Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

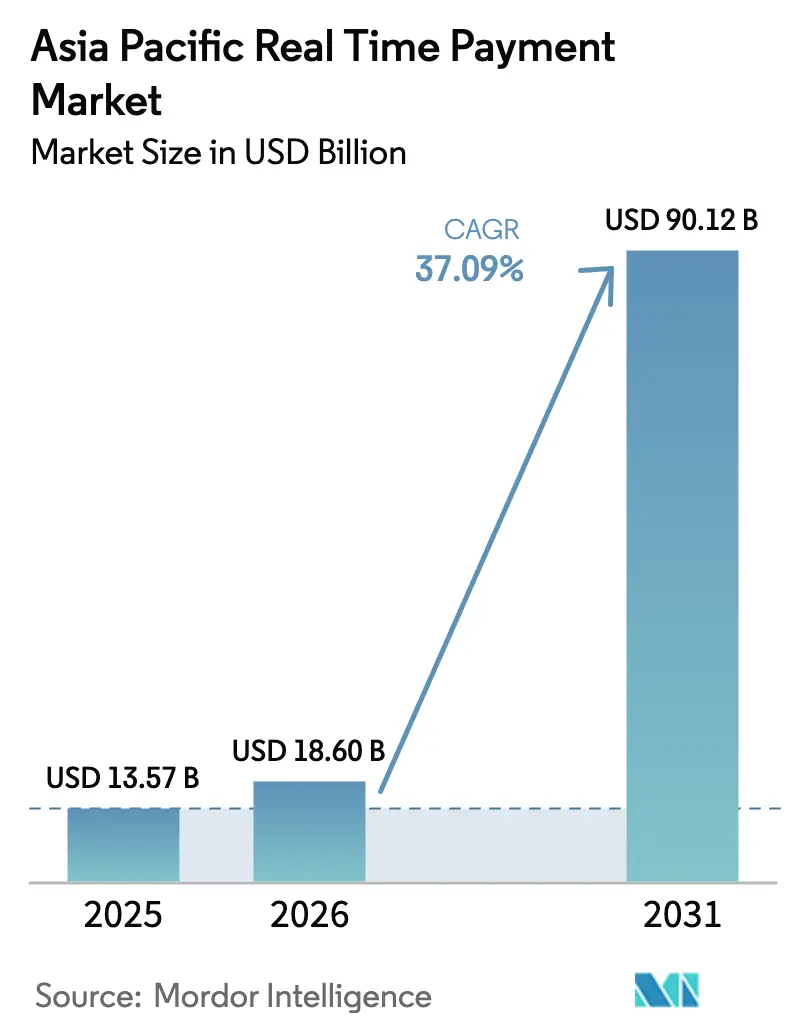

| Base Year Market Size (2025) | USD 13.57 Billion |

| Market Size (2026) | USD 18.60 Billion |

| Market Size (2031) | USD 90.12 Billion |

| Growth Rate (2026 - 2031) | 37.09% CAGR |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia Pacific Real Time Payment Market Analysis by Mordor Intelligence

The Asia Pacific real time payment market size is expected to grow from USD 13.57 billion in 2025 to USD 18.6 billion in 2026 and is forecast to reach USD 90.12 billion by 2031 at 37.09% CAGR over 2026-2031. Robust transaction growth-185.8 billion real-time transfers processed in 2023-confirms that the region has become the global epicenter of instant-payment innovation.[1]IR Team, “Global RTP Volumes 2023,” ir.com Expansion is catalyzed by public-sector infrastructure programs, widespread smartphone adoption, and the proliferation of QR-code standards that make account-to-account payments intuitive for consumers and cost-effective for merchants. Government incentives that remove merchant-discount fees, the rollout of ISO 20022 messaging, and the rise of cross-border corridors such as ASEAN Regional Payment Connectivity are accelerating commercial uptake, especially among small businesses and e-commerce sellers. Competitive dynamics vary by country: China maintains scale leadership through Alipay and WeChat Pay, whereas India’s open UPI architecture sustains multi-provider competition and delivers the fastest volume growth.

Key Report Takeaways

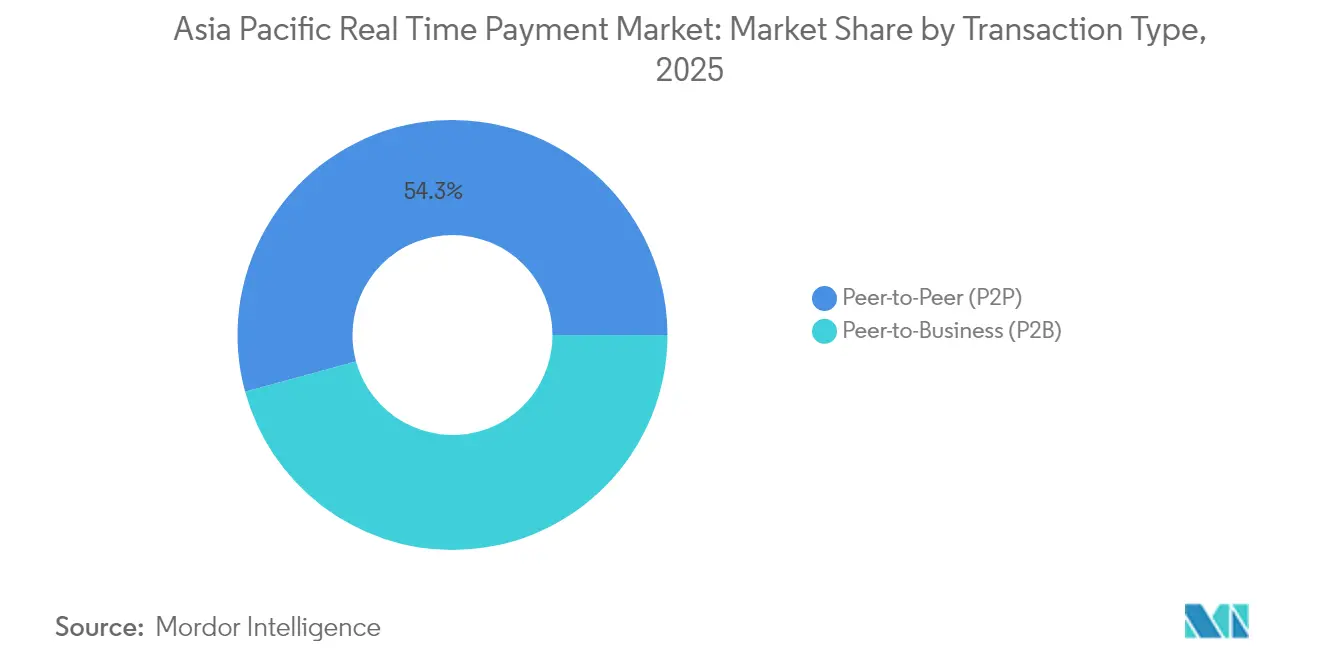

- By transaction type, peer-to‐business transactions posted the quickest expansion at a 44.32% CAGR between 2026-2031 while peer-to-peer transfers held 54.25% of the Asia Pacific real time payment market share in 2025.

- By component, platforms and solutions commanded 67.15% revenue in 2025, whereas services are forecast to grow at 41.05% CAGR on mounting demand for API integration and fraud-mitigation consulting.

- By deployment mode, cloud installations captured 59.45% of the Asia Pacific real time payment market size in 2025 and are expected to register 40.7% CAGR through 2031.

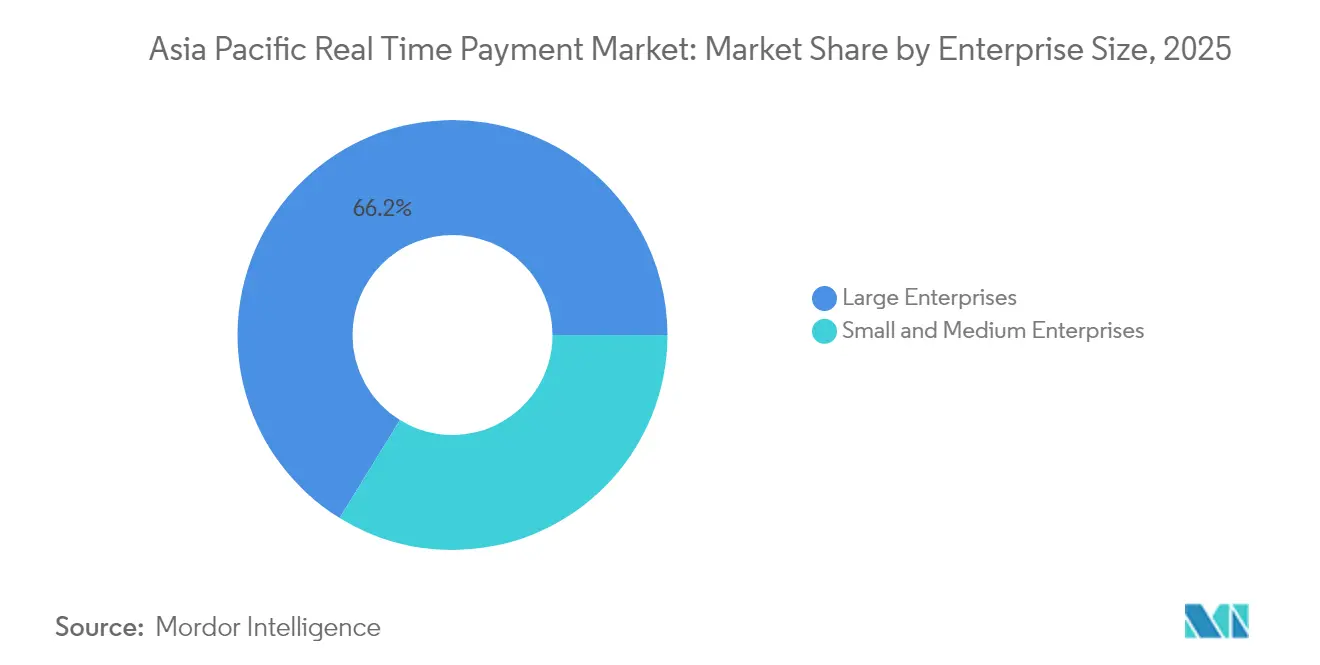

- By enterprise size, small and medium enterprises are projected to expand at 42.95% CAGR, outpacing the large-enterprise segment while still accounting for a smaller revenue base.

- By end-user industry, retail and e-commerce is advancing at the highest 39.95% CAGR, while banking, financial services, and insurance retained 37.40% of 2025 revenue.

- By geography, China contributed 40.65% of 2025 revenue and India is growing at 41.62% CAGR, the strongest pace among major economies.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Asia Pacific Real Time Payment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated Adoption of National Instant-Payment Rails in Developing APAC Economies | +12.5% | India, Indonesia, Philippines, Thailand, Malaysia | Medium term (2-4 years) |

| Mobile-First Consumer Base Enabling QR-Code and App-Based RTP Ecosystems | +8.7% | China, India, Southeast Asia core markets | Short term (≤ 2 years) |

| Government-Led Cashless Initiatives such as India's Digital Public Infrastructure | +7.2% | India, China, Singapore, Thailand | Long term (≥ 4 years) |

| Cross-Border RTP Corridors Driving Merchant Acceptance in E-commerce | +5.1% | ASEAN+3, Australia-New Zealand corridor | Medium term (2-4 years) |

| API-Driven Open-Banking Frameworks Lowering Integration Barriers for RTP | +3.8% | Singapore, Australia, Hong Kong, Japan | Short term (≤ 2 years) |

| Rising Demand from Gig-Economy and Salary-On-Demand Platforms | +2.1% | Urban centers across APAC, particularly China and India | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Accelerated Adoption of National Instant-Payment Rails in Developing APAC Economies

National instant-payment schemes are transforming financial inclusion across emerging Asia. Indonesia’s BI-FAST, the Philippines’ InstaPay, and Malaysia’s RTP platform illustrate how central banks use 24/7 rails to bypass correspondent networks, shrink settlement from days to seconds, and stimulate GDP through improved cash-flow velocity.[2]The Banker Editorial Board, “National Instant Rails in Emerging Asia,” thebanker.com Thailand’s PromptPay now accounts for 43.2% of domestic payments, demonstrating that low-cost merchant onboarding can unlock mass acceptance. Pakistan’s Raast projects 63.5 million new banked citizens by 2028, reinforcing the link between real-time rails and social-equity outcomes. Across India, Brazil, China, Thailand, and Mexico, instant payments lifted USD 99.6 billion in incremental GDP during 2023, validating the macroeconomic multiplier that accompanies real-time settlement. [3]ACI Worldwide, “Prime Time for Real-Time 2024 Report,” aciworldwide.com

Mobile-First Consumer Base Enabling QR-Code and App-Based RTP Ecosystems

Smartphones are ubiquitous and affordable across Asia, and standard QR specifications make them powerful payment instruments. In China, mobile wallets expanded from 3.5% share in 2011 to 83% in 2018, giving app-based payments near-universal consumer reach. Indonesia’s QRIS framework harmonizes previously fragmented codes, enabling over 26 million merchants to accept domestic and cross-border QR payments on low-cost handsets. Surveys reveal that 72% of Southeast Asian consumers attempted cashless payments in 2023, with 79% using mobile wallets; cross-border QR interoperability, such as the Cambodia–Japan Bakong-JPQR link, further reduces remittance costs by 80% while shrinking settlement times to 10 seconds.

Government-Led Cashless Initiatives

Fiscal and regulatory interventions have accelerated digital adoption. India’s USD 180 million incentive pool for FY 2024-25 reimburses merchants for low-value UPI transactions, eliminating MDR fees and sustaining volume in the long tail of micro-retail. Japan’s cashless ratio touched 39.3% in 2023, nearing the 40% milestone the Cabinet set for June 2025. China’s digital yuan pilot-with 1.8 billion wallets and programmable money features-expands use cases such as prepayment escrow and smart-contract-linked subsidies, aligning monetary policy with digital-economy targets. Singapore’s Payment Services Act delivers regulatory clarity that attracts fintech-driven unattended payment models, including EV-charging micro-kiosks and automated dining installations.

Cross-Border RTP Corridors Driving Merchant Acceptance in E-Commerce

Region-wide settlement corridors are dismantling the cost and latency barriers that once constrained small exporters. The ASEAN Regional Payment Connectivity framework links Indonesia, Malaysia, the Philippines, Singapore, and Thailand, covering trade flows equal to 38% of global commerce when fully operational. The live PayNow-PromptPay bridge already allows Singaporean and Thai consumers to send money in real time using only a mobile number proxy, cutting fees by up to 70% compared with SWIFT-based transfers. India’s UPI became the first non-ASEAN system invited to Project Nexus, positioning domestic wallets to reach new customers in four Southeast Asian markets.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Fraud and Scam Incidence in Instant-Payment Channels Hinders the Market | -6.8% | India, Australia, China, developed APAC markets | Short term (≤ 2 years) |

| Fragmented Regulatory Standards Across APAC Jurisdictions | -4.2% | ASEAN, broader APAC cross-border corridors | Medium term (2-4 years) |

| Legacy Core Banking Systems Limiting Real-Time Settlement by Tier-2 Banks | -3.1% | Indonesia, Philippines, Thailand, smaller banks across APAC | Long term (≥ 4 years) |

| Capex Constraints Among SMEs for RTP API Integration | -2.4% | Rural and semi-urban areas, developing APAC economies | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Fragmented Regulatory Standards Across APAC Jurisdictions

Diverging data-localization mandates, AML rules, and ISO 20022 adoption schedules complicate cross-border connections. Providers often duplicate compliance teams country-by-country, pushing up operating costs and slowing time-to-market. Absence of harmonized technical standards leaves each scheme running unique message formats, creating one-off integration projects that inflate capital budgets. Patchy central-bank digital-currency frameworks add another compliance layer, particularly for fintechs that lack legal resources. Smaller merchants may be deterred altogether, reinforcing digital divides among ASEAN economies.

High Fraud and Scam Incidence in Instant-Payment Channels

The irrevocable nature of real-time transfers compresses the window for manual fraud checks. India recorded USD 1.32 billion in scam-driven losses during 2024, while authorized-push-payment fraud climbs at 8.7% CAGR in Australia. Institutions invest in AI detection engines that score transactions in milliseconds, but false-positive rates remain a cost concern. Criminal rings exploit cross-border corridors, leveraging uneven enforcement to launder funds before detection. Consumer confidence can falter in the wake of viral “digital-arrest” scams, pushing regulators toward mandatory reimbursement regimes that may reshape liability models for banks and wallets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Transaction Type: P2B Drives Commercial Transformation

Peer-to-peer transfers held 54.25% revenue in 2025, reflecting the consumer origins of the Asia Pacific real time payment market. Yet the peer-to-business segment shows superior momentum, growing 44.32% CAGR to 2031 as merchants embrace instant settlement to unlock working capital. Corporates in China alone could free USD 421 billion by optimizing payment timing, while 71% of Southeast Asian SMBs link digital payments to sales increases.

The P2B surge also rides government digitization of procurement and tax receipts, illustrated by India’s Bharat Bill Payment System registering 60% yearly value growth. Retailers showcase tangible benefits: Reliance Retail achieved 19.4% revenue growth with 40% digital payments; D-Mart lifted profitability as UPI captured a quarter of sales. Cross-border B2B instant transfers are forecast to reach 42% of USD 16 trillion in enterprise payments by 2028, signifying growing reliance on open-loop account-to-account rails that bypass card fees.

By Component: Services Accelerate Through Integration Complexity

Platforms and solutions controlled 67.15% of 2025 spend, yet professional services now expand at 41.05% CAGR, reflecting the technical and regulatory complexity of modern instant-payment ecosystems. Cloud migrations, ISO 20022 upgrades, and API security assessments require specialized knowledge that banks often outsource. Malaysia’s PayNet relied on consulting partners to adapt core systems for DuitNow QR and regional QR interoperability within nine months, underscoring services demand.

Legacy modernization is another driver; 14% of financial institutions still depend on outdated mainframes that need gradual conversion to avoid disruption. Service integrators deploy façade APIs, message converters, and hybrid cloud designs to maintain uptime during cutovers. Consequently, advisory and managed-service revenue outpaces traditional license fees, anchoring a recurring-revenue layer inside the Asia Pacific real time payment market.

By Deployment Mode: Dominance Accelerates

Cloud captured 59.45% of the Asia Pacific real time payment market share in 2025, boosted by elasticity, global distribution, and pay-as-you-grow economics. Instant-payment peaks around shopping festivals like Singles’ Day and 12-12 sales strain on-premise estates; cloud bursting mitigates risk without excessive idle capacity. Banks migrating non-core payment modules report up to 40% opex savings across five years, even after factoring data-sovereignty safeguards.

Not all regulators allow unfettered public-cloud hosting, so hybrid models persist. Institutions in India and Indonesia often process transactions in-country while leveraging cloud analytics for fraud scoring. Conversely, Singapore, Australia, and Japan increasingly endorse cloud-first directives, accelerating SaaS adoption among smaller fintechs that lack data-center budgets. The deployment mix will continue tilting toward cloud as harmonized encryption and sovereign-cloud offerings satisfy compliance officers.

By Enterprise Size: SME Growth Outpaces Large Enterprises

Large enterprises still held 66.20% of 2025 value because of their scale and complex integration needs, but SMEs exhibit a 42.95% CAGR through 2031, narrowing the gap each year. With 90% of Asia-Pacific businesses classified as MSMEs yet facing USD 2.7 trillion in financing gaps, real-time payments become vital for liquidity and market access. Tokenization-driven fraud reduction and higher authorization rates delivered USD 7.9 billion in collective SME benefits between 2019-2024.

Cloud-native payment gateways package compliance, settlement, and reconciliation into subscription models priced for small merchants. Government support is equally pivotal: India’s zero-MDR policy sustains margin for micro-retailers, and Japan’s DX Connect Gate streamlines invoice-to-payment workflows for regional suppliers. As adoption costs fall, SMEs will command a larger portion of the Asia Pacific real time payment market size over the forecast horizon.

By End-User Industry: Retail Disrupts BFSI Leadership

Banking, financial services, and insurance provided 37.40% of revenue in 2025, reflecting their role as both network operators and early adopters. Yet retail and e-commerce, expanding at 39.95% CAGR, is poised to narrow that lead as instant checkout, embedded finance, and buy-now-pay-later options flourish. Mobile commerce is expected to represent 80% of Asia-Pacific e-commerce sales by 2028, and real-time settlement minimizes cart abandonment by reassuring consumers of immediate order confirmation.

Healthcare adoption grows through Insurtech platforms that settle claims in real time, improving patient experience and provider cash flow. Utilities and telecoms automate bill presentment with instant activation upon payment, shrinking collection lags. Public-sector agencies digitize tax, subsidy, and procurement flows, unlocking billions in cost savings. Collectively, these vertical expansions amplify addressable revenue for solution vendors across the Asia Pacific real time payment industry.

Geography Analysis

China retained 40.65% revenue in 2025 thanks to its entrenched digital-wallet culture and cross-border ambitions. Alipay and WeChat Pay penetrate nearly every consumer touchpoint, while the digital renminbi pilot added programmable functions reaching 7.3 trillion yuan in transactions across 26 regions. CIPS processed 8.2 million cross-border transactions worth 175.49 trillion yuan in 2024, a 42.6% jump that highlights growing global relevance.

India is the fastest riser with a 41.62% CAGR. UPI posted 18.3 billion transfers worth ₹24.77 lakh crore (USD 298 billion) in March 2025, proving the scalability of open APIs and multi-bank participation. International expansion into 27 countries positions UPI as a technology export, while the FY 2024-25 merchant incentive program keeps onboarding costs near zero for corner stores.

Japan, South Korea, Australia, Singapore, Indonesia, and the rest of Asia-Pacific form a diverse growth bloc. Japan’s cashless ratio nears 40% as unified QR initiatives bridge municipal tax payments. South Korea’s KB Pay integrates AI fraud screening, anticipating generative-AI chat services by 2026. Australia’s New Payments Platform cooperates with New Zealand on e-invoicing, and Indonesia’s QRIS standardization connects MSMEs to digital commerce quickly. Collectively, these markets assure a balanced opportunity mix across mature and emerging economies, advancing the Asia Pacific real time payment market.

Competitive Landscape

Global card networks, regional super-apps, domestic clearing houses, and fintech specialists compete in a moderately fragmented arena. Visa processed USD 16 trillion in 2024 payment volume, strengthening its real-time proposition through network-to-network links with PromptPay and PayNow. Mastercard’s Send and Click-to-Pay solutions position it for cross-border RTP, while PayPal’s Fastlane guest-checkout reduces friction for 450 million active users.

Chinese titans Ant Group and Tencent maintain a duopoly at home via Alipay and WeChat Pay, but are expanding regionally through joint QR-code standards and investment in logistics. India’s NPCI anchors an open ecosystem where PhonePe, Google Pay, and Paytm compete on loyalty programs and credit overlays. Australian Payments Plus merges eftpos, BPAY, and NPP to create scale efficiencies, demonstrating that government-backed utility models can co-exist with commercial networks.

Strategic differentiation centers on fraud analytics, ISO 20022 readiness, and API orchestration. Vendors allocate increasing R&D to AI models that flag mule activity within 100 milliseconds. White-space growth opportunities include SME cross-border invoices, instant wage disbursements, and government-to-citizen welfare payouts. Consequently, partnerships-such as Visa’s merchant-acceptance alliance with Grab or ACI Worldwide’s cloud tie-up with Microsoft Azure-are likely to proliferate as players pursue defensible niches inside the Asia Pacific real time payment market.

Asia Pacific Real Time Payment Industry Leaders

ACI Worldwide

FIS Global

Mastercard Inc.

PayPal Holdings Inc.

Fiserv Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: KB Kookmin Card upgraded KB Pay with AI fraud detection and plans generative-AI conversational finance by mid-2025, reinforcing its mobile-first growth strategy.

- May 2025: India’s UPI hit a fresh peak of 18.68 billion transfers worth ₹25.14 lakh crore (USD 303 billion), displaying resilience after a temporary outage and strengthening NPCI’s case for global partnerships Economic Times.

- April 2025: Cambodia and Japan signed a Bakong-JPQR agreement enabling bilateral QR payments, lowering remittance costs for migrant workers and SMEs Asian Banking & Finance.

- April 2025: Hiroshima Bank, TIS, and Japan ICS launched DX Connect Gate for SME invoice digitization, signaling banks’ shift toward value-added services in the enterprise payment stack Hiroshima Bank, TIS.

Asia Pacific Real Time Payment Market Report Scope

Real-time payments are instant or immediate payments and are defined by the Euro Retail Payments Board (ERPB) as electronic retail payment solutions that are available 24/7/365. Immediate payments enable businesses and consumers to make and receive payments in real-time, providing convenience, speed, and faster availability of funds.

Asia Pacific Real-Time Payment Market is segmented by Type (P2P, P2B) and by Country (China, India, Japan, South Korea, and the Rest of the Asia Pacific).

By Transaction Type

| Peer-to-Peer (P2P) |

| Peer-to-Business (P2B) |

By Component

| Platform / Solution |

| Services |

By Deployment Mode

| Cloud |

| On-Premise |

By Enterprise Size

| Large Enterprises |

| Small and Medium Enterprises |

By End-User Industry

| Retail and E-Commerce |

| BFSI |

| Utilities and Telecom |

| Healthcare |

| Government and Public Sector |

| Other End-user Industries |

By Country

| China |

| India |

| Japan |

| South Korea |

| Australia |

| Singapore |

| Indonesia |

| Rest of Asia-Pacific |

| By Transaction Type | Peer-to-Peer (P2P) |

| Peer-to-Business (P2B) | |

| By Component | Platform / Solution |

| Services | |

| By Deployment Mode | Cloud |

| On-Premise | |

| By Enterprise Size | Large Enterprises |

| Small and Medium Enterprises | |

| By End-User Industry | Retail and E-Commerce |

| BFSI | |

| Utilities and Telecom | |

| Healthcare | |

| Government and Public Sector | |

| Other End-user Industries | |

| By Country | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Singapore | |

| Indonesia | |

| Rest of Asia-Pacific |

Key Questions Answered in the Report

What is the current size of the Asia Pacific real time payment market?

The market is valued at USD 18.6 billion in 2026 and is forecast to reach USD 90.12 billion by 2031 at a 37.09% CAGR.

Which country is growing fastest within the region?

India shows the highest growth, advancing at a 41.62% CAGR, driven by UPI’s record transaction volumes.

Why are peer-to-business payments important?

P2B transactions improve merchant cash flow, cut card fees, and are expanding at a 44.32% CAGR—the fastest among transaction types.

How does cloud deployment influence cost?

Banks migrating payment workloads to cloud environments report up to 40% operating-expense savings over five years while ensuring elastic scalability for peak events.

What are the main challenges facing providers?

Key challenges include fragmented regulatory frameworks that increase compliance costs and rising fraud scams that demand continual investment in AI-based security.

Page last updated on: