Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

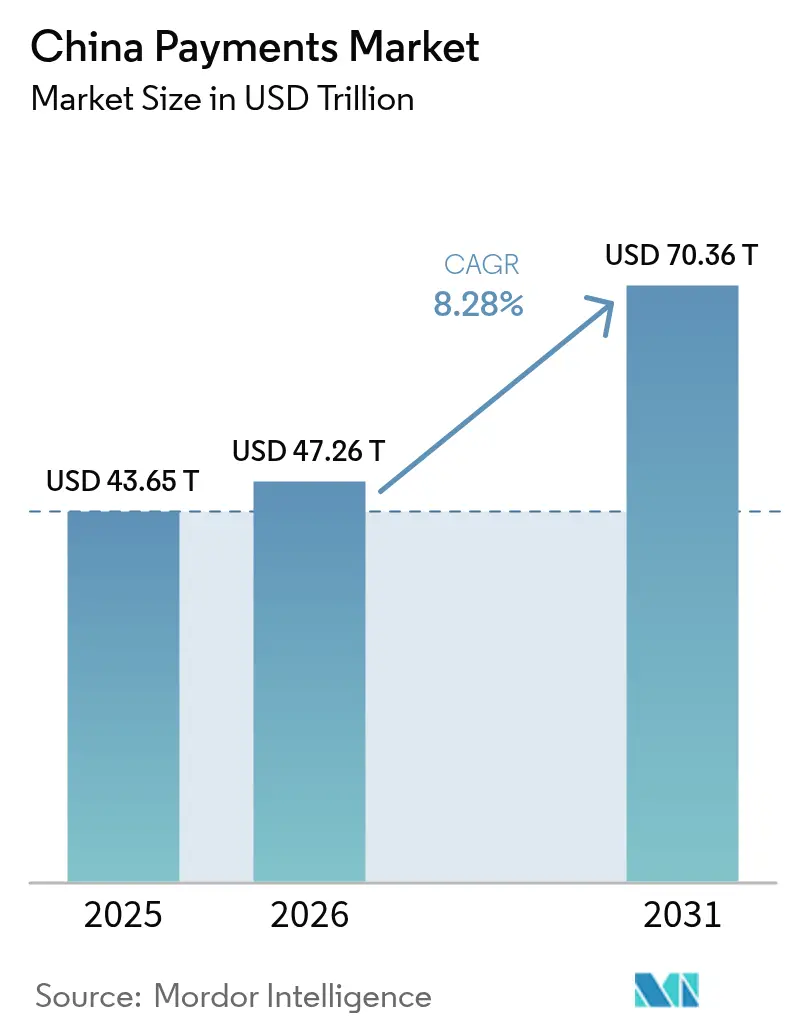

| Base Year Market Size (2025) | USD 43.65 Trillion |

| Market Size (2026) | USD 47.26 Trillion |

| Market Size (2031) | USD 70.36 Trillion |

| Growth Rate (2026 - 2031) | 8.28% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Payments Market Analysis by Mordor Intelligence

The China payments market size was valued at USD 43.65 trillion in 2025 and estimated to grow from USD 47.26 trillion in 2026 to reach USD 70.36 trillion by 2031, at a CAGR of 8.28% during the forecast period (2026-2031). The China payments market is propelled by the near-universal reach of mobile wallets, rapid build-out of real-time account-to-account rails, and strong policy backing for a cash-light society. The digital yuan pilot adds a programmable, central-bank rail that coexists with private super-apps, while biometric authentication and IoT use cases widen the addressable transaction universe. Competitive intensity revolves around platform ecosystem lock-in rather than fee compression, and regulatory oversight has become the principal brake on growth momentum. Merchant enablement tools, rural digitization programs, and cross-border commerce corridors continue to broaden the user base and diversify revenue streams, reinforcing the upward trajectory of the China payments market.

Key Report Takeaways

- By mode of payment, digital wallets led with 72.05% of the China payments market share in 2025; account-to-account payments are advancing at a 9.09% CAGR through 2031.

- By end-user industry, retail accounted for 45.18% of the China payments market size in 2025, while healthcare is growing at an 8.52% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

China Payments Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of Mobile Wallets and Super-apps | +2.2% | National, with highest penetration in Tier 1-2 cities | Medium term (2-4 years) |

| Expansion of E-commerce and M-commerce Ecosystems | +1.8% | National, with rural acceleration via livestreaming | Long term (≥ 4 years) |

| Government Push for Digital Yuan and Cashless Society | +1.5% | National pilot cities expanding to full coverage | Long term (≥ 4 years) |

| Rise of Mini-Program In-App Payments | +1.2% | Urban centers with super-app ecosystem maturity | Medium term (2-4 years) |

| Adoption of Biometric POS Authentication | +0.8% | Tier 1-3 cities with infrastructure readiness | Short term (≤ 2 years) |

| Integration of Payments into Industrial IoT | +0.6% | Manufacturing hubs and smart city pilots | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Proliferation of Mobile Wallets and Super-apps

Super-app architecture pioneered by Alipay and WeChat Pay keeps users inside closed-loop ecosystems that blend payments, commerce, and public services. More than 1.3 billion monthly active users tap mini-programs that remove checkout friction and give merchants built-in marketing and credit tools. These network effects depress customer-acquisition costs and raise switching barriers, which in turn deepen user engagement and lift transaction frequency within the China payments market. Platform compliance with central-bank cybersecurity and resilience requirements underpins public trust, while continuous feature releases such as wealth management modules add further stickiness. The result is a virtuous cycle that sustains double-digit volume growth even in saturated urban pockets.

Expansion of E-commerce and M-commerce Ecosystems

Domestic online retail sales exceeded CNY 43.8 trillion in 2024, with the vast majority routed through mobile checkout. Livestream shopping, group buying, and social-commerce formats use instant settlement to shorten working-capital cycles for merchants and creators. Rural shoppers gain equal footing via 5G coverage and low-cost smartphones, bringing fresh cohorts into the China payments market. Cross-border shopping grows on simplified currency conversion modules and compliance screening tools embedded in super-apps, expanding reach for both Chinese exporters and overseas brands. Taken together, these forces support sustained high-single-digit expansion in payment volume even as overall consumer spending growth moderates.

Government Push for Digital Yuan and Cashless Society

The People’s Bank of China has distributed over 260 million digital-yuan wallets across 26 pilot cities.[1]People’s Bank of China, “Progress of E-CNY Pilot Work,” PBOC.gov.cn Programmable features allow targeted subsidies, automated tax collection, and transaction-level data visibility, giving policymakers new levers for macro-stability. Private platforms already plug the CBDC rail into existing checkout flows, ensuring continuity for consumers while widening settlement choices. The initiative accelerates financial inclusion in underbanked regions and reduces dependence on commercial intermediaries, adding structural momentum to the China payments market.

Rise of Mini-Program In-App Payments

Mini-programs processed transactions in the high hundreds of billions of yuan during 2024. Merchants deploy these lightweight apps inside super-apps instead of funding separate mobile builds, cutting integration time and boosting conversion through single-click payment. Small businesses gain enterprise-grade tooling, inventory, CRM, and credit scoring, delivered as plug-ins, flattening the digital-divide barrier. In parallel, municipal agencies use mini-program interfaces for bill payments and benefit disbursements, turning super-apps into citizen gateways and further entrenching their role in the China payments market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tightening FinTech Regulatory Oversight | -1.1% | National, with stricter enforcement in major financial centers | Short term (≤ 2 years) |

| Fraud and Cybersecurity Risks in Cross-Border Transactions | -0.7% | Cross-border corridors and international tourist destinations | Medium term (2-4 years) |

| Ageing Population Hindering Rural Digital Adoption | -0.5% | Rural areas and smaller cities with higher elderly demographics | Long term (≥ 4 years) |

| Interoperability Gaps – CBDC Wallets vs. Legacy Rails | -0.4% | Digital yuan pilot cities and areas with mixed payment infrastructure | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Tightening FinTech Regulatory Oversight

Post-2024 enforcement has intensified under the National Financial Regulatory Administration, with fines on banking partners topping CNY 738 million in the first half of 2024.[2]China National Financial Regulatory Administration, “Administrative Penalties Disclosed in H1 2024,” nra.gov.cn Revised Anti-Money Laundering rules effective 2025 significantly raise penalty ceilings and require external compliance monitors for high-risk entities. Payment-service-provider licences remain capped at 184, forcing aspirants to enter the China payments market via costly acquisitions rather than new grants. Continuous reporting and stress-testing obligations elevate fixed costs, squeezing smaller players and nudging market power further toward scale incumbents. Innovation budgets face pressure as firms divert capital to regulatory tooling.

Fraud and Cybersecurity Risks in Cross-Border Transactions

Emergent toolkits such as Z-NFC exploit contactless protocols, targeting travelers and merchants in duty-free zones. UnionPay International’s 2024 advisories underscore rising phishing sophistication in overseas checkout flows. New court precedents expand liability for providers that cannot prove “best-effort” fraud controls, amplifying compliance spend. Cross-border data-sharing constraints slow down risk-model calibration, eroding the friction-less edge that Chinese wallets enjoyed abroad. These headwinds temper the cross-border growth node of the China payments market even as domestic security metrics improve.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Mode of Payment: Digital Wallets Dominate While A2A Payments Accelerate

Digital wallets captured 72.05% of the China payments market share in 2025 on the back of ubiquitous QR infrastructure and seamless super-app checkout. The China payments market size linked to wallets is projected to grow at high single digits through 2030 as consumer preference solidifies in both urban and rural settings. Account-to-account options are climbing at a 9.09% CAGR, driven by new instant-payment rails that bypass card networks and undercut interchange fees. Real-time transfers are gaining traction for payroll disbursement, peer-to-peer gifting, and merchant settlement, indicating wallet and A2A convergence ahead. Cash continues to shrink, estimated at just 5% of transaction value in megacities, while card traffic remains relevant mainly for large-ticket, rewards-driven travel purchases. Niche instruments such as prepaid cards find survival niches in corporate expense management but face stagnant volume prospects.

Second-order effects reinforce A2A momentum. E-commerce sellers reduce working-capital cycles because funds settle within seconds, enabling just-in-time inventory strategies. Cross-border remittances leverage the same rails to avoid correspondent-bank charges, bringing fee relief to students and migrant workers. Wallet providers embed A2A modules, giving users a single interface to shuttle money between bank accounts and in-app balances, further blurring category lines in the China payments market. Over time, analysts expect the value share gap between wallets and A2A to narrow, though the volume hierarchy is likely to persist.

By End-User Industry: Retail Leadership Challenged by Healthcare Acceleration

Retail transactions accounted for 45.18% of the China payments market size in 2025 as QR codes reached every checkout, from luxury malls to street stalls. Strong loyalty integration, BNPL add-ons, and gamified coupons keep consumer stickiness high. In contrast, healthcare payments are advancing at an 8.52% CAGR, the fastest among tracked sectors. Hospital information-system upgrades enable integrated registration, diagnosis, and payment in one app encounter, curbing queuing times and administrative costs. Telemedicine visits finalize billing within the consultation window, exemplifying embedded finance in public services.

Transportation, entertainment, and hospitality also post swift cashless adoption. Ride-hailing and food-delivery operators impose wallet or A2A default options, normalizing digital settlement for daily micro-transactions. Government service portals channel bill payments and fee receipts directly through super-apps, extending the routine use case set. While average ticket sizes vary widely, the unified experience advances the goal of a cash-light China payments market. Sector divergences will continue to narrow as policy pushes healthcare, education, and utilities toward full digital acceptance.

Geography Analysis

Tier-1 cities such as Beijing, Shanghai, and Shenzhen exhibit near-total digital penetration, with cash’s share of consumer spend in low single digits. Merchant acceptance infrastructure supports biometric checkout, IoT vending, and CBDC wallet top-ups, creating an innovation flywheel that keeps the China payments market at the frontier of global best practice. In these hubs, competition now pivots to value-added services including micro-investing and loyalty-marketing engines rather than raw payment processing.

Tier-2 and Tier-3 urban clusters show similar wallet adoption curves, albeit with heavier reliance on QR rather than biometric authentication. Government smart-city programs subsidize POS upgrades, and regional banks partner with super-apps to extend consumer credit at point of sale. Digital-yuan trials are rolled out selectively, providing households with an alternative settlement rail while maintaining the familiar super-app interface. As infrastructure deepens, usage patterns in these cities increasingly mirror those of the megacities, reinforcing nationwide cohesion in the China payments market.

Rural counties lag in device penetration and merchant readiness, yet mobile-network coverage and smartphone affordability are closing the gap. Agricultural e-commerce platforms funnel subsidies and seed financing through instant transfers, nudging farmers into digital rails. Younger cohorts introduce peer-influence dynamics, teaching older relatives to scan QR codes for grocery runs and utility bills. Policy initiatives bundle consumer-protection education with fintech-literacy drives, ensuring responsible onboarding. Over time, analysts expect growth rates in rural regions to outpace urban centers on a low-base effect, driving the next leg of the China payments market expansion.

Competitive Landscape

Alipay and WeChat Pay command over 90% of digital-transaction volume, giving the China payments market one of the highest concentration ratios globally. Their super-app ecosystems host everything from micro-loans to municipal-service fees, weaving payments invisibly into daily life. UnionPay remains dominant in plastic-card issuance, but its mobile front-end, Cloud QuickPass, competes head-on with QR wallets by enabling tokenized NFC checkout and digital-yuan compatibility. The strategic battleground has moved from per-transaction economics to ecosystem depth, data-analytics prowess, and cross-border reach.

Licensing caps since 2015 mean new entrants must acquire existing permit holders, as seen when Ant Group bought MultiSafePay in 2024 and Payoneer took over Easylink in 2025. These deals expand technical capabilities and region-specific risk controls but face stringent regulatory vetting. Niche players carve space in healthcare payments, industrial IoT, and global B2B settlements where incumbents’ scale may be offset by specialized compliance or vertical expertise. Feature innovation centers on biometric hardware, AI-based fraud detection, and instant-remittance corridors, each aimed at tightening user lock-in.

Regulation is the wild card. The digital-yuan rail introduces a central-bank alternative that could reset bargaining power between private wallets and the state. Mandatory data localization and stepped-up cybersecurity audits raise compliance thresholds, raising fixed costs but also creating higher entry barriers. Given these dynamics, the China payments market is likely to remain a duopoly flanked by a long tail of specialist providers.

China Payments Industry Leaders

WeChat Pay (Tencent Holdings Ltd.)

JDPay.com (JD.com))

Alipay.com Co., Ltd.

China UnionPay Co., Ltd.

Apple Inc. (Apple Pay)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Payoneer acquired Easylink Payment Co., expanding cross-border settlement reach for export-oriented merchants.

- January 2025: Ant Group completed its USD 200 million purchase of MultiSafePay, adding European licences for global expansion.

- December 2024: The People’s Bank of China issued facial-recognition payment standards through TC260, defining encryption and consent requirements.

- August 2024: The National Financial Regulatory Administration levied CNY 738 million in fines on 380 bank entities for consumer-protection and risk-control breaches.

China Payments Market Report Scope

The China Payments Market is segmented by Mode of Payment (Point of Sale (Card Payments, Digital Wallet, Cash), Online Sale (Card Payments, Digital Wallet)), and by End-user Industries (Retail, Entertainment, Healthcare, Hospitality). E-commerce payments include online purchases of goods and services, such as purchases made on e-commerce websites and online booking of travel and accommodation. The scope of the market excludes online purchases of motor vehicles, real estate, utility bill payments (such as water, heating, and electricity), mortgage payments, loans, credit card bills, or purchases of shares and bonds. As for Point-of-Sale, all transactions that occur at the physical point of sale are included in the scope of the market. It includes traditional in-store transactions and all face-to-face transactions regardless of the location of the transaction. Cash is also considered for both cases (cash-on-delivery for e-commerce sales).

The study tracks key market metrics, underlying growth influencers, and significant industry vendors, providing support for China's market estimates and growth rates throughout the anticipated period. The study looks at COVID-19's overall influence on the China payment ecosystem.

The market sizes and forecasts are provided in terms of value (USD million) for all the above segments.

By Mode of Payment

| Point of Sale | Debit Card Payments |

| Credit Card Payments | |

| A2A Payments | |

| Digital Wallet | |

| Cash | |

| Other Point of Sale Payment Mode | |

| Online Sale | Debit Card Payments |

| Credit Card Payments | |

| A2A Payments | |

| Digital Wallet | |

| Cash-on-Delivery | |

| Other Online Sales Payment Mode |

By End-User Industry

| Retail |

| Entertainment |

| Hospitality |

| Healthcare |

| Transportation and Logistics |

| Other End-User Industries |

| By Mode of Payment | Point of Sale | Debit Card Payments |

| Credit Card Payments | ||

| A2A Payments | ||

| Digital Wallet | ||

| Cash | ||

| Other Point of Sale Payment Mode | ||

| Online Sale | Debit Card Payments | |

| Credit Card Payments | ||

| A2A Payments | ||

| Digital Wallet | ||

| Cash-on-Delivery | ||

| Other Online Sales Payment Mode | ||

| By End-User Industry | Retail | |

| Entertainment | ||

| Hospitality | ||

| Healthcare | ||

| Transportation and Logistics | ||

| Other End-User Industries | ||

Key Questions Answered in the Report

What is the current value of the China payments market?

The China payments market size stood at USD 47.26 trillion in 2026 and is projected to keep rising through the decade.

How fast is the sector expected to grow?

Aggregate transaction value is forecast to expand at an 8.28% CAGR between 2026 and 2031.

Which payment mode leads in China?

Digital wallets hold 72.05% of transaction value, far ahead of cards or cash.

Which industry vertical is growing the fastest in payments?

Healthcare payments are projected to rise at an 8.52% CAGR as hospitals and telemedicine platforms digitize billing.

How concentrated is competition among wallet providers?

The top two players, Alipay and WeChat Pay, capture more than 90% of digital volumes, resulting in a highly concentrated landscape.

Page last updated on: