.4% to RMB 1.28 billion, and investment banks see domestic self-sufficiency reaching 50% by 2027. Mandates favoring indigenous tech speed adoption in public-sector and military workloads. Even private hyperscalers add domestic cards to hedge license risk.

Government Vouchers Incentivizing Domestic AI Compute

Shanghai earmarked CNY 600 million for vouchers that reimburse up to 30% of compute charges, while Fujian offers a 50% subsidy capped at RMB 500,000 per firm per year. Guizhou issued 152 coupons worth CNY 2.182 billion tied to 110,000 Ascend chips across 48 data centers. Beijing and Chengdu launched parallel schemes in 2025, reducing effective GPU-hour rates for inference tasks. Voucher rules usually limit reimbursement per GPU-hour, so enterprises prioritize inference clusters that consume lower power and integrate faster than large-scale training builds. The policy shortens payback periods and accelerates the China data center GPU market’s transition to production workloads.

Liquid-Cooling Adoption Enabling 80 kW+ Racks

Regulators in Beijing and Tianjin impose PUE thresholds below 1.3, forcing operators to move beyond air cooling. Dawning released a megawatt-class phase-change immersion solution topping 900 kW in April 2026. KSTAR followed in October 2025 with 600 kW distribution units that fit 64-128 high-end GPUs per rack. [3]Shanghai Municipal Government, “Computing Power Voucher Program,” shanghai.gov.cnAcross China, documented immersion capacity reached 15-20 MW by early 2026, chiefly in Beijing-Tianjin-Hebei and Yangtze River Delta clusters. Liquid cooling lowers PUE to below 1.2 and carves roughly 20% off electricity bills, enabling denser clusters within the same grid envelope. This technological shift is a gateway for edge and micro-module deployments where space and power are limited.

Rapid Price Declines in GPU Cloud Leasing

Hourly rates for NVIDIA H20 instances collapsed from above RMB 90 in early 2025 to RMB 15-20 by early 2026. The price drop widened access to LLM inference for smaller developers who could not justify the upfront cost of hardware acquisition.[4]Dawning Information Industry, “Phase-Change Immersion Cooling Launch,” sugon.comCompetition among hyperscalers, combined with voucher reimbursements, means an enterprise can now run a 7-billion-parameter chatbot for less than RMB 0.05 per query, with a 64% gross margin. Lower entry costs channel demand toward inference cards on 6-nanometer nodes that sidestep CoWoS constraints and ease pressure on HBM supply chains.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Advanced Packaging (CoWoS/HBM) Capacity Bottlenecks | -1.8% | Global, limiting imports and domestic tape-outs | Medium term (2-4 years) |

| Persistent Software Ecosystem Gap vs CUDA | -1.4% | Nationwide, impacts enterprise migration speed | Long term (≥ 4 years) |

| Low Utilization Rates in Newly Built AI Centers | -0.9% | Northwest and Southwest hubs | Short term (≤ 2 years) |

| Grid-Connection Delays in Remote Western Hubs | -0.7% | Inner Mongolia, Gansu, Ningxia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Advanced Packaging (CoWoS/HBM) Capacity Bottlenecks

TSMC quadrupled CoWoS output to about 120,000 wafers per month by early 2026, yet NVIDIA locks down close to 60% of that allocation. HBM3e remains tight with a 30% global shortfall even after SK Hynix and Samsung expansions. Domestic vendors tap 7-nanometer nodes with LPDDR memory to avoid the queue, but high-end training chips still need CoWoS, delaying deliveries by more than 50 weeks. The bottleneck forces Chinese buyers to stretch training schedules or pay premiums for scarce imports, clipping near-term upside for the China data center GPU market.

Persistent Software Ecosystem Gap vs CUDA

CUDA has matured over 18 years with thousands of optimized libraries. Huawei’s CANN stack, even after open-sourcing in August 2025, offers fewer operators, so developers report rewriting up to 40% of code when moving workloads. NVIDIA banned translator layers from CUDA 11.6 onward, raising migration friction. CANN 8.0 narrows the gap with 200 optimized ops, yet autonomous-vehicle and drug-discovery teams that spent years tuning CUDA kernels resist wholesale shifts. The lag curbs the addressable base for domestic GPUs and holds back conversions despite attractive price-performance.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Type: Edge Acceleration Outpaces Cloud Consolidation

Edge facilities represented the fastest-growing slice of the China data center GPU market during 2025 and are forecast to post a 20.3% CAGR through 2031. Cloud data centers still dominate with 62.84% of China's data center GPU market share in 2025, thanks to hyperscalers that run 100,000-GPU clusters to achieve economies of scale.

China Mobile and China Unicom staged 5G MEC pilots that use GPUs for cloud gaming and real-time video, proving that sub-15-millisecond round-trip is achievable when compute sits within the city core. Lower leasing prices weaken the business case for small private halls, so many mid-sized firms burst workloads into public cloud but keep sensitive data on on-premise edge nodes. Liquid-cooled micro-modules shipping from ZTE help solve space and power limitations in retail and factory environments.

By GPU Type: Inference Dominance Reflects Deployment-Phase Economics

Inference accelerators held 59.21% of the China data center GPU market size in 2025 and are projected to grow at a 16.8% CAGR, making them both the largest and fastest segment. Training GPUs, while indispensable for new foundation models, expand more slowly as major clusters already exist and inference drives near-term revenue.

Alibaba Cloud’s TensorRT-LLM and vLLM services can answer billions of daily calls on mid-tier GPUs paired with LPDDR memory, cutting chip costs by 30-40% against HBM-based alternatives. Huawei’s 950PR sold to ByteDance focuses on inference throughput with 1.56 PFLOPS FP4 rather than peak FP16 performance. Domestic designers choose 6- or 7-nanometer nodes to dodge CoWoS queues, aligning with price-sensitive inference deployments.

By Interconnect: Bandwidth-Intensive Workloads Drive High-Speed Fabric Adoption

High-bandwidth interconnect GPUs secured 56.37% of 2025 sales and should keep expanding faster than PCIe cards to 2031. Distributed SQL and trillion-parameter model training require 400-Gbps links and microsecond-scale latency.

Alibaba’s 700-GB/s Zhenwu fabric reached 95% utilization in a 10,000-card cluster brought online in April 2026. Huawei’s Atlas 950 SuperPoD strings 8,192 Ascend 950DT chips into 8 exaflops of FP8 compute with proprietary switching, answering the same need. State-operated carriers are subsidizing backbone upgrades that will bring 400-Gbps to 42 cities by 2028, removing the last hurdle to cross-regional distributed training.

By Workload Type: Analytics Acceleration Captures Enterprise Budgets

AI and ML commanded a 73.55% share in 2025, but GPU-accelerated analytics shows the highest growth and is on track for a 19.1% CAGR. Financial services and e-commerce firms deploy GPU SQL engines that shrink query latency from hours to seconds, unlocking immediate ROI.

Sub-second TPC-H performance on 1-TB data sets proves why enterprises shift budgets from model training to monetizing existing data. Affordable H20 cloud rates mean a mid-size merchant can spin up 64 GPUs for weekend batch ETL jobs without capex. HPC and CAD visualization grow steadily but stay niche compared with production analytics workloads that feed real-time pricing and fraud models.

By End-User: Hyperscaler Oligopoly Faces Enterprise Diversification

Hyperscalers accounted for 56.91% of 2025 demand and still anchor the China data center GPU market, yet enterprise adoption is projected to lead growth at a 18.2% CAGR. Voucher programs and data-residency rules motivate banks, automakers, and telcos to build private clusters.

ByteDance’s USD 5.6 billion order for 950PR chips illustrates how hyperscalers hedge export uncertainty with domestic silicon. Enterprises blend on-premise nodes for sensitive data with low-cost cloud bursts for peak traffic, a hybrid model made feasible by collapsing hourly rates. Government labs and universities add steady volume under local-procurement mandates tied to indigenous GPUs.

Geography Analysis

East China and South-Central China remained the largest contributors in 2025 on account of dense fiber backbones and power reliability that fulfill sub-10-millisecond requirements. Hangzhou committed USD 3.7 billion to GPU procurement in February 2026, part of a region-wide push that includes Alibaba’s Zhenwu cluster in Shaoguan. Shanghai’s CNY 600 million voucher pool tilts enterprise analytics and inference to local halls, tightening demand for edge micro-centers near industrial parks.

Southwest China is forecast to expand the fastest through 2031 on the back of East-Data West-Compute incentives. Guizhou already hosts 48 intelligent data centers with 85 exaflops of capacity and 110,000 Ascend chips. Chengdu invested CNY 10.9 billion in a Huawei cluster brought online in May 2026, which equals 150,000 high-performance PCs. Power tariffs as low as RMB 0.25/kWh offset latency penalties, but 1-Gbps lines still cost RMB 160,000 monthly, keeping utilization near 40%.

North China, home to ministries and research institutes, pushes liquid-cooling adoption as regulators cap PUE at 1.3 for new builds. Northwest hubs attract big names under cheap-power promises yet face grid-connection delays that slowed more than 100 projects since 2025. Northeast provinces grow slower but benefit from a tripling of state AI allocations in 2024 aimed at revitalizing heavy industry.

Competitive Landscape

Market concentration is moderate. NVIDIA still sells legacy Ampere and H20 parts under cap limits, while Huawei and Cambricon scale domestic offerings. Alibaba’s in-house Zhenwu went live in April 2026 and targets 100,000 cards, signaling that integrated cloud-plus-silicon strategies are no longer limited to U.S. firms. Baidu filed Kunlunxin for a Hong Kong IPO in January 2026 to capture chip value outside its core search and cloud units.

Vendors compete on software abstractions that hide hardware heterogeneity. Huawei open-sourced CANN and Mind to entice PyTorch and Triton developers, adding 200 optimized ops in version 8.0. Dawning and KSTAR invest in immersion cooling that reduces PUE to 1.2 and triples rack density, an advantage when urban land is scarce. MIIT’s national cloud network plan requires cross-vendor orchestration by 2028, so players with flexible schedulers and open APIs are positioned to win regional contracts.

China Data Center GPU Industry Leaders

NVIDIA Corporation

Huawei Technologies Co., Ltd. (Ascend)

Alibaba Group Holding Limited (Kunlunxin/T-Head)

Advanced Micro Devices, Inc.

Biren Technology Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Huawei began mass production of Ascend 950PR on SMIC N+3; ByteDance ordered 750,000 units for Volcengine.

- April 2026: Alibaba activated a 10,000-card Zhenwu cluster in Guangdong with plans to expand tenfold.

- April 2026: Dawning launched 900 kW phase-change immersion systems aimed at hyperscale AI halls.

China Data Center GPU Market Report Scope

The China Data Center GPU Market Report is Segmented by Deployment Type (Cloud Data Centers, Enterprise/Private Data Centers, Edge Data Centers), GPU Type (Training GPUs, Inference GPUs), Interconnect (PCIe-Based GPUs, High-Bandwidth Interconnect GPUs), Workload Type (AI and ML, HPC, Data Analytics, Graphics and Visualization), End-User (Hyperscalers/CSPs, Enterprises, Government and Research Institutions), and Geography (East, North, South Central, Southwest, Northeast, Northwest China). Market Forecasts are Provided in Terms of Value (USD).

| Cloud Data Centers |

| Enterprise / Private Data Centers |

| Edge Data Centers |

| Training GPUs |

| Inference GPUs |

| PCIe-Based GPUs |

| High-Bandwidth Interconnect GPUs |

| Artificial Intelligence (AI) and Machine Learning (ML) |

| High-Performance Computing (HPC) (non-AI scientific computing) |

| Data Analytics (database acceleration, query processing) |

| Graphics and Visualization (VDI, rendering, digital twins) |

| Hyperscalers / Cloud Service Providers |

| Enterprises |

| Government and Research Institutions |

| By Deployment Type | Cloud Data Centers |

| Enterprise / Private Data Centers | |

| Edge Data Centers | |

| By GPU Type | Training GPUs |

| Inference GPUs | |

| By Interconnect | PCIe-Based GPUs |

| High-Bandwidth Interconnect GPUs | |

| By Workload Type | Artificial Intelligence (AI) and Machine Learning (ML) |

| High-Performance Computing (HPC) (non-AI scientific computing) | |

| Data Analytics (database acceleration, query processing) | |

| Graphics and Visualization (VDI, rendering, digital twins) | |

| By End-User | Hyperscalers / Cloud Service Providers |

| Enterprises | |

| Government and Research Institutions |

Key Questions Answered in the Report

What revenue level will China’s data-center GPU market likely hit by 2031?

It is forecast to reach USD 26.23 billion by 2031, expanding from USD 13.22 billion in 2026 at a 14.69% CAGR.

Which deployment model is set to grow the quickest over the next five years?

Edge data centers, supported by 5G MEC rollouts and low-latency demands, are projected to post a 20.3% CAGR.

Why are inference GPUs overtaking training GPUs in purchase volume?

Enterprises are shifting from model building to large-scale deployment, and inference cards cost 30-40% less because they bypass CoWoS and HBM bottlenecks.

How are voucher programs influencing GPU demand?

Subsidies covering up to 30-50% of compute costs lower effective prices, accelerating domestic GPU adoption, especially for inference workloads.

Page last updated on: