Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

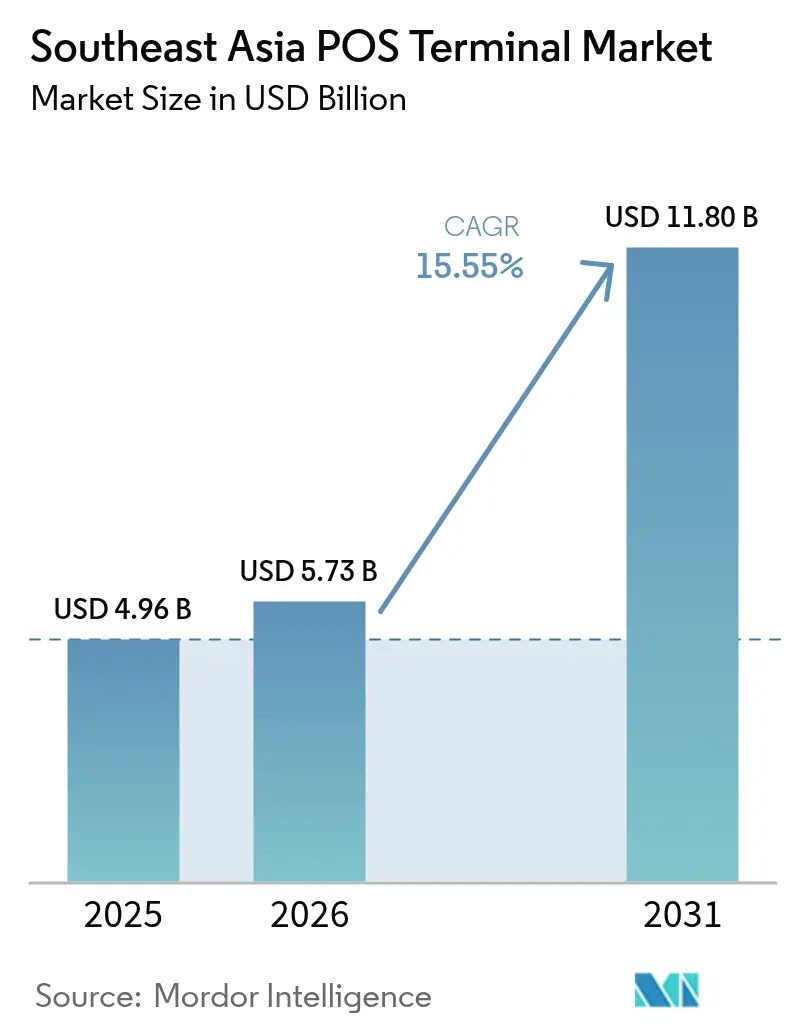

| Base Year Market Size (2025) | USD 4.96 Billion |

| Market Size (2026) | USD 5.73 Billion |

| Market Size (2031) | USD 11.8 Billion |

| Growth Rate (2026 - 2031) | 15.55% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Southeast Asia POS Terminal Market Analysis by Mordor Intelligence

The Southeast Asia POS Terminal Market size was valued at USD 4.96 billion in 2025 and estimated to grow from USD 5.73 billion in 2026 to reach USD 11.8 billion by 2031, at a CAGR of 15.55% during the forecast period (2026-2031). Strong consumer migration to mobile wallets, rising ubiquity of QR codes, and government mandates that compel digital payment acceptance are keeping the Southeast Asia POS Terminal market on a steep growth trajectory. Merchants are shifting capital toward software-defined or hybrid devices that consolidate QR, NFC, and card functions, trimming counter clutter while future-proofing acceptance needs. Competitive focus has moved from hardware specifications to software ecosystems, favoring vendors that bundle inventory, CRM, and financing tools into cloud dashboards. Cross-border payment initiatives under the ASEAN Regional Payment Connectivity program promise faster certification cycles, a factor set to unlock incremental demand for the Southeast Asia POS Terminal market through 2030.[1]ASEAN Secretariat, “Regional Payment Connectivity Initiative,” asean.org

Key Report Takeaways

- By mode of payment acceptance, contactless payments captured 56.97% revenue share in 2025 and is advancing at a 17.05% CAGR through 2031.

- By POS type, mobile and portable systems held 46.25% share of the Southeast Asia POS Terminal market size in 2025 and are poised for a 16.7% CAGR to 2031.

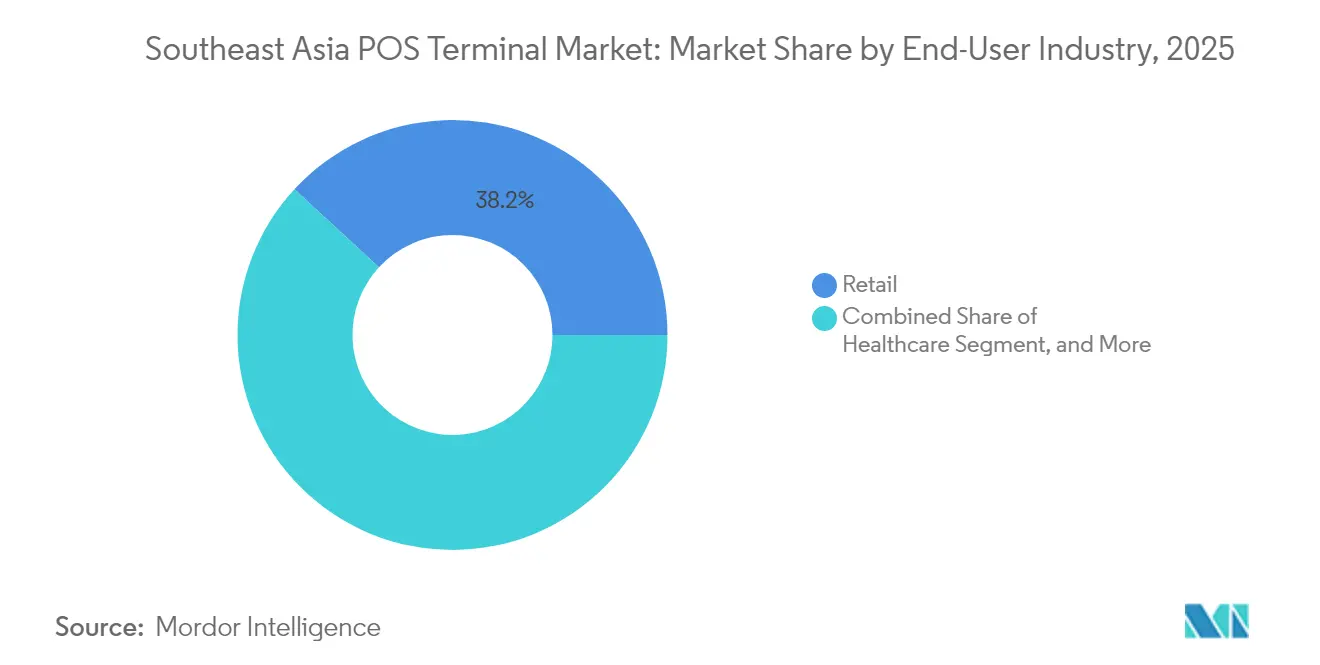

- By end-user industry, retail accounted for 38.15% share in 2025, while healthcare is forecast to expand at a 16.25% CAGR through 2031.

- By country, Indonesia captured 29.55% of the Southeast Asia POS Terminal market share in 2025 and is projected to post a 16.05% CAGR to 2031

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Southeast Asia POS Terminal Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid expansion of digital payments across Southeast Asia | +4.2% | Indonesia, Thailand, Philippines with spillover to Vietnam | Medium term (2-4 years) |

| Government cash-less initiatives and e-payment regulations | +3.8% | Singapore, Malaysia leading, Indonesia and Thailand following | Short term (≤ 2 years) |

| Rising adoption of mPOS among SMEs and micro-merchants | +3.1% | Indonesia, Philippines, Vietnam rural markets | Medium term (2-4 years) |

| Integration of BNPL capabilities into POS hardware | +2.3% | Singapore, Malaysia urban centers expanding regionally | Long term (≥ 4 years) |

| Tourism-driven omnichannel retail recovery post-COVID | +1.8% | Thailand, Singapore, Malaysia tourism corridors | Short term (≤ 2 years) |

| Migration to Android-based open-OS terminals and app stores | +1.5% | Global with early adoption in Indonesia, Thailand | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Expansion of Digital Payments Across Southeast Asia

Mobile wallets processed more transactions than traditional card networks in Indonesia, Thailand, and the Philippines during 2024, a shift that has amplified replacement cycles for multi-modal devices across the Southeast Asia POS Terminal market. QRIS in Indonesia alone logged more than 16 billion transactions, forcing merchants to ditch single-function card readers in favor of integrated QR/NFC units. Device makers now design terminals with omnichannel APIs, enabling unified reconciliation across storefront and delivery channels. Payment processors, in turn, preload value-added apps loyalty, inventory, BNPL to keep devices sticky over a five-year lifespan. The net effect is sustained double-digit hardware refresh demand, particularly from micro-merchants upgrading from paper or cash registers.

Government Cash-less Initiatives and E-payment Regulations

Malaysia’s e-Tunai Rakyat, Thailand’s PromptPay, and Indonesia’s SME subsidy schemes collectively inject thousands of subsidized terminals into the Southeast Asia POS Terminal market every quarter. Compliance clauses require certified NFC and EMV functionality, accelerating orders for mid-range Android models able to pass local security audits. Because subsidies often cover up-front hardware costs, vendors increasingly pivot to SaaS-based licensing that drives recurring revenue even after grants expire. Rural onboarding programs extend demand into second-tier cities, helping distributors expand beyond capital regions much faster than organic merchant acquisition would allow.

Rising Adoption of mPOS Among SMEs and Micro-merchants

Indonesia-based providers DealPOS and Qasir now serve a combined 500,000 merchants, proving portable readers can scale quickly within the Southeast Asia POS Terminal market ecosystem. Low monthly fees, bundled inventory modules, and simplified KYC have turned tablets into de-facto cash registers for kiosks, food trucks, and pop-up stalls. Hardware durability is less critical than battery life and LTE connectivity, leading suppliers to innovate around hot-swap batteries and rugged casings. Payment aggregators leverage this installed base to up-sell micro-loans, creating a virtuous circle where software-centric vendors outpace legacy hardware incumbents in customer stickiness.

Integration of BNPL Capabilities into POS Hardware

Visa’s Installment Solutions now resides inside several Android terminals sold across Singapore and Malaysia, enabling in-store installment offers without external middleware.[2]Visa, “Installment Solutions Platform,” visa.com Larger ticket retailers such as consumer electronics chains notice 15-20% upticks in average basket size, fueling merchant willingness to refresh to BNPL-ready units early in the lifecycle. Vendors differentiate by embedding instant credit scoring, often via API calls to fintech lenders, allowing approvals within seconds. The inclusion of BNPL workflows cements software as the chief battleground for feature updates, reinforcing a platform mindset throughout the Southeast Asia POS Terminal market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cyber-security and data-privacy vulnerabilities | -2.8% | Singapore, Malaysia leading security concerns, Indonesia following | Short term (≤ 2 years) |

| High total cost of ownership for modern POS devices | -2.1% | Philippines, Vietnam price-sensitive markets, Indonesia SME segment | Medium term (2-4 years) |

| Fragmented certification rules across SEA nations | -1.6% | Global impact with highest complexity in Malaysia, Thailand, Indonesia | Medium term (2-4 years) |

| Weak device-servicing networks beyond tier-1 cities | -1.3% | Indonesia, Philippines, Vietnam rural markets, Thailand secondary cities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cyber-security and Data-privacy Vulnerabilities

Bank Indonesia recorded a 45% jump in POS-linked fraud attempts during 2024, highlighting real-time threats that could stall new deployments if unaddressed. Malware that exploits outdated firmware spreads quickly once a single device is breached, prompting regulators to mandate over-the-air patch cycles. Smaller retailers, lacking IT staff, depend on vendors for security orchestration; when updates lag, risk-averse merchants defer purchases. Consequently, suppliers must bundle managed security services to keep the Southeast Asia POS Terminal market growth momentum intact.

High Total Cost of Ownership for Modern POS Devices

Modern contactless-enabled terminals often cost USD 1,500–3,000 upfront, plus USD 500–1,000 in yearly fees, a barrier for micro-merchants with thin margins. In the Philippines and Vietnam, traders prolong the life of mag-stripe readers until compelled by regulation to upgrade. Financing models such as hardware-as-a-service and revenue-share bundles are gaining traction, yet many small outlets still hesitate. Unless unit economics improve, price sensitivity could shave two full percentage points off the Southeast Asia POS Terminal market CAGR projection.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Mode of Payment Acceptance: Contactless Dominance Reshapes Terminal Architecture

Contactless payments controlled 56.97% revenue share within the Southeast Asia POS Terminal market in 2025, and the segment is forecast to widen at a 17.05% CAGR through 2031. That dominance positions tap-to-pay as the baseline capability for every new device SKU. Vendors now engineer antenna placement and screen prompts to accelerate sub-two-second checkouts, an attribute that merchants equate with higher throughput. QR fallback remains essential for low-value micro-merchant use cases, ensuring no consumer gets blocked by wallet preference.

Terminal makers are stripping mechanical card slots from entry-level units, dropping component costs while promoting SoftPOS for PIN-on-glass transactions. This evolution underlines how the Southeast Asia POS Terminal market size tied to contactless solutions will eclipse card-only hardware retirements by mid-decade. The push also drives telcos to bundle higher LTE data caps with mPOS subscriptions, reflecting traffic spikes from always-connected firmware updates and analytics pings.

By POS Type: Mobile Solutions Drive Market Transformation

Mobile and portable readers owned 46.25% of the Southeast Asia POS Terminal market in 2025 and are on track for a 16.7% CAGR through 2031. Street vendors, ride-hail drivers, and delivery couriers prefer belt-clip or smartphone-based units, which let them accept payment at customer doorsteps. Battery density improvements extend operating time to a full shift, eliminating power-bank dependence.

The Southeast Asia POS Terminal industry further amplifies mobility’s appeal by integrating barcode inventory apps and rider tracking dashboards on the same device, streamlining reconciliations. SUNMI’s decision to open repair hubs in Bangkok trims device downtime from weeks to days, a critical factor for cash-flow-sensitive SMEs. As more cloud POS platforms secure EMV Level 3 certification, fixed countertop hardware risks marginalization except in hyper-volume supermarkets.

By End-User Industry: Healthcare Emerges as Growth Engine

Retail accounted for 38.15% of the Southeast Asia POS Terminal market in 2025, but healthcare is projected to clock a 16.25% CAGR to 2031. Clinics and telemedicine platforms now demand terminals able to tokenize patient data while routing split payments among insurers, doctors, and labs. Such niche workflows push vendors into HIPAA-equivalent compliance builds, creating a specialized SKU tier.

This healthcare tilt also increases average selling prices, lifting overall Southeast Asia POS Terminal market size for clinical environments compared with standard retail. Further, pharmacies running consultation booths shell out for BCODE scanning to verify e-prescriptions, expanding attach rates for ancillary modules like label printers and biometric sensors.

Geography Analysis

Indonesia’s 29.55% revenue share anchors the Southeast Asia POS Terminal market, with a forecast 16.05% CAGR keeping it the region’s growth locomotive. Mandatory QRIS compliance triggers rapid swap-outs of legacy standalone card readers for code-scanning hybrids. Local certification norms favor vendors, with Jakarta labs able to test firmware against Bank Indonesia’s security checklists, leading global brands to seek domestic channel partners.

Secondary markets such as Thailand and Malaysia exhibit advanced feature adoption, think SoftPOS PIN entry and BNPL APIs, despite smaller absolute volumes. Singapore maintains record terminal density per capita, yet its mature status means replacement, not expansion, drives orders. The Philippines and Vietnam, home to vast unbanked populations, represent white-space opportunities where low-cost mobile form factors resonate.

Indonesia continues to set installation records, fueled by state subsidies that slash merchant onboarding fees and by telecom operators bundling SIM data plans with terminal leases. Java and Bali now near saturation, prompting distributors to push deeper into Sumatra and Kalimantan.

Thailand’s tourist-centric corridors witness accelerated upgrades to multilingual user interfaces, aligning with duty-free operators’ push to accept Chinese and European wallet schemes. Malaysia’s interoperable DuitNow QR ecosystem drives cross-industry pilots where the same terminal toggles between food-delivery settlements and utility bill collections.

Vietnam and the Philippines trail on per-capita device count but leapfrog in SoftPOS pilots, aided by cloud KYC flows that approve merchants in minutes. Urban migration patterns in Ho Chi Minh City and Manila heighten card-not-present fraud concerns, convincing regulators to expedite tokenized contactless rollouts. Cambodia, Laos, and Myanmar remain nascent yet poised to benefit once ASEAN connectivity cuts certification duplication costs.

Competitive Landscape

Global incumbents Worldline, Verifone, and PAX Technology still hold the lion’s share, propelled by deep distributor footprints and full EMV certification catalogs. Yet the Southeast Asia POS Terminal market now prizes software richness over hardware revision cadence. Fintech entrants like HitPay, NETS, and Qasir overlay cloud dashboards that merge payments, inventory, and micro-lending into one login, eroding hardware-only players’ pricing power

SoftPOS crystallizes this pivot. NETS’ January 2025 launch turned ordinary Android handsets into contactless readers for food-delivery riders and home-service technicians.[3]NETS, “SoftPOS Solution Launch,” nets.com.sg Once PCI CPoC standards mature locally, analysts expect sub-USD 100 smartphones to cannibalize low-end countertop sales, compressing gross margins but enlarging total acceptance points.

Despite rising competition, barriers persist. EMV Level 3 and PCI DSS certifications still require lab fees and audits that deter under-capitalized startups. Meanwhile, the ASEAN Payment Connectivity roadmap could homogenize specs, yet cybersecurity add-ons, AI-driven fraud scoring, and real-time key rotation become key differentiators, painting a picture of a Southeast Asia POS Terminal market where platform alliances outweigh isolated hardware upgrades.

Southeast Asia POS Terminal Industry Leaders

Verifone Systems LLC

PAX Technology Ltd.

NCR Corporation

Toshiba TEC Corporation

Newland Payment Technology Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: NETS launched SoftPOS in Singapore, letting smartphones accept contactless payments without extra hardware.

- December 2024: SUNMI opened Thai service centers offering local repair and software updates.

- November 2024: Verifone rolled out Victa Portable with enhanced NFC range for street vendors.

- October 2024: Bank Indonesia imposed stricter POS cybersecurity rules requiring real-time fraud monitoring.

Southeast Asia POS Terminal Market Report Scope

A POS terminal is a digital terminal that helps businesses complete sales transactions. It helps to store, capture, share, and report data related to sales transactions.

Southeast Asia POS Terminal Market is segmented by component (hardware, software, and services), type (fixed point of sale terminals and mobile/portable point of sale terminals), end-user industries (entertainment, hospitality, healthcare, and retail), and country (Singapore, Indonesia, Vietnam, Malaysia, and other Southeast Asian countries). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

By Mode of Payment Acceptance

| Contact-based |

| Contactless |

By POS Type

| Fixed Point-of-Sale Systems |

| Mobile / Portable Point-of-Sale Systems |

By End-User Industry

| Retail |

| Hospitality |

| Healthcare |

| Transportation and Logistics |

| Other End-User Industries |

By Country

| Singapore |

| Malaysia |

| Thailand |

| Indonesia |

| Philippines |

| Vietnam |

| Rest of Southeast Asia |

| By Mode of Payment Acceptance | Contact-based |

| Contactless | |

| By POS Type | Fixed Point-of-Sale Systems |

| Mobile / Portable Point-of-Sale Systems | |

| By End-User Industry | Retail |

| Hospitality | |

| Healthcare | |

| Transportation and Logistics | |

| Other End-User Industries | |

| By Country | Singapore |

| Malaysia | |

| Thailand | |

| Indonesia | |

| Philippines | |

| Vietnam | |

| Rest of Southeast Asia |

Key Questions Answered in the Report

How large is the Southeast Asia POS Terminal market in 2026?

The market is valued at USD 5.73 billion in 2026 and is projected to reach USD 11.8 billion by 2031 at a 15.55% CAGR.

Which country leads terminal deployment in the region?

Indonesia holds 29.55% revenue share and maintains the fastest expansion, supported by the nationwide QRIS mandate.

What segment grows fastest by end-user?

Healthcare posts a 16.25% CAGR to 2031 as clinics integrate real-time payment and patient-data workflows.

Why are merchants moving toward SoftPOS?

Smartphone-based acceptance cuts hardware costs, supports contactless payments, and allows rapid feature updates via app stores.

What is the biggest restraint to wider adoption?

High total cost of ownership, ranging from USD 1,500 to USD 3,000 upfront plus subscriptions, deters small merchants in price-sensitive markets.

Page last updated on: