Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

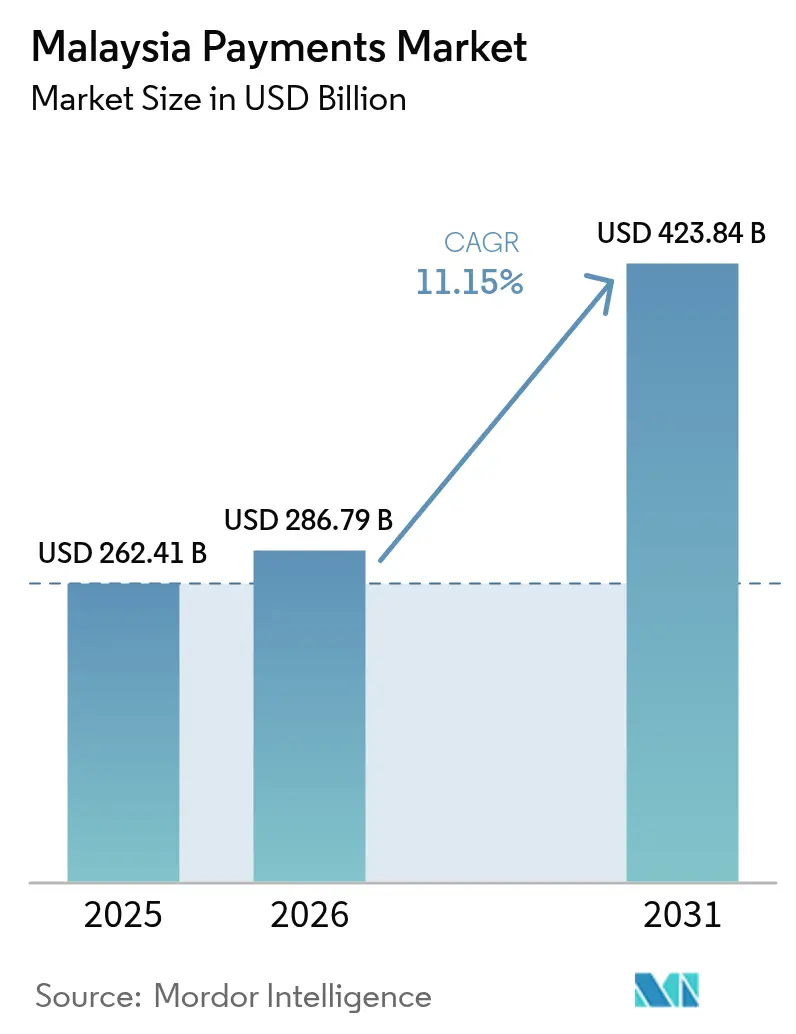

| Base Year Market Size (2025) | USD 262.41 Billion |

| Market Size (2026) | USD 286.79 Billion |

| Market Size (2031) | USD 423.84 Billion |

| Growth Rate (2026 - 2031) | 11.15% CAGR |

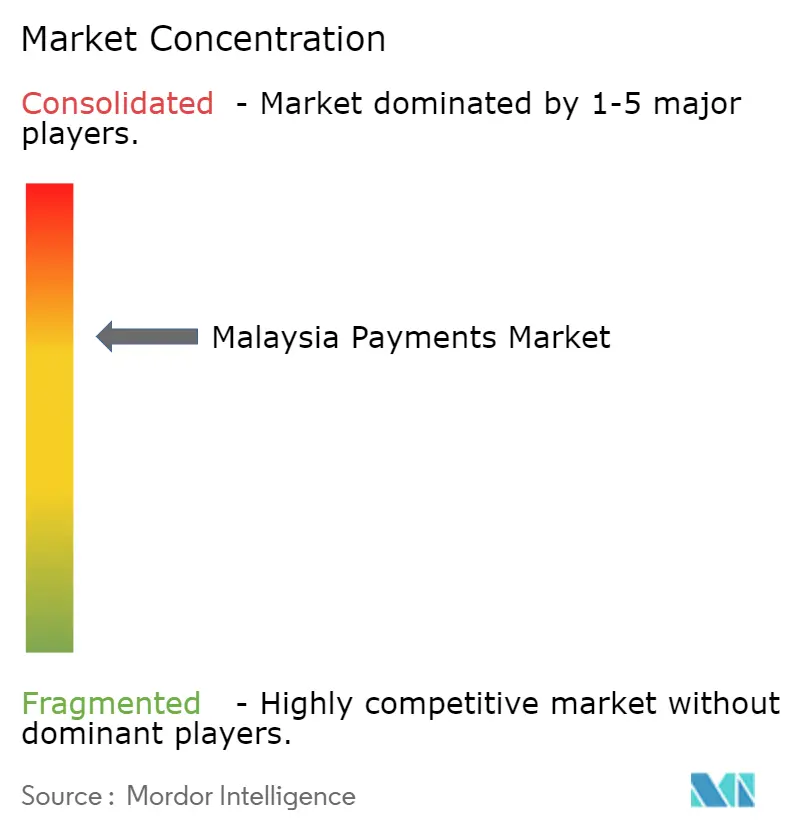

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Malaysia Payments Market Analysis by Mordor Intelligence

The Malaysia payments market size is projected to expand from USD 262.41 billion in 2025, USD 286.79 billion in 2026, and reach USD 423.84 billion by 2031, registering a CAGR of 8.13% during 2026-2031. Debit and credit cards still anchor physical retail, yet transaction value is tilting toward interoperable QR codes that compress interchange fees and toward real-time rails that promise instant settlement. The central bank’s DuitNow infrastructure has already connected millions of merchants, while ASEAN cross-border agreements let travelers scan a single code across Malaysia, Singapore, and Thailand. Islamic digital wallets, gig-economy payout demands, and government e-invoice rules are deepening wallet penetration, whereas persistent fraud and rural connectivity gaps temper adoption speed. Competitive pressure is migrating from fee-based card issuers to data-rich platform ecosystems that monetize payments through lending, insurance, and loyalty rather than pure interchange.

Key Report Takeaways

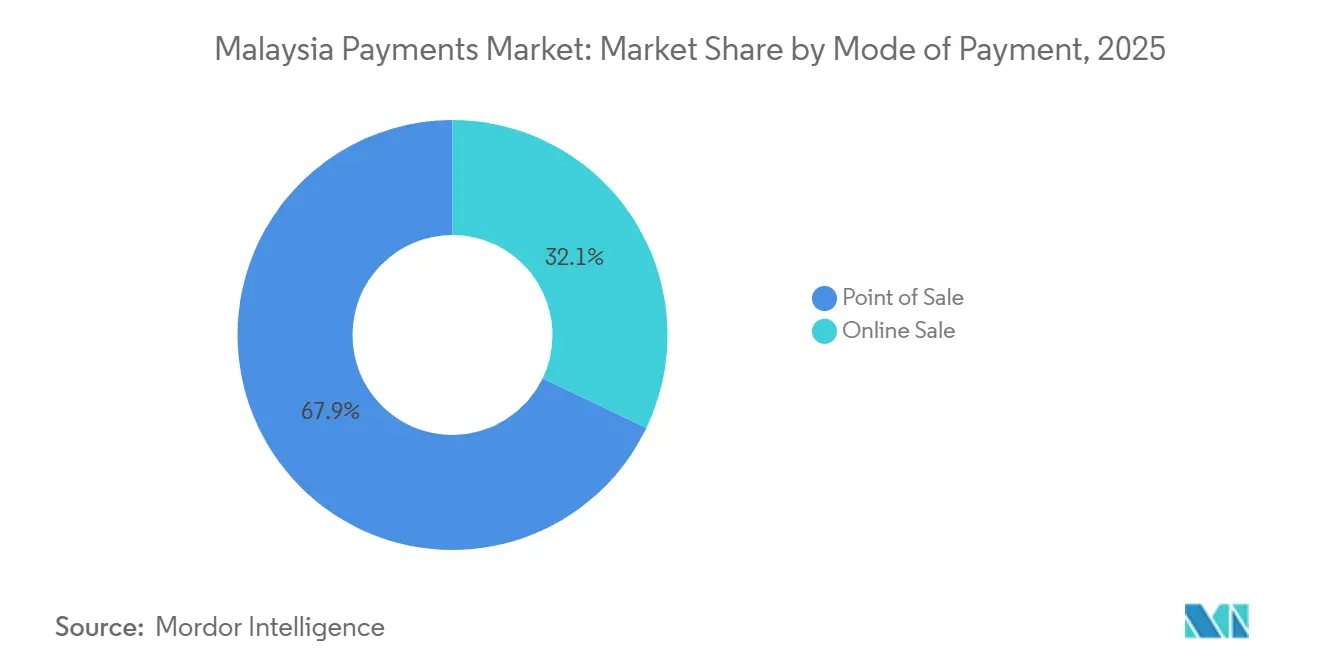

- By mode of payment, Point of Sale channels led with 67.89% of transaction value in 2025, while Online Sale channels are forecast to grow at a 10.13% CAGR to 2031.

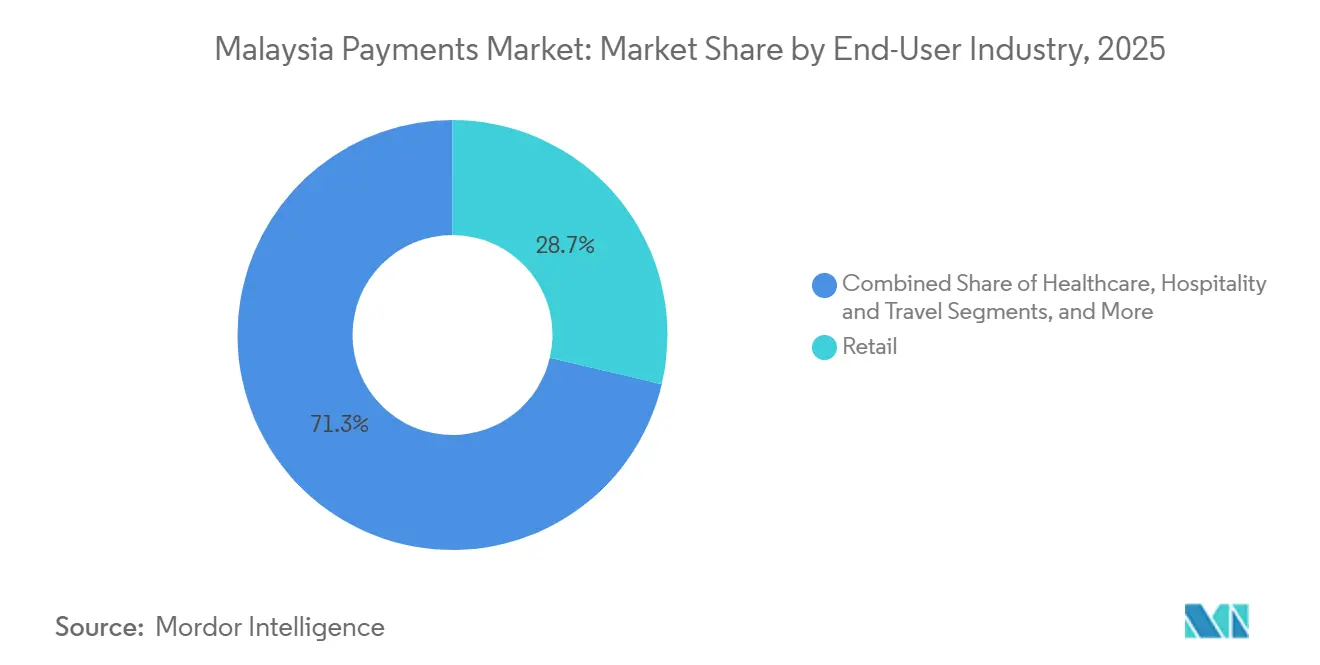

- By end-user industry, retail captured 28.67% of value in 2025, whereas hospitality and travel are advancing at an 11.24% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Malaysia Payments Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid E-Commerce Expansion and Mobile-Shopping Adoption | +1.8% | National, concentrated in Klang Valley, Penang, Johor Bahru | Medium term (2-4 years) |

| Government Push for Interoperable QR (DuitNow) and Contactless Cards | +1.5% | National, mandated by Bank Negara Malaysia | Short term (≤ 2 years) |

| Contactless Card Penetration and NFC Terminal Rollout | +1.2% | Kuala Lumpur, George Town, Johor Bahru | Short term (≤ 2 years) |

| Rise of Islamic Fintech and Sharia-Compliant Payment Propositions | +0.9% | States with higher Islamic banking penetration | Long term (≥ 4 years) |

| ASEAN Cross-Border E-Wallet Interoperability Initiatives | +0.7% | Malaysia-Singapore and Malaysia-Thailand corridors | Medium term (2-4 years) |

| Instant Payouts for Gig-Economy via Real-Time Rails | +0.6% | Klang Valley, Penang, Johor Bahru | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rapid E-Commerce Expansion and Mobile-Shopping Adoption

Smartphone penetration exceeded 90% in 2025, and super-apps such as Shopee and Lazada integrated one-tap wallet checkouts that bypass card-network fees.[1]Malaysian Communications and Multimedia Commission, “Hand Phone Users Survey 2025,” MCMC.GOV.MY Mobile-first buyers transact 40% more often than desktop users, improving merchant customer-acquisition economics. Touch 'n Go’s link-up with Grab’s ride-hailing and food-delivery services embeds payments inside daily routines, heightening platform stickiness. The phased e-invoice mandate pushes businesses to digitize invoices, indirectly nudging suppliers and buyers into online settlements.[2]Inland Revenue Board of Malaysia, “Implementation of E-Invoice in Malaysia,” HASIL.GOV.MY Cash-on-delivery is shrinking as prepaid digital wallets gain dispute-resolution credibility. If rural broadband roll-out under the Jendela plan slips behind schedule, the usage gap between urban and outstation shoppers could widen.

Government Push for Interoperable QR (DuitNow) and Contactless Cards

Bank Negara Malaysia requires all payment terminals to migrate to PIN authentication by June 2026, closing loopholes that enabled signature-based fraud.[3]Bank Negara Malaysia, “Payment Systems,” BNM.GOV.MY DuitNow QR unifies previously siloed wallet codes and has enrolled 2.6 million merchants, with volumes jumping 47% year-on-year in 2025. The George Town Accord among ASEAN central banks guarantees reciprocal QR acceptance, so Malaysian tourists buy meals in Bangkok with Touch 'n Go while avoiding foreign-exchange spreads. Tourism rebound, already at 85% of 2019 levels by mid-2025, accelerates QR adoption among hospitality merchants. Visa and Mastercard see card-present revenue erosion because flat-fee QR rails undercut percentage-based interchange models.

Contactless Card Penetration and NFC Terminal Rollout

Maybank and CIMB distributed 8 million contactless cards by end-2025, shrinking average supermarket checkout time from 45 seconds to 12 seconds. Touch 'n Go retrofit 6 million vehicles with RFID tags that double as wallet identifiers for tolls and parking.[4]Touch n Go, “Corporate Overview and Product Updates,” TOUCHNGO.COM.MY NFC readers now dominate Malaysia’s main transit and retail nodes, lowering the psychological barrier to mobile-tap payments. Samsung and Huawei preload wallets on devices sold through the country’s top telcos and achieve a 30% activation rate by mid-2025. A looming challenge is terminal-subsidy withdrawal once card-network interchange pools compress.

Rise of Islamic Fintech and Sharia-Compliant Payment Propositions

Islamic banking assets hit RM 1.2 trillion (USD 267.0 billion) in 2025, amounting to 39.5% of national banking Bank Islam Malaysia’s wallet automatically diverts zakat contributions, satisfying observant users’ faith obligations. Maybank Islamic structures buy-now-pay-later plans as murabaha contracts, side-stepping interest and gaining traction among 12 million MAE users. The Securities Commission approved Sharia-compliant crowdfunding portals that clear payments only through Islamic wallets. Foreign workers remit RM 30 billion (USD 6.7 billion) annually, and pilots such as Wahed’s gold-backed stablecoins promise faster, halal-compliant cross-border transfers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent Cash Preference Among SMEs and Rural Consumers | -0.8% | Rural Sabah, Sarawak, Interior Pahang, Kelantan | Long term (≥ 4 years) |

| Rising Fraud and Cybersecurity Concerns Lowering Trust | -0.6% | National, higher incidence in urban areas | Short term (≤ 2 years) |

| Fragmented Acquiring Market Keeps MDR High for Micro-Merchants | -0.4% | National, micro-enterprises | Medium term (2-4 years) |

| E-KYC Hurdles for Migrant and Foreign Workers | -0.3% | Klang Valley, Penang, Johor | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Persistent Cash Preference Among SMEs and Rural Consumers

Seventy percent of SMEs still prefer cash, citing tax-audit fears and liquidity needs. Sabah and Sarawak’s intermittent internet and aging demographics reinforce this behavior. The 2024 eBelia youth subsidy drove short-term wallet activation but post-incentive usage cratered, proving that handouts without merchant ubiquity lack staying power. QR pilots in wet markets faltered because 24-hour settlement cycles undermine vendors’ working capital. Until real-time payouts reach tier-three towns, cash maintains speed and trust advantages.

Rising Fraud and Cybersecurity Concerns Lowering Trust

Consumers lost MAR 1.51 billion (USD 335.0 million) to 51,020 scams in 2024, a 218% jump year-on-year. The National Scam Response Centre froze MAR 200 million (USD 44.4 million) of suspicious funds in six months, yet 42% of surveyed users said they dialed back wallet usage after hearing of fraud. Mandatory cooling-off periods and step-up biometrics mitigate risk but add friction. Gig-economy riders on shared smartphones experience rising credential theft, prompting Grab to deploy behavioral analytics at additional cost. Without continued investment in AI-driven detection, a trust spiral could undermine digital adoption.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Mode of Payment: Online Channels Capture Checkout Velocity as QR Codes Commoditize Point-of-Sale

Point of Sale methods accounted for 67.89% of value in 2025, supported by entrenched card habits in supermarkets, fuel pumps, and restaurants. Within this group debit cards remain dominant among salaried workers, while credit cards capture big-ticket discretionary spending through reward programs and flexible installment plans. Bank financing blends Islamic murabaha structures with conventional installment offers, appealing to consumers furnishing homes or buying electronics. Prepaid cards are losing utility to reloadable wallets that facilitate contactless transit and instant peer transfers. Digital wallets are the star turn, their growth amplified by DuitNow QR’s fee waivers that attract micro-merchants.

Online Sale channels, though smaller, are scaling at a 10.13% CAGR to 2031 as mobile-optimized checkouts eliminate form-fill friction. Cards still mediate roughly 60% of e-commerce value, yet their share is bleeding to wallets embedded inside Shopee and Lazada that avoid card-network tolls. Bank financing online supports zero-interest installment plans for mid-range smartphones and white goods, with Islamic variants expanding appeal. Prepaid cards see limited rotation because refund handling is clunky. Digital wallets dominate low-value, high-frequency orders such as food delivery, with Touch 'n Go boasting 82.41% of user penetration and Boost at 66.68%. Buy-now-pay-later products like BigPay Later funnel users who want budgeting discipline and interest-free spreading of payments.

By End-User Industry: Hospitality Outpaces Retail as Contactless Becomes Table Stakes

Retail captured 28.67% of transaction value in 2025, driven by supermarkets and convenience chains that now favor self-checkout kiosks and QR acceptance. Entertainment and digital content follows, as recurring billing for streaming and gaming locks users into monthly debits that reduce churn. Healthcare digitization remains piecemeal; the newly launched iPayment portal standardizes government-hospital charges but private clinics lag behind.

Hospitality and travel is the fastest-growing vertical, rising at an 11.24% CAGR toward 2031 thanks to recovering inbound tourism and widespread adoption of contactless check-ins and mobile room keys. Airlines embed wallet payments for baggage and seat upgrades, shaving cash handling at counters. Government and utilities migrate tax, water, and vehicle-license fees to the MyGovernment portal, yet older citizens and rural users still queue at brick-and-mortar offices. Miscellaneous categories, including education fees and charitable giving, test automated monthly debits, but consumer-protection rules on auto-renewals are still evolving.

Geography Analysis

Urban Malaysia drives digital adoption. The Klang Valley alone contributes roughly 45% of national transaction value as dense merchant networks, high smartphone penetration, and multinational payrolls reinforce cashless behavior. Penang and Johor Bahru together add another 20%, buoyed by cross-border QR spending with Singapore and Thailand. The ASEAN Payment Connectivity initiative, which cleared 12.9 million QR transactions in H1 2025, is most active in these border corridors.

Rural Sabah and Sarawak cover 60% of land mass yet generate barely 15% of payments value. Only 70% of populated areas enjoy reliable 4G, and bank branches are sparse. Broadband under the Jendela program promises 100 Mbps to 9 million premises, but mountainous interior districts remain unprofitable for fiber roll-out. Wet-market digitization pilots stumbled because settlement delays erode vendors’ liquidity. Until wallets work offline and offer same-day settlement, cash will keep its velocity and privacy appeal.

The East Coast states form a mixed picture. Urban centers such as Kuantan mirror Penang’s payment patterns, while rural hinterlands emulate Sabah’s cash preference. Youth-oriented eBelia subsidies posted 75% redemption in Kuala Lumpur but only 50% in Kelantan, signaling that merchant acceptance, not consumer willingness, is the bottleneck. Islamic wallet features, including zakat auto-deduct and halal merchant flags, resonate in these states. Migrant workers in Klang Valley factories and Penang tech parks remain an untapped segment because strict e-KYC rules bar onboarding without local IDs. Regulatory elasticity here could unlock a 5-7% boost in volume.

Competitive Landscape

The Malaysia payments market exhibits moderate concentration, with no single player exceeding 20% value share, but leadership hinges on ecosystem breadth rather than pure payments functionality. Touch 'n Go wields a multimodal moat across highways, parking, and mass transit that delivers 15 million active users and granular mobility data. Maybank’s MAE leverages 2,400 physical branches and corporate payroll ties to cross-sell wealth and insurance products, monetizing insights harvested from 12 million wallet users. Visa, Mastercard, and UnionPay defend relevance through co-branded cards and loyalty, yet flat-fee QR rails dilute their interchange margin.

White-space opportunities persist. Roughly 2.4 million foreign workers remain outside mainstream wallets because document checks fail. BigPay courts them with low-cost remittance corridors that undercut Western Union fees. Razer Merchant Services, by integrating Alipay+ across 60,000 terminals, aims squarely at rebounding Chinese tourist spend. Embedded-finance challengers such as Shopee and Lazada are pursuing digital bank licenses to lock users into a unified commerce-lending-payment loop. Technology sophistication is varied: tier-one players deploy AI-driven fraud detection, yet smaller gateways cling to rule-based filters that frustrate merchants through false positives.

Regulation influences trajectories. Bank Negara Malaysia’s five digital bank licensees, including Sea Group and Grab, must meet capital and consumer-protection thresholds that could temper disruptive pace. Mandatory PIN authentication from June 2026 will squeeze acquirers that postpone EMV upgrades. As card-present volume shifts to QR, fee pools thin and acquirers scramble for ancillary revenue such as data analytics and lending.

Malaysia Payments Industry Leaders

Ipay88 (m) Sdn Bhd

United overseas bank (Malaysia) Bhd

Malayan Banking Berhad (Maybank)

CIMB Group Holdings Berhad

PayPal Holdings, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: UnionPay International completed deployment of 10,000 additional QR-capable terminals, expanding total Malaysian acceptance points to 110,000.

- April 2025: Google Pay integrated ShopeePay and Touch ’n Go eWallet for Android users in Malaysia, enabling seamless checkout experiences through mobile Chrome with initial merchant rollout including Nando’s, US Pizza and Alpro Pharmacy The Paypers.

- April 2025: UOB Malaysia introduced UOB Infinity, a real-time cross-border payment tracking platform providing corporate clients with instant notifications, transparent fee visibility and multi-market cash flow management The Edge Malaysia.

- April 2025: Capital A announced plans to sell a majority stake in BigPay to an undisclosed regional bank while retaining approximately 30% ownership, with BigPay serving over 1.6 million cardholders as of end-2024 The Edge Malaysia.

Malaysia Payments Market Report Scope

Payments are voluntary transfer of funds, equivalent, or other valuable items from one person to another in exchange for goods and services received or satisfying an obligation under the law.

The Malaysia Payments Market Report is Segmented by Mode of Payment (Point of Sale - Card Payments, Bank Financing, Prepaid Cards, Digital Wallets, Other; Online Sale - Card Payments, Bank Financing, Prepaid Cards, Digital Wallets, Other Online Sales), End-User Industry (Retail, Entertainment and Digital Content, Healthcare, Hospitality and Travel, Government and Utilities, Other), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

By Mode of Payment

| Point of Sale | Card Payments | Debit Cards |

| Credit Cards | ||

| Bank Financing Prepaid Cards | ||

| Digital Wallets (includes Mobile Wallet) | ||

| Other Point of Sale | ||

| Online Sale | Card Payments | Debit Cards |

| Credit Cards | ||

| Bank Financing Prepaid Cards | ||

| Digital Wallets | ||

| Other Online Sales (includes Cash on Delivery, Bank Transfer, and Buy Now Pay Later) |

By End-User Industry

| Retail |

| Entertainment and Digital Content |

| Healthcare |

| Hospitality and Travel |

| Government and Utilities |

| Other End-User Industries |

| By Mode of Payment | Point of Sale | Card Payments | Debit Cards |

| Credit Cards | |||

| Bank Financing Prepaid Cards | |||

| Digital Wallets (includes Mobile Wallet) | |||

| Other Point of Sale | |||

| Online Sale | Card Payments | Debit Cards | |

| Credit Cards | |||

| Bank Financing Prepaid Cards | |||

| Digital Wallets | |||

| Other Online Sales (includes Cash on Delivery, Bank Transfer, and Buy Now Pay Later) | |||

| By End-User Industry | Retail | ||

| Entertainment and Digital Content | |||

| Healthcare | |||

| Hospitality and Travel | |||

| Government and Utilities | |||

| Other End-User Industries | |||

Key Questions Answered in the Report

How large is the Malaysia payments market in 2026?

The Malaysia payments market size is expected to reach USD 286.79 billion in 2026, on its way to USD 423.84 billion by 2031.

What is the projected growth rate through 2031?

The market is forecast to register an 8.13% CAGR between 2026 and 2031.

Which payment mode is growing fastest online?

Digital wallets embedded in super-apps are expanding online transaction value at a 10.13% CAGR, displacing cards for low-value, high-frequency purchases.

Which industry segment shows the strongest growth?

Hospitality and travel is advancing at an 11.24% CAGR as hotels and airlines adopt contactless and in-app payment flows.

How is fraud affecting user trust?

Financial scams cost consumers USD 335 million in 2024, prompting stricter authentication rules and influencing 42% of surveyed users to reduce wallet usage.

What role does Islamic fintech play?

Sharia-compliant wallets offer zakat automation and riba-free installment plans, capturing a share of the RM 1.2 trillion Islamic banking pool and attracting faith-driven consumers.

Page last updated on: