Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

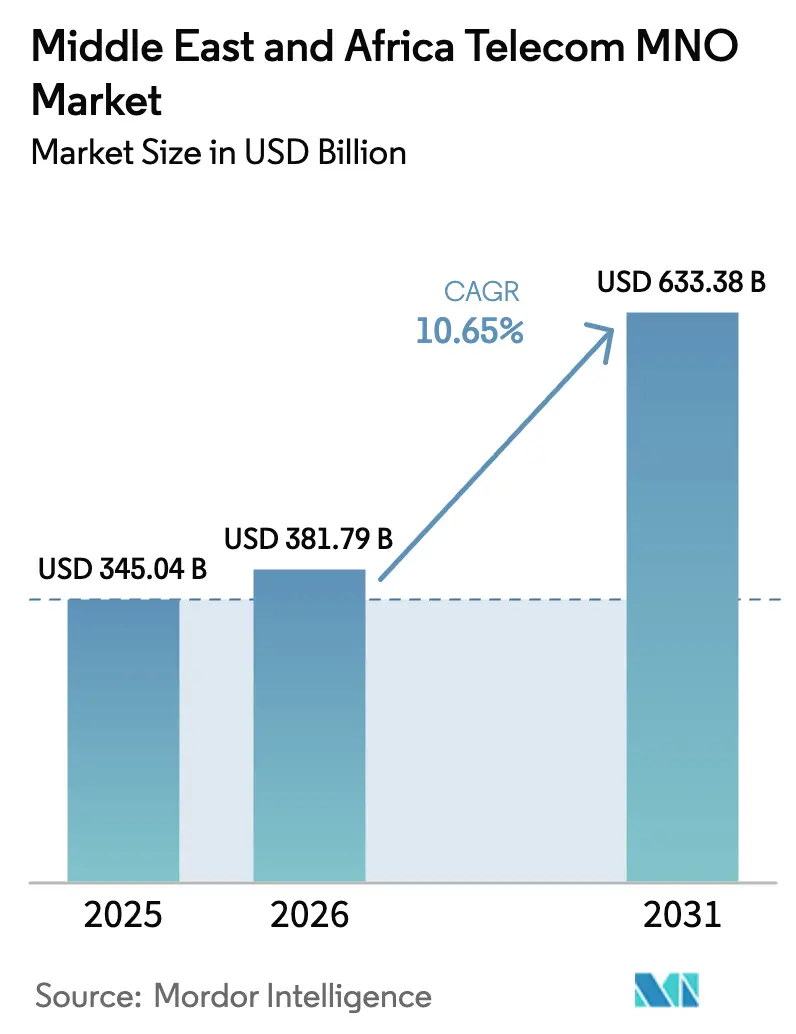

| Base Year Market Size (2025) | USD 345.04 Billion |

| Market Size (2026) | USD 381.79 Billion |

| Market Size (2031) | USD 633.38 Billion |

| Growth Rate (2026 - 2031) | 10.65% CAGR |

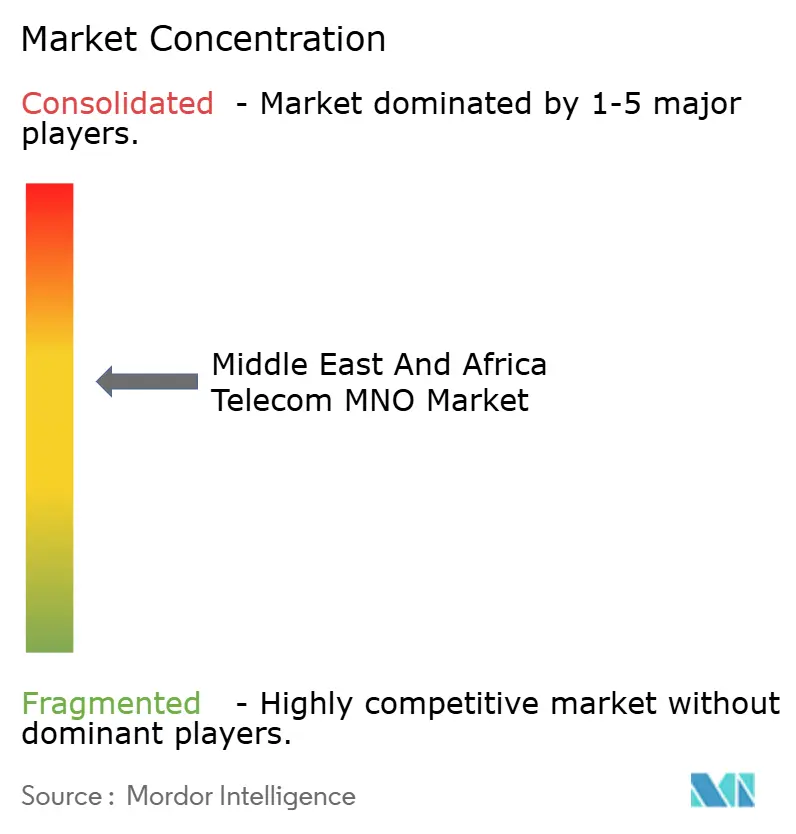

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle East And Africa Telecom MNO Market Analysis by Mordor Intelligence

Middle East And Africa Telecom MNO Market size in 2026 is estimated at USD 381.79 billion, growing from 2025 value of USD 345.04 billion with 2031 projections showing USD 633.38 billion, growing at 10.65% CAGR over 2026-2031.

Rapid 5G deployments, expanding fiber backhaul, and rising smartphone penetration combine to keep the region on a structurally high-growth trajectory. Investment intensity remains elevated: Egypt paid USD 150 million for its first 5G license, while Saudi Arabia pushed 5G Fixed Wireless Access (FWA) to 78% population coverage in 2025. Morocco committed USD 475 million to reach 25% 5G coverage by end-2025, underscoring a broad policy focus on next-generation access. Competitive pressure from low-earth-orbit (LEO) satellite broadband and geopolitical risks around the Red Sea cable corridor temper sentiment, but are offset by enterprise digitalization and mobile-money-driven ARPU gains.

Key Report Takeaways

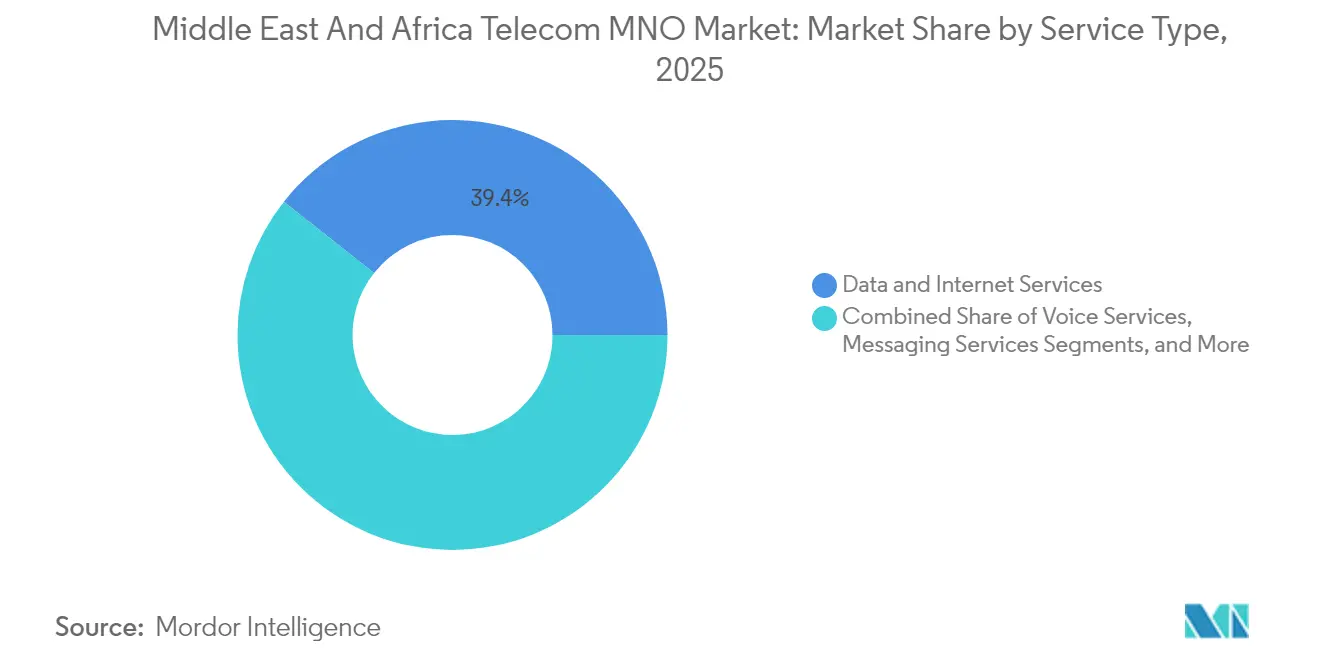

- By service type, data and Internet services held 39.35% of the Middle East and Africa telecom MNO market share in 2025; IoT and M2M services are projected to expand at a 10.74% CAGR between 2026 and 2031, the fastest growth among service categories.

- By end-user, consumer connections contributed 72.95% revenue in 2025, while enterprise subscriptions are poised for an 11.05% CAGR through 2031.

- By geography, the Middle East commanded 52.10% revenue share in 2025; Africa is advancing at a 10.70% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Middle East And Africa Telecom MNO Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Video-centric mobile data boom | +2.8% | Gulf cities, Cairo, Johannesburg | Short term (≤ 2 years) |

| Supportive spectrum auctions for 4G/5G | +2.1% | Saudi Arabia, UAE, North Africa | Medium term (2-4 years) |

| Enterprise IoT/M2M adoption | +1.9% | UAE, South Africa, Nigeria | Medium term (2-4 years) |

| Youth-led smartphone uptake | +1.7% | Nigeria, Kenya, Tanzania | Long term (≥ 4 years) |

| Cross-border mobile-money use | +1.4% | Kenya–Gulf, West Africa corridors | Medium term (2-4 years) |

| Private 5G for mega-projects | +1.3% | UAE, Saudi giga cities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Explosive growth in mobile data traffic from video-centric apps

Video viewing reshapes operator revenue architecture as users pivot from voice and SMS to high-definition streaming. SMS revenue in the Gulf fell from USD 4.3 billion in 2013 to a projected USD 3.2 billion in 2018, while mobile data volumes rose 180% in the same span [1]Ben Flanagan, “RIP, SMS? Text Messaging on Decline in Mideast,” Alarabiya.net. Operators respond by densifying 5G small cells; the MENA small-cell market is projected to reach USD 412.54 million by 2030, a 40.9% CAGR [2]ABN Newswire, “MENA Small Cell 5G Network Market Set to Experience Considerable Growth in 2030,” Abnnewswire.net. FWA subscriptions, priced near USD 70 each month, monetize in-home streaming traffic without fresh fiber builds. Network planners now weigh the cost of massive-MIMO upgrades against the rising willingness of premium users to pay for gigabit packages. In Sub-Saharan Africa, monthly data usage is forecast to triple to 14 GB per user by 2030, demanding parallel investment in both spectrum and backhaul.

Accelerated 4G and 5G roll-outs enabled by supportive spectrum auctions

Regulators across the Gulf and North Africa now favor coverage targets over windfall auction fees. Saudi Arabia’s 2025-2027 Spectrum Outlook sets aside new bands for non-terrestrial networks and FWA via light licensing, slashing time-to-market for operators. South Africa’s draft 2025 National Radio Frequency Plan similarly carves out dedicated private-network spectrum that encourages industrial 5G [3]Lexi Parvin, “South Africa: ICASA Releases Draft National Radio Frequency Plan 2025,” Globalvalidity.com. The UAE already operates 7,000 5G sites, with a policy aiming for 500 on-campus private networks by 2025. Concurrent 2G/3G switch-offs in Bahrain, Jordan, Kuwait, and Saudi Arabia release low-band spectrum for 5G, further boosting spectral efficiency. The collective result is faster rural broadband coverage and lower per-bit delivery cost, crucial for sustaining the Middle East and Africa telecom MNO market’s profit pool.

Enterprise digitization fueling IoT/M2M connectivity demand

Industrial players demand deterministic latency and on-site data sovereignty, propelling private LTE/5G investment that will top USD 6 billion by 2027, with 60% earmarked for standalone 5G cores. e& built what it calls the world’s largest private 5G network for ADNOC, validating the business case for high-volume, low-latency industrial connectivity. Verticals such as mining, oil and gas, and utilities rely on network slicing to segregate mission-critical traffic. The rise of Network-as-a-Service platforms lowers capex thresholds, enabling mid-tier enterprises and smart-city authorities to order pay-as-they-grow connectivity. As these use cases scale, IoT SIM activations accrue directly to the Middle East and Africa telecom MNO market.

Youth-driven smartphone adoption across Sub-Saharan Africa

Africa’s median age of 19.7 years supports a long runway for first-time smartphone ownership. Devices in use will grow from 540 million in 2024 to 890 million by 2030, and average monthly data per user will triple to 14 GB. Backhaul remains the key bottleneck: 584 million people already live within reach of fiber nodes, but many landlocked states still lack affordable middle-mile routes. Governments that streamline rights-of-way and import duties, such as Côte d’Ivoire, are rewarded with 23.8 Mbps median 4G speeds that stimulate further device adoption [4]Karim Yaici, “Government and Regulatory Support Is Key to Improving 4G Performance in Africa,” Ookla.com. Youth cohorts also embrace mobile wallets, deepening operator relevance in daily commerce and raising blended ARPU.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price competition plus SIM registration | −1.8% | Ghana, Kenya, South Africa | Short term (≤ 2 years) |

| Geopolitical instability | −1.2% | Red Sea corridor, Sahel, Gaza | Medium term (2-4 years) |

| LEO satellite substitution | −0.9% | Rural Nigeria, remote Oman | Long term (≥ 4 years) |

| Limited fiber backhaul | −0.7% | Chad, Central African Republic | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Aggressive price competition and SIM registration curbing ARPU

Mandatory biometric SIM registration raises compliance costs even as new entrants trigger price wars in markets like Kenya and Ghana. Inflation adds a second squeeze by eroding consumer spend capacity, while regulators cap tariff hikes to protect households. Operators counter with content bundles and loyalty apps, but execution is uneven in fragmented regulatory environments, restraining monetization in the Middle East and Africa telecom MNO market.

Geopolitical instability delaying infrastructure investment

The February 2024 Red Sea cable cut disrupted connectivity for more than 100 million users and forced rerouting of traffic, underscoring the vulnerability of a region that handles up to 17% of the world’s Internet flows. Capital-intensive projects such as new landing stations face financing delays when conflict risk rises, slowing coverage expansion in Yemen, Sudan, and Ethiopia. To mitigate single points of failure, investors now insist on dual-path designs and on-shoring of key equipment, measures that add cost and extend build timelines.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Data services consolidate revenue leadership

Data and Internet plans accounted for 39.35% of 2025 revenue, making them the single largest contributor to the Middle East and Africa telecom MNO market. IoT/M2M is the standout, expanding at a CAGR of 10.74% in the Middle East and Africa telecom MNO market size by 2031. Voice and messaging together will slip below 25% as OTT platforms cannibalize usage. Operators respond by zero-rating video services and bundling PayTV to sustain stickiness. Edge computing nodes and API monetization emerge as adjacent revenue streams that complement data plans.

Over the forecast horizon, Apps-as-a-Service models will lean on 5G standalone cores, opening low-latency use cases in gaming and telemedicine. Roaming and wholesale traffic, once cyclical, stabilize as intra-Africa trade flows broaden. Average data pricing will continue its southward drift but remain offset by strong volume elasticity, supporting the Middle East and Africa telecom MNO market size expansion.

By End-User: Enterprise acceleration chips away at consumer dominance

Consumers still delivered 72.95% of 2025 revenue, but their share will dip by 2031 as enterprises ramp dedicated networks. The enterprise slice of the Middle East and Africa telecom MNO market size is projected to reach 11.05% CAGR by 2031. Manufacturing, oil and gas, and logistics drive demand for low-latency connectivity and deep indoor coverage. Private 5G proofs-of-concept in Saudi giga-projects and South African mines validate willingness to pay premiums of 2-2.5× consumer ARPU.

In parallel, consumer growth is fueled by smartphone affordability. Sub-USD 60 handsets now support 4G, widening the addressable base. Mobile-money interoperability, live across 28 African markets, has raised average user spend from USD 2.2 to USD 3.2 per month, cushioning the Middle East and Africa telecom MNO market against unit price erosion.

Geography Analysis

The Middle East delivered 52.10% of revenue in 2025 on the back of higher ARPU; Saudi postpaid averages USD 34 per month. Operators leverage extensive fiberized towers and dense small-cell overlays to upsell premium FWA packages, ensuring the Middle East and Africa telecom MNO market share of the sub-region remains robust. Africa delivers the fastest 10.70% CAGR. Nigeria, Kenya, and South Africa account for two-thirds of sub-Saharan data traffic, yet large white spaces persist in the Sahel and Central Africa, preserving long-term upside.

Forecast models show that by 2031, Africa will contribute 49.20% of the Middle East and Africa telecom MNO market size, nearly closing the gap with the Gulf. North Africa acts as a swing region: Egypt’s USD 150 million 5G license and Morocco’s 25% coverage target illustrate rapid modernization trajectories that pull average regional speeds upward.

Competitive Landscape

Competitive intensity is bifurcated. Gulf markets remain oligopolistic: STC, e&, and Ooredoo together hold a significant share of regional revenue, allowing scale efficiencies. Africa is more fragmented, with over 230 licensed operators. Consolidation is accelerating; STC gained regulatory clearance for a Public Investment Fund purchase that deepens domestic integration and frees capital for cross-border expansion. Vodacom and Orange are evaluating infrastructure-sharing in multiple African markets to cut duplicated capex and speed rural rollouts.

Technology strategies differ by market maturity. Gulf incumbents deploy AI for predictive maintenance and launch open API platforms via the GSMA Open Gateway initiative, an effort e& joined through a strategic stake in Aduna. African challengers focus on cash-generating mobile-money ecosystems; Safaricom’s M-Pesa clone partnerships now span 12 markets. Private 5G is a new battleground: Nokia, Ericsson, and Huawei are chasing contracts in mining, ports, and petrochemicals with solutions already live or in trial across Saudi gigaprojects and South African platinum pits. LEO operators upend rural economics; traditional MNOs counter with hybrid satellite-cellular bundles to retain subscribers.

Regulatory acceptance of in-market mergers has loosened. The number of consumer-facing brands is expected to fall by 15% through 2027 as spectrum scarcity encourages rationalization. Despite this, entry barriers remain modest for virtual operators focused on diaspora voice and fintech-adjacent niches, preserving innovation dynamics within the Middle East and Africa telecom MNO market.

Middle East And Africa Telecom MNO Industry Leaders

eand (Etisalat Group)

MTN Group

STC Group

Zain Group

Vodacom Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Telecom Egypt and Orange Egypt signed EGP 15 billion (USD 306 million) multi-year transmission and fiber-to-site agreements that underpin nationwide 5G rollout.

- October 2024: STC Group and Ooredoo Group agreed to co-develop digital-service platforms targeting smart-city and cloud markets across MENA.

- August 2024: Liquid Intelligent Technologies secured exclusive rights to sell Globalstar XCOM RAN private-network solutions across Africa and the Gulf, broadening enterprise 5G choice.

- July 2024: Saudi Arabia’s Public Investment Fund received STC shareholder approval to acquire a controlling stake in a domestic telecom subsidiary, signaling deeper sector consolidation.

Middle East And Africa Telecom MNO Market Report Scope

The study tracks the telecom industry in the Middle East, with detailed coverage of the underlying market trends, subscriber base, revenues, and vendor operations. The major segments covered in the study include fixed-line services, mobile services, broadband services, and upcoming areas such as IoT & M2M in the region.

The Middle East and Africa telecom market is segmented by type (Mobile, Fixed Line, and Broadband) and by geography.

Service Type

| Voice Services |

| Data and Internet Services |

| Messaging Services |

| IoT and M2M Services |

| OTT and PayTV Services |

| Other Services (VAS, Roaming, Enterprise and Wholesale, etc.) |

End-user

| Enterprises |

| Consumer |

Geography

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of the Middle East (Qatar, Kuwait, Bahrain, Oman, Jordan, Iraq, Lebanon, Israel, and Others) | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa (Egypt, Morocco, Algeria, Tunisia, Ghana, Tanzania, Senegal, Ethiopia, Uganda, Kenya, and Others) |

| Service Type | Voice Services | |

| Data and Internet Services | ||

| Messaging Services | ||

| IoT and M2M Services | ||

| OTT and PayTV Services | ||

| Other Services (VAS, Roaming, Enterprise and Wholesale, etc.) | ||

| End-user | Enterprises | |

| Consumer | ||

| Geography | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of the Middle East (Qatar, Kuwait, Bahrain, Oman, Jordan, Iraq, Lebanon, Israel, and Others) | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa (Egypt, Morocco, Algeria, Tunisia, Ghana, Tanzania, Senegal, Ethiopia, Uganda, Kenya, and Others) | ||

Key Questions Answered in the Report

How large is the Middle East and Africa telecom MNO market in 2026?

It stands at USD 381.79 billion, with a projected rise to USD 633.38 billion by 2031.

Which service category leads regional revenue?

Data and Internet plans generate 39.35% of total revenue, far ahead of voice and messaging.

What CAGR is expected for IoT/M2M lines?

IoT and M2M connections are projected to grow at 10.74% CAGR through 2031, the fastest among all segments.

Which geography is growing quickest?

Africa is forecast to expand at a 10.70% CAGR as youth-driven smartphone adoption accelerates.

How will private 5G influence enterprise spending?

Private 5G networks are unlocking new industrial automation use cases and are expected to lift enterprise revenue to more than USD 190 billion by 2031.

What competitive threat do LEO satellites pose?

LEO services such as Starlink already serve rural customers in 18 African nations, pressuring MNOs to refine rural pricing and bundle strategies.

Page last updated on: