Japan Telecom Towers Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 2.72 Billion |

| Market Size (2026) | USD 2.82 Billion |

| Market Size (2031) | USD 3.35 Billion |

| Growth Rate (2026 - 2031) | 3.55% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Japan Telecom Towers Market Analysis by Mordor Intelligence

Japan Telecom Towers Market size in 2026 is estimated at USD 2.82 billion, growing from 2025 value of USD 2.72 billion with 2031 projections showing USD 3.35 billion, growing at 3.55% CAGR over 2026-2031.

This advance reflects the country’s steady 5G densification program, the growing shift toward shared infrastructure economics and continued institutional investment despite currency-driven cost pressures. Operators’ joint-build models, expanding enterprise private-network activity and fiscal incentives for rural roll-outs anchor near-term demand, while heightened zoning limits, seismic retro-fit costs and yen weakness temper margins. Independent tower companies gain traction as neutral-host partners, creating new capital inflows even as the four incumbent MNOs retain sizable captive portfolios. Surging rooftop deployments, early adoption of renewable power systems and concealed tower designs help operators navigate dense urban landscapes and sustainability mandates.

Key Report Takeaways

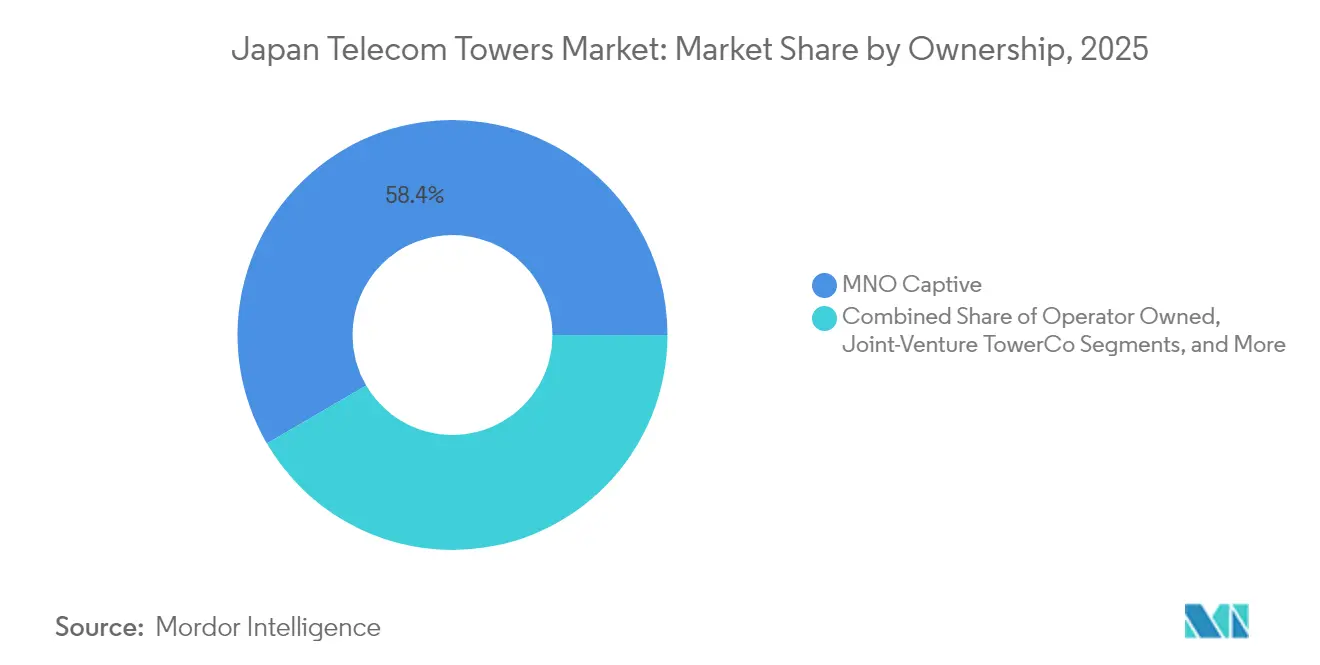

- By ownership, MNO-captive structures held 58.42% of Japan telecom towers market share in 2025; joint-venture TowerCos are projected to grow at a 41.85% CAGR through 2031.

- By installation type, rooftop deployments accounted for 55.15% share of the Japan telecom towers market size in 2025 and are advancing at a 4.32% CAGR through 2031.

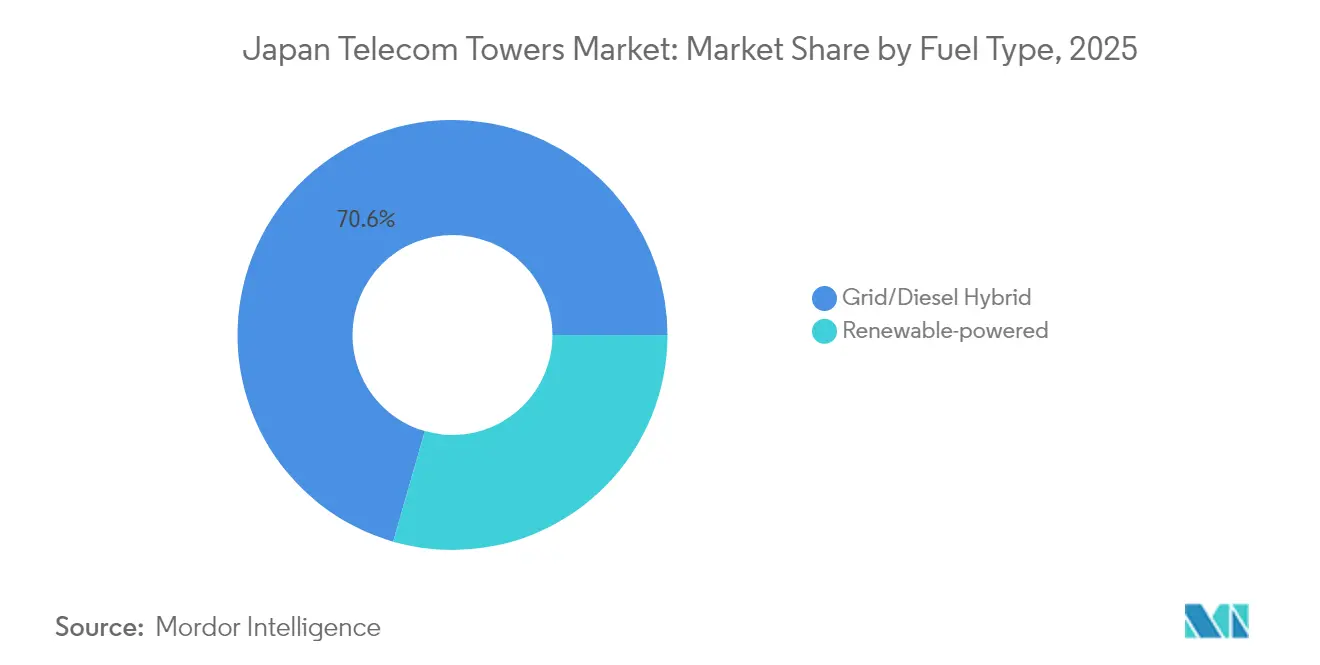

- By fuel type, renewable-powered sites are projected to expand at a 15.62% CAGR between 2026-2031, although grid/diesel hybrids retained 70.55% share of the Japan telecom towers market size in 2025.

- By tower configuration, monopoles led with 40.05% Japan telecom towers market share in 2025, while stealth towers are forecast to post a 5.78% CAGR to 2031.

- KDDI and SoftBank’s nationwide co-construction venture targets 100,000 base stations each by 2030, unlocking JPY 120 billion in CapEx savings for every operator involved.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Japan Telecom Towers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aggressive 5G macro-cell densification targets by MNOs | +1.2% | National, Tokyo-Osaka corridor | Medium term (2-4 years) |

| Government pressure to lower consumer prices via infrastructure sharing | +0.8% | National, rural focus | Long term (≥ 4 years) |

| Rural-coverage subsidies under Digital Garden City Nation initiative | +0.6% | 1,000+ municipalities | Medium term (2-4 years) |

| Sale-and-leaseback transactions unlocking CapEx for Beyond-5G upgrades | +0.5% | National | Short term (≤ 2 years) |

| Enterprise private-network boom demanding rooftop sites | +0.7% | Kanto-Kansai belt | Medium term (2-4 years) |

| Drone-based inspection mandates lowering OPEX and downtime | +0.3% | National | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Aggressive 5G Macro-Cell Densification Targets by MNOs

Japan’s operators pursue nationwide 5G coverage with unprecedented base-station counts. KDDI and SoftBank plan 100,000 sites each by 2030 through a joint build that already delivers JPY 120 billion in CapEx savings per carrier. [1]Pipeline Magazine Staff, “KDDI and SoftBank Scale 5G Through Joint Build,” pipeline-pub.comNTT DOCOMO aims to exceed 90% population coverage across all 1,741 municipalities, forcing site density multipliers in dense wards where 5G’s shorter propagation range demands 3-5× more cells than 4G. Dual-band strategies that pair 700 MHz-1.7 GHz coverage layers with high-capacity 3.7 GHz and 28 GHz bands diversify siting requirements. MIC’s spectrum coordination rules under the Radio Wave Law sustain orderly roll-outs, while tower firms refine design templates to shorten permitting cycles.

Government Pressure to Lower Consumer Prices via Infrastructure Sharing

MIC’s Plan for Promoting Competition in the Mobile Communications Market centers on cost reduction through network sharing. National policy now rewards co-location and shared civil works, delivering up to 15% tax credits for rural deployments under the 5G Introduction Promotion Tax scheme. KDDI and SoftBank exemplify this mandate; their collaboration accelerates coverage yet preserves retail competition by keeping spectrum and customer interfaces separate. Joint-venture TowerCos, boosted by regulatory clarity, are posting a 44.09% CAGR as operators re-allocate capital from steel to services. Rural mandates under Digital Garden City Nation further hard-wire shared builds where single-operator economics remain challenging.

Rural-Coverage Subsidies under the Digital Garden City Nation Initiative

The Cabinet-level program earmarks substantial subsidies and depreciation allowances to close rural gaps across 1,000 municipalities. Tax incentives of 15% for qualifying tower spend and 30% special depreciation fuel a multiyear pipeline of macro-cells in depopulating prefectures. Municipal digital-service ambitions—including real-time dashboards and cloud migrations—raise backhaul requirements, anchoring tower demand even where subscriber growth stagnates. The Digital Agency’s well-being indicator platform, using survey data from 668 local governments, exemplifies rural bandwidth uptake.[2]Digital Agency, “Digital Garden City Nation—Implementation Status 2025,” digital.go.jp Non-terrestrial trials featuring high-altitude platforms at Expo 2025 complement ground towers but do not displace them, reinforcing site construction in rugged terrain.

Enterprise Private-Network Boom Demanding Rooftop Sites

Manufacturing, rail and port operators deploy local 5G on premises, catalyzing rooftop demand. NEC’s Kakegawa factory reported 30% efficiency gains after adopting private 5G, illustrating quantified ROI. Enterprises tap dedicated 4.6-4.9 GHz and 28 GHz bands, avoiding public-network contention and favoring compact rooftop masts that dodge ground-space limitations. Rooftop share already stands at 55.44% and climbs at 4.47% CAGR. Building-code compliance encourages lighter mounting hardware, while neutral-host providers bundle spectrum, radios and managed services, easing adoption for factories unfamiliar with telco operations. Railway and port estates, rich in real estate, emerge as the next growth nodes for rooftop tenancy.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Strict zoning height limits in urban wards | -0.9% | Tokyo, Osaka metro | Long term (≥ 4 years) |

| Shrinking population reducing long-term mobile traffic growth | -0.7% | National, rural pref. | Long term (≥ 4 years) |

| Yen weakness inflating imported steel & RF components | -1.1% | Import-dependent nation | Short term (≤ 2 years) |

| High exposure to seismic retro-fit costs | -0.5% | Earthquake zones | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Strict Zoning Height Limits in Urban Wards

Municipal district plans overlay national Building Standards Law, restricting tower heights via slant-plane controls to preserve skyline aesthetics. Telcos confront lengthy permitting as every ward enforces bespoke rules. Operators respond with concealed antennas, pole-top small cells and even underground base stations trialed by KDDI. Camouflaged monopoles priced at USD 5,000-20,000 gain favor, yet engineering complexity adds weeks to construction timelines. Floor-area ratio constraints also narrow space for equipment shelters, pushing suppliers to develop integrated radio/antenna units that mount flush to walls, reducing visual impact while maintaining coverage.

Yen Weakness Inflating Imported Steel and RF Components

The yen’s 50% slide versus USD between 2021-2024 lifted imported steel and antenna prices, inflating build costs by double digits. [3]TowerXchange Editorial Team, “Currency Headwinds and Tower CapEx in Japan,” towerxchange.comImport price pass-through shows 30% correlation over 13 months, making site budgets highly sensitive to FX moves. Steel volatility meets semiconductor tightness, compounding pressures on RF chain pricing. Tower builders pass risk via escalation clauses or hedge in forward markets, but smaller contractors lack scale to hedge, prompting bid inflation. Unpredictable BOJ intervention complicates multi-year CapEx planning, encouraging operators to recycle existing structures, intensify sharing and adopt modular designs that defer steel outlays.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Ownership: Asset-Light Strategies Drive Joint Venture Growth

The Japan telecom towers market size for ownership structures reached USD 1.59 billion in 2025, with MNO-captive models controlling 58.42% share. Despite this dominance, the joint-venture TowerCo segment is projected to compound at 41.85% through 2031, the fastest trajectory among all categories. KDDI-SoftBank’s shared build sets the blueprint, pooling passive assets while safeguarding spectrum strategies. DigitalBridge’s USD 631 million privatization of JTower underscores escalating investor appetite for cash-flow-backed tower real estate. Operators continue to divest via sale-and-leaseback; Rakuten Mobile’s JPY 150-300 billion transaction with Macquarie typifies capital recycling for Beyond-5G upgrades. Policy nudges from MIC further validate this shift, granting tax incentives and streamlined approvals to shared-ownership entities.

Lease economics exert downward pressure on cash OPEX, freeing carriers to fund Open RAN, edge compute and network slicing. Consequently, the Japan telecom towers market witnesses rising tenancy ratios as neutral hosts aggregate tenants and pursue 1.5× tenancy by 2030. Yet captive portfolios linger where height or power constraints make sharing unwieldy, especially in coastal and mountainous zones requiring bespoke engineering. Independent TowerCos leverage flexible covenants, decoupling tower valuation from subscriber ARPU trends and thus attracting infrastructure funds seeking inflation-linked returns. Despite complex vendor-lock clauses, the regulatory stance favors further asset-light pivoting, implying sustained double-digit revenue growth for joint-venture platforms.

By Installation: Rooftop Deployments Accelerate with Enterprise 5G

Rooftop solutions captured 55.15% of Japan telecom towers market share in 2025, translating to a Japan telecom towers market size of USD 1.5 billion. Factories, malls and transport nodes prefer roofline masts, circumventing scarce ground plots in Japanese metros. Local 5G spectrum liberalization in 4.6-4.9 GHz fosters corporate deployments, with Sumitomo, NEC and rail operators piloting production-grade private networks. Steady 4.32% CAGR reflects growing industrial digitalization and tighter zoning curbs that impede new ground towers. In rural prefectures, ground-based lattice or guyed structures remain essential for macro coverage and disaster resilience; nevertheless, rooftop adoption even in smaller cities rises as mixed-use real estate expands.

Rooftop designs exploit lighter monopoles and wall-mount panels, lowering seismic loads and expediting permits under the Building Standards Law. Tenants negotiate multi-utility real estate contracts bundling HVAC and fiber, enhancing host revenue streams. Neutral-host models thrive on rooftops within shopping centers, where JTOWER’s shared radio units trimmed power draw by 35% in April 2025. Height restrictions still apply, prompting adjustable pole systems that retract for typhoon safety. Looking forward, rooftop micro-cells will knit into 6G-ready architectures supporting sub-THz bands, extending the rooftop growth curve beyond the current forecast period.

By Fuel Type: Renewable Energy Surge Amid Grid Reliability Mandates

Grid/diesel hybrids dominated with 70.55% Japan telecom towers market share in 2025, equal to a Japan telecom towers market size of USD 1.92 billion. Robust diesel backup is critical in earthquake-prone Japan where telecoms are lifelines during outages. Nonetheless, renewable-powered sites are scaling at 15.62% CAGR, propelled by operator ESG targets, high retail electricity tariffs and maturing battery economics. Rakuten Mobile’s long-term solar PPAs with Photon Capital illustrate the commercial feasibility of zero-carbon sites. MIC regulations accept hybrid micro-grids incorporating photovoltaic arrays and lithium-ion storage provided runtime meets emergency service thresholds, easing integration hurdles.

Decentralized solar plus battery reduces OPEX after year three and shelters operators from yen-driven imported diesel costs. Shared sites magnify returns as one array serves multiple tenants, compressing payback periods further. While typhoon resilience poses design challenges, frameless PV modules and hurricane clips mitigate panel loss. Hydrogen fuel-cell pilots led by NTT Anode open longer-term pathways toward diesel displacement. Over the forecast window, renewable share could double if carbon pricing accelerates, yet diesel generators will persist as compliance-mandated secondary power across critical sites.

By Tower Type: Stealth Solutions Navigate Urban Constraints

Monopoles delivered 40.05% market share in 2025, favored for their compact footprint and rapid erection. Stealth or concealed towers, however, are climbing at 5.78% CAGR, mirrored by city halls tightening visual ordinances. Camouflaged pine-tree designs or antenna-in-flagpole concepts command premiums but secure quicker approvals. KDDI’s underground base-station prototype reveals an extreme response to height limits, hiding radios beneath sidewalks while venting passive cooling through manholes. Lattice structures dominate rural spans where multi-operator panels stack vertically, optimizing wind loading for multi-tenant revenue.

Guyed masts remain niche, reserved for sparsely populated valleys where land is abundant and capital budgets lean. Stealth solutions leverage composite materials to minimize weight and simplify seismic anchoring, cutting construction time by 20%. Concealed radiators integrated into building facades appeal to landlords seeking visual harmony. This aesthetic imperative drives co-development with architects, creating a secondary services market for design consultancies. Over the outlook, demand for urban stealth options will intensify as mmWave densification shifts focus to street-level deployments requiring elegant integration into the built environment.

Geography Analysis

Japan’s telecom tower landscape clusters along the Tokyo-Osaka industrial megaregion, which hosts the bulk of the nation’s 194 million mobile subscriptions and posts the highest traffic density. Urban wards enforce strict slant-plane zoning that compresses tower heights, steering operators toward compact monopoles, concealed poles and rooftop micro-cells. Stealth installs are thus most pronounced in Shinjuku, Minato and Chuo districts, where skyline preservation rules tighten each year. Concurrently, suburban rings such as Saitama and Chiba witness brisk ground-based expansion as land availability permits taller lattice builds that balance height limits and seismic codes.

Rural prefectures—including Hokkaido, Shimane and Kochi—benefit from the Digital Garden City Nation program that subsidizes up-to-15% of tower CapEx and accelerates fiber backhaul grants. These incentives counterbalance declining population densities and lower ARPUs, ensuring service parity with urban peers. Non-terrestrial demonstrations slated for Expo 2025 in Osaka showcase high-altitude platform stations complementing terrestrial towers but also highlight the continued requirement for dense ground networks, especially to offload local traffic surges at events. Mountainous terrain and typhoon exposure in Kyushu trigger higher wind-load specifications, inflating build costs by 8-12% relative to flat Kanto plains.

Enterprise private-network clusters map to the Kanto-Kansai manufacturing belt. Aichi and Shizuoka prefectures, rich in automotive plants, pioneer local 5G, feeding rooftop tower demand. Port zones in Tokyo Bay and Osaka Bay integrate private 5G for automated cranes, spawning high-capacity rooftop and pole-top sites connected via redundant fiber rings. Meanwhile, Tohoku’s reconstruction push after 2011 sustains fresh macro-cell builds tied to regional resilience mandates. Overall, geography shapes a multi-speed market: urban stealth densification, industrial rooftop proliferation and subsidized rural macro-cell expansion, all underpinned by a nationwide orientation toward infrastructure sharing.

Competitive Landscape

Japan’s telecom tower arena shows moderate concentration, with the four national MNOs still owning most structures yet ceding ground to emerging neutral hosts. JTower, acquired by DigitalBridge for USD 631 million in 2024, now steers the independent cohort with roughly 7,000 sites, focusing on indoor DAS and urban rooftop portfolios. KDDI and SoftBank’s joint build forms a quasi-duopoly in shared passive assets, granting both carriers scale efficiencies while limiting the addressable pie for independent TowerCos. NTT DOCOMO experiments with Open RAN multivendor stacks that lower upgrade costs and make its captive towers more adaptable, potentially extending captive lifespans.

Investment funds view tower real estate as a hedge against Japan’s low-yield bond environment, prompting fresh capital inflows. Sale-and-leaseback deals, epitomized by Rakuten Mobile’s JPY 150-300 billion arrangement with Macquarie, allow operators to finance radios and cloud-native cores while off-loading depreciation risk. Technology differentiation becomes a competitive lever; drone-based inspections supplied by Skyller trim maintenance OPEX, and artificial-intelligence-driven tilt optimization piloted by NTT Communications shrinks energy draw. Vendors scramble to supply lightweight monopole kits certified for Japan’s stringent seismic zone, giving domestic steel fabricators an edge over import-reliant rivals amid yen weakness.

Regulatory complexity forms a competitive moat. Experience navigating MIC’s Radio Wave Law, municipal zoning hearings and environmental assessments grants incumbents an approval-cycle advantage that new entrants must bridge through local partnerships. While infrastructure sharing boosts overall tenancy, it can also erode pricing power as TowerCos barter lower rents for longer tenures. Looking forward, neutral hosts targeting enterprise verticals—factories, rails, ports—will likely gain share, as carriers prefer opex-based solutions that drive service revenue without bloating balance sheets. Still, top-line growth hinges on sustained 5G densification and nascent 6G testbeds slated for 2029-2030.

Japan Telecom Towers Industry Leaders

NTT DOCOMO

KDDI

SoftBank Corp.

Rakuten Mobile

JTower

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: JTOWER deployed shared 5G-compatible equipment at Mitsui Shopping Park LaLaport Anjo, cutting power use by 35% with its new modular shared-unit design.

- April 2025: Obayashi Corporation activated local 5G for autonomous cable-crane operations at the Shin-Maruyama Dam site.

- April 2025: Tokyo Boeki Techno-System and Net One Systems launched a LiDAR-enabled digital-twin project over local 5G in manufacturing settings.

- March 2025: SONIX began a 5G-based in-vehicle content delivery pilot, examining network-capacity stress factors.

Japan Telecom Towers Market Report Scope

Telecommunication towers come in various structures, such as monopoles, tripoles, lattice towers, guyed towers, self-supporting towers, poles, masts, and similar configurations. These towers house one or more telecommunication antennas, facilitating radio communications. They can be situated on the ground or atop a building, often including storage for equipment and electronic components. While these towers don't need constant staffing, they do require periodic maintenance. Driven by the rollout of 5G infrastructure, the expansion of telecom towers is poised to persist during the forecast period.

The Japanese telecom towers market is segmented by ownership (operator-owned, private-owned, and MNO captive), installation (rooftop and ground-based), and fuel type (renewable and non-renewable). The market sizes and forecasts are provided in terms of volume (units) for all the above segments.

| Operator-owned |

| Independent TowerCo |

| Joint-Venture TowerCo |

| MNO Captive |

| Rooftop |

| Ground-based |

| Renewable-powered |

| Grid/Diesel Hybrid |

| Monopole |

| Lattice |

| Guyed |

| Stealth / Concealed |

| By Ownership | Operator-owned |

| Independent TowerCo | |

| Joint-Venture TowerCo | |

| MNO Captive | |

| By Installation | Rooftop |

| Ground-based | |

| By Fuel Type | Renewable-powered |

| Grid/Diesel Hybrid | |

| By Tower Type | Monopole |

| Lattice | |

| Guyed | |

| Stealth / Concealed |

Key Questions Answered in the Report

How large is the Japan telecom towers market in 2026?

It is valued at USD 2.82 billion, with a forecast to reach USD 3.35 billion by 2031.

What CAGR is expected for tower revenue through 2031?

The market is projected to grow at a 3.55% CAGR during 2026-2031.

Which installation type leads new deployments?

Rooftop towers lead with 55.15% share and a 4.32% CAGR, driven by enterprise private-network roll-outs.

Why are joint-venture TowerCos expanding quickly?

Regulatory incentives and operator CapEx savings fuel a 41.85% CAGR for joint-venture structures.

How does yen weakness affect tower economics?

A 50% yen slide versus USD since 2021 has raised imported steel and RF costs, squeezing margins and lengthening payback periods.

What role do renewables play in powering Japanese towers?

Renewable-powered sites are scaling at 15.62% CAGR as operators pursue sustainability targets and hedge electricity costs.

Page last updated on: