South Korea Smart Home Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

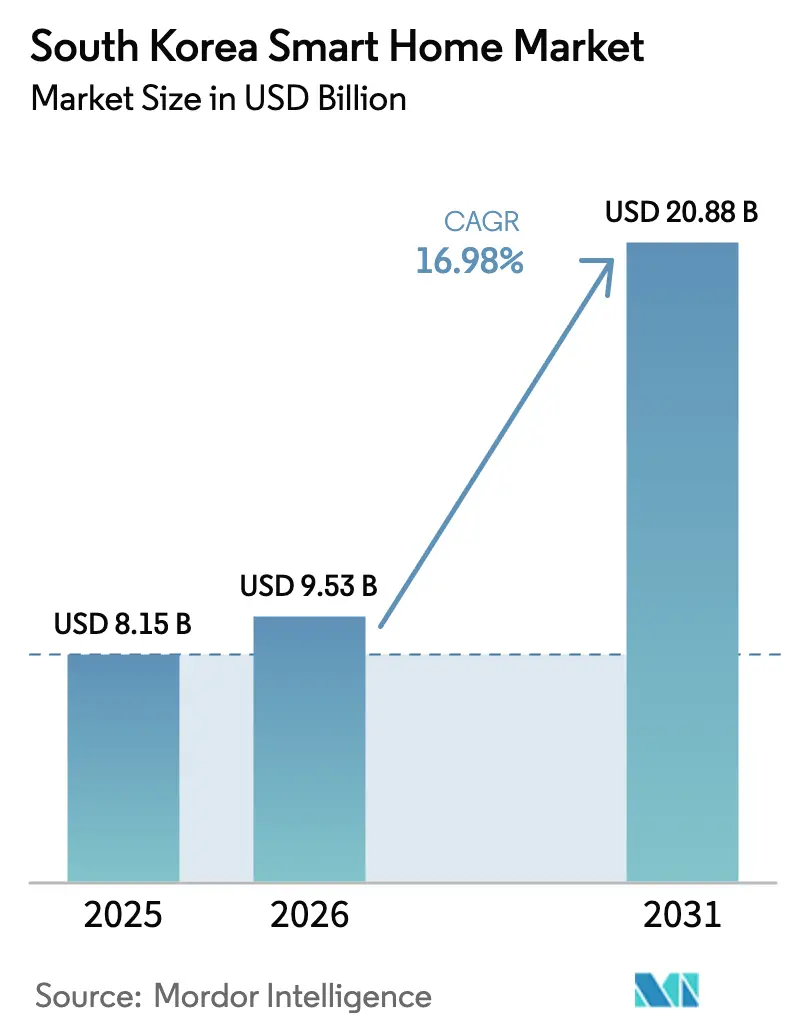

| Base Year Market Size (2025) | USD 8.15 Billion |

| Market Size (2026) | USD 9.53 Billion |

| Market Size (2031) | USD 20.88 Billion |

| Growth Rate (2026 - 2031) | 16.98% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Korea Smart Home Market Analysis by Mordor Intelligence

The South Korea Smart Home market size is expected to grow from USD 8.15 billion in 2025 to USD 9.53 billion in 2026 and is forecast to reach USD 20.88 billion by 2031 at 16.98% CAGR over 2026-2031. The market’s upward trajectory reflects Korea’s first-mover advantage in 5G deployment, tight integration between consumer electronics manufacturing and domestic demand, and early regulatory clarity under the AI Framework Act. Chaebol ecosystems combine hardware, software, and services, creating high switching costs and locking in households to single-brand platforms. Nationwide concern over summer heatwaves and rising electricity bills is accelerating the uptake of connected energy-saving devices [1]Ki-hwan Kim, “Koreans Keep an Eye on Electricity Bills as Temperatures Head Toward 40 °C,” koreajoongangdaily.joins.com. Builder pre-installation in premium apartments provides plug-and-play convenience, enlarging the addressable base beyond tech-savvy early adopters. Telecommunications operators are pivoting toward high-margin “techco” services that bundle AI agents with private 5G, positioning connectivity as a managed subscription rather than a one-time hardware transaction.

Key Report Takeaways

- By product type, Smart Appliances led with a 23.55% revenue share of the South Korean Smart Home market in 2025, while energy management is advancing at an 18.41% CAGR through 2031.

- By connectivity technology, Wi-Fi retained a 40.72% share in 2025, while Cellular LPWAN is projected to rise at a 18.77% CAGR through 2031.

- By installation type, DIY/Self-Install held a 46.85% share in 2025, whereas new-build integrated solutions are expanding at an 17.66% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

South Korea Smart Home Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising concern about home security and safety | +3.2% | National, Seoul metro strongest | Short term (≤ 2 years) |

| Advances in IoT, AI and voice-controlled assistants | +4.1% | Technology-forward urban centers | Medium term (2-4 years) |

| Government-backed smart-apartment and smart city programs | +2.8% | Songdo, Busan, Daegu pilots | Medium term (2-4 years) |

| Senior-care and aging-population demand for health-monitoring homes | +3.5% | Rural and suburban regions | Long term (≥ 4 years) |

| 5G/indoor small-cell rollout enabling low-latency device ecosystems | +2.9% | Urban cores first | Short term (≤ 2 years) |

| Builder pre-installation in premium apartments amid real-estate competition | +1.8% | Major metros | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Concern About Home Security and Safety

Smart door locks, AI video analytics, and biometric access are proliferating after well-publicized break-ins, making security the typical entry point for first-time adopters. Hybrid cloud-edge architectures deliver real-time threat alerts while maintaining data residency under domestic privacy rules. Municipal “safe-city” initiatives reinforce consumer confidence by showcasing vetted solutions in public housing. Strong demand from working parents and single-person households drives bundled sales that later expand into comfort and energy categories.

Advances in IoT, AI and Voice-Controlled Assistants

Samsung’s on-device NPU, SK Telecom’s HyperCLOVA X, and Naver’s Clova stack localize voice services for Korean dialects, reducing latency versus foreign cloud assistants [2]SK Telecom, “Press Release,” sktelecom.com. Edge AI predicts routines, shifting the user experience from manual control to autonomous orchestration. Semiconductor vertical integration lowers BOM cost, enabling mass-market SKUs that embed machine learning into rice cookers, air purifiers, and washing machines. Continuous software upgrades keep installed bases current, mitigating obsolescence fears and strengthening the South Korea Smart Home market lock-in.

Government-Backed Smart-Apartment and Smart-City Programs

The Ministry of Land’s smart-apartment certification subsidizes IoT installations during construction, guaranteeing baseline functionality and cybersecurity compliance. Songdo’s mixed-use pilot validates city-scale energy optimization, creating reference models for developers nationwide. Tax incentives and relaxed zoning accelerate project approvals when builders adopt standardized smart infrastructure. Public investment de-risks private capital, sustaining a pipeline of new “model homes” that showcase the latest South Korea Smart Home market capabilities to prospective buyers.

Senior-Care and Aging-Population Demand for Health-Monitoring Homes

Ambient sensors embedded in lighting, floor mats, and bathroom fixtures generate real-time anomalies that caregivers monitor via AI dashboards. Fall detection and medication reminders integrate with national emergency-response centers, shortening dispatch times. Insurers now reimburse qualified devices under preventive-care programs, reducing hospital readmissions and fueling recurring service revenues. Multi-stakeholder purchasing, adult children buying systems for parents, broadens the payer base and lifts overall South Korea Smart Home market adoption.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Complex installation and set-up | -2.1% | National, seniors hardest hit | Short term (≤ 2 years) |

| Interoperability/ecosystem fragmentation | -1.8% | Multi-brand households | Medium term (2-4 years) |

| Regulatory uncertainty under Korea’s new AI Framework Act | -1.4% | All IoT categories | Short term (≤ 2 years) |

| Rising cyber-insurance premiums for unmanaged smart devices | -0.9% | Device-dense urban areas | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Complex Installation and Set-Up

Fragmented protocols and legacy wiring deter non-tech-savvy segments, forcing reliance on costly professional installers that are scarce outside Seoul. Failed DIY attempts result in product returns, eroding retailer margins and slowing repeat purchases. To counter, vendors bundle color-coded wiring harnesses, NFC tap-to-pair onboarding, and 24/7 remote support. Yet perceived complexity still subtracts from the South Korea Smart Home market CAGR in the near term.

Interoperability/Ecosystem Fragmentation

Proprietary hubs from Samsung, LG, and telecom carriers limit cross-brand functionality and increase switching costs. The Home Connectivity Alliance and Matter protocol promise convergence, but the installed base evolves slowly, keeping consumers locked into siloed ecosystems. Lack of backward compatibility discourages large-scale retrofits, capping the immediate addressable market even as new standards gain mindshare.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Smart Appliances Lead Through Manufacturing Excellence

Smart Appliances commanded 23.55% of South Korea's Smart Home market share in 2025, buoyed by Samsung and LG’s domestic brand equity and export-class R&D pipelines. Converged cooking, laundry, and refrigeration devices embed Wi-Fi and AI routines that auto-optimize energy draw and maintenance cycles. Cross-selling bundles with robotic vacuums and air purifiers lifts household annual spending.

Energy Management is the fastest-growing cohort, forecast to rise at 18.41% CAGR by 2031. Smart meters, demand-response plugs, and AI thermostats gain traction as Korea Electric Power Corporation phases dynamic tariffs into residential billing. Consumers accept device-driven curtailment programs that trade minor comfort concessions for bill credits, enlarging the South Korean Smart Home market size for energy services.

By Connectivity Technology: Wi-Fi Dominance Faces 5G Challenge

A 40.72% share in 2025 keeps Wi-Fi the primary backbone for multimedia and appliance control, but private 5G’s 18.77% CAGR threatens incumbency by offering ultra-low-latency, interference-resistant links suitable for security cameras and robotic assistants. SK Telecom’s bundled home 5G gateways shift bandwidth from consumer routers to edge micro-cells, promising carrier-grade SLAs.

ZigBee, Z-Wave, Thread, and UWB fill niche roles where battery life and spatial awareness trump raw throughput. Multi-radio SoCs now ship in mass-market appliances, letting devices float across protocols without user intervention. This seamless orchestration reduces friction and underpins the long-run scalability of the South Korean Smart Home market size.

By Installation Type: DIY Preference Yields to Professional Integration

DIY/Self-Install solutions captured 46.85% share in 2025 as digitally fluent owners sourced devices online and configured them via smartphone apps. However, New-Build Integrated systems are set to outpace at 17.66% CAGR, with developers embedding smart hubs, sensors, and ceiling-mounted Wi-Fi in condominiums to command premium pricing.

Professional Install maintains relevance in bespoke retrofits and high-end villas demanding custom scenes, hidden cabling, and central audiovisual racks. Service providers now market subscription-based post-installation support, security monitoring, firmware patching, and predictive maintenance, which turns one-off projects into annuity streams, boosting the lifetime value of each South Korean Smart Home market customer.

Geography Analysis

Greater Seoul accounts for the lion’s share of deployments thanks to high disposable incomes, dense broadband coverage, and aggressive marketing by electronics flagships. Busan and Daegu follow as secondary tech hubs where smart city pilots demonstrate ROI to municipal leaders. Suburban counties adopt later but often leapfrog with 5G-native architectures that integrate farm-to-door cold-chain monitoring and rural tele-health.

Housing stock age dictates installation type: new metro high-rises integrate backbone cabling, while rural hanok renovations rely on battery-powered mesh devices. Consumer priorities vary; urban millennials emphasize convenience and entertainment, whereas rural households prioritize elder safety. Nevertheless, uniform national enforcement of the AI Framework Act ensures privacy and cybersecurity baselines regardless of location.

Inter-regional competition ignites “smart apartment” branding wars, prompting local governments to fast-track building approvals for projects that meet IoT certification. This virtuous cycle accelerates the diffusion curve and expands the South Korea Smart Home market to outlying provinces, narrowing the urban-rural adoption gap by 2028.

Competitive Landscape

Market concentration is moderate. Samsung SmartThings anchors a vertically integrated ecosystem spanning phones, TVs, appliances, and cars, while LG’s ThinQ leverages cross-product AI to retain customers [3]Samsung Electronics, “Samsung’s ‘AI for All’ Vision Unveiled at CES 2024,” news.samsung.com. Google and Amazon remain niche due to limited Korean-language content, but Matter compliance signals renewed competition for device neutrality.

Telecom incumbents SK Telecom, KT, and LG Uplus transform into platform operators, bundling AI agents, cloud gaming, and security monitoring on monthly plans that embed hardware financing. Partnerships with automakers extend smart home boundaries to the vehicle cabin, allowing HVAC pre-conditioning and door unlock commands via dashboard infotainment.

HT Beyond streamlines apartment-wide integration; Robotom injects AI into modular furniture; niche firms craft ondol-compatible HVAC controllers. Venture capital inflows and public R&D grants keep the innovation pipeline active, but distribution remains dominated by chaebol retail networks that set de facto standards for the South Korean Smart Home market.

South Korea Smart Home Industry Leaders

Samsung Electronics Co., Ltd.

LG Electronics Inc.

SK Telecom Co., Ltd.

LG Uplus Corp.

Signify N.V.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Samsung Electronics unveiled its Smart Modular Home at IFA 2025, featuring AI-enabled appliances and unified SmartThings Pro connectivity.

- July 2025: HT Beyond raised KRW 7 billion (USD 5.3 million) for its BYEBY integration platform.

- May 2025: Robotom secured KRW 2.3 billion (USD 1.7 million) in government funding for multimodal smart furniture solutions.

- February 2025: Samsung and Kia integrated SmartThings Pro into Kia’s Platform Beyond Vehicles for remote workspace control.

- January 2025: Samsung announced commercial launch of Ballie AI home robot by June 2025.

South Korea Smart Home Market Report Scope

A smart home refers to a set of integrated and networked devices that automate different functions within a home and can communicate with each other and with a centralized control interface. The prominent purpose of this type of system is to enhance comfort, safety, energy efficiency, and management of household resources.

The South Korean smart home market is segmented by product type (comfort and lighting, control and connectivity, energy management, home entertainment, security, smart appliances, and HVAC control) and technology (Wi-Fi, Bluetooth, and other technologies). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Comfort and Lighting |

| Control and Connectivity |

| Energy Management |

| Home Entertainment |

| Security |

| Smart Appliances |

| HVAC Control |

| Wi-Fi |

| Bluetooth |

| ZigBee |

| Z-Wave |

| Cellular LPWAN (NB-IoT/LTE-M) |

| Other Technologies (Thread, UWB, PLC, etc.) |

| New-Build Integrated |

| Professional Install |

| DIY/Self-Install |

| By Product Type | Comfort and Lighting |

| Control and Connectivity | |

| Energy Management | |

| Home Entertainment | |

| Security | |

| Smart Appliances | |

| HVAC Control | |

| By Connectivity Technology | Wi-Fi |

| Bluetooth | |

| ZigBee | |

| Z-Wave | |

| Cellular LPWAN (NB-IoT/LTE-M) | |

| Other Technologies (Thread, UWB, PLC, etc.) | |

| By Installation Type | New-Build Integrated |

| Professional Install | |

| DIY/Self-Install |

Key Questions Answered in the Report

What is the forecast value of the South Korea Smart Home market in 2031?

The South Korea Smart Home market is projected to reach USD 20.88 billion by 2031.

Which product type currently holds the largest revenue share?

Smart Appliances lead with 23.55% share.

Which segment is growing fastest?

Energy Management is expanding at an 18.41% CAGR to 2031.

How dominant is Wi-Fi versus emerging 5G connectivity?

Wi-Fi holds 40.72% share, but Cellular LPWAN driven by 5G is growing at 18.77% CAGR.

What installation channel is gaining momentum among developers?

New-Build Integrated systems are rising at 17.66% CAGR as apartment builders embed IoT during construction.

Page last updated on: