Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2020 - 2024 |

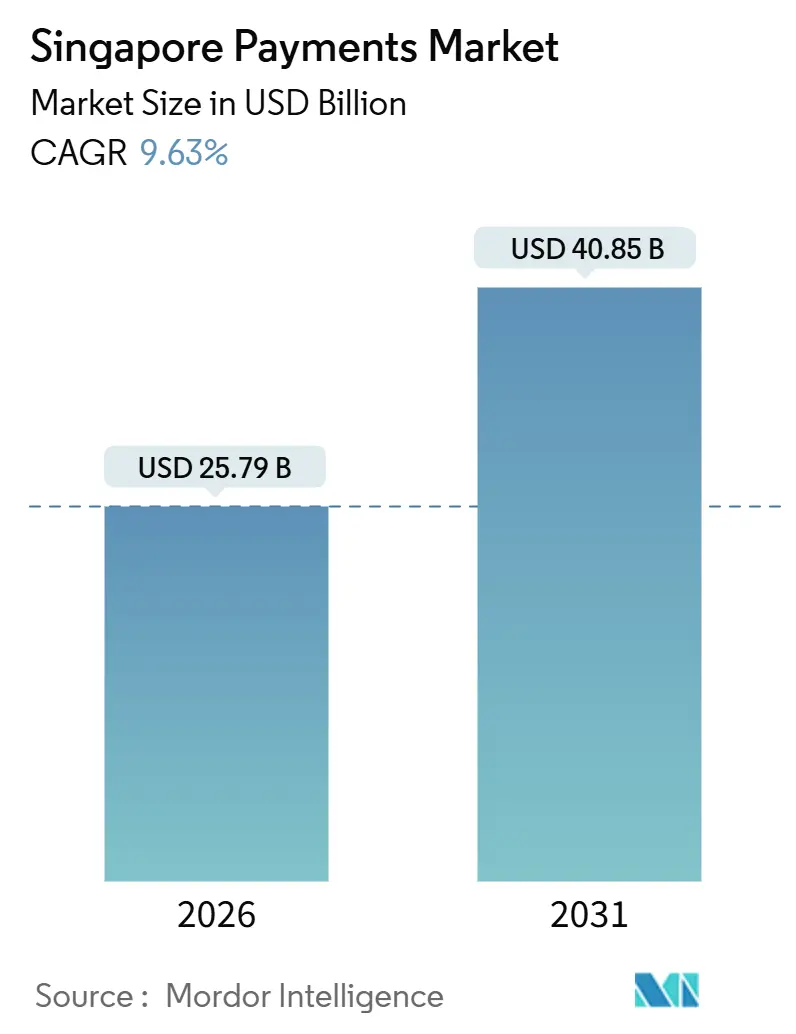

| Market Size (2026) | USD 25.79 Billion |

| Market Size (2031) | USD 40.85 Billion |

| Growth Rate (2026 - 2031) | 9.63% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Singapore Payments Market Analysis by Mordor Intelligence

The Singapore payments market size is valued at USD 25.79 billion in 2026 and is forecast to reach USD 40.85 billion by 2031, reflecting a 9.63% CAGR. Ongoing government mandates, the rapid scaling of PayNow rails, and aggressive super-app expansion position the Singapore payments market as a living laboratory for real-time, low-cost transactions. Real-time account-to-account options are absorbing share in e-commerce, while physical retail still leans on cards because of terminal ubiquity. Cross-border corridors that connect PayNow to India, Malaysia, and Thailand shorten settlement cycles from days to seconds, supporting inbound tourism and overseas remittances. Competitive pressure stems from merchant-discount-rate caps that squeeze processors even as volumes rise, forcing pivot toward lending, foreign-exchange conversion, and loyalty orchestration.

Key Report Takeaways

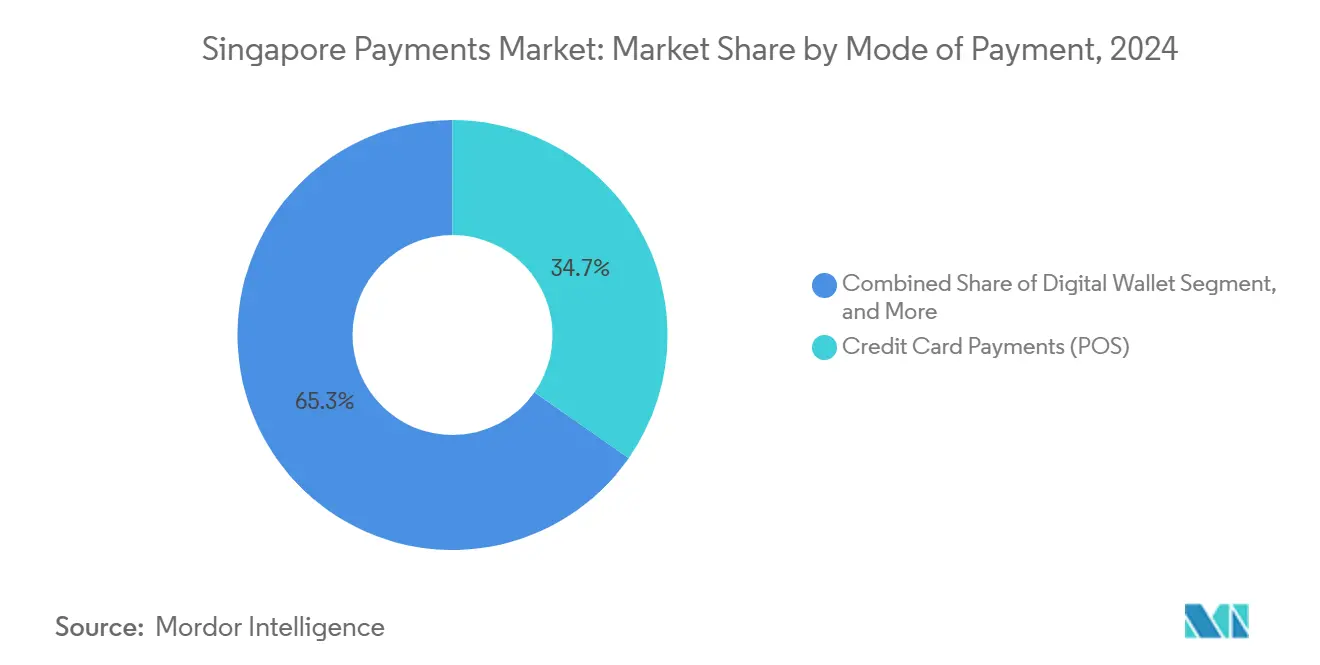

- By mode of payment, credit cards held 34.72% of transaction value at point-of-sale in 2025, whereas online account-to-account transfers are projected to post a 10.62% CAGR through 2031.

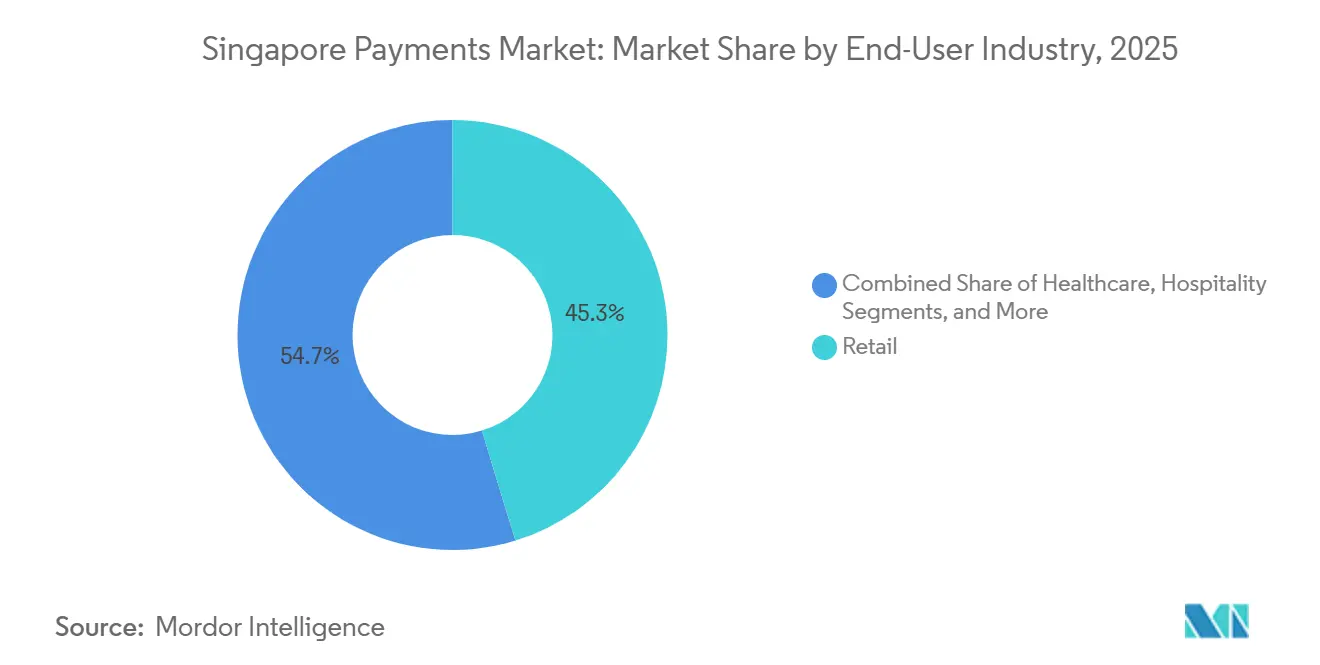

- By end-user industry, retail commanded 45.72% of value in 2025, while healthcare is projected to expand at a 10.73% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Singapore Payments Market Trends and Insights

Drivers Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-commerce boom and cross-border retail spend | +2.3% | National, spillover to ASEAN | Medium term (2-4 years) |

| Government-led digital voucher and SGQR initiatives | +2.1% | National, concentrated in hawker centers, healthcare, public transport | Short term (≤ 2 years) |

| Near-real-time PayNow and FAST rails scaling to SMEs | +1.9% | National, cross-border extension to India, Malaysia, Thailand | Medium term (2-4 years) |

| Super-app ecosystems bundling payments and services | +1.7% | National, Southeast Asia reach | Long term (≥ 4 years) |

| Project Orchid CBDC pilots for B2B settlement | +0.8% | National, pilot phase | Long term (≥ 4 years) |

| ESG-linked incentives for low-carbon transactions | +0.5% | National, early corporate banking adoption | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

E-Commerce Boom and Cross-Border Retail Spend

Visa-free entry restoration in 2024, PayNow-UPI linkage in February 2025, and previous tie-ups with PromptPay and DuitNow compress settlement to seconds, shaving 40-60 basis points off foreign-exchange spreads.[1]Monetary Authority of Singapore, “PayNow and FAST Payment Services,” MAS.gov.sg Chinese tourists increasingly favor Alipay+ and WeChat Pay at Orchard Road and Changi outlets, reflecting Beijing’s QR-code push over card schemes. E-commerce majors such as Shopee and Lazada route Singapore-dollar proceeds via SGQR, letting overseas sellers bypass local bank accounts, which intensifies competition in fashion, electronics, and beauty.

Government-Led Digital Voucher and SGQR Initiatives

The RedeemSG scheme disbursed SGD 300 (USD 222) digital vouchers to citizens in 2024, compelling 164,000 PayNow-enabled merchants to accept SGQR payments.[2]Infocomm Media Development Authority, “Hawkers Go Digital Programme,” IMDA.gov.sg Hawkers Go Digital waived the 0.5% merchant discount rate through December 2025, removing cost objections for small food vendors. SGQR reached 27 public hospitals and polyclinics in May 2025, cutting outpatient queue times by 30%.[3]SingHealth, “SGQR Rollout to Public Healthcare Facilities,” SingHealth.com.sg Healthcare’s high-ticket, repeat transactions now reinforce habitual wallet use that spills into retail and entertainment.

Near-Real-Time PayNow and FAST Rails Scaling to SMEs

PayNow registrations topped 5 million by end-2024, with cumulative value above SGD 50 billion (USD 37 billion). The Inland Revenue Authority’s November 2025 InvoiceNow mandate embeds PayNow numbers in Peppol invoices, shrinking accounts-receivable cycles from 30 days to under 48 hours. Freelancers and gig workers now generate QR codes at zero marginal cost, while SMEs gain automated reconciliation that disadvantages card settlements lacking machine-readable data.

Super-App Ecosystems Bundling Payments and Services

Grab’s 43.9 million monthly users generated USD 253 million in financial-services revenue in 2024, underpinned by USD 1.2 billion in deposits and a USD 536 million loan book. GrabPay’s 35.3% wallet share and loyalty program lock users into ride-hailing, delivery, and commerce. The November 2025 pact with StraitsX pilots stablecoin payouts that could sidestep correspondent fees, though regulatory clarity on reserves is pending.

Restraints Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising e-commerce fraud and social-engineering scams | -1.4% | National, affects consumer trust | Short term (≤ 2 years) |

| Merchant MDR cap pressures PSP profitability | -1.2% | National, hawker and small-merchant focus | Medium term (2-4 years) |

| Inter-wallet gaps for inbound foreign visitors | -0.6% | Tourist districts and airport retail | Short term (≤ 2 years) |

| Real-time rails cannibalizing card interchange | -0.9% | National, card network revenues | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising E-Commerce Fraud and Social-Engineering Scams

Scam losses hit SGD 1.01 billion (USD 750 million) in 2024, a 53% jump year-on-year. Real-time irrevocability speeds fund dispersal across jurisdictions. Banks responded with Money Lock sub-accounts that impose 12-hour withdrawal cooling-off, while the Monetary Authority’s shared-liability proposal would reimburse compliant victims up to SGD 100,000 (USD 74,000). PSPs must now invest in behavioral analytics and device fingerprinting, raising onboarding costs.

Merchant MDR Cap Pressures PSP Profitability

The Hawkers Go Digital subsidy erased a 0.5% MDR through December 2025, forcing acquirers to absorb interchange and network fees without offsetting revenue. Expectations of zero-cost acceptance may linger, making fee reinstatement politically sensitive. Processors seek margin in working-capital loans and inventory financing but need credit-risk capabilities many lack. International entrants such as Stripe and Adyen face local super-apps that can cross-subsidize acceptance from profits in ride-hailing and banking, producing a cost dynamic hard to match.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Mode of Payment: Real-Time Rails Reshape Channel Economics

Credit cards retained a 34.72% slice of point-of-sale value in 2025, underscoring entrenched terminal networks and rewards propositions. Conversely, online account-to-account transfers are forecast to grow at 10.62% CAGR, the fastest pace across channels, reflecting consumer preference for instant, low-fee settlement. Digital wallets captured 39% of e-commerce value in 2024, down from 47% a year earlier as card issuers countered with enhanced cashback and installment options. Debit cards remain relevant for spend-control users, yet growth lags wallets that bundle loyalty and one-click checkout. Cash-on-delivery persists for luxury goods but continues to shrink.

Apple’s Tap to Pay on iPhone debuted in December 2025, letting merchants accept contactless payments with only a phone, which could accelerate small-merchant card and wallet penetration. Legacy stored-value cards such as NETS FlashPay survive in transport niches but face gradual displacement as mobile wallets integrate NFC and QR formats. These shifts illustrate how the Singapore payments market recalibrates economic models as real-time rails cannibalize card interchange in digital commerce, while physical retail remains anchored to cards until hardware costs fall.

By End-User Industry: Healthcare Digitization Outpaces Retail

Retail accounted for 45.72% of transaction value in 2025, driven by high-frequency supermarket and e-commerce spend. Healthcare, however, is projected to post a 10.73% CAGR through 2031, the swiftest among industries, after SGQR reached 27 public hospitals and polyclinics in May 2025. The Singapore payments market size attributable to healthcare is therefore on a steeper growth curve than legacy retail as aging demographics push recurring medical outlays.

Digital acceptance now spans telemedicine and pharmacy chains, where PayNow numbers embed directly into bills, cutting reconciliation overhead. Entertainment and hospitality receive a lift from tourism rebound, with Alipay+ and WeChat Pay acceptance at Sentosa, Marina Bay Sands, and Changi Airport capturing Chinese visitor spend. Education, transport, and government services are integrating digital channels but remain smaller contributors. The InvoiceNow mandate compels large businesses to embed PayNow IDs in invoices, shortening receivables cycles and reinforcing account-to-account uptake.

Geography Analysis

The compact city-state concentrates 5.9 million digitally connected residents, letting regulators pivot the entire Singapore payments market with policy strokes. The regulatory sandbox born in 2016 nurtured fintech pilots that matured into PayNow and FAST, which now act as ASEAN templates. Cross-border ties to India’s UPI, Thailand’s PromptPay, and Malaysia’s DuitNow remove correspondent banks, lowering migrant-worker remittance costs and simplifying merchant settlement.

The June 2025 creation of Singapore Payments Network unified oversight of NETS, SGQR, and real-time schemes, tackling wallet fragmentation that frustrated tourists. Project Orchid’s November 2025 BLOOM trial tokenized wholesale deposits for instantaneous cross-border B2B settlement, hinting at liquidity savings of 20-30%.

While retail CBDC remains distant, wholesale insights shape future architecture. The Payment Services Act licenses all providers and aligns AML, CTF, and cybersecurity rules with FATF norms, while the shared-liability scam framework shifts risk onto institutions, prompting heavier investment in fraud controls. Regional peers observe Singapore’s model when crafting their own regulatory blueprints, cementing the city-state’s influence on Southeast Asian payment standards.

Competitive Landscape

Competition spans global card networks, super-apps, and specialist processors. Visa and Mastercard still earn interchange on point-of-sale flows but face margin compression as PayNow rails siphon digital-commerce volume. Grab leverages its closed ecosystem, 43.9 million users, and USD 1.2 billion in deposits to cross-sell loans, insurance, and wealth products, blunting pure-play processors. Stripe, Adyen, and Checkout.com attract merchants via developer-friendly APIs yet must operate within MDR caps that local super-apps can subsidize through ancillary profits.

White-space lies in cross-border B2B payments as the BLOOM CBDC trial proved tokenized settlement can slash liquidity costs, attracting banks and corporates. Emerging players such as StraitsX pilot stablecoin payouts with Grab, aiming at near-zero FX costs for remittances, though capital rules remain unsettled. Technology differentiation now tilts toward embedded finance, where payments become a feature inside vertical software rather than a standalone integration.

Singapore Payments Industry Leaders

PayPal Holdings, Inc.

Grab Holdings Ltd.

Network for Electronic Transfers (Singapore) Pte Ltd.

Visa Inc.

Apple Inc. (Apple Pay)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Grab confirms Tap to Pay integration for early-2026 merchant rollout, expanding contactless acceptance for micro-merchants.

- December 2025: Apple launched Tap to Pay on iPhone in Singapore on December 2 2025, partnering with Stripe, Adyen, Revolut, HitPay, Fiuu, and Zoho.

- November 2025: Grab signed a memorandum of understanding with StraitsX on November 18, 2025 to pilot stablecoin settlements for cross-border remittances and merchant payouts.

- November 2025: The Monetary Authority completed the BLOOM wholesale CBDC trial, demonstrating 20-30% liquidity cost savings for banks in cross-border settlement.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Singapore payments market as the total value of transactions carried out by consumers at physical points of sale and on domestic e-commerce or travel platforms. The model counts card, account-to-account, and digital wallet flows settled in Singapore dollars or cross-border rails that terminate in Singapore merchants; cash usage is tracked only as a share driver, not as value.

Scope Exclusion. The framework omits motor vehicle and real estate purchases, utility or loan bill payments, and capital market trades.

Segmentation Overview

- By Mode of Payment

- Point-of-Sale

- Debit Card Payments

- Credit Card Payments

- Account-to-Account (A2A) Payments

- Digital Wallet

- Cash

- Other Point-of-Sale Payment Mode

- Online Sale

- Debit Card Payments

- Credit Card Payments

- Account-to-Account (A2A) Payments

- Digital Wallet

- Cash-on-Delivery

- Other Online Sales Payment Mode

- Point-of-Sale

- By End-User Industry

- Retail

- Entertainment

- Hospitality

- Healthcare

- Other End-User Industries

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed acquiring banks, payment gateways, and large online merchants across Central, North, and East regions. These conversations let us stress test growth levers such as instant payment adoption and average ticket sizes, while short consumer pulse surveys clarified channel migration after PayNow rail expansions.

Desk Research

We began with datasets issued by the Monetary Authority of Singapore, the Infocomm Media Development Authority, and the Department of Statistics, which anchor transaction volumes, smartphone penetration, and household e-commerce outlay. Industry associations such as the Singapore Retailers Association and ASEAN+3 Macroeconomic Research Office supplied supplemental indicators on card circulation and regional remittance corridors. Our team next pulled company filings, investor decks, and press releases to track fee structures and wallet load value. Select modules from D&B Hoovers and Dow Jones Factiva helped us validate issuer revenue and news driven shocks. This list is illustrative, and many additional public and paid sources informed our desk work.

Market-Sizing & Forecasting

We reconstructed the 2025 baseline through a top down transaction value pool that layers MAS card switch data, FAST rail statistics, and estimated wallet balances, which are then cross checked with sampled average selling price × volume calculations at leading acquirers. Key drivers, smartphone penetration, e-commerce gross merchandise value, real time transfer share, credit card rewards intensity, and merchant QR acceptance feed a multivariate regression that projects demand to 2030. Bottom up supplier roll ups fill any channel gaps, and scenario analysis adjusts for regulatory fee caps.

Data Validation & Update Cycle

Outputs flow through variance checks against external benchmarks and prior editions. Senior analysts review anomalies before sign off, and we refresh every twelve months, with interim updates triggered by material policy or infrastructure changes.

Why Mordor's Singapore Payments Baseline Inspires Confidence

Published estimates often diverge because firms choose distinct scopes, currency conversions, or refresh cadences, and we acknowledge that upfront.

The most common gaps arise when broader studies fold in wholesale clearing totals or, conversely, study only card issuance revenue, while Mordor reports the consumer facing transaction pool supported by MAS data and annual model recalibration.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 23.53 B (2025) | Mordor Intelligence | |

| USD 120 B (2024) | Regional Consultancy A | Bundles peer to peer transfers and interbank settlement layers without de-duplication |

| USD 4.48 B (2024) | Industry Association B | Focuses solely on card issuer fee revenue and ignores wallet and A2A flows |

These comparisons show that, by selecting a balanced scope and validating every assumption through public statistics and first hand interviews, Mordor Intelligence delivers a dependable baseline that decision makers can trace back to transparent variables and repeatable steps.

Key Questions Answered in the Report

How fast is the Singapore payments market expected to grow through 2031?

Market value is projected to rise from USD 25.79 billion in 2026 to USD 40.85 billion by 2031, registering a 9.63% CAGR.

Which payment channel is expanding the quickest?

Online account-to-account transfers are forecast to grow at 10.62% CAGR, the fastest among all modes.

Why is healthcare becoming a high-growth vertical?

SGQR deployment across 27 public hospitals and polyclinics in 2025 streamlined billing, pushing healthcare transaction value to a projected 10.73% CAGR.

What is driving cross-border payments growth?

PayNow links to India, Malaysia, and Thailand reduce settlement times to seconds and lower FX costs, increasing tourist and remittance flows.

How are providers countering MDR caps?

Processors diversify into lending, FX conversion, and data analytics to offset thinner acceptance margins.

Page last updated on: