Southeast Asia Credit And Risk Management Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

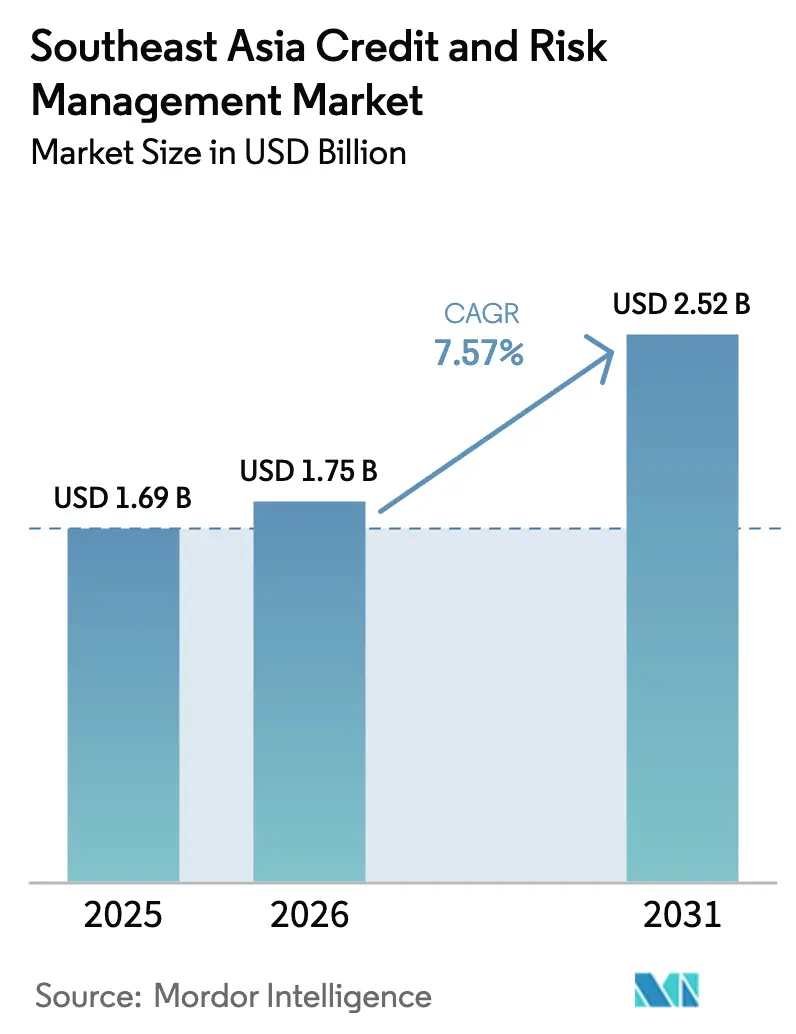

| Base Year Market Size (2025) | USD 1.69 Billion |

| Market Size (2026) | USD 1.75 Billion |

| Market Size (2031) | USD 2.52 Billion |

| Growth Rate (2026 - 2031) | 7.57% CAGR |

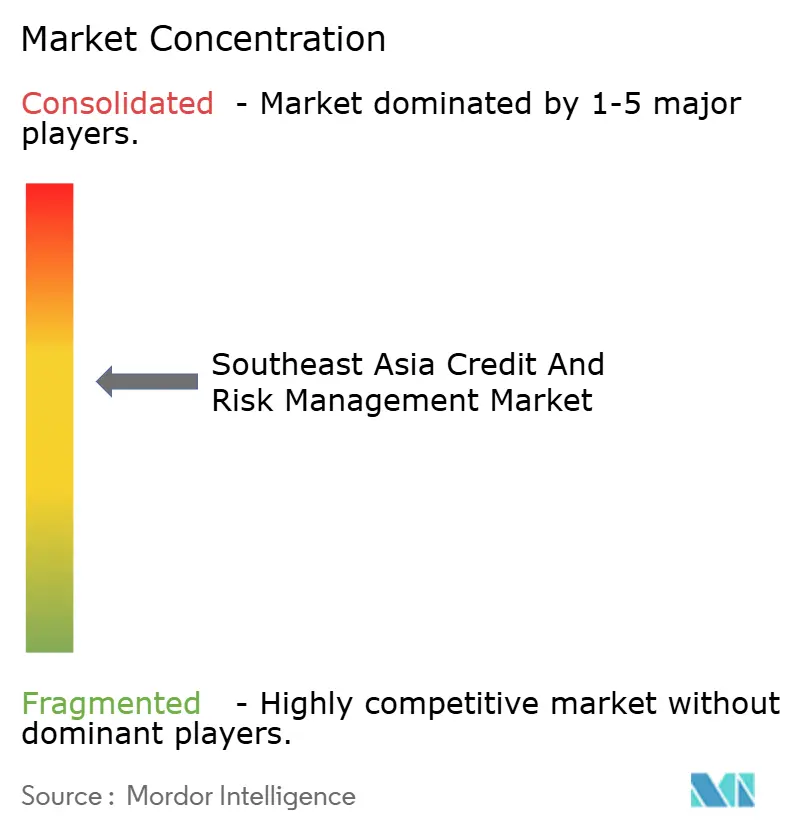

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Southeast Asia Credit And Risk Management Market Analysis by Mordor Intelligence

The Southeast Asia risk analytics market size is expected to grow from USD 1.69 billion in 2025 to USD 1.75 billion in 2026 and is projected to reach USD 2.52 billion by 2031, registering a 7.57% CAGR over the forecast period. This growth pace reflects how banks, fintechs, and non-bank lenders recalibrate credit decisioning processes while regulators demand real-time portfolio visibility. Credit digitalization, the rollout of cloud availability zones in Indonesia and Malaysia, and intensified scrutiny of non-performing loans are converging to accelerate platform spending. Vendors able to harmonize model explainability with alternative-data ingestion stand to capture an expanding share as thin-file borrowers enter formal finance and supervisory reporting windows shorten. At the same time, cloud deployment economics, managed-service contracts, and rising operational-risk exposures are reshaping competitive positioning across the market.

Key Report Takeaways

- By deployment mode, cloud solutions secured 60.22% of the Southeast Asia credit and risk management market share in 2025, and they are advancing at an 8.93% CAGR through 2031.

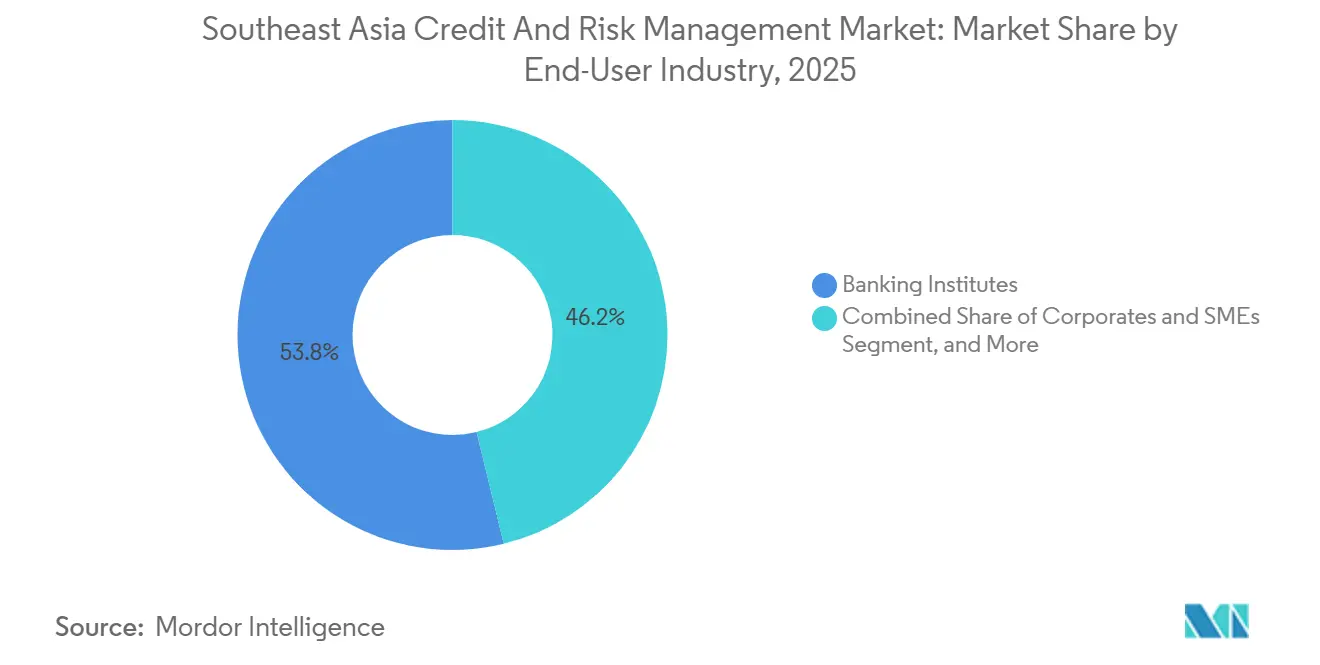

- By end-user industry, banking institutions accounted for 53.84% of the Southeast Asia credit and risk management market in 2025, while fintech and digital lending platforms are expanding at a 9.33% CAGR between 2026 and 2031.

- By component, software platforms captured 66.43% of the Southeast Asia credit and risk management market in 2025; managed services posted the strongest outlook, with a 7.98% CAGR to 2031.

- By risk type, credit risk led with 56.92% of the Southeast Asia credit and risk management market share in 2025, yet operational-risk modules are growing at a 7.82% CAGR across the forecast horizon.

- By country, Indonesia maintained 28.73% of regional revenue in 2025, and Vietnam is set to record the fastest growth at an 8.03% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Southeast Asia Credit And Risk Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Purchasing Power Fuelling Consumer Credit Demand | +1.8% | Indonesia, Vietnam, Philippines with spillover to Thailand | Medium term (2-4 years) |

| BFSIs' Imperative to Diminish Non-Performing Loans (NPLs) | +2.1% | Indonesia, Thailand, Malaysia, Vietnam | Short term (≤ 2 years) |

| Regulatory Mandates | +1.5% | Singapore, Indonesia, Thailand, Malaysia, Philippines | Short term (≤ 2 years) |

| Open-Banking APIs Unlocking Alternative Data Scoring | +1.2% | Singapore, Thailand with gradual adoption in Indonesia, Vietnam | Medium term (2-4 years) |

| Digital-Lending Surge Among Micro-SMEs | +0.9% | Indonesia, Vietnam, Philippines | Long term (≥ 4 years) |

| Peer-to-Peer Platforms' Need for Advanced Risk Analytics | +0.7% | Indonesia, Singapore, Thailand | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Purchasing Power Fuelling Consumer Credit Demand

Household credit penetration across ASEAN-6 economies climbed from 68% of GDP in 2020 to 74% in 2025, pushing lenders to widen underwriting lenses beyond bureau data that cover just 40% of Indonesia’s adult population and 30% of Vietnam’s. Motorcycle finance and point-of-sale installments drove Indonesia’s 12% retail-loan expansion, while digital wallets with embedded lending boosted Vietnam’s unsecured personal-loan book by 18%. Alternative-data signals drawn from utility payments, e-commerce receipts, and mobile-airtime top-ups allow underwriters to score first-time borrowers more accurately, a priority as the unbanked cohort across ASEAN fell to 210 million in 2025 from 290 million in 2020. Vendors embedding psychometric testing and smartphone metadata analytics into decision engines, therefore, gain early-mover advantages, provided they meet upcoming AI-governance disclosure norms.

BFSIs’ Imperative to Diminish Non-Performing Loans (NPLs)

Regional NPL ratios settled at 3.2% in 2025 compared with a 2.1% pre-pandemic baseline, with Indonesia at 3.8%, Thailand at 3.5%, and Vietnam at 2.9%. Higher default levels erode net interest margins because every 100-basis-point rise in NPLs lifts credit costs by roughly 15-20 basis points. Indonesia’s Financial Services Authority enforced Circular POJK 48/2024, which obliges banks with assets above IDR 10 trillion to implement automated daily distress-signal models, a rule that accelerated platform rollouts during 2025. Institutions that identify at-risk exposures 90-120 days in advance can restructure loans proactively, protecting asset quality and customer relationships and thereby strengthening competitive resilience.

Regulatory Mandates

Regional supervisors tightened oversight in 2024-2025. Singapore’s Monetary Authority refreshed Technology Risk Management Guidelines that now require annual penetration tests and board-level accountability for model risk. Malaysia’s Bank Negara issued a Climate Risk Management and Scenario Analysis framework obliging banks to overlay physical and transition-risk scenarios onto loan books. Cumulatively, compliance now absorbs about one-third of large-bank risk-analytics budgets, up from one-fifth in 2020, incentivizing demand for software that arrives with pre-built supervisory templates and audit trails. Vendors offering country-specific reporting packs lower time-to-compliance for clients and therefore claim premium pricing.

Open-Banking APIs Unlocking Alternative Data Scoring

Thailand went live with its open-banking API ecosystem in early 2024 and Singapore expanded SGFinDex to cover insurance and investment accounts by mid-2025, enabling lenders to pull real-time cash-flow data with customer consent. A Bank for International Settlements study found that incorporating such data cut default rates by up to 22% among thin-file borrowers in pilot programs.[2]Bank for International Settlements, “Open Banking and Alternative Credit Scoring: Evidence from Southeast Asia,” bis.org Adoption lags in Indonesia and Vietnam, where full frameworks will only materialize after 2027; nevertheless, early movers accumulate feedback loops that sharpen model accuracy and amplify user acquisition. Vendors must also solve consent-management workflows and observe data-residency statutes that diverge sharply across member states.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Implementation and Integration Complexity with Legacy Cores | -0.9% | Indonesia, Thailand, Malaysia, Philippines | Short term (≤ 2 years) |

| Heightened Data-Privacy / Cyber-Security Compliance Costs | -0.7% | Singapore, Indonesia, Thailand, Malaysia, Vietnam | Medium term (2-4 years) |

| Thin-File Borrower Data Scarcity | -0.5% | Vietnam, Philippines, Cambodia, Indonesia | Long term (≥ 4 years) |

| Shortage of Skilled Risk-Analytics Professionals | -0.4% | Vietnam, Philippines, Indonesia, Thailand | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Implementation and Integration Complexity with Legacy Cores

Tier-1 and tier-2 banks across the region still run 15-year-old core-banking systems on mainframes, making data-pipeline engineering and parallel-run testing both lengthy and costly. Integration budgets often exceed USD 3 million for mid-sized lenders, and compressed regulatory timelines can force tactical workarounds that undercut analytics ambitions. Vendors featuring low-code integration kits and certified connectors to popular cores cut lead times, yet they must update continuously as legacy providers patch software.

Heightened Data-Privacy and Cyber-Security Compliance Costs

Thailand’s Personal Data Protection Act, Indonesia’s Personal Data Protection Law, and Vietnam’s Decree 13/2023 all reached enforcement in 2024-2025, mandating encryption-at-rest, role-based access controls, and breach notifications. These safeguards add about 20% to software license costs and require ongoing security audits. Phishing attacks targeting bank employees rose 34% in 2025, according to the Monetary Authority of Singapore, pushing institutions to demand ISO 27001 certifications from solution vendors. Compliance overhead therefore narrows the budgets available for other innovation and slows purchasing cycles.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Mode: Cloud Gains Momentum on Scalability

Cloud implementations captured 60.22% of the Southeast Asia credit and risk management market share in 2025, and their 8.93% CAGR through 2031 reflects demand for elastic compute to run stress scenarios. OJK’s clarification that public-cloud workloads are permissible if data stay onshore unlocked delayed migrations in Indonesia. Local availability zones launched by Amazon Web Services and Microsoft Azure in 2025 reduced latency, further lifting appetite. On-premise architectures persist at institutions that prioritize sovereign-data control, especially in Vietnam, yet even these banks are adopting hybrid stacks that keep personally identifiable information on-premise while shifting model training to cloud GPU clusters. Consumption pricing tied to API calls lowers up-front capex for smaller lenders, but it can create budget volatility when transaction volumes spike, persuading procurement teams to renegotiate capacity tiers annually.

The Southeast Asia credit and risk management market for cloud deployments is projected to reach USD 1.62 billion by 2031, accounting for 64% of total spending. Competitive differentiation hinges on cloud-agnostic containers that run identically across AWS, Azure, and regional providers. Vendors optimized for a single hyperscaler achieve faster performance but face client-concentration risk, whereas multi-cloud platforms must master orchestration and policy harmonization.

By Component: Managed Services Surge as Talent Gaps Widen

Software platforms accounted for 66.43% of revenue in 2025, but managed-service contracts will post the fastest 7.98% CAGR. Mid-tier banks in Indonesia and the Philippines routinely outsource model validation, Basel III capital calculations, and stress-scenario design because domestic data-science pipelines remain shallow. Managed-service providers embed domain experts who handle monthly performance monitoring and regulator-facing reports, creating sticky revenue and deep client lock-in. The market for managed services is anticipated to exceed USD 650 million by 2031.

Advisory and implementation services stay material, yet they generate one-off revenue. Vendors, therefore, seek annuity streams through multi-year operating contracts. Supervisors warn boards not to abdicate oversight, prompting the inclusion of explicit monitoring clauses in service-level agreements. Providers that can assemble multilingual teams in Jakarta, Bangkok, Ho Chi Minh City, and Manila enjoy a proximity advantage, as institutions prioritize documentation of local-language models.

By End-User Industry: Fintech Platforms Accelerate Adoption

Banks held 53.84% of 2025 revenue, but fintech and digital lenders will record a 9.33% CAGR as peer-to-peer operators and buy-now-pay-later schemes comply with tougher conduct codes. Indonesia required automated scoring and daily portfolio reporting for all licensed P2P lenders starting 2025, spurring a rapid procurement cycle. Fintech entrants favor API-first modules that deliver sub-second credit decisions at e-commerce checkout, driving volume spikes that reward platforms architected for horizontal scale.

Non-bank financial institutions, such as leasing and microfinance companies, represent a mid-growth cohort seeking modular scorecards to upgrade paper-based workflows. Corporates and SMEs primarily adopt risk analytics for treasury operations and supply chain finance. The convergence of embedded finance pulls non-financial firms into the regulatory perimeter, expanding addressable demand and cementing the market as foundational infrastructure for Southeast Asian credit ecosystems.

By Risk Type: Operational Risk Gains Prominence

Credit risk modules accounted for 56.92% of 2025 revenue, yet operational risk spending will grow faster at a 7.82% CAGR as cyber incidents and technology outages escalate. Thailand’s largest bank suffered a 14-hour core-system failure in 2024 that froze transactions and triggered fines, elevating board-level focus on operational resilience. New Basel standards link operational-risk capital directly to historical loss databases, prompting banks to invest in enhanced loss-event capture and scenario analysis.

Integrated platforms that model credit, liquidity, and operational threats in a unified framework win share among larger institutions, while mid-tier banks still favor point solutions, leading to data silos. Inter-risk contagion - for example, a cyber breach that triggers liquidity strain - underscores the need for connected analytics, an area where market penetration remains low but strategically important.

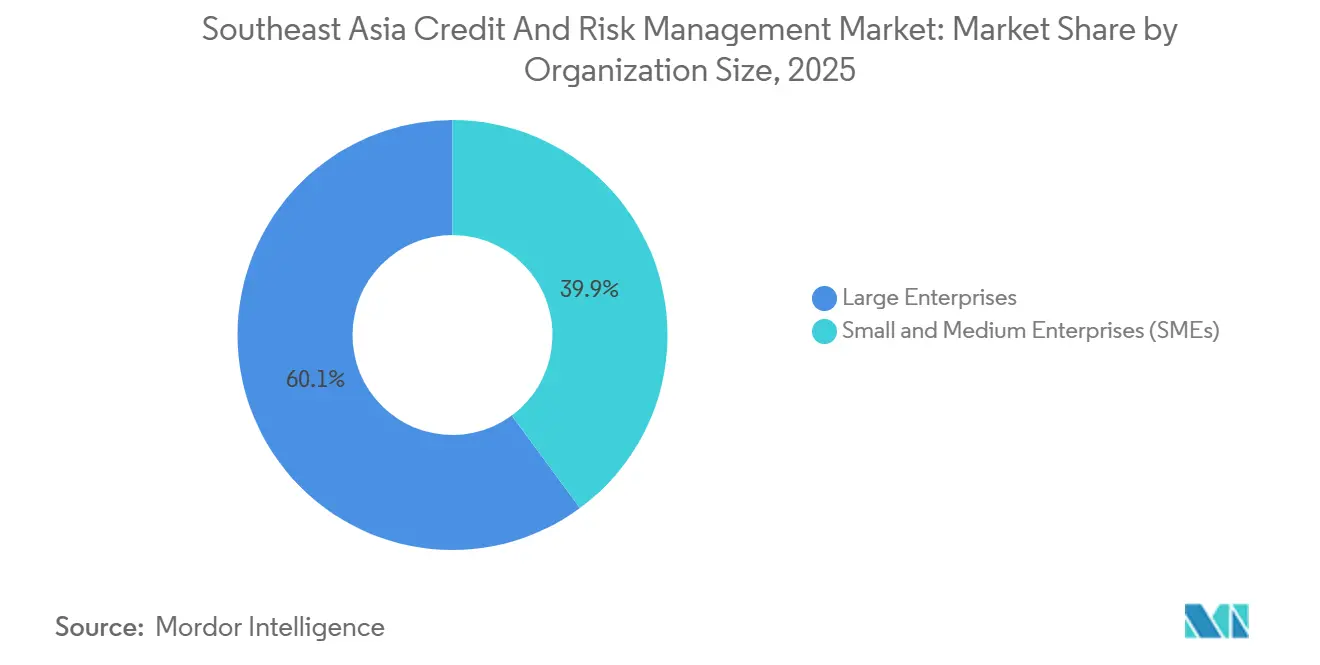

By Organization Size: SMEs Embrace Affordable Solutions

Large enterprises accounted for 60.11% of spending in 2025, but small and medium lenders will grow at a 8.31% CAGR as subscription pricing lowers entry barriers. Indonesia’s mandates apply to rural banks with assets under USD 500 million, forcing them to roll out platforms for the first time. Basic scorecards priced at USD 10,000-20,000 per year have gained traction because they ship with pre-trained models and browser-based dashboards that require no dedicated data-science teams.

Vendors run dual go-to-market motions: online trials and reseller channels target SMEs, while direct enterprise sales teams court tier-1 banks that demand bespoke integration and service-level guarantees. The Southeast Asia credit and risk management market size among SMEs is set to more than double by 2031, yet customer success hinges on up-front training and local language support because staff turnover rates at small lenders are high.

Geography Analysis

Indonesia contributed 28.73% of regional revenue in 2025, reflecting its 110 commercial banks, 1,600 rural banks, and more than 100 licensed fintech lenders.[3]Asian Development Bank, “ASEAN Financial Integration Report 2025,” adb.org OJK’s series of circulars on credit, operational, and technology risk created predictable, if stringent, compliance roadmaps that sustain platform demand. Cloud availability zones established in 2025 resolved prior sovereignty concerns, and large banks have begun experimenting with graph analytics to expose related-party lending. Price sensitivity remains a hurdle, pushing local vendors that offer rupiah contracts and in-country support to the front of competitive bids.

Vietnam, with an 8.03% forecast CAGR, is the fastest-expanding slice of the Southeast Asia credit and risk management market. State-owned giants such as Vietcombank and BIDV are onboarding enterprise platforms in response to Circular 39/2024, which phases out collateral-only credit decisions by 2027. Consumer-credit-to-GDP at 18% in 2025 signals headroom for loan growth, yet bureau coverage reaches only 30% of adults, so lenders rely on alternative-data scores that platforms must ingest natively. Data-localization rules compel onshore hosting, favoring cloud providers investing in domestic sites.

Singapore, Malaysia, Thailand, and the Philippines form a mature middle tier. Singapore’s Monetary Authority sets regulatory benchmarks that ripple through ASEAN, making its market a proving ground for vendors. Malaysia’s consolidated banking sector pursues incremental platform extensions rather than greenfield replacements, whereas Thailand’s elevated NPLs motivate stress-testing spend. The Philippines continues to reduce its unbanked population, but patchy connectivity outside Metro Manila slows cloud uptake. Frontier markets such as Cambodia and Laos remain small today, but rising digital-lending penetration hints at latent demand once supervisory capacity strengthens.

Competitive Landscape

Global software majors - SAS Institute, IBM, Oracle, and SAP - hold about 40-45% combined share across tier-1 banks through wide product portfolios and legacy contracts. Yet regional system integrators and cloud-native specialists are winning deals among fintechs and mid-tier banks by packaging country-specific compliance templates and agile APIs. Companies like Integro Technologies and RiskEdge Solutions localize faster and price flexibly, while Provenir and Finastra compete on low-code configuration and consumption billing. Data-localization statutes create barriers for entrants without onshore hosting, leading to winner-take-all dynamics in smaller economies.

White-space opportunities cluster around climate-risk stress testing, ESG scoring, and embedded-finance underwriting, where few vendors currently provide turnkey solutions. Enterprises that balance standard SaaS economics with deep localization- language packs, regulatory reporting libraries, and domestic support centers- will outpace rivals. Vendor selection increasingly weighs cyber-security posture and ISO certifications because supervisors hold boards accountable for third-party exposures. As managed-service contracts scale, providers that deliver outcome guarantees rather than just platform licenses are positioned to command premium margins.

Southeast Asia Credit And Risk Management Industry Leaders

SAS Institute Inc.

IBM Corporation

Oracle Corporation

SAP SE

Experian Information Solutions Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Oracle Corporation signed a USD 15 million multi-year deal with Bank Mandiri to deploy OFSAA across credit, market, and operational-risk units, reinforcing its foothold among Indonesia’s tier-1 banks.

- November 2025: SAP SE introduced SAP Risk Management for Banking, a cloud-native module within SAP S/4HANA, with first rollouts in Thailand and Malaysia and wider ASEAN launch planned for 2026.

- October 2025: Moody’s Analytics purchased a minority stake in a Singapore regtech specializing in climate-risk analytics to integrate transition-risk modeling into its RiskCalc and CreditEdge suites.

- September 2025: FICO partnered with Vietcombank to implement Origination Manager and Debt Manager platforms, enabling real-time loan decisioning and automated collections that will go live in 2026.

- August 2025: IBM formed a joint venture with a Malaysian integrator to deliver subscription-based risk analytics-as-a-service to mid-sized banks and non-bank lenders across the region.

Southeast Asia Credit And Risk Management Market Report Scope

The Southeast Asia Credit and Risk Management Market Report is Segmented by Deployment Mode (Cloud, On-premise), Component (Software, Services), End-User Industry (Banking, NBFIs, FinTech, Corporates), Risk Type (Credit, Market, Operational, Liquidity), Organization Size (Large, SMEs), and Geography (Indonesia, Singapore, Malaysia, Thailand, Philippines, Vietnam, Others). The Market Forecasts are in Value (USD).

| Cloud |

| On-premise |

| Software Platform | |

| Services | Advisory and Implementation |

| Managed Services |

| Banking Institutes |

| Non-Bank Financial Institutions |

| FinTech and Digital Lending Platforms |

| Corporates and SMEs |

| Credit Risk |

| Market Risk |

| Operational Risk |

| Liquidity Risk |

| Large Enterprises |

| Small and Medium Enterprises (SMEs) |

| Indonesia |

| Singapore |

| Malaysia |

| Thailand |

| Philippines |

| Vietnam |

| Cambodia |

| Other Southeast Countries |

| By Deployment Mode | Cloud | |

| On-premise | ||

| By Component | Software Platform | |

| Services | Advisory and Implementation | |

| Managed Services | ||

| By End-User Industry | Banking Institutes | |

| Non-Bank Financial Institutions | ||

| FinTech and Digital Lending Platforms | ||

| Corporates and SMEs | ||

| By Risk Type | Credit Risk | |

| Market Risk | ||

| Operational Risk | ||

| Liquidity Risk | ||

| By Organization Size | Large Enterprises | |

| Small and Medium Enterprises (SMEs) | ||

| By Country | Indonesia | |

| Singapore | ||

| Malaysia | ||

| Thailand | ||

| Philippines | ||

| Vietnam | ||

| Cambodia | ||

| Other Southeast Countries | ||

Key Questions Answered in the Report

How large is the Southeast Asia Credit and Risk Management market in 2026?

The Southeast Asia Credit and Risk Management market size stands at USD 1.75 billion in 2026 and is forecast to grow at a 7.57% CAGR to 2031.

Which deployment model is winning client preference?

Cloud implementations hold 60.22% of 2025 revenue and will widen their lead as regulatory clarity and local data centers reduce sovereignty risk.

Why is Vietnam considered the fastest-growing geography?

Vietnam’s 8.03% CAGR stems from regulatory reforms that shift banks toward risk-based lending while consumer-credit penetration rises from a lower base.

What is driving demand for managed services?

Scarcity of in-house data-science talent and the need for continual model calibration push banks and fintechs to outsource risk analytics under multi-year contracts.

Which risk type is gaining prominence beyond credit?

Operational-risk modules are expanding at 7.82% CAGR due to increased cyber attacks, technology outages, and stricter Basel capital rules.

Page last updated on: