South Korea Telecom Tower Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

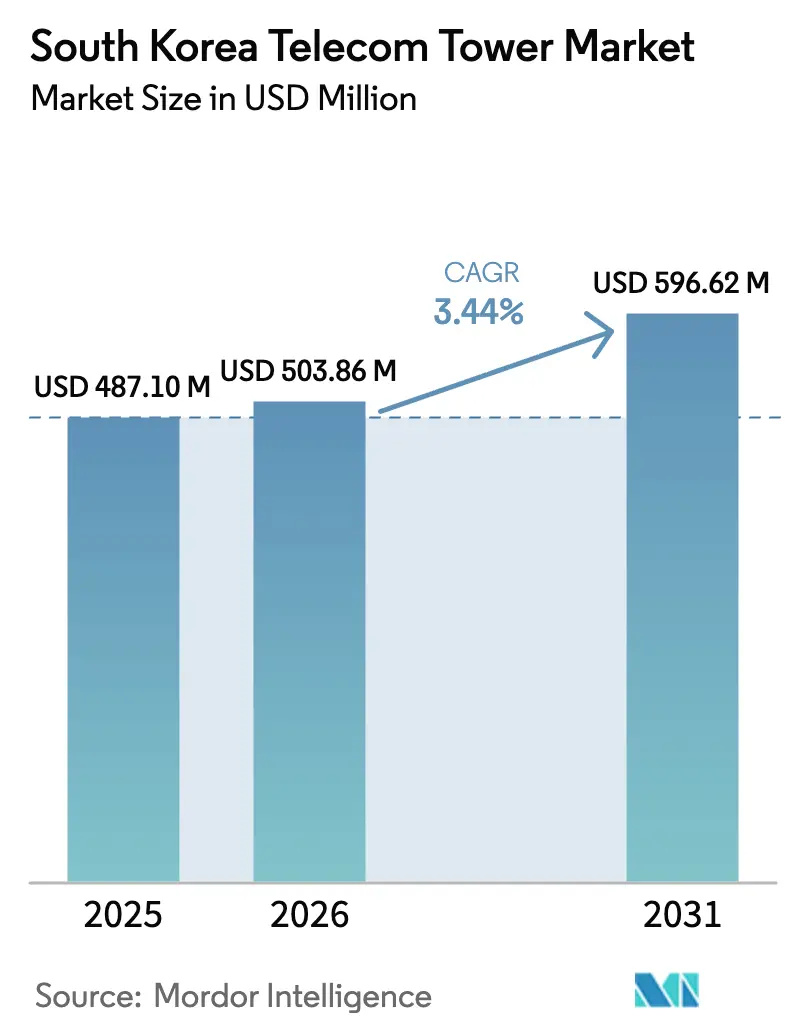

| Base Year Market Size (2025) | USD 487.10 Million |

| Market Size (2026) | USD 503.86 Million |

| Market Size (2031) | USD 596.62 Million |

| Growth Rate (2026 - 2031) | 3.44% CAGR |

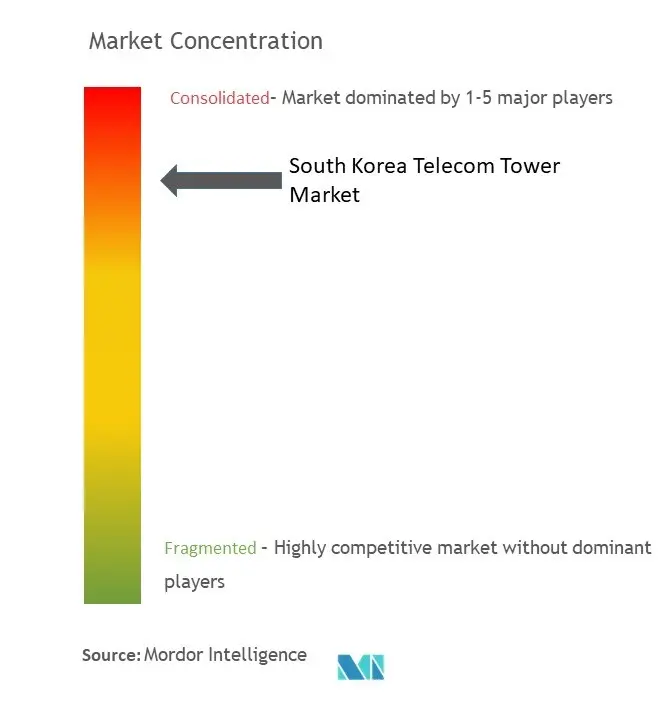

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Korea Telecom Tower Market Analysis by Mordor Intelligence

The South Korea Telecom Tower Market size in 2026 is estimated at USD 503.86 million, growing from 2025 value of USD 487.10 million with 2031 projections showing USD 596.62 million, growing at 3.44% CAGR over 2026-2031.

Current growth momentum is moderating as aggressive 5 G roll-outs shift toward densification and optimization phases, yet tower demand remains underpinned by a world-leading density of 419 5 G base stations per 100,000 inhabitants. Private-network expansion, rural coverage mandates, and renewable-energy retrofits collectively reinforce a medium-term growth runway, while regulatory actions—most notably the 10% tenancy-fee cap introduced in 2024—compress revenue yields and sharpen the industry’s focus on operating efficiency. New revenue pockets are emerging from industrial private 5 G sites, neutral-host indoor systems, and edge-computing nodes that often co-locate on existing structures. Competitive dynamics revolve around three incumbent mobile network operators (MNOs) that increasingly monetize assets via tower-company partnerships even as they divert capital toward AI data centers and quantum-secure networks. Risks to the demand outlook include potential contraction of millimeter-wave investments following the 28 GHz license revocations, rising land-lease renewals, and fiber-first backhaul preferences in Seoul-Busan corridors.

Key Report Takeaways

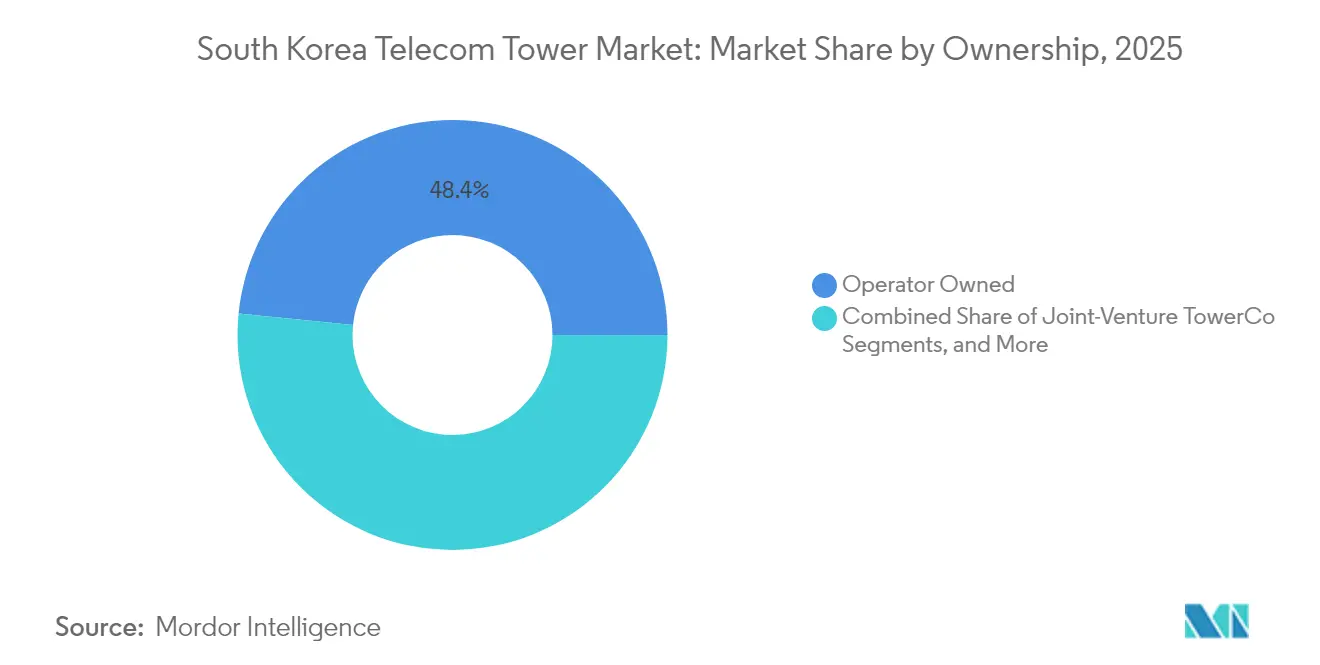

- By ownership, the operator-owned segment led with 48.41% of the South Korea telecom towers market share in 2025; independent tower companies are projected to expand at a 6.18% CAGR through 2031.

- By installation, ground-based sites held 53.78% share of the South Korea telecom towers market size in 2025, whereas rooftop sites are advancing at a 11.87% CAGR to 2031.

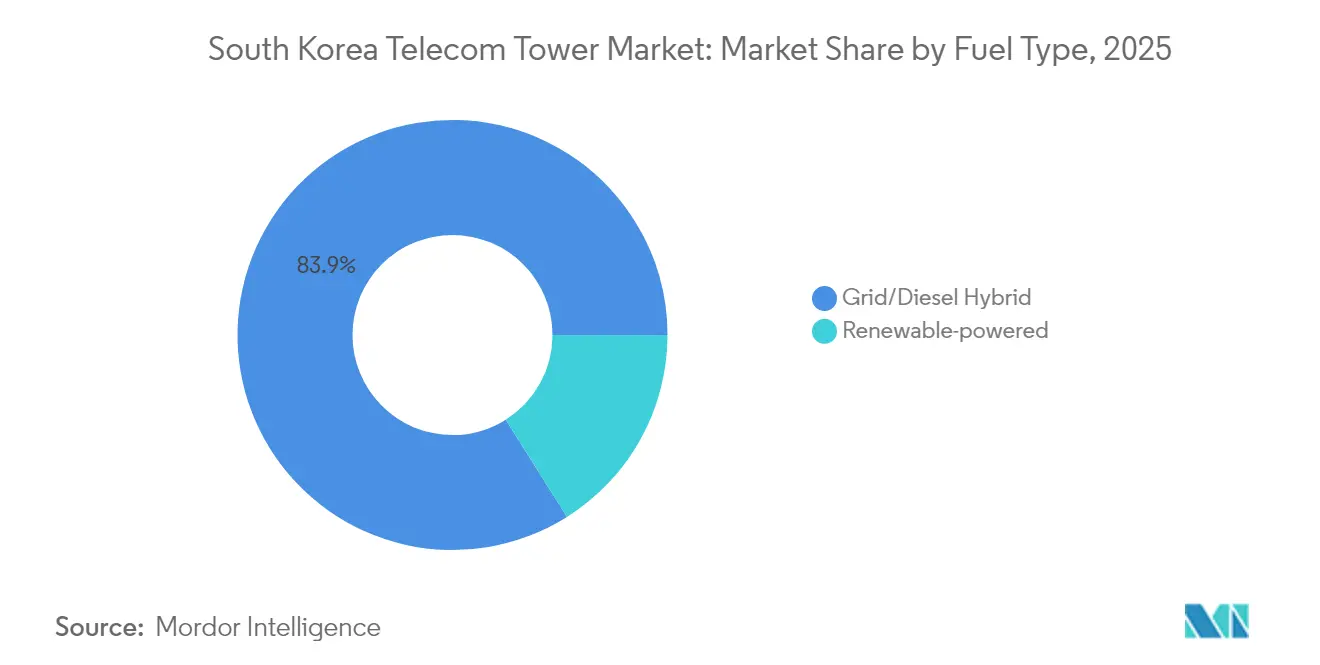

- By fuel type, grid/diesel hybrid systems accounted for 83.94% share of the South Korea telecom towers market size in 2025; renewable-powered sites are growing at a 7.34% CAGR over the forecast period.

- By tower type, monopoles captured 44.96% of the South Korea telecom towers market share in 2025, while stealth/concealed designs post the fastest CAGR at 4.96% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

South Korea Telecom Tower Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| 5 G SA densification mandates (3.5 GHz & 28 GHz) | +1.2% | National; Seoul–Busan corridor | Medium term (2–4 years) |

| Rural network-sharing JV “One Network” | +0.8% | Countrywide rural & suburban areas | Long term (≥ 4 years) |

| 26,000+ private-5 G licenses for smart factories | +0.9% | Industrial zones | Medium term (2–4 years) |

| Grid-tied solar-hybrid retrofit subsidies | +0.4% | Remote & rural sites | Long term (≥ 4 years) |

| E-band (80 GHz) backhaul liberalization | +0.3% | Urban & suburban areas | Short term (≤ 2 years) |

| Neutral-host indoor DAS tax credits | +0.2% | Major metropolitan buildings | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

5G SA Densification Mandates Drive Urban Infrastructure Expansion

Dense standalone 5 G requirements across 3.5 GHz and 28 GHz frequencies compel operators to add more macro and small-cell sites in urban cores. Average nationwide 5 G download speeds reached 1,025.52 Mbps in 2024, up 9.2% year over year, yet rural speeds lag at 645.70 Mbps. Regulatory quality-of-service thresholds obligate continuous coverage upgrades, which in turn sustain demand for monopole structures, rooftop nodes, and distributed-antenna systems. Faster permitting cycles favor monopoles because they minimize visual impact and footprint, particularly in Seoul’s high-density districts. This driver also boosts ancillary demand for power-saving radios and AI-assisted optimization modules that can retrofit onto existing towers. Network planners increasingly blend macro-towers with micro-cells to balance capacity and coverage, catalyzing additional tenancy opportunities for tower owners.

Rural Network-Sharing Cost-Offset Schemes Enable Coverage Extension

The “One Network” joint venture allows MNOs to co-invest and co-operate sites in sparsely populated regions, lowering per-site economics that would otherwise be prohibitive. Mountainous terrain covering roughly 70% of the country elevates build-out costs, so shared passive infrastructure mitigates both capex and opex. The scheme dovetails with government digital-equality targets that demand near-ubiquitous 5G reach. Long-term cost recovery is further improved because shared towers often qualify for renewable-energy grants, which alleviate diesel reliance at remote sites. Collaboration in rural areas also frees capital for competitive service differentiation in urban centers without jeopardizing universal-service compliance. Over time, this partnership model could mature into permanent neutral-host entities that diversify rural revenue streams for independent tower companies.

Private 5G Spectrum Licensing Unlocks Industrial Connectivity Demand

More than 26,000 private-5 G licenses have been issued for 4.7 GHz and 28 GHz bands, enabling 82 live sites that serve 36 factories, hospitals, and logistics hubs. Enterprises demand low-latency, high-reliability links unattainable on shared public networks, creating niche tower opportunities inside industrial campuses. On-premises structures often require hardened cabinets, redundant power, and secure edge-computing racks—features that command premium lease rates. The South Korea telecom towers market therefore taps a new customer class beyond MNOs, diversifying revenue and lowering churn risk. Tailored service-level agreements aligned with manufacturing cycle times further differentiate tower offerings in this segment. As Industry 4.0 adoption widens, tower owners that establish early footholds in smart factories can cross-sell analytics, private-core hosting, and mini-data-center space.[1]Bo-Young Lee, “Korea’s Private 5G Licenses Top 26,000,” The Korea Herald, koreaherald.com

Grid-Tied Solar Retrofit Programs Enhance Operational Sustainability

Subsidies for installing solar-hybrid power systems on more than 1,000 remote sites push operators toward greener energy mixes and lower diesel burn. Renewable retrofits reduce operating costs amid volatile electricity tariffs, lengthen back-up autonomy, and support corporate carbon-neutrality pledges—SK Telecom targets net-zero by 2025. [2]“SK Telecom Targets Net-Zero by 2025,” Fibre Systems Magazine, fibresystems.orgThe retrofit scheme leverages existing masts, eliminating the need for greenfield builds while complying with stricter environmental standards. Solar-integrated power systems also pair well with AI-based energy-management software that can lower 5 G radio power draw by 20%. Financial incentives shorten payback periods to fewer than four years, stimulating a stable pipeline of modernization projects that sustain the South Korea telecom towers market through 2030.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| 28 GHz license revocations for SKT/KT/LGU+ | -0.7% | Nationwide; focus on metro cores | Short term (≤ 2 years) |

| 10% tenancy-fee cap imposed by MSIT | -0.5% | National | Medium term (2–4 years) |

| Fiber-first backhaul preference in Seoul–Busan | -0.3% | Seoul–Busan corridor | Medium term (2–4 years) |

| Rising land-lease renewals at 7% CAGR in metro zones | -0.4% | Major metropolitan areas | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

28 GHz License Revocations Constrain Millimeter-Wave Investment Strategies

The regulator canceled 28 GHz licenses from all three MNOs for missed rollout obligations in 2024, clouding business cases for ultra-high-band sites and curbing short-term capex. Millimeter-wave propagation requires site densities several times higher than sub-6 GHz, a financial hurdle exacerbated by spectrum uncertainty. Operators are reallocating capital to mid-band and AI edge initiatives rather than risk additional write-offs. The setback lowers the immediate addressable demand for new rooftop and small-cell poles designed for 28 GHz sectors, trimming growth potential for urban tower providers. Although future re-tenders may revive interest, near-term tower procurement pipelines reflect a pivot to 3.5 GHz densification instead.

MSIT Tenancy-Fee Cap Pressures Tower Revenue Growth

A nationwide 10% ceiling on tenancy-fee increases took effect in 2024 to temper consumer tariffs. While beneficial for operators, capped indexation compresses tower cash flows, especially for independent firms reliant on rent escalators to offset inflation and land-lease renewals. Lower yield prospects raise hurdle rates for constructing marginal sites in mountainous or low-traffic districts. Tower owners now emphasize operational excellence, multi-tenancy maximization, and energy savings to protect margins. Over the medium term, value-added offerings such as edge-computing enclosures and AI-enabled predictive maintenance emerge as compensatory revenue levers within the South Korea telecom towers market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Ownership: Operator Dominance Meets Independent Momentum

Operator-controlled assets held 48.41% of the South Korea telecom towers market share in 2025, equating to more than 26,000 macro and micro sites nationwide. Robust cash positions allow SK Telecom, KT Corp, and LG Uplus to dictate rollout tempo and technology upgrades, safeguarding network quality and brand differentiation. This concentration, however, ties up balance-sheet capital and exposes MNOs to infrastructure depreciation risks at a time when AI and data-center investments beckon.

Independent tower companies—although presently smaller—are projected to log a 6.18% CAGR to 2031 as operators monetize portfolios via sale-and-leaseback deals. Such transactions unlock capital while maintaining long-term site access under master lease agreements. The South Korea telecom towers market size for independent owners could therefore surpass USD 312 million by the decade’s end, contingent on regulatory support for fair-rent principles and multi-tenant neutrality. Joint-venture models also gain traction, especially for shared rural towers under the “One Network” scheme, where combined traffic volumes boost site economics. Meanwhile, MNO captive sub-segments endure for mission-critical installations—data-center campuses and border security sites—where heightened control trumps financial optimization.

By Installation: Rooftop Nodes Outpace Ground-Based Footings

Ground-based towers accounted for 53.78% of the South Korea telecom towers market size in 2025, favored for superior elevation, ease of multi-tenant loading, and straightforward maintenance access. Typical sites in suburban zones support 3-4 tenants and accommodate weighty legacy 2 G/3 G gear alongside modern 5 G Massive-MIMO arrays. Yet urban land scarcity and rising lease tariffs foster a shift toward rooftop platforms, which the industry expects to grow at 11.87% CAGR through 2031.

Rooftop structures offer accelerated deployment—often under 90 days from contract to on-air—making them ideal for rapid densification along congested Seoul boulevards. Compact monopoles and wall-mounted panels satisfy zoning authorities concerned with skyline aesthetics. Despite smaller coverage radii, high traffic density in apartment clusters and shopping districts yields attractive capacity revenue per square meter. Future rooftop opportunities may spring from urban-air-mobility corridors, where vertiports require reliable command-and-control links, adding incremental demand within the South Korea telecom towers industry.

By Fuel Type: Grid-Diesel Hybrids Remain Mainstream as Renewables Scale

Hybrid grid/diesel systems supplied 83.94% of total tower energy in 2025, balancing cost efficiency with resilience against Korea’s typhoon-induced outages. Diesel gensets provide backup autonomy of 12–24 hours, while grid power remains the primary source in most urban and suburban sites. However, sustainability mandates and subsidy programs propel renewable penetration to a 7.34% CAGR over 2026-2031.

Solar photovoltaics combined with lithium-ion storage dominate retrofit projects atop mountain ridges and island locales, trimming diesel consumption by up to 60%. Renewable-powered towers accrue carbon credits that can monetize under Korea’s emissions-trading framework, indirectly raising site returns. Furthermore, AI-driven battery-management systems extend asset lifespans and optimize charging cycles, improving total-cost-of-ownership metrics. As renewable component prices fall, hybrid-solar penetration could exceed 24.70% of the South Korea telecom towers market by 2031, subject to grid connection availability and storage economics.

By Tower Type: Monopole Efficiency Spurs Stealth Adoption

Monopoles owned 44.96% of market share in 2025 because they require just 12–16 m² of land and streamline permitting processes. Single-shaft steel poles can be erected within 30 days, underpinning operators’ need for fast capacity adds in urban canyons. Their sleek profile also reduces wind load, lowering structural-engineering costs compared with lattice frames.

Stealth or concealed solutions, though only a single-digit share today, are expanding at a forecast 4.96% CAGR as municipalities tighten visual-impact ordinances. Camouflaged “street-furniture” poles blend with lamp posts, and building-integrated antennas hide behind facades or glass, gaining favor in heritage districts. Lattice and guyed configurations still dominate rural and coastal macros where taller heights enhance coverage but face minimal aesthetic pushback. Choice of tower form increasingly hinges on local zoning and community acceptance factors, compelling vendors in the South Korea telecom towers market to broaden design catalogs and engage in early stakeholder consultations.

Geography Analysis

South Korea’s topography—70% mountainous terrain—creates stark contrasts between urban mega-clusters and sparsely populated uplands. The Seoul-Busan corridor concentrates more than half of national traffic and hosts the densest tower grids, with some CBD blocks averaging one site every 200 meters. Operators willingly absorb higher land-lease escalations averaging 7% CAGR in exchange for premium data monetization opportunities and high-margin enterprise contracts. Rooftop tenancy demand is greatest here, driving multi-operator agreements that optimize limited skyline real estate. Advanced fiber rings, exemplified by KT’s 867,056 km backbone, supply abundant backhaul bandwidth.

Central-region industrial parks—anchored by automotive and semiconductor fabs—rely on private-5 G licenses, spurring custom tower builds on factory grounds. These installations often integrate edge servers for machine-vision analytics, giving tower providers a platform to bundle compute-and-connectivity solutions. Coastal provinces grapple with typhoon exposure, leading to reinforced lattice designs and corrosion-resistant materials that push capex per site above inland averages. Border districts near the Demilitarized Zone prioritize security hardening and electromagnetically shielded shelters, a niche segment typically retained under MNO captive ownership.

Rural heartlands benefit from the “One Network” sharing paradigm that spreads financial burden across operators, ensuring 5 G-level service without duplicative infrastructure. Renewable power kits find greatest applicability here, given sporadic grid reach and diesel delivery challenges during winter snows. Looking toward 2026-2028, budding urban-air-mobility corridors in greater Seoul may demand specialized low-latency C2 (command-and-control) nodes atop high-rise rooftops, opening incremental revenue streams for proactive tower companies. Altogether, geographic complexity solidifies the need for diversified asset strategies across the South Korea telecom towers market.

Competitive Landscape

SK Telecom, KT Corp, and LG Uplus together steward nearly half of national tower stock through direct ownership, underpinning an oligopolistic market structure. Their scale guarantees site pipeline continuity, but rising spectrum fees and AI-data-center ambitions prompt renewed interest in asset-light models. SK Telecom’s plan to channel KRW 3.4 trillion into AI data centers by 2028 exemplifies this capital reallocation. Sale-leaseback discussions with domestic infrastructure funds indicate momentum toward greater independent ownership, which could usher in more transparent pricing benchmarks.

Independent tower companies leverage neutrality to host multi-tenant configurations, offering MNOs 15–20% savings versus solitary builds. Global investors such as DigitalBridge’s USD 631 million acquisition of Japan’s JTower demonstrate robust valuation appetite across Northeast Asia. [3]Ben Baker, “DigitalBridge Acquires JTower for USD 631 Million,” Capacity Media, capacitymedia.comSimilar monetization plays in Korea would inject liquidity and propel professional tower-management practices, including AI-driven drone inspection and predictive maintenance. Renewable-energy integration and edge-computing cabinets become differentiators, with providers bundling turnkey services to elevate lease ARPUs.

Regulation shapes the competitive field: the 10% rent cap suppresses income upside, but tax credits for indoor DAS installations and solar retrofits partially offset margin compression. Meanwhile, spectrum policy uncertainty—especially around future 28 GHz allocations—requires agile capital planning. Operators diversifying into quantum-secure networking, as evidenced by SK Telecom’s USD 65 million infusion into ID Quantique, may eventually demand towers outfitted with quantum-random-number-generator modules for ultra-secure backhaul. As technology complexity escalates, collaborative ecosystems between tower firms, power-solution vendors, and edge-cloud providers will dominate strategic agendas within the South Korea telecom towers market.

South Korea Telecom Tower Industry Leaders

SK Telecom

KT Corp

LG Uplus

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: SK Telecom joined the MIT GenAI Impact Consortium to accelerate AI research for network optimization.

- January 2025: SK Telecom invested USD 65 million in Swiss quantum firm ID Quantique, with plans for a Seoul R&D hub in H2 2025.

- November 2024: SK Telecom acquired an additional 24.76% stake in SK Broadband for KRW 1.15 trillion, boosting ownership to 99.1%.

- August 2024: DigitalBridge bought Japan’s JTower for USD 631 million, providing a regional valuation benchmark.

South Korea Telecom Tower Market Report Scope

Telecom towers encompass a variety of structures, such as monopoles, tripoles, lattice towers, guyed towers, self-supporting towers, poles, masts, and other similar forms. These towers, equipped with one or more telecommunication antennas, facilitate radio communications. They can be situated on the ground or atop a building's rooftop and often include storage for equipment and electronic components.

The South Korea telecom towers market is segmented by ownership (operator-owned, private-owned, and MNO Captive sites), by installation (rooftop, and ground-based), and by fuel type (renewable and non-renewable). The Market Sizes and Forecasts are Provided in Terms of Installed Base (in Thousand Units) for all the Above Segments.

| Operator-owned |

| Independent TowerCo |

| Joint-Venture TowerCo |

| MNO Captive |

| Rooftop |

| Ground-based |

| Renewable-powered |

| Grid/Diesel Hybrid |

| Monopole |

| Lattice |

| Guyed |

| Stealth / Concealed |

| By Ownership | Operator-owned |

| Independent TowerCo | |

| Joint-Venture TowerCo | |

| MNO Captive | |

| By Installation | Rooftop |

| Ground-based | |

| By Fuel Type | Renewable-powered |

| Grid/Diesel Hybrid | |

| By Tower Type | Monopole |

| Lattice | |

| Guyed | |

| Stealth / Concealed |

Key Questions Answered in the Report

What is the current value of the South Korea telecom towers market?

The market is valued at USD 503.86 million in 2026 and is projected to reach USD 596.62 million by 2031.

How fast is renewable power adoption at Korean tower sites?

Renewable-powered installations are expanding at a 7.34% CAGR as subsidies and carbon targets gain traction.

Which tower ownership model is growing the fastest?

Independent tower companies are forecast to grow at a 6.18% CAGR through 2031 as operators monetize assets.

What regulatory move is putting pressure on tower tenancy revenue?

The Ministry of Science and ICT imposed a nationwide 10% cap on tenancy-fee increases starting in 2024.

How are private 5G licenses affecting tower demand?

More than 26,000 licenses for industrial users are creating new on-premises tower opportunities inside smart factories.

Why has millimeter-wave investment slowed recently?

The revocation of all 28 GHz licenses in 2024 reduced operator confidence, redirecting capex toward mid-band densification.

Page last updated on: