Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

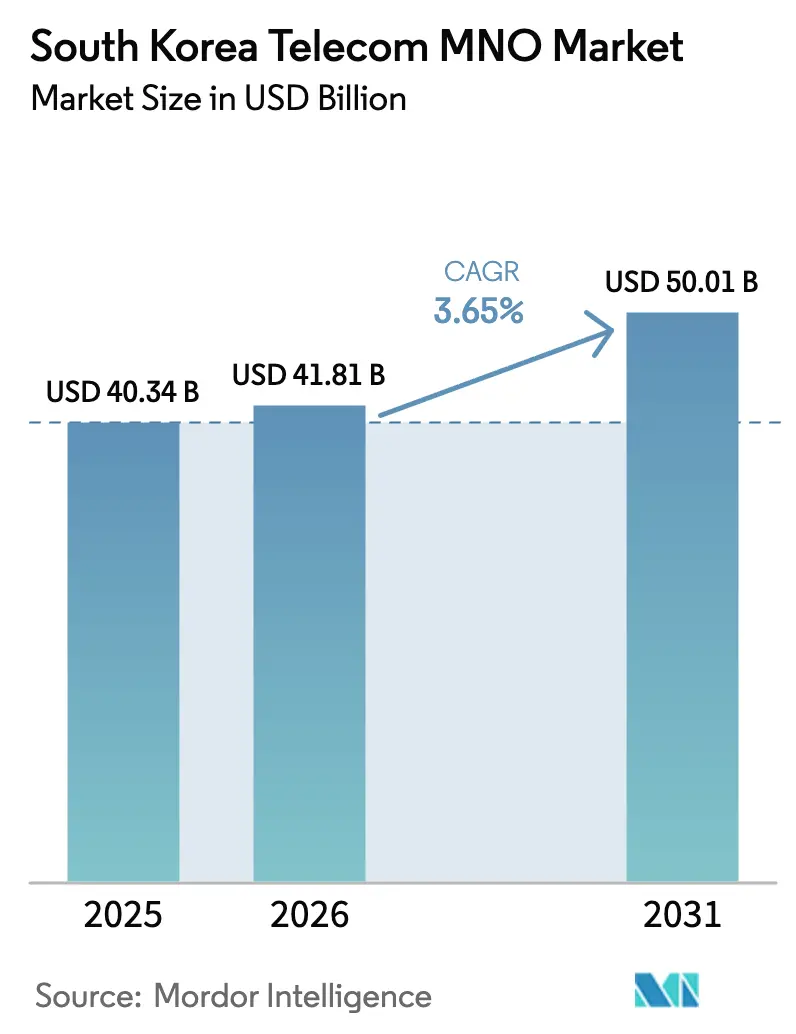

| Base Year Market Size (2025) | USD 40.34 Billion |

| Market Size (2026) | USD 41.81 Billion |

| Market Size (2031) | USD 50.01 Billion |

| Growth Rate (2026 - 2031) | 3.65% CAGR |

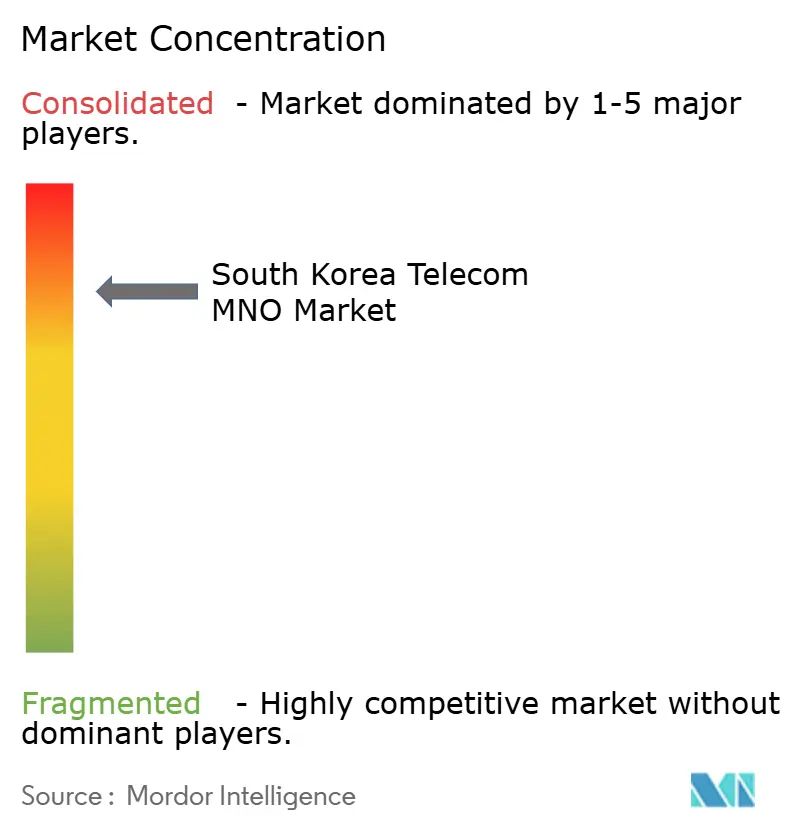

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Korea Telecom MNO Market Analysis by Mordor Intelligence

The South Korea telecom MNO market size was valued at USD 40.34 billion in 2025 and estimated to grow from USD 41.81 billion in 2026 to reach USD 50.01 billion by 2031, at a CAGR of 3.65% during the forecast period (2026-2031). Operators are prioritizing enterprise network slicing, private 5G, and fixed-mobile convergence to counter price pressure from mid-tier 5G plans and MVNO-driven competition. Regulatory wholesale-rate cuts amplify that pressure, yet also broaden addressable demand in lower-income user groups, sustaining traffic growth. Manufacturing digitalization, cloud-edge partnerships, and AI-powered personal assistants are jointly enlarging the data services pie, while OTT substitution accelerates voice and SMS decline. Against this backdrop, spectrum fees and the 49% foreign-ownership cap continue to weigh on free cash flow and limit external funding.

Key Report Takeaways

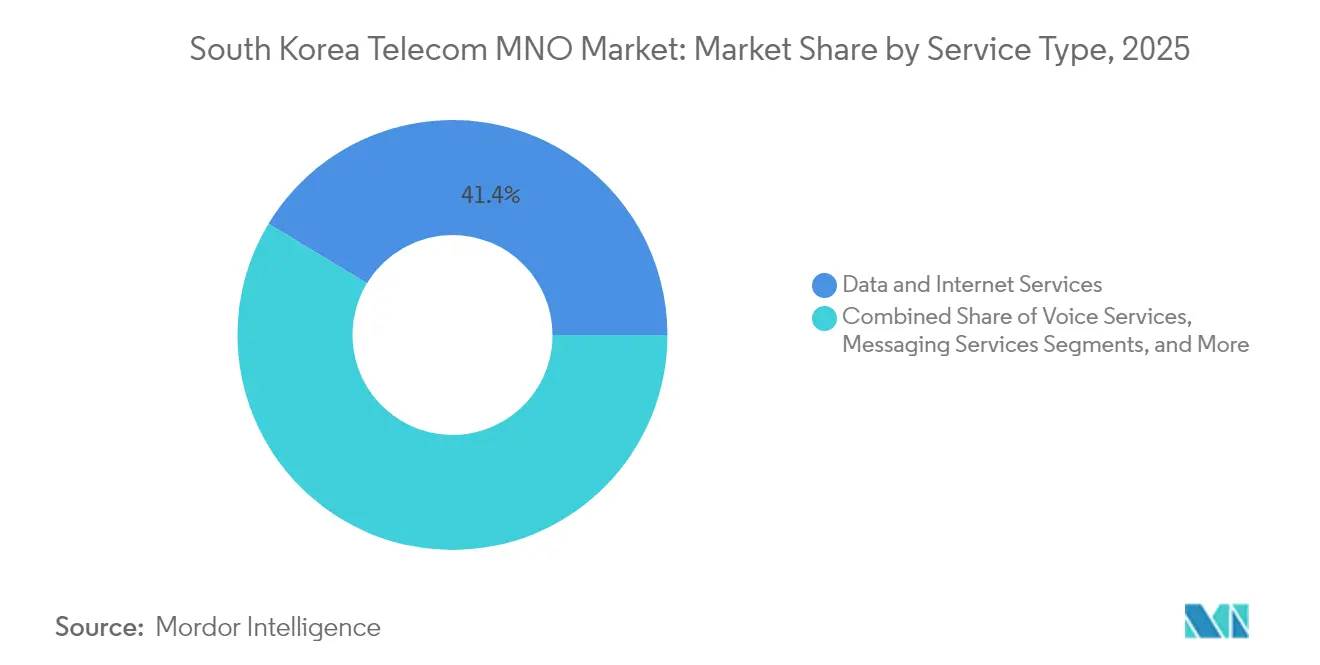

- By service type, data and internet services held 41.35% of the South Korea telecom MNO market share in 2025. IoT and M2M services are projected to expand at a 3.76% CAGR from 2026 to 2031.

- By end user, the consumer segment accounted for 70.42% of the South Korea telecom MNO market size in 2025. The enterprise segment records the quickest trajectory, advancing at a 4.02% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

South Korea Telecom MNO Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Premium-priced 5G SA enterprise slicing | +0.8% | National, concentrated in Seoul-Incheon industrial corridor | Medium term (2-4 years) |

| Fixed-mobile convergence (FMC) bundles pushing churn below 2% | +0.6% | National, with higher penetration in urban areas | Short term (≤ 2 years) |

| MVNO-wholesale rate cuts enabling fourth-player price wars | +0.4% | National, with spillover effects in rural markets | Short term (≤ 2 years) |

| National push for private 5G in manufacturing "smart factories" | +0.7% | National, early gains in Ulsan, Gyeonggi, and Chungcheong provinces | Medium term (2-4 years) |

| AI-powered personal assistants driving data traffic | +0.5% | National, with early adoption in metropolitan areas | Long term (≥ 4 years) |

| Cloud-edge partnerships monetizing ultra-low-latency video | +0.3% | National, focused on high-density urban centers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Premium-priced 5G SA enterprise slicing drives B2B transformation

Operators deploy dedicated network slices to guarantee latency and security for mission-critical tasks, enabling premium tariffs that shield margins in a saturated consumer arena. The Republic of Korea Navy’s private 5G project highlights the strategic value of isolated bandwidth for digital-twin and security workloads. Early industrial adopters such as Hyundai report zero connectivity-related downtime after integrating RedCap 5G into smart-factory lines. Regulators have already awarded private 5G frequencies to 35 firms across 56 sites, creating a robust pipeline for enterprise revenue [1]Harrison J. Son, “Private 5G Frequency Allocation Status in Korea,” Netmanias, netmanias.com.

Fixed-mobile convergence bundles reduce churn through service integration

Bundling broadband, mobile, and IPTV under a unified bill raises switching costs and pulls churn below 2%. Historical household surveys show bundle adoption drives markedly stronger retention compared with single-play subscriptions. KT’s Digico strategy illustrates the shift, leveraging fixed assets to cross-sell AI, cloud, and big-data services that deepen customer lock-in [2]Candice Kim, “KT Evolves from Telecom Company to Global Digital Powerhouse,” Aju Press, ajupress.com. SK Broadband’s full ownership by SK Telecom further underlines the prioritization of converged packages to enlarge lifetime value.

MVNO wholesale-rate cuts intensify fourth-player competition

The Ministry of Science and ICT slashed usage-based wholesale fees by up to 52%, from KRW 1.29 to KRW 0.62 per MB, granting MVNOs more economic headroom and stimulating tariff competition at the low end [3]Gigi Onag, “South Korea Plans to Cut Wholesale Telco Rates to Boost MVNO Growth,” Light Reading, lightreading.com. LG Uplus’s decision to pursue MVNO partnerships underscores incumbents’ acknowledgement of the need to defend market share among price-conscious users. Although Stage X’s license revocation removed a full-network entrant, the expanded wholesale regime effectively seeds a de facto fourth-player dynamic in the budget segment.

National manufacturing digitization accelerates private 5G adoption

Government frequency allocations (100 MHz at 4.7 GHz and 600 MHz at 28 GHz) target smart-factory initiatives, pushing operators into turnkey automation roles. Samsung and Hyundai’s RedCap proof-of-concept demonstrated uplink reliability gains essential for real-time robotics, and follow-on projects span logistics and healthcare campuses.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Saturated >130% SIM penetration ceiling | -0.9% | National, with highest saturation in metropolitan areas | Short term (≤ 2 years) |

| Foreign-ownership cap (49%) limiting new capital inflows | -0.4% | National, affecting all major operators | Long term (≥ 4 years) |

| OTT substitution eroding voice/SMS ARPU | -0.7% | National, with higher impact in younger demographics | Medium term (2-4 years) |

| High spectrum-renewal fees squeezing FCF | -0.5% | National, affecting all licensed operators | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Saturated >130% SIM penetration ceiling

With 130% SIM penetration and 24 million 5G accounts already live, net-add upside is negligible, rerouting competition toward ARPU uplift rather than subscriber wins [4]Maeil Business Newspaper, “5G Subscribers Match Nearly Half of 4G in S. Korea,” pulse.mk.co.kr. Operators are introducing sub-USD 20 equivalent 5G plans to avoid churn, yet these dilute blended revenue. In response, SK Telecom pivots resources into AI infrastructure and service differentiation to stabilize margins.

OTT substitution eroding voice/SMS ARPU

Household spend on telecom and streaming is projected to top KRW 140,000 in 2025, diverting wallet share from voice and SMS toward content subscriptions. Netflix and YouTube price hikes magnify the squeeze, particularly for youth cohorts who rely on data-rich apps instead of operator messaging. Telcos respond with content alliances and in-platform recommendation engines, yet low-margin data bundles offset gains in premium tiers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Data services dominate while IoT accelerates

Data and internet services secured 41.35% of the South Korea telecom MNO market share in 2025, benefiting from nationwide 5G coverage and consumer appetite for UHD streaming and cloud gaming. Voice and messaging continue a low-single-digit slide as OTT preference solidifies. The South Korea telecom MNO market size contribution from IoT and M2M remains smaller in absolute value but leads growth at a 3.76% CAGR due to connected-factory and telematics adoption. Operators extend edge-compute nodes that lower latency by 60%, enabling differentiated data-centric use-cases. OTT and PayTV bundles add incremental revenue, with AI-curated channels aiming to stem churn.

Moving through 2026-2031, revenue mix tilts further to data as 6G research collaboration seeds early proofs. Ultra-low-latency video and cloud gaming act as gateway applications for premium tiers, offsetting commoditized connectivity. Operators layer security and analytics on IoT lines to raise ARPU, and private-network slices for factory automation accelerate fee-based growth. Together, these shifts reinforce a pivot toward high-value, data-intensive models that lower reliance on legacy voice contributions.

By End User: Enterprise expansion outpaces consumer maturity

Consumer connections still anchor 70.42% of 2025 revenue, reflecting multi-device households and ubiquitous smartphone penetration. Yet the South Korea telecom MNO market size uplift now skews to enterprise lines, which chart a 4.02% CAGR as manufacturers install private 5G systems to link robots, digital twins, and AGVs. Enterprises adopt network-slice SLAs that command premiums over mass-market price plans, cushioning operator margins in a saturated household arena.

From 2025 onward, regulatory support for Industry 4.0 and the rise of AI-enabled assistants in retail, logistics, and healthcare will broaden the enterprise addressable base. Operators bundle cloud, edge, and security into managed offerings, embedding themselves deeper into customer workflows. While affordable consumer 5G plans safeguard base retention, their limited pricing power keeps overall blended ARPU flat, reinforcing enterprise as the decisive growth engine within the South Korea telecom MNO market.

Geography Analysis

South Korea’s compact geography and government coverage mandates have delivered blanket 5G availability since April 2024. Metropolitan Seoul-Incheon drives premium uptake and early enterprise slicing, owing to dense headquarters clusters and affluent consumers. Manufacturing provinces, Ulsan for shipbuilding, Gyeonggi for electronics, Chungcheong for automotive, anchor private 5G deployments that feed enterprise revenue lines. Rural regions witness MVNO-fueled adoption after wholesale-rate cuts, narrowing the digital divide but at thinner margins.

Urban ARPU remains highest, buoyed by AI-bundled IPTV and cloud gaming. Edge hubs sited in metropolitan exchanges further shorten packet journeys, enabling 8-millisecond latency for AR and industrial control. In industrial belts, private spectrum allocations let factories run autonomous guided vehicles without interference, a capability central to export competitiveness. Coastal naval facilities adopt bespoke 5G for security surveillance, expanding telco reach into defense verticals.

Limited domestic green-field expansion steers operators toward overseas partnerships. SK Telecom’s 6G collaboration with Singtel and Aster AI launch in North America broadens revenue horizons while exporting Korean platform IP. Such ventures offset home-market saturation and leverage advanced network expertise developed under stringent Korean quality-of-service benchmarks.

Competitive Landscape

South Korea’s telecom MNO market is highly concentrated: SK Telecom, KT Corporation, and LG Uplus collectively control a major share of industry revenue, creating an oligopolistic structure that suppresses pricing latitude yet funds R&D scale. Competitive vectors pivot from headline speeds to AI, edge compute, and quantum-secured networks. SK Telecom’s quantum partnership with Nokia underscores first-mover aspirations in post-5G security. KT blends nationwide fiber backbones with cloud services to woo enterprise CIOs, while LG Uplus courts MVNO affiliations to backfill share lost in top-tier segments.

Regulatory enablers such as lower MVNO tariffs prevent excessive rent extraction and sustain churn discipline. Nevertheless, investment obligations stay heavy, with operators pledging multibillion-dollar data-center outlays to serve AI workloads; SK Telecom alone injected USD 200 million into Smart Global Holdings’ U.S. edge facilities. Failure of Stage X to secure a nationwide license eliminated the prospect of a facilities-based fourth entrant, but indirect price warfare persists through MVNO proxies.

Strategic optionality centers on enterprise verticals. Telcos bundle robotics-friendly 5G, cloud analytics, and managed security for export-oriented manufacturers. Defense, smart-port, and smart-city tenders likewise create differentiation opportunities. Partnership ecosystems now extend beyond traditional OEMs into generative-AI labs, evidenced by SK Telecom’s entry into the MIT Consortium and its USD 10 million stake in Perplexity AI, positioning the firm to fuse AI agents with connectivity offers.

South Korea Telecom MNO Industry Leaders

SK Telecom

KT Corporation

LG Uplus

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Samsung and Hyundai completed the industry’s first RedCap trial on private 5G, targeting EV production scaling for 2026.

- February 2025: SK Telecom joined the MIT Generative AI Impact Consortium and unveiled Aster AI assistant for North American beta users.

- November 2024: SK Telecom raised its SK Broadband stake to 99.1% for KRW 1.15 trillion to deepen submarine-cable and data-center reach.

- October 2024: Samsung and KT secured the Republic of Korea Navy smart-port contract, slated for completion in December 2025.

- August 2024: LG and KT formed a 6G research pact to expedite next-gen wireless innovation.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the South Korea telecom market as every billed service revenue generated by licensed mobile network operators across voice, data, messaging, IoT-M2M, OTT, and Pay-TV access. Fixed enterprise connectivity, wholesale transit, and tower leasing are incorporated only where the revenue is booked under the operator's telecom segment, ensuring a like-for-like service view.

Scope exclusion: equipment sales and standalone satellite communications are outside the sizing universe.

Segmentation Overview

- Overall Telecom Revenue and ARPU

- Service Type

- Voice Services

- Data and Internet Services

- Messaging Services

- IoT and M2M Services

- OTT and PayTV Services

- Other Services (VAS, Roaming and International Services, Enterprise and Wholesale Services, etc.)

- End-user

- Enterprises

- Consumer

Detailed Research Methodology and Data Validation

Primary Research

Multiple touch points with operator finance managers, former regulators, tower installers, and enterprise telecom buyers across Seoul, Busan, and Daegu helped verify gray areas such as IoT pricing spreads, 5G private network adoption rates, and likely policy shifts. Their on-ground perspectives enabled us to fine-tune growth drivers that raw desk data could not fully capture.

Desk Research

Analysts began by assembling historical service revenue, subscriber, and traffic series released by the Ministry of Science and ICT, the Korea Communications Commission, the ITU, and the OECD Broadband Portal. Annual and quarterly filings of SK Telecom, KT, and LG Uplus supplied granular ARPU, churn, and capex disclosures. Complementary insight was pulled from Factiva for tariff moves, Questel for 5G-related patent families, and D&B Hoovers for private player financials. These sources, among others consulted, provided the foundational data that underpins each model assumption.

Market-Sizing & Forecasting

A top-down reconstruction converts operator service line revenues to constant 2024 dollars, after which totals are stress tested through bottom-up checks built on subscriber pools multiplied by blended ARPU and sampled enterprise contract values. Key variables tracked include smartphone penetration, monthly data usage per user, 5G subscriber mix, enterprise IoT node counts, and regulated mobile termination rates. Multivariate regression links these indicators to revenue change, while scenario analysis brackets upside from premium 5G slicing and downside from ARPU erosion. Gaps in company-level disclosure, for example, MVNO traffic, are bridged through industry average ratios discussed during interviews and validated against customs data on handset imports.

Data Validation & Update Cycle

Outputs pass a three-level analyst review where variances over ±3% versus external benchmarks trigger a revisit of source files and interview notes. Models refresh every twelve months, with mid-cycle revisions issued when spectrum auctions, tax shifts, or force majeure events materially alter assumptions.

Why Our South Korea Telecom MNO Baseline Commands Reliability

Published estimates often differ because firms pick unequal service baskets, currency bases, and refresh cadences.

Key gap drivers include narrower scopes that drop OTT add-ons, aggressive consumer price inflation factors, or one-off currency spot rates instead of averaged FX conversions. Mordor's base year relies on audited operator statements, cross-checked traffic metrics, and annual FX averages, which together temper volatility and keep the baseline stable.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 40.34 B (2025) | Mordor Intelligence | - |

| USD 35.7 B (2024) | Regional Consultancy A | Excludes OTT and IoT revenues; relies on single-quarter FX rate |

| USD 40.0 B (2024) | Global Consultancy B | Applies higher 5G tariff escalation and no enterprise discounting |

Taken together, the comparison shows that Mordor Intelligence delivers a balanced, transparent baseline rooted in clearly documented variables and repeatable steps, giving decision makers a dependable reference point for strategic planning.

Key Questions Answered in the Report

How large is the South Korea telecom MNO market in 2026?

It is valued at USD 41.81 billion in 2026.

Which service line currently leads revenue?

Data and internet services hold 41.35% share, the highest among service categories.

What CAGR is expected for enterprise connections?

Enterprise lines are projected to grow at a 4.02% CAGR between 2026 and 2031.

Who is the largest mobile operator?

SK Telecom leads with 33.6% revenue share.

Why are MVNOs expanding quickly?

Government-mandated wholesale-rate cuts of up to 52% lowered network-access costs, enabling aggressive retail pricing.

Which technology offers new premium revenue streams?

5G standalone network slicing provides guaranteed performance for mission-critical enterprise applications.

Page last updated on: