Thailand Telecom Towers Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

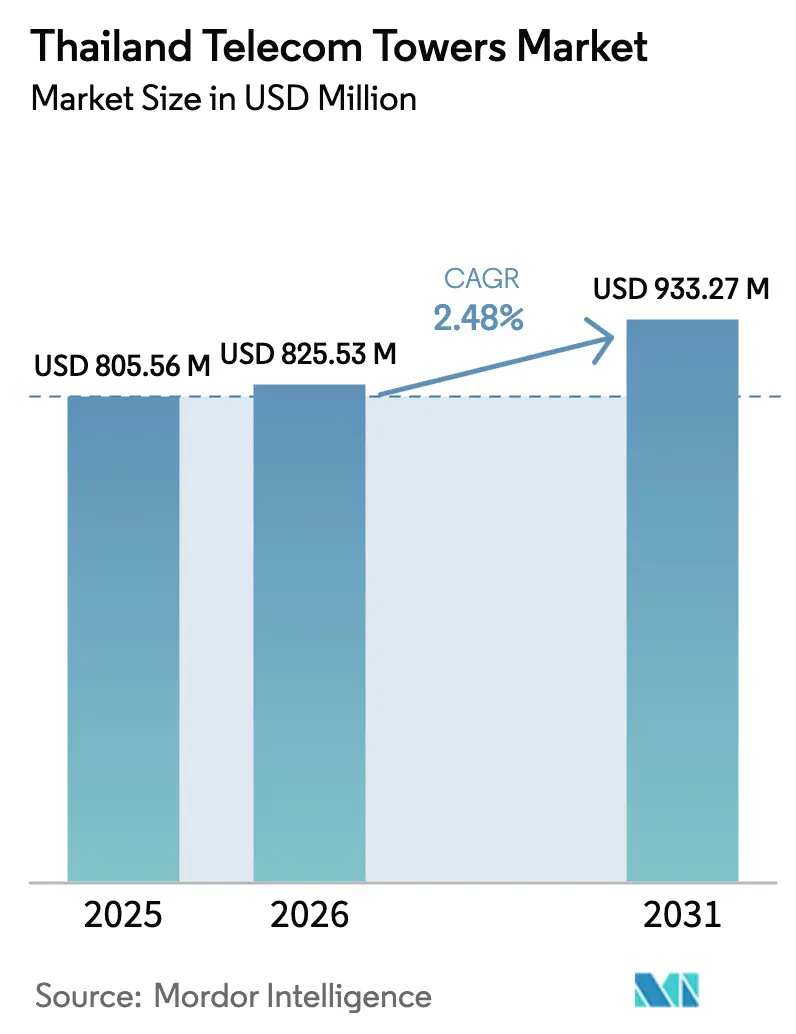

| Base Year Market Size (2025) | USD 805.56 Million |

| Market Size (2026) | USD 825.53 Million |

| Market Size (2031) | USD 933.27 Million |

| Growth Rate (2026 - 2031) | 2.48% CAGR |

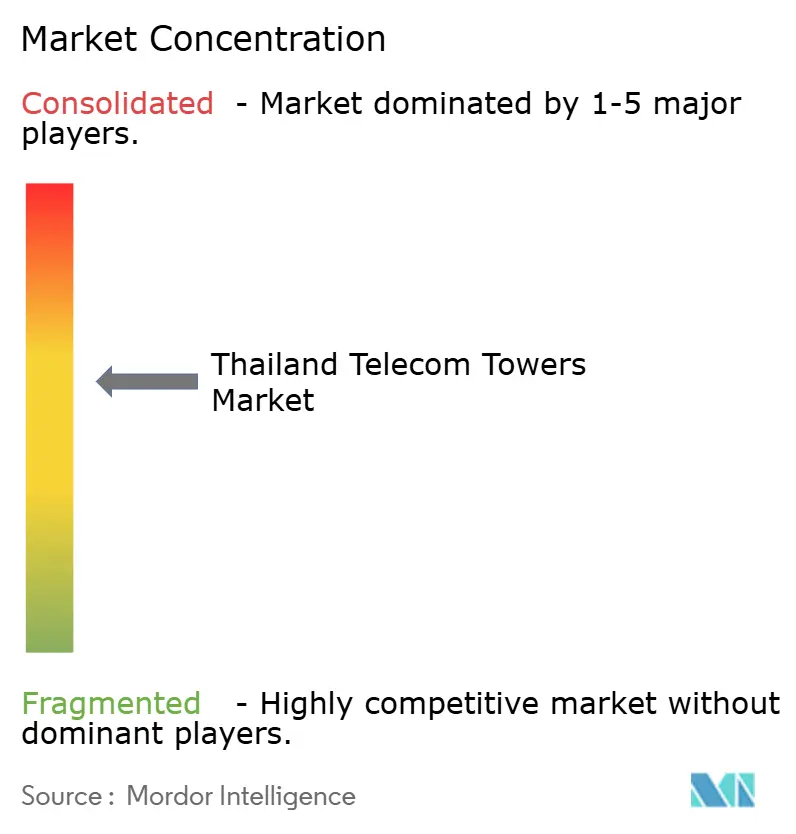

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Thailand Telecom Towers Market Analysis by Mordor Intelligence

Thailand Telecom Towers Market size in 2026 is estimated at USD 825.53 million, growing from 2025 value of USD 805.56 million with 2031 projections showing USD 933.27 million, growing at 2.48% CAGR over 2026-2031.

Solid 5G handset uptake, post-merger asset monetization by True Corporation and Dtac, and government-backed passive-infrastructure sharing rules are keeping capital flowing into new builds while encouraging operators to unlock cash from legacy portfolios. Macro-site demand remains healthy in provincial corridors where rural connectivity gaps persist, yet urban densification is pivoting budgets toward rooftop structures and small cells that complement the macro grid. Cost pressures from elevated steel and zinc prices are nudging tower companies to embrace standardized monopole designs and solar-hybrid energy systems that cut both material tonnage and diesel consumption. Edge-computing nodes clustered around Bangkok and the Eastern Economic Corridor (EEC) are also expanding the addressable tenancy base for micro-tower formats serving hyperscale data centers.

Key Report Takeaways

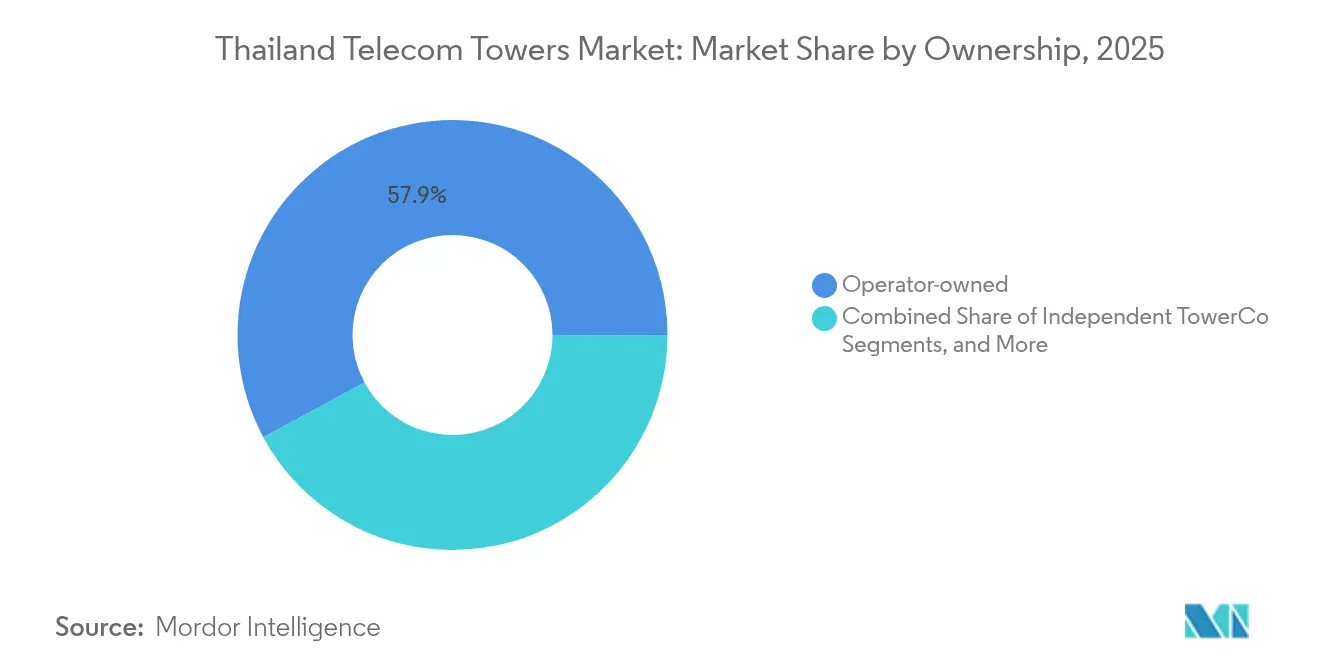

- By ownership, operator-controlled sites led with 57.88% of Thailand telecom tower market share in 2025, while independent TowerCos are expanding at an 8.62% CAGR through 2031.

- By installation type, ground-based structures commanded 68.35% of the Thailand telecom tower market size in 2025; rooftop deployments are advancing at a 5.88% CAGR to 2031.

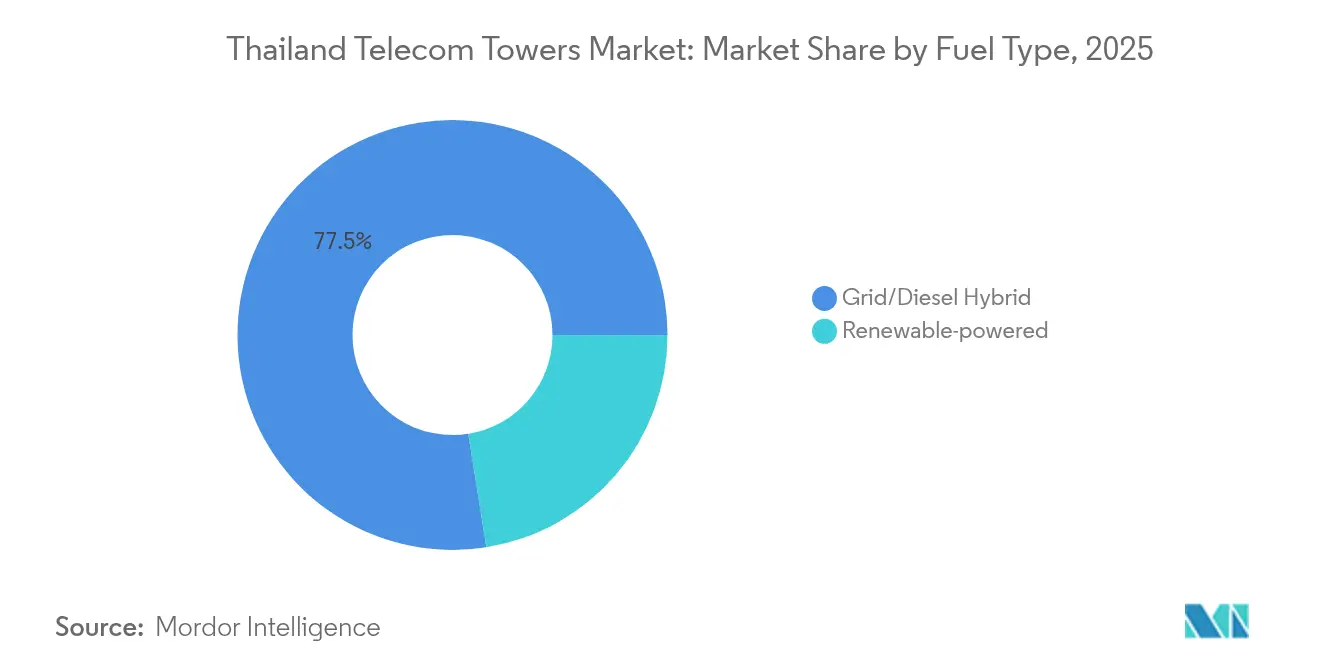

- By fuel mix, grid-diesel hybrids powered 77.52% the Thailand telecom tower market share in 2025; renewable configurations are forecast to grow 10.74% CAGR to 2031.

- By tower type, monopoles held 55.02% of the Thailand telecom tower market share in 2025, and stealth/concealed are advancing at a 5.10% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Thailand Telecom Towers Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| 5G densification mandates and rural-suburban coverage gaps | +1.2% | Nationwide, strongest in Bangkok and EEC | Medium term (2-4 years) |

| Tower-sale-and-leaseback wave post True-Dtac merger | +0.8% | Central and Eastern provinces | Short term (≤ 2 years) |

| NBTC-enforced passive-infrastructure sharing rules | +0.4% | National, excluding restricted border zones | Medium term (2-4 years) |

| Surge in data-center and edge-computing hubs needing micro-edge towers | +0.6% | Bangkok, Chonburi, Rayong, Samut Prakan | Long term (≥ 4 years) |

| Corporate PPAs+ green-site tax credits lowering solar-hybrid TCO | +0.3% | Industrial provinces | Medium term (2-4 years) |

| Railway and motorway smart-corridor roll-outs (EV-charging / C-V2X poles) | +0.2% | Bangkok-Rayong, Thai-Chinese railway corridor | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

5G Densification Mandates and Rural Coverage Gaps

Thailand’s 5G handset penetration crossed the 50% threshold in Q1 2024, up 119.9% year-over-year, driving operators to tighten urban grids while extending macro reach into underserved provinces [1]Trace Media International, “Asia-Pacific Tower and Small Cell Market Sees Notable Growth Despite Ongoing Challenges,” Telecom Review Asia Pacific, telecomreviewasia.com. Advanced Info Service (AIS) is front-loading radio investments to defend network leadership, and National Telecom is adding Tier-3 facilities in Chiang Mai, Khon Kaen, and Hat Yai that backhaul elevated traffic volumes. Although Bangkok enjoys near-continuous 5G coverage, government smart-city targets for 105 municipalities by 2027 are widening the deployment footprint. Consequently, site counts in rural and peri-urban districts are climbing as operators pursue spectrum efficiency and meet universal-service mandates. Macro towers remain essential for contiguous coverage across farmland, mountain passes, and national highways where small-cell economics remain unfavorable.

Sale-and-Leaseback Wave After the True-Dtac Merger

True Corporation’s merger with Dtac ignited Thailand’s largest tower monetization cycle to date, freeing balance-sheet capacity and opening the field to specialist TowerCos. Digital Telecommunications Infrastructure Fund (DIF) emerged as the biggest beneficiary and now manages 16,059 structures, with True retaining a 20.557% stake that aligns incentives between the operator and the REIT. Malaysian-based OCK Group is leveraging its 5,500-tower ASEAN footprint to capture newly vacated assets and sign build-to-suit contracts in suburban districts where capacity growth is brisk. The resulting uptick in independent ownership is altering landlord-tenant dynamics, improving tenancy ratios, and injecting fresh equity capital into the Thailand telecom tower market.

Data-Center and Edge-Computing Hubs Create Micro-Tower Demand

Thailand’s ambition to become Southeast Asia’s data-center gateway has already attracted USD 7.8 billion in confirmed hyperscale investments through 2027, including a USD 950 million campus by Google and a multiyear USD 5.8 billion plan by AWS. These campuses cluster around Bangkok, Chonburi, and Rayong, where latency-sensitive enterprise workloads demand on-premise edge nodes. Micro-towers and rooftop masts are being co-located on data-center rooftops and adjacent parcels to reduce fiber hops and accelerate 5G private-network rollouts. TowerCos is able to package power redundancy, fiber backhaul, and neutral-host radio access to secure high-yield, long-term contracts with hyperscale tenants.

Corporate PPAs and Green-Site Tax Credits Lower Solar-Hybrid TCO

Altervim’s rollout of 1,200 solar-hybrid sites for True has validated a commercial model that generates 7.6 million kWh per year and avoids 107,000 tons of lifetime CO₂ emissions [2]Altervim PLC, “Business Solution,” Altervim, altervim.com. The economics are sharpening further as the Energy Regulatory Commission grants 25-year feed-in tariffs and as corporates sign fixed-price PPAs that hedge diesel volatility. EGCO’s award of 448 MW of solar capacity under the FiT program exemplifies the scale now achievable. Industrial provinces such as Chonburi and Rayong are early movers because co-located factories already host rooftop PV that can be cross-wired to power telecom loads during daylight hours. Improved lithium-iron-phosphate storage prices are reducing overnight CAPEX burdens, allowing TowerCos to capture opex savings without compromising uptime guarantees.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid switch to small-cell street furniture diluting macro-tower tenancy ARPU | -0.7% | Bangkok Metropolitan Region and core provincial cities | Short term (≤ 2 years) |

| Border-zone height and power limits (2025 NBTC directive) | -0.3% | Northern, Western, Southern border provinces | Medium term (2-4 years) |

| High steel and zinc costs inflating new-build CAPEX volatility | -0.4% | National, acute on greenfield builds | Short term (≤ 2 years) |

| Slow permitting on community land and sacred sites | -0.2% | Rural provinces with communal land tenure | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Small-Cell Adoption Pressures Macro-Tower Economics

Street-level 5G nodes mounted on lamp posts and billboards are proliferating across Bangkok and high-traffic provincial downtowns. Asia-Pacific benchmarks already show small cells accounting for 37.8% of active sites and growing 18.9% annually as operators re-allocate budget to street furniture that improves spectral reuse, tenancy growth on traditional macro infrastructure slows, eroding average revenue per tenant at legacy towers. TowerCos are countering by offering end-to-end neutral-host packages, yet EBITDA margins narrow when leasing rates per antenna are lower than macro norms.

Border-Zone Height and Power Restrictions

The NBTC’s 2025 directive caps tower heights to 15 m within 200 m of international borders and 30 m within 3.5 km, while instructing operators to throttle radiated power on existing sites [3] John Formichella et al., “In Brief: Telecoms Regulation in Thailand,” Lexology, lexology.com. Tighter rules particularly constrain northern districts adjoining Myanmar and Laos, and southern provinces near Malaysia. Operators now require denser grids of shorter poles, inflating capex per square kilometer and complicating land acquisition. The restrictions channel demand into stealth installations and indoor repeaters, but those alternatives cannot always replicate the wide-area coverage of taller lattices, leaving sporadic service gaps along border corridors.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Ownership: Independent TowerCos Gain Momentum

Operator-controlled portfolios retained 57.88% of the Thailand telecom tower market share in 2025, underscoring how vertically integrated models still dominate national coverage maps. The 2024-initiated consolidation of True and Dtac, however, accelerated the spin-off of redundant steel, propelling the independent cohort to an 8.62% CAGR through 2031. Digital Telecommunications Infrastructure Fund’s 16,059-site estate anchors the segment, while OCK Group’s cross-border balance sheet allows it to underwrite multi-province build-to-suit programs. The Thailand telecom tower market size attributed to independent TowerCos is projected to close much of the gap with MNO portfolios before 2030 as operators pivot toward spectrum and customer acquisition missions.

Lease-up rates on acquired assets are trending upward because neutral owners can court multiple tenants without competitive conflicts. Joint-venture vehicles that pair equity funds with provincial utilities are emerging as an intermediate model, especially for rural clusters where investor appetite is tempered by lower traffic. MNO captive models linger among tier-2 operators that prioritize end-to-end network control, but rising spectrum costs and dividend expectations are eroding tolerance for low-return steel ownership.

By Installation: Rooftop Deployments Accelerate Urban Coverage

Ground-based masts accounted for 68.35% of the Thailand telecom tower market size in 2025 due to historical rollouts across farmland, highways, and peri-urban plots. Bangkok’s saturation and escalating land prices, however, are pushing TowerCos to elevate antennas atop commercial high-rises and factory rooftops, a format advancing 5.88% annually. High-rise landlords view shared digital infrastructure as a new revenue line, shortening lease negotiations and enabling coverage in elevator cores and parking decks that traditional macro beams cannot penetrate.

Rooftop preference is also rising inside the EEC as automotive and electronics plants deploy private 5G for robotics and quality control. Industrial tenants favor roof-edge installations that avoid ground-level logistics disruptions, accelerating time-to-service for on-premise networks. Despite the urban pivot, macro towers will sustain relevance along national motorways and rural municipalities where pole-top heights of 30-50 m remain the most economical path to continuous coverage.

By Fuel Type: Renewable Transition Gains Commercial Momentum

Grid-diesel hybrids still energized 77.52% of active towers in 2025, but double-digit renewable site growth demonstrates that operational attitudes are shifting. The Thailand telecom tower market size tied to solar-hybrid configurations is benefiting from PPAs that lock electricity costs well below diesel parity, generating predictable opex savings for fifteen years or more. Altervim’s 1,200-site program illustrates the payback, and follow-on agreements with EGCO and GUNKUL have cleared procurement hurdles at multiple TowerCos.

Battery prices are easing fast enough that lithium-iron-phosphate systems now match diesel gensets on lifecycle cost under Thailand’s humidity and temperature profiles. Remote provinces with unstable grid supply, particularly in mountainous northwestern corridors, rank highest for early renewable adoption because they derive the greatest benefit from diesel displacement and carbon-credit monetization.

By Tower Type: Monopole Efficiency Drives Market Leadership

Monopole structures captured 55.02% of the 2025 Thailand telecom tower market share because their one-piece shafts trim steel tonnage by up to 25% relative to lattices, saving both material outlays and shipping fees. Prefabrication also compresses assembly times, a boon in congested Bangkok districts where work-hour windows are narrow. Lattice frames still rule on high-capacity sites that host three or more tenants, especially in rural fields where plot footprints are inexpensive. Guyed masts find niche roles in broadcast relays and emergency networks, but permitting hurdles in urban zones curb broader uptake.

Stealth and concealed poles are gaining cultural currency in heritage precincts like Ayutthaya and Chiang Mai, where UNESCO guidelines discourage visible clutter. A 5.10% CAGR through 2031 indicates steady momentum as antenna-wrapping technologies allow cylindrical shrouds to house multiband arrays without RF loss. Tourism-heavy islands such as Phuket are already mandating concealed designs along beachfront promenades.

Geography Analysis

Bangkok Metropolitan Region remains the revenue engine of the Thailand telecom tower market, hosting the densest grid and the highest tenant-per-tower ratio in 2024. Every incremental megabyte of traffic in the city generates disproportionate lease income because antennas from three national MNOs, plus myriad MVNOs, frequently share the same shafts. The adjacent provinces of Nonthaburi, Pathum Thani, and Samut Prakan bolster lease-up averages thanks to industrial estates and airport logistics zones that require continuous 5G coverage.

Eastern Economic Corridor provinces, Chonburi, Rayong, and Chachoengsao, are the fastest-growing cluster. These hyperscale projects spawn demand for edge nodes, fiber interconnects, and private 5G micro-grids, all of which rely on rooftop or short monopole towers to deliver last-mile radio access. The Thailand telecom tower market size associated with the EEC is expected to close the decade at a level nearly double that of 2024 installations. Northern provinces wrestle with border-zone height restrictions that hamper macro coverage along rugged, forested terrain. Operators compensate by increasing pole density but still face higher cost-per-subscriber metrics than in flat central plains. Southern Thailand presents a split picture: tourist hubs like Phuket insist on concealed or palm-tree designs for visual harmony, whereas deep-water port cities such as Songkhla favor conventional steel for maritime and oil-and-gas backhaul. The Isan plateau of Northeast Thailand posts steady, albeit slower, site growth driven by agricultural IoT adoption and the government’s smart-village pilots.

Competitive Landscape

Competition in the Thailand telecom tower market is moderately concentrated around three models: operator-owned portfolios, the DIF REIT platform, and a rising tier of regional TowerCos. Advanced Info Service and True Corporation continue to wield bargaining leverage through integrated networks, but their sale-and-leaseback pipelines indicate a gradual retreat from tower ownership. DIF’s 16,059-tower inventory provides scale economies that lower maintenance opex per tenant and attract institutional capital seeking predictable dividends.

Independent TowerCos like OCK Group and InTouch Infrastructure are exploiting this ownership gap with flexible leasing terms and turnkey renewable packages that appeal to MNO sustainability mandates. Technology differentiation increasingly rests on energy management and edge-compute colocation, rather than sheer mast count. Regulatory rigors, including NBTC sharing mandates and 15 m border height ceilings, reward incumbents fluent in local zoning statutes and provincial stakeholder management. New entrants must navigate land-use negotiations, power-access permits, and community outreach, tasks that add months to rollout schedules and deter speculative builds.

Thailand Telecom Towers Industry Leaders

Digital Telecommunications Infrastructure Fund (DIF)

OCK Group Berhad

Advanced Info Service (AIS)

True Corporation Public Company Limited

National Telecom (NT)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: NBTC revoked K4 Communication’s telecom license amid fraud litigation valued at THB 50 million, affecting 46,000 subscribers and underscoring sharper regulatory oversight.

- December 2024: EGCO won 11 solar projects totaling 448 MW under the national feed-in-tariff program, paving the way for deeper renewable penetration across telecom sites.

Thailand Telecom Towers Market Report Scope

Telecommunication towers encompass a variety of structures, such as monopoles, tripoles, lattice towers, guyed towers, self-supporting towers, poles, masts, and other similar forms. These towers, equipped with one or more telecommunication antennas, facilitate radio communications. They can be situated on the ground or atop a building's rooftop and often include storage for equipment and electronic components.

The Thail telecom towers market is segmented by ownership (operator-owned, private-owned, and MNO captive sites), by installation (rooftop and ground-based), and by fuel type (renewable and non-renewable). The market size and forecasts are provided in terms of installed base (Thousand Units) for all the above segments.

| Operator-owned |

| Independent TowerCo |

| Joint-Venture TowerCo |

| MNO Captive |

| Rooftop |

| Ground-based |

| Renewable-powered |

| Grid/Diesel Hybrid |

| Monopole |

| Lattice |

| Guyed |

| Stealth / Concealed |

| By Ownership | Operator-owned |

| Independent TowerCo | |

| Joint-Venture TowerCo | |

| MNO Captive | |

| By Installation | Rooftop |

| Ground-based | |

| By Fuel Type | Renewable-powered |

| Grid/Diesel Hybrid | |

| By Tower Type | Monopole |

| Lattice | |

| Guyed | |

| Stealth / Concealed |

Key Questions Answered in the Report

What is the current valuation of Thailand’s telecom tower business?

The Thailand telecom tower market size was USD 825.53 million in 2026 and is forecast to hit USD 933.27 million by 2031.

How fast are independent TowerCos growing in Thailand?

Independent TowerCos are expanding at an 8.62% CAGR through 2031, fueled by sale-and-leaseback deals after the True–Dtac merger.

Which Thai region shows the highest tower growth potential?

The Eastern Economic Corridor provinces of Chonburi, Rayong, and Chachoengsao lead with a projected 4.05% CAGR due to heavy data-center investment.

Why are solar-hybrid power systems gaining traction on Thai towers?

Corporate PPAs and 25-year feed-in tariffs are cutting energy opex, making solar-hybrid sites cheaper than diesel-reliant grids over the asset life.

How do border regulations affect tower deployment?

NBTC limits poles to 15 m height near borders, forcing operators to build more but shorter towers and to reduce transmit power, which slows rollout in frontier provinces.

What design dominates tower construction in Thailand?

Monopole towers hold 55.02% market share because their modular build lowers steel usage and speeds erection, especially in congested urban sites.

Page last updated on: