Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2020 - 2024 |

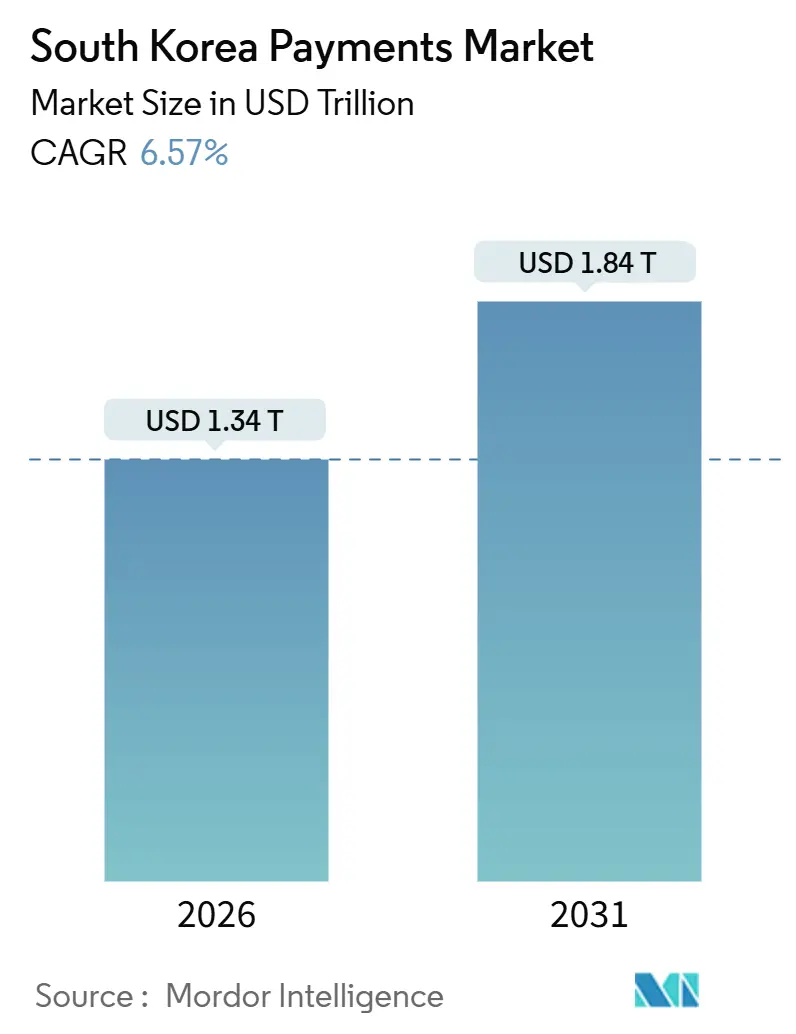

| Market Size (2026) | USD 1.34 Trillion |

| Market Size (2031) | USD 1.84 Trillion |

| Growth Rate (2026 - 2031) | 6.57% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Korea Payments Market Analysis by Mordor Intelligence

The South Korea payments market size reached USD 1.34 trillion in 2026 and is projected to climb to USD 1.84 trillion by 2031, translating into a 6.57% CAGR over the forecast period. Structural momentum favors real-time account-to-account rails, mobile wallets, and tokenized settlement networks that bypass legacy card infrastructure. Merchant take-up of QR codes, the 30 million-strong open-banking user base, and Samsung Wallet’s blockchain-backed digital identity credentials together reinforce a mobile-first consumer culture. Private-sector tokenization is also accelerating, as Naver’s planned won-pegged stablecoin ecosystem and Kakao’s parallel initiative highlight a shift away from sovereign digital-currency experiments. Meanwhile, elevated interchange fees, aging demographics in rural provinces, and high-profile deepfake fraud episodes temper the overall growth outlook for the South Korea payments market.

Key Report Takeaways

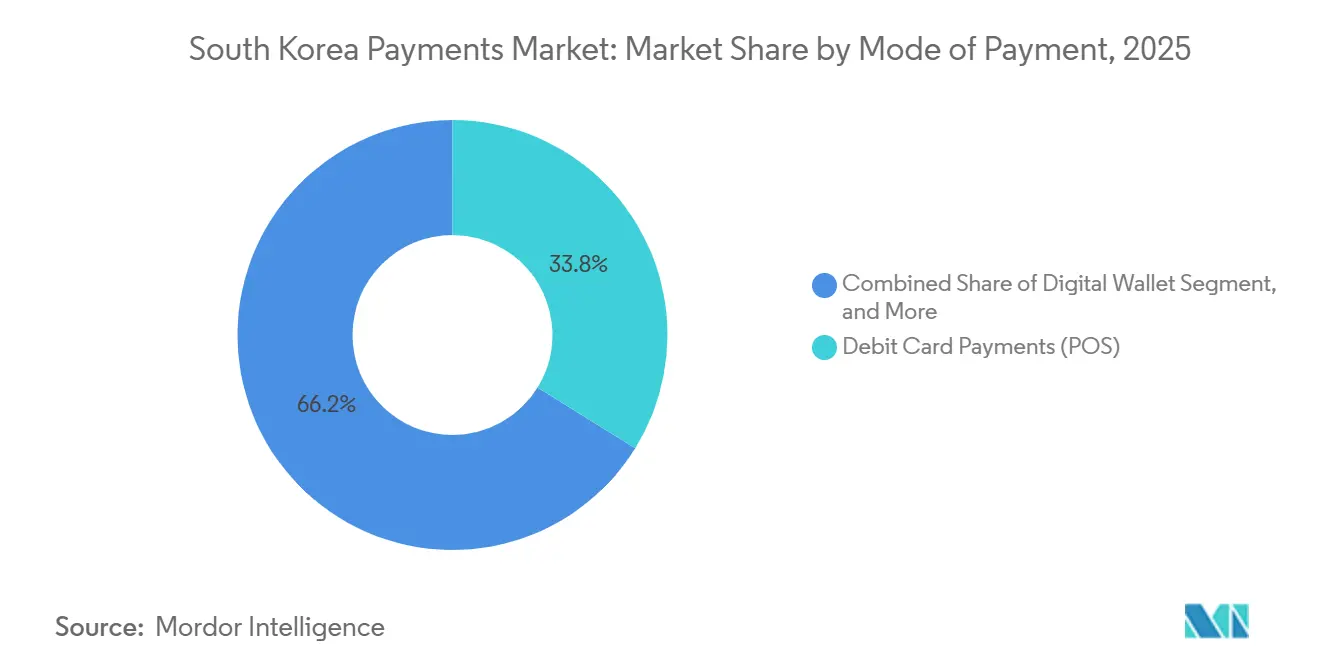

- By mode of payment, debit cards led with 33.82% of the South Korea payments market share in 2025. Digital wallets deployed online are forecast to expand at a 7.55% CAGR through 2031, the fastest pace among payment instruments.

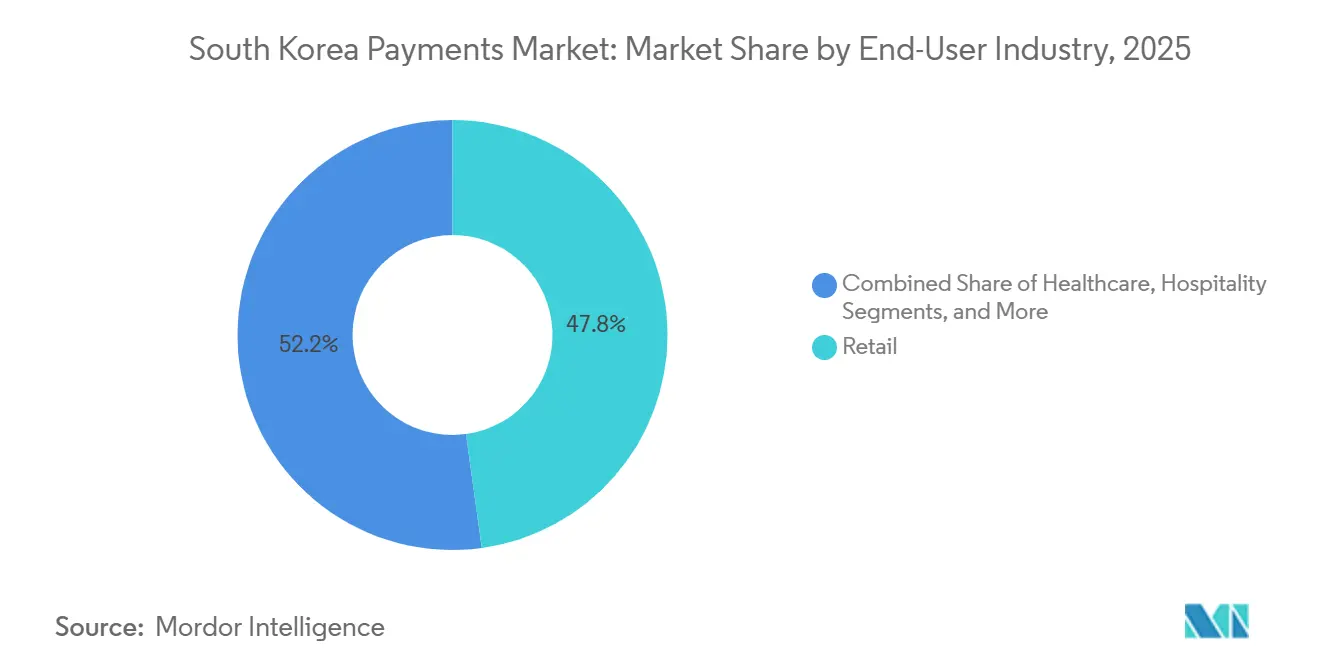

- By end-user industry, retail accounted for 47.83% of the South Korea payments market size in 2025. Healthcare payment volume is advancing at a 7.62% CAGR between 2026 and 2031, the quickest among major industries.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

South Korea Payments Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High proliferation of e-commerce and m-commerce | +1.8% | National, strongest in Seoul, Busan, Incheon | Short term (≤ 2 years) |

| Government digitization initiatives | +1.5% | Country-wide pilots in Seoul and Sejong | Medium term (2-4 years) |

| Growth of real-time payments and open banking | +1.2% | Urban centers nationwide | Medium term (2-4 years) |

| Rising adoption of mobile wallets and NFC | +1.0% | Led by Seoul Capital Area | Short term (≤ 2 years) |

| CBDC (Digital Won) pilot momentum | +0.6% | Wholesale pilots in major financial centers | Long term (≥ 4 years) |

| Blockchain-based corporate settlement | +0.4% | Early adoption in Seoul financial district | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Proliferation of E-Commerce And M-Commerce

Mobile commerce already generates 76-79% of Korean online-retail value, a level unmatched in most OECD economies.[1]Korea Communications Commission, “Mobile Commerce Penetration Reaches 76-79%,” kcc.go.kr Daily simple-payment turnover reached KRW 954.5 billion (USD 715 million) during 2025 as one-click checkout became standard across Naver Shopping, Coupang, and others.[2]Bank of Korea, “BOK Suspends Retail CBDC Pilot Project Hangang,” bok.or.kr Kakao Pay processed KRW 167.3 trillion (USD 125 billion) in 4Q 2024 alone because its wallet lives inside KakaoTalk, creating social-commerce switching costs that card networks cannot match. Government plans to interconnect public-service portals with private fintech APIs under the Digital Platform Government blueprint lower merchant onboarding friction. Together, these forces channel transaction growth toward real-time rails that underpin the South Korea payments market.

Government Digitization Initiatives

Thirty million Koreans used open-banking services by 2024, and the MyData 2.0 rollout in 2025 granted consumers holistic control over credit, insurance, and investment data.[3]Financial Services Commission, “Interchange Fee Caps and Open Banking Updates,” fsc.go.kr The Bank of Korea is phasing in an ISO 20022-compliant real-time gross-settlement platform that will finalize corporate transfers on central-bank money, eliminating interbank credit exposure. NH Nonghyup Bank and Hana Financial piloted cross-border ledger settlements on Partior’s blockchain in December 2025, shrinking remittance cycles from days to minutes. Blockchain-anchored digital IDs, live in Samsung Wallet since March 2025, add biometric security to card-not-present flows. Collectively, these moves upgrade the plumbing that propels the South Korea payments market toward higher real-time volume.

Growth of Real-Time Payments And Open Banking

Open-banking users equal roughly 58% of Korea’s adult population, yet they initiate just 2.3 account-to-account transfers monthly versus 6.1 card swipes. Planned instant-settlement functionality should tilt high-value B2B corridors toward bank rails that offer irrevocable finality. The nationwide QR-ATM service, launched in 2023, now lets any banking app withdraw cash from any ATM, eroding old network moats. Toss, Kakao Pay, and Naver Pay exploited open-banking APIs to move KRW 640.31 billion (USD 480 million) in foreign remittances during 2024, a 443% surge from 2022. This trajectory validates the real-time thesis that underpins long-run expansion of the South Korea payments market.

Rising Adoption of Mobile Wallets And NFC

Samsung Wallet counted 18.66 million users by 2025, moving KRW 88.6 trillion (USD 66 billion) annually, yet its magnetic-secure transmission keeps merchants from investing in NFC hardware. Apple Pay entered in 2023 but touches only KRW 2 trillion (USD 1.5 billion) a year because NFC terminals remain below 10% penetration. Terminal upgrades cost roughly KRW 200,000 (USD 150), a hurdle most merchants sidestep while Samsung Pay works on legacy equipment. The government’s blockchain ID program may reignite NFC demand in healthcare and public services where authentication rigor matters. Meanwhile, Naver Pay installations soared 186% after integrating with Samsung Pay, showing how platform alliances can scale wallet acceptance without new hardware.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High credit-card interchange fees | -0.8% | National, acute for small and medium enterprises | Short term (≤ 2 years) |

| Cybersecurity and fraud risks | -0.6% | Metropolitan areas with high digital adoption | Short term (≤ 2 years) |

| Aging population’s payment habits | -0.4% | Rural provinces | Long term (≥ 4 years) |

| Cross-border data-transfer compliance | -0.3% | Multinational payment processors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Credit-Card Interchange Fees

Merchant discount rates range from 1.5-2.5%, pressuring margins at convenience stores and quick-service restaurants. Tiered caps introduced in 2024 cut fees to 0.5% for micro-merchants under KRW 500 million turnover, yet loopholes persist for contactless and online categories. Regulatory arbitrage steers retailers toward zero-fee account-to-account QR options that sidestep card networks. BC Card’s travel card, launched in March 2025, charges a flat 1% FX markup to retain merchant loyalty without relying on interchange. Should policymakers mandate zero-fee ceilings for small tickets, card issuers may shrink rewards programs, diminishing transaction incentives and limiting the upside for the South Korea payments market.

Cybersecurity And Fraud Risks

A USD 4.1 million deepfake voice-phishing event in 2024 spurred new authentication requirements on transactions above KRW 1 million. The Virtual Asset User Protection Act broadened KYC obligations for token issuers in July 2024, but enforcement gaps surfaced when Kakao Pay transmitted user data to Alipay without explicit consent, triggering a temporary data-flow freeze. Strict data localization under the Personal Information Protection Act requires processors to host Korean records domestically, complicating cloud migrations for global gateways. Extra biometric and behavioral analytics layers add 15-20 basis points to processing costs, tightening margins for mid-tier acquirers. Such cost inflation could slow adoption among small merchants and moderate the South Korea payments market growth trajectory.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Mode of Payment: Digital Wallets Overtake Cards Online

Debit cards controlled 33.82% of point-of-sale value in 2025, anchoring habitual in-store spending patterns among salaried workers. Credit cards still dominate high-ticket travel and electronics categories thanks to installment plans and mileage perks, but their online share is slipping as one-click wallets streamline checkout. Digital wallets used in e-commerce are set to grow at a 7.55% CAGR to 2031, the swiftest among instruments, driven by tokenized credentials and biometric login that eliminate form-fill friction. Account-to-account transfers capture peer-to-peer and bill-pay use cases by leveraging the 30 million open-banking accounts. Cash on delivery remains a fallback in rural counties yet continues its steady retreat as logistics couriers embrace QR settlement. Overall, heightened convenience, loyalty integration, and cross-border reach cement wallets as the centerpiece of the South Korea payments market.

Processors now extend rails beyond borders to harness outbound tourism. KG INICIS debuted a Japan-optimized gateway in March 2025, while its December 2025 tie-up with Samsung Wallet Money lets users top up balances directly from bank accounts, bypassing card tolls. BC Card’s passport-linked QR service, live since December 2025, allows foreign visitors to pay domestically with linked overseas cards, widening merchant reach for inbound travel. Such innovations underscore how the South Korea payments market size for wallets is poised to cannibalize card-based revenue even in traditionally card-centric verticals.

By End-User Industry: Healthcare Emerges As Fastest Riser

Retail racked up 47.83% of total transaction value in 2025, underpinned by ubiquitous QR codes at convenience outlets and loyalty integrations that drive repeat footfall. Entertainment and hospitality benefit from the revival of domestic tourism, yet their expansion lags healthcare, which is on a 7.62% CAGR trajectory through 2031. Telemedicine pilots began in mid-2023 and gained ground when reimbursement schedules widened again in February 2024, spurring wallet-based copay settlements and subscription monitoring tools. The Ministry of Food and Drug Safety approved 376 software-as-a-medical-device products between 2020-2023, each requiring frictionless payment hooks for prescription delivery and data analytics subscriptions. As digital consults scale, hospitals integrate open-banking APIs to automate claim reconciliation, positioning healthcare as a pivotal contributor to the South Korea payments market.

Education and public-sector payments trail, constrained by procurement rules and legacy invoicing, yet the Digital Platform Government mandate for standardized APIs is lowering technical barriers. Stablecoins, once regulated under the forthcoming Phase 2 Digital Assets Act, could automate school-fee escrow and municipal disbursements, unlocking new flows. Consequently, healthcare’s current 7.62% CAGR marks only the foreground of broader industry diversification within the South Korea payments market.

Geography Analysis

Real-time payments adoption remains most intense in the Seoul Capital Area, where population density, 5G penetration, and NFC-enabled transit systems converge. Merchants in Gangnam and Songpa accounted for the bulk of mobile-wallet volume in 2025, reflecting high disposable income and tech affinity. Busan’s port logistics hub exhibits rising account-to-account B2B settlements as exporters embrace instant foreign-exchange quotes within open-banking dashboards. Incheon’s airport-driven hospitality sector benefits from BC Card’s passport-linked QR wallet, which captured a noticeable share of duty-free transactions during the Chuseok peak travel season. Together, the three metropolitan regions constitute the lion’s share of the South Korea payments market.

Secondary cities such as Daegu, Daejeon, and Gwangju are seeing accelerating wallet adoption as retail chains roll out standard QR code acceptance stickers, yet digital inclusion gaps persist in neighboring rural counties. Agricultural provinces in Jeolla and Gyeongsang still rely on cash-on-delivery for crop-supply purchases, although postal-bank pilots using QR-based subsidy disbursements show promise in nudging older residents toward mobile channels. The Statistics Korea projection that citizens aged 65 or older will exceed 24% of the population by 2030 underscores the necessity of geriatric-friendly UX design to maintain the South Korea payments market momentum.

Cross-border corridors also shape geographic dynamics. Outbound tourists originating from Seoul and Busan airports accounted for the largest share of KRW-denominated wallet spend in Japan and Malaysia, aided by processor partnerships that waive FX spreads. Conversely, inbound travelers from Southeast Asia increasingly leverage passport-linked QR wallets to pay in Korean won, boosting transaction counts in tourist zones from Myeong-dong to Haeundae. Regional policy coordination on stablecoin redemption guarantees could further blur domestic and cross-border boundaries, reinforcing geographic diversification inside the South Korea payments market.

Competitive Landscape

NICE Payments held most of the value-added-network throughput as of December 2024, servicing 1.16 million merchants and anchoring fee-based middleware for acquirers. Fintech challengers remain fragmented as Kakao Pay leverages 47 million messaging users, Naver Pay thrives on search and e-commerce traffic, Toss capitalizes on millennial budgeting tools, and Samsung Pay continues to ride handset pre-installs. Each platform courts distinct demographics, generating healthy rivalry that sustains user-centric innovation in the South Korea payments market.

Strategy is tilting toward vertical integration. Kakao Pay’s failed July 2025 bid for SSG Pay and Smile Pay sought to fold checkout data into its advertising flywheel. Naver’s January 2026 purchase of Dunamu earmarks KRW 10 trillion for building a won-pegged stablecoin backed by high-quality reserves, betting that programmable money will capture B2B escrow and royalty-split functions now underserved by card networks. NH Nonghyup Bank’s Partior pilot and Hana Financial’s Dunamu partnership show incumbents hedging against fintech encroachment through distributed-ledger experimentation.

Infrastructure gaps create openings for alliances. Only 10% of point-of-sale terminals support NFC, so Apple Pay relies on Shinhan Card’s June 2025 issuer approval but remains volume-constrained. This bottleneck primes account-to-account instant rails to siphon low-value spend, particularly after the Financial Services Commission hinted at a zero-fee model for micro-merchants. As interchange economics shift, participants pursue fee diversification via foreign-exchange markups, data-analytics subscriptions, and embedded lending. These maneuvers collectively reinforce medium-level rivalry, keeping the South Korea payments market in a dynamic equilibrium.

South Korea Payments Industry Leaders

Visa Inc.

American Express Company

Naver Financial Corp. (Naver Pay)

Samsung Electronics Co., Ltd. (Samsung Pay)

Toss Payments Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Naver acquired Dunamu and earmarked KRW 10 trillion (USD 7.5 billion) over five years to build a won-pegged stablecoin platform, while Kakao announced its own retail-deposit-token project.

- December 2025: NH Nonghyup Bank finalized a Partior blockchain proof-of-concept for minute-level cross-border settlement.

- December 2025: BC Card rolled out a passport-linked QR wallet for foreign visitors, widening inbound tourism acceptance.

- December 2025: KG INICIS integrated Samsung Wallet Money funding links to lower interchange costs for merchants.

South Korea Payments Market Report Scope

The South Korea Payments Market Report is Segmented by Mode of Payment (Point of Sale [Debit Card, Credit Card, Account-to-Account, Digital Wallet, Cash, and More], Online Sale [Debit Card, Credit Card, Account-to-Account, Digital Wallet, Cash-on-Delivery, and More]), and End-User Industry (Retail, Entertainment, Hospitality, Healthcare, Other). Market Forecasts are Provided in Terms of Value (USD).

By Mode of Payment

| Point of Sale | Debit Card Payments |

| Credit Card Payments | |

| Account-to-Account (A2A) Payments | |

| Digital Wallet | |

| Cash | |

| Other Point-of-Sale Payment Modes | |

| Online Sale | Debit Card Payments |

| Credit Card Payments | |

| Account-to-Account (A2A) Payments | |

| Digital Wallet | |

| Cash-on-Delivery | |

| Other Online-Sales Payment Modes |

By End-User Industry

| Retail |

| Entertainment |

| Hospitality |

| Healthcare |

| Other End-User Industries |

| By Mode of Payment | Point of Sale | Debit Card Payments |

| Credit Card Payments | ||

| Account-to-Account (A2A) Payments | ||

| Digital Wallet | ||

| Cash | ||

| Other Point-of-Sale Payment Modes | ||

| Online Sale | Debit Card Payments | |

| Credit Card Payments | ||

| Account-to-Account (A2A) Payments | ||

| Digital Wallet | ||

| Cash-on-Delivery | ||

| Other Online-Sales Payment Modes | ||

| By End-User Industry | Retail | |

| Entertainment | ||

| Hospitality | ||

| Healthcare | ||

| Other End-User Industries | ||

Key Questions Answered in the Report

How large is the South Korea payments market in 2026?

The South Korea payments market size stood at USD 1.34 trillion in 2026 and is forecast to hit USD 1.84 trillion by 2031.

Which payment instrument is growing fastest online?

Digital wallets used in e-commerce are expanding at a 7.55% CAGR, the quickest among all modes of payment.

What segment holds the biggest share of transaction value?

Retail commands 47.83% of 2025 transaction value, reflecting widespread QR-code acceptance and loyalty integration.

Why is NFC adoption lagging despite Apple Pay’s entry?

Only about 10% of Korean point-of-sale terminals support NFC because Samsung Pay’s magnetic-secure transmission works on legacy hardware, limiting merchant incentive to upgrade.

How are interchange fees affecting small merchants?

Fees as high as 2.5% erode thin margins, prompting regulators to cap rates at 0.5% for micro-merchants and encouraging a shift toward zero-fee account-to-account options.

Page last updated on: