Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

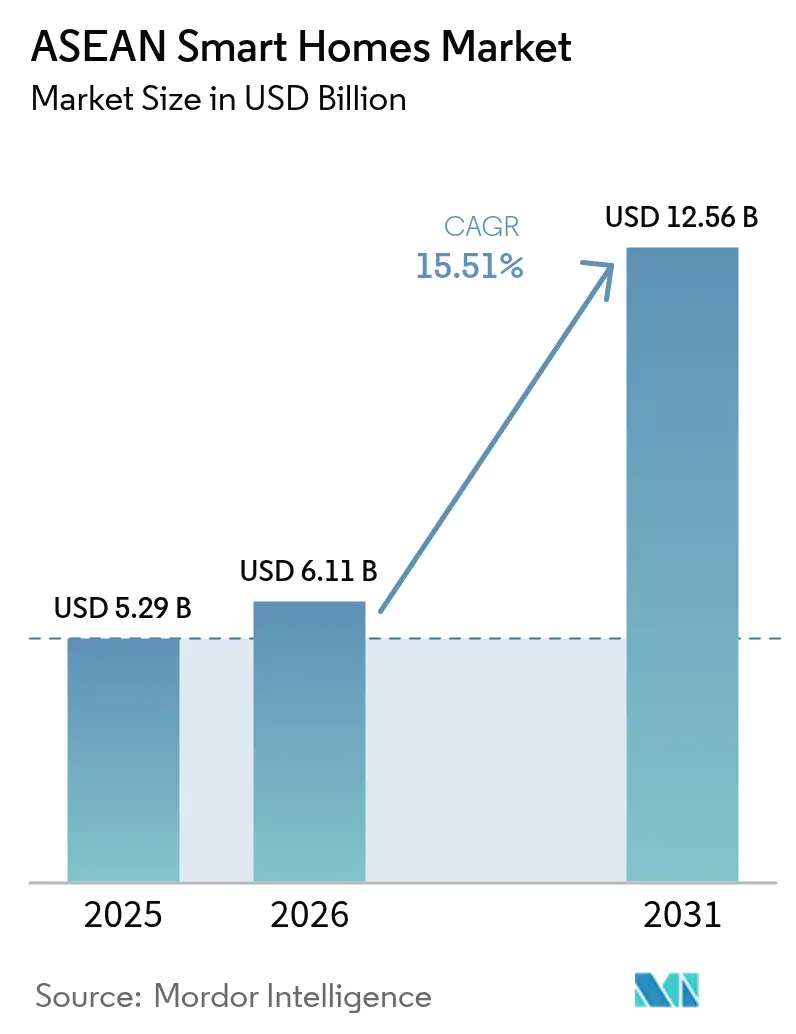

| Base Year Market Size (2025) | USD 5.29 Billion |

| Market Size (2026) | USD 6.11 Billion |

| Market Size (2031) | USD 12.56 Billion |

| Growth Rate (2026 - 2031) | 15.51% CAGR |

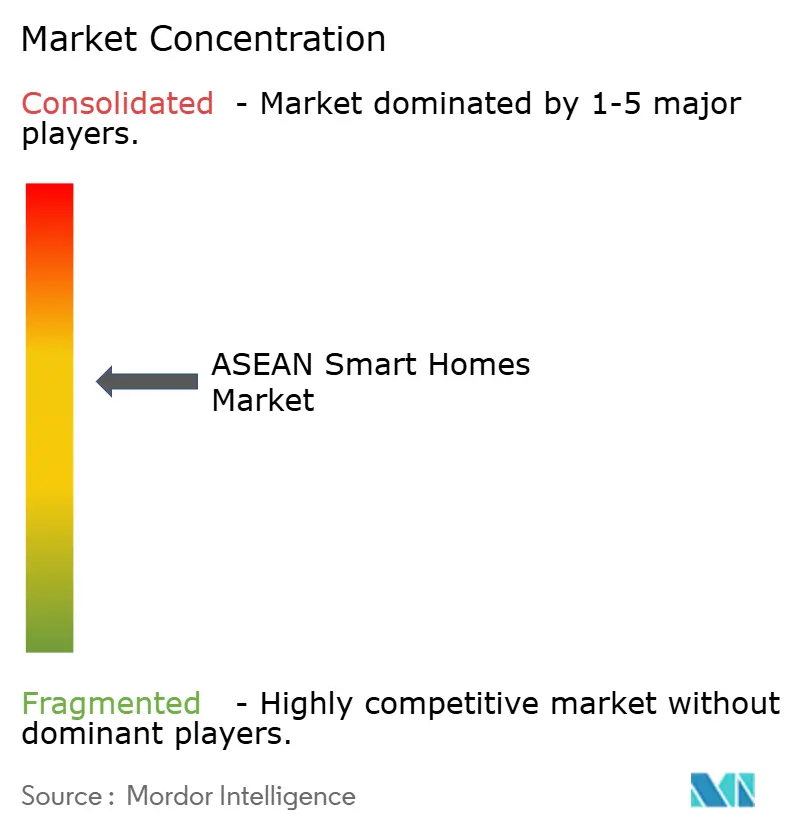

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

ASEAN Smart Homes Market Analysis by Mordor Intelligence

The ASEAN Smart Homes market size is expected to grow from USD 5.29 billion in 2025 to USD 6.11 billion in 2026 and is forecast to reach USD 12.56 billion by 2031 at 15.51% CAGR over 2026-2031. Large-scale cloud investments by Google, AWS, and other hyperscalers are strengthening the backbone that supports device ecosystems and data-intensive services, while government energy-efficiency incentives, 5G rollout, and cross-brand protocol standardization deepen the addressable base for connected living. Infrastructure commitments such as Google’s USD 2 billion Malaysian data-center project and AWS’s USD 5 billion Thailand region lower latency for cloud-managed devices and expand developer toolkits. [1]Amazon Web Services, “AWS Launches Infrastructure Region in Thailand,” press.aboutamazon.com Consumers’ growing focus on safety, comfort, and energy savings, combined with telecom-bundled offerings and the roll-out of Matter-ready hardware, positions the ASEAN smart homes market for broad-based uptake across income tiers and housing types. Interoperability gains reduce vendor lock-in, while aggressive price competition from regional brands compresses margins but widens consumer choice.

Key Report Takeaways

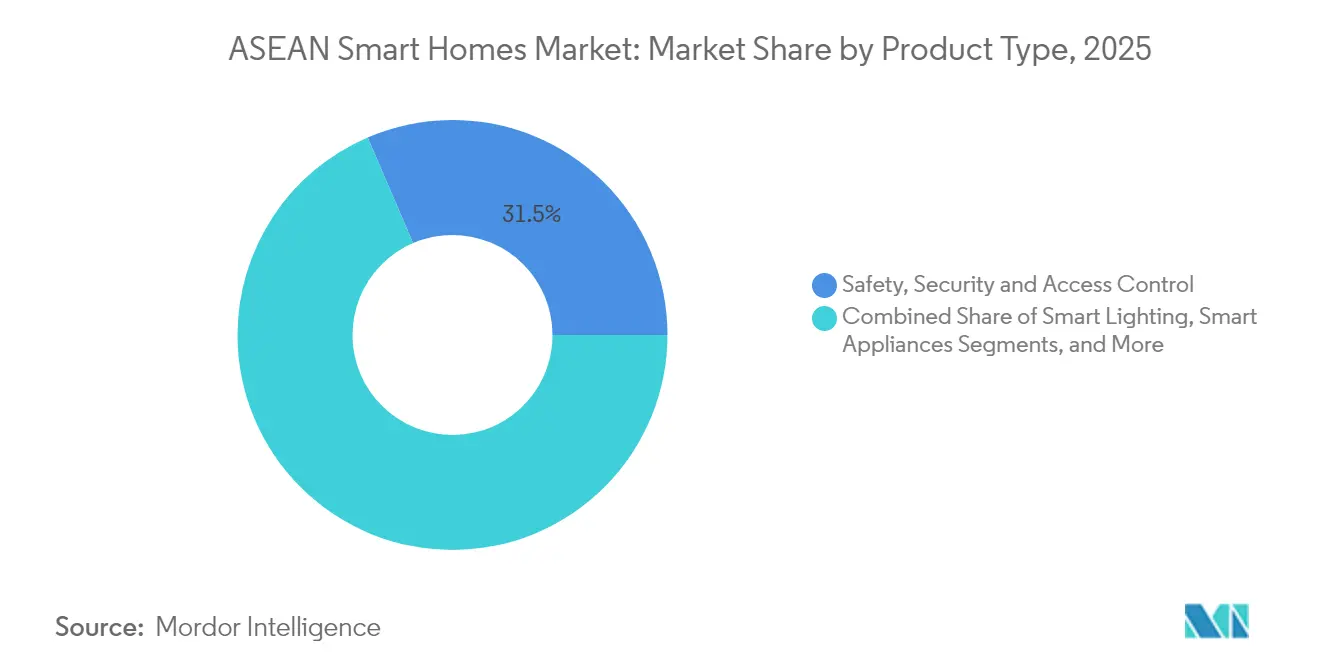

- By product category, safety, security, and access control devices led with 31.45% revenue share in 2025; HVAC and energy-management devices are forecast to expand at a 16.78% CAGR to 2031.

- By communication protocol, Wi-Fi maintained 38.55% of the ASEAN smart homes market share in 2025, while Thread and Matter protocols are projected to grow at 16.55% CAGR through 2031.

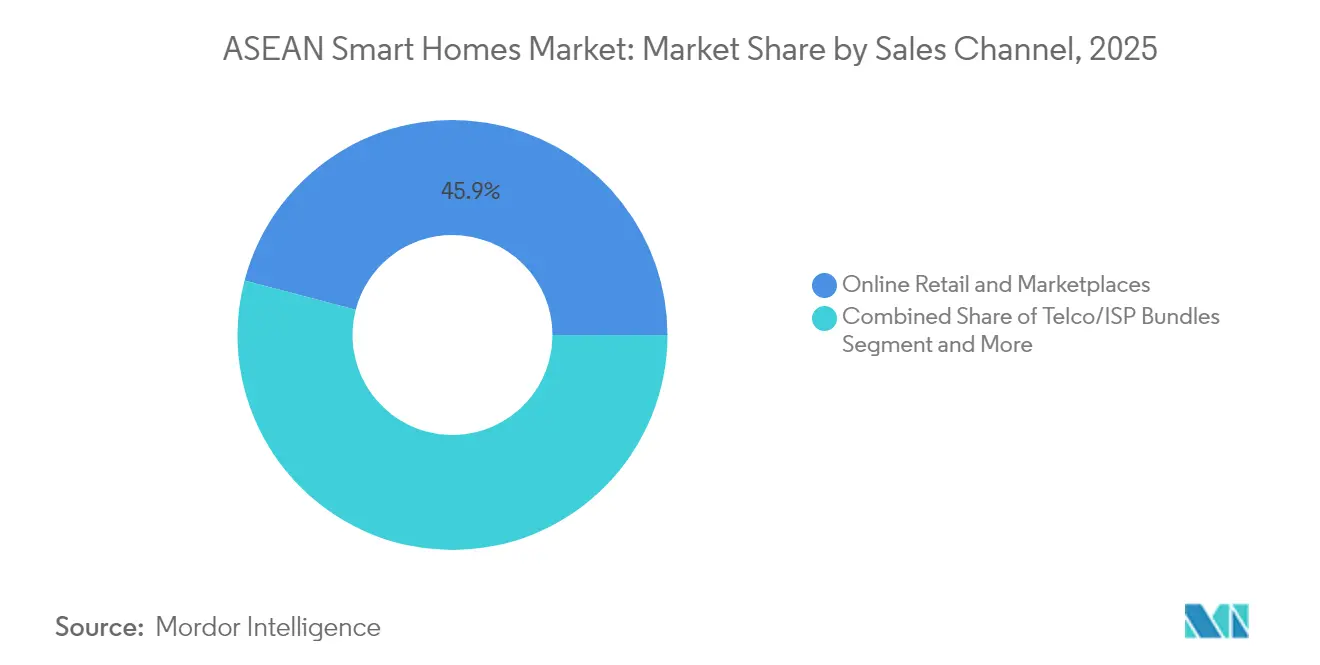

- By sales channel, online retail and marketplaces captured 45.92% share of the ASEAN smart homes market size in 2025; telco/ISP bundles are advancing at a 16.90% CAGR through 2031.

- By installation type, retrofit installations held 59.35% share of the ASEAN smart homes market size in 2025, and new-build integrated solutions are set to expand at 17.02% CAGR between 2026-2031.

- By country, Indonesia commanded 30.55% of the ASEAN smart homes market share in 2025, while Vietnam is forecast to grow at 16.30% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

ASEAN Smart Homes Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government-backed energy-efficiency incentives | +3.2% | Singapore, Thailand, Malaysia with spillover to Indonesia | Medium term (2-4 years) |

| Rising urban middle-class disposable income | +4.1% | Indonesia, Vietnam, Philippines with moderate gains in Thailand, Malaysia | Long term (≥ 4 years) |

| Smartphone and broadband penetration surge | +2.8% | Vietnam, Philippines, Indonesia with established presence in Singapore, Malaysia | Short term (≤ 2 years) |

| Matter protocol enabling cross-brand IoT | +2.3% | Global with early adoption in Singapore, Malaysia | Medium term (2-4 years) |

| Security and safety concerns in dense cities | +1.9% | Singapore, Malaysia, urban centers in Indonesia, Thailand | Short term (≤ 2 years) |

| Telco-bundled IoT subscription models | +1.7% | Indonesia, Thailand, Malaysia with emerging presence in Vietnam | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Government-backed Energy-efficiency Incentives

Singapore’s Climate-Friendly Households Programme gives every HDB household SGD 400 vouchers for energy-efficient appliances and sets an influential benchmark that neighboring markets monitor closely. [2]National Environment Agency, “$300 Climate Vouchers For All HDB Households,” nea.gov.sg Thailand’s Building Energy Code and Malaysia’s National Semiconductor Strategy provide similar regulatory nudges that elevate demand for connected HVAC and energy-management devices. Utilities in multiple countries have begun piloting time-of-use tariffs, rewarding homes equipped with smart thermostats and load controllers. Integration of Home Energy Management Systems into Singapore’s Punggol Northshore estates demonstrates how bake-in infrastructure shortens payback periods and boosts user confidence. Collectively, these measures move smart energy devices from nice-to-have to default specifications, lifting the ASEAN smart homes market outlook for the medium term.

Rising Urban Middle-class Disposable Income

ASEAN’s expanding urban middle class drives a shift from basic appliances to feature-rich, connected products. Vietnam’s home-appliance spend is on course to touch USD 13 billion by 2025, growing over 10% annually. Indonesian developers now position smart homes as standard rather than premium, reinforcing consumer perception that connected living is part of modern housing. Regional firms such as Vietnam’s Lumi, which operates a 6,000 m² IoT factory and serves 70,000 customers, illustrate how localized design, language support, and climate-appropriate hardware create defensible niches against multinational brands. Rising disposable income thus unlocks multi-device purchases and subscription upgrades, increasing lifetime customer value for vendors.

Smartphone and Broadband Penetration Surge

Declining mobile-data tariffs and aggressive fiber roll-outs give ASEAN one of the world’s highest ratios of smartphone use to PC ownership, making phones the de facto smart home hub. Thailand’s IoT market is projected to reach USD 2.19 billion by 2030 as 5G coverage boosts low-latency applications. Vietnam’s ICT sector grew 14% in 2024 to USD 10.2 billion, translating bandwidth upgrades into addressable demand for connected devices. Telkomsel’s IndiHome bundle combines broadband with starter smart-home kits, multiplying attach rates and familiarizing first-time buyers with entry-level automation. As connectivity improves even in secondary cities, device control moves seamlessly from dedicated hubs to smartphones, cutting acquisition friction.

Matter Protocol Enabling Cross-brand IoT

Matter’s promise of interoperability is gaining tangible traction: Google and MediaTek’s Filogic MT7903 chipset integrates native Thread to simplify manufacturer onboarding. LG already enables users to orchestrate 600 million devices through Google Home, exemplifying full-house experiences over single-brand silos. Tuya’s 200-plus Matter certifications and Apple Wallet–ready smart locks show how the protocol lets smaller manufacturers compete on user experience rather than proprietary ecosystems. Clearer standards spur confident purchasing, widening the ASEAN smart homes market as consumers avoid the fear of obsolescence.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront device and install cost | -2.8% | Vietnam, Philippines, Indonesia with moderate impact in Thailand | Short term (≤ 2 years) |

| Ecosystem fragmentation and legacy protocol lock-in | -1.9% | Global with acute impact in markets with diverse device ecosystems | Medium term (2-4 years) |

| Data-localisation compliance costs | -1.2% | Indonesia, Vietnam with emerging requirements in Thailand, Malaysia | Long term (≥ 4 years) |

| Limited certified installer base beyond tier-1 cities | -1.5% | Indonesia, Philippines, Vietnam with moderate impact in Thailand | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront Device and Install Cost

Component inflation and tariff pressures have lifted BOM costs just as price-sensitive ASEAN consumers weigh discretionary upgrades. Manufacturers diversifying production into Malaysia and Vietnam to reduce duty exposure incur short-term capex that can raise end-user prices, slowing adoption in entry-level segments. Bulk-purchase government subsidies partially offset sticker shock, yet many households still start with single devices rather than full-suite installs. Vendors respond with stripped-down SKUs, but these pared features sometimes dilute the seamless experience that anchors recurring revenue models, tempering near-term uptake.

Ecosystem Fragmentation and Legacy Protocol Lock-in

Early adopters who invested in Zigbee-only or proprietary ecosystems face costly transitions to Matter-ready products. Thread 1.4 specification will ease multi-border-router interoperability, but full roll-out is unlikely before 2026, prompting some buyers to defer purchases until the ecosystem stabilizes. Manufacturers must balance firmware support for legacy fleets with R&D spend on multi-protocol chips, stretching engineering budgets and complicating SKU roadmaps. The resulting uncertainty marginally dampens ASEAN smart homes market momentum during the protocol transition window.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Security Dominance Meets Energy Innovation

Safety, security, and access control devices accounted for 31.45% of the ASEAN smart homes market in 2025, reflecting dense urban living and rising consumer focus on personal safety. The segment enjoys strong retrofit demand, as door locks, cameras, and sensors can be installed without structural changes. HVAC and energy-management devices register the quickest pulse, expanding at 16.78% CAGR as utilities launch variable tariffs and governments tie appliance rebates to energy-star ratings. Smart lighting remains an established gateway category; Philips Hue’s AI-enhanced offerings illustrate growing convergence between ambiance, security, and automation. Entertainment hubs face substitution pressure from smartphone-based control panels, yet multi-room setups still favor dedicated bridges for latency-sensitive streaming. Emerging niches such as smart water valves and leak detectors address resilience in water-stressed markets.

Philips Hue’s generative-AI assistant exemplifies how legacy lighting brands extend into whole-home security, while Tuya’s AI-enabled pet-health feeders highlight category blurring that keeps the ASEAN smart homes market vibrant. Competitive intensity varies: mature devices like motion sensors are commoditizing, but AI-enabled cameras and energy-optimizing HVAC controls sustain premium pricing. As user trust in cloud analytics rises, vendors that bundle software dashboards with hardware achieve higher stickiness and recurring service revenue.

By Communication Protocol: Wi-Fi Leadership Faces Thread Challenge

Wi-Fi underpins 38.55% of connected devices in 2025, benefiting from ubiquitous router presence and straightforward user onboarding. Power consumption and congested 2.4 GHz bands, however, open space for Thread’s low-energy mesh to grow at 16.55% CAGR. Zigbee maintains a foothold in cost-sensitive, multi-sensor deployments, especially for lighting. Bluetooth Low Energy powers proximity-based functions such as door unlocks, but rarely manages entire homes. Proprietary sub-GHz protocols persist in long-range security peripherals yet lose share as multi-protocol chips become mainstream. Google–MediaTek’s Thread-native chipset signals the silicon ecosystem’s pivot toward standardized stacks, reducing development overhead and boosting cross-vendor interoperability. Silicon Labs’ support for native Matter-over-Thread smart locks further validates the protocol’s viability in high-security use cases. As chipset prices fall, ASEAN manufacturers integrate dual-band Wi-Fi/Thread radios, granting end users future-proof flexibility.

By Sales Channel: Online Retail Meets Telco Innovation

Online marketplaces retained 45.92% of 2025 sales as consumers leverage price comparison tools and user reviews prior to purchase. Telco/ISP bundles, however, expand fastest at 16.90% CAGR, converting connectivity customers into recurring smart-home subscribers. Operators package routers, cloud storage, and starter kits, lowering upfront hardware cost via installment billing. Brick-and-mortar electronics chains still command premium product displays where experiential demos close high-ticket security or HVAC sales. Value-added integrators thrive in luxury condominiums, offering bespoke design and maintenance contracts. Grab’s decision to ride AWS cloud infrastructure indicates how super-apps may soon cross-sell home automation alongside mobility and payments, widening omnichannel competition. Channel evolution thus intertwines hardware, connectivity, and service layers, expanding the ASEAN smart homes market playbook.

By Installation Type: Retrofit Reality Meets New-Build Vision

Retrofit installations dominate with a 59.35% share in 2025 due to the substantial existing housing stock across Indonesia, the Philippines, and Vietnam. DIY-friendly sensors, smart bulbs, and plug-in energy monitors provide low-risk entry paths. New-build integrated solutions advance at 17.02% CAGR as developers realize smart capabilities differentiate properties and accelerate presales. Indonesia’s 3 million-home construction plan embeds conduits and wired backbones so that smart hubs can be added cost-effectively during finishing. Singapore’s Punggol Northshore estates integrate smart switches and energy dashboards from day one, demonstrating lifetime cost savings that convince financiers and end buyers alike. Falling wireless relay costs now let retrofits mimic many wired benefits, but new builds still capture higher average selling prices as bundled ecosystems present an upgrade-free operating environment.

Geography Analysis

Indonesia leads the ASEAN smart homes market with a 30.55% share in 2025, propelled by a 270 million population and the government’s aggressive housing push. The USD 2.5 billion Qatari investment in affordable housing expands greenfield opportunities where smart wiring can be embedded during construction. Local production of sensors and hubs in Jakarta’s manufacturing corridors lowers logistics costs and buffers tariff shocks, improving price competitiveness. Telkomsel’s IndiHome bundles shift focus from connectivity ARPU to device attach rates, accelerating market penetration.

Vietnam, though smaller, delivers the fastest CAGR at 16.30%, with the smart home market expected to jump from USD 440.2 million in 2026 to USD 804.8 million by 2030. Domestic champions like Lumi tailor products to humid subtropical climates and local language apps, capturing loyalty. Strong ICT growth and a 24% rise in electronics e-commerce sales, even as sellers consolidate, signal sustained digital appetite. Government 5G trials in Hanoi and Ho Chi Minh City will further ease latency concerns for cloud-controlled devices.

Thailand and Malaysia benefit from cloud-region launches by AWS and Google, which reduce latency and support AI-heavy edge applications. AWS’s USD 5 billion Thailand region is expected to generate 11,000 jobs annually and inject USD 10 billion into GDP. Malaysia’s twin Google investments position Kuala Lumpur as a regional data-hub magnet. Singapore, already top in per-capita adoption, pushes sustainability with SGD 400 appliance rebates that drive upgrades rather than first-time installs. The Philippines, while lagging in fixed broadband, benefits from mobile-first device control and growing remittance-driven spending power, pointing to volume upside once fiber penetration improves.

Competitive Landscape

Competitive Landscape

The ASEAN smart homes market remains moderately fragmented, yet ecosystem convergence is steadily consolidating share among platform leaders. Amazon, Google, Samsung, and Xiaomi exploit cloud, voice, and device ecosystems to lock in users. Xiaomi surpassed CNY 100 billion in Q4 2024 IoT and appliance revenue by packaging premium-feel products at mass-market prices, an approach that resonates in cost-sensitive ASEAN segments. Samsung allies with Aqara to integrate sensors into SmartThings, bridging legacy and Matter worlds and easing migration friction.

Regional specialists thrive by localizing for language, climate, and after-sales support. Vietnam’s Lumi deploys in-country assembly and a 150-strong distributor network to ensure rapid installation and maintenance. Thailand’s AiTAN targets commercial estates with 10,000-device deployments through a Tuya partnership that brings white-label flexibility. Channel innovation also shapes competition: ISPs leverage home-grown billing relationships, while e-commerce giants boost private-label device visibility through algorithmic promotions.

Supply-chain diversification remains a moving target; component makers shift capacity from China to ASEAN yet grapple with scale-up timelines that raise input costs in the interim. Firms that secure local assembly incentives in Vietnam or Malaysia gain tariff advantages and faster shipping windows. Strategic moves such as Google’s Thread chipset collaboration with MediaTek and Philips Hue’s AI security launch show how R&D alliances accelerate roadmap execution and create feature moats. Vendors that offer unified dashboards spanning lighting, HVAC, and security win higher customer lifetime value, nudging the market toward ecosystem stickiness and raising competitive barriers.

ASEAN Smart Homes Industry Leaders

Amazon.com Inc. (Ring/Echo)

Google LLC (Nest)

Samsung Electronics Co. Ltd (SmartThings)

Xiaomi Corp. (Aqara)

Signify N.V. (Philips Hue)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Google and MediaTek unveiled the Filogic MT7903 chipset with native Thread support, facilitating energy-efficient multi-protocol connectivity.

- January 2025: AWS opened its Asia Pacific (Thailand) Region after a USD 5 billion outlay, enabling low-latency cloud services for local IoT workloads.

- January 2025: Tuya Smart released a Matter-compatible door lock that supports Apple Wallet home keys and palm-vein recognition.

- January 2025: Philips Hue debuted AI-powered lighting and smoke-alarm sound detection features to deepen its security proposition.

- December 2024: Grab chose AWS as its preferred cloud provider to scale mobility, delivery, and fintech services across eight ASEAN countries.

- October 2024: Google began construction of a USD 2 billion data center in Selangor, Malaysia, with a projected USD 3.2 billion economic impact.

ASEAN Smart Homes Market Report Scope

Smart homes automate their infrastructure, lighting, security, heating, ventilation, air conditioning, and energy management. In a smart home, devices can be controlled remotely from anywhere in the world via the internet, using a mobile or networked device. These homes connect devices through the Internet, allowing users to manage functions like security access, temperature, lighting, and home theatre. Leveraging technology, smart homes enhance building efficiency, sustainability, safety, and cost-effectiveness. These solutions integrate into the broader IoT and connected sensor ecosystem.

Smart home technology enhances building efficiency, sustainability, safety, and cost-effectiveness. These solutions integrate into a broader ecosystem of IoT and connected sensors. This study delves into the smart home market, focusing on five key ASEAN nations: Malaysia, Thailand, Vietnam, Singapore, and Indonesia, and further categorizes them by product type.

The study encompasses various product types, including Lighting Solutions, Energy Management Systems, Security Systems, Connectivity Enhancements, Home Entertainment Systems, and Smart Appliances.

By Product Type

| Smart Lighting |

| HVAC and Energy-Management Devices |

| Safety, Security and Access Control |

| Smart Appliances |

| Entertainment and Connectivity Hubs |

| Water and Utility-Management Devices |

By Communication Protocol

| Wi-Fi |

| Zigbee |

| Bluetooth/BLE |

| Z-Wave |

| Thread and Matter |

| Proprietary/Others |

By Sales Channel

| Online Retail and Marketplaces |

| Telco/ISP Bundles |

| Home-Improvement and Electronics Stores |

| Value-added Service Integrators |

By Installation Type

| Retrofit |

| New-Build Integrated |

By Country

| Indonesia |

| Thailand |

| Malaysia |

| Vietnam |

| Singapore |

| Philippines |

| Others |

| By Product Type | Smart Lighting |

| HVAC and Energy-Management Devices | |

| Safety, Security and Access Control | |

| Smart Appliances | |

| Entertainment and Connectivity Hubs | |

| Water and Utility-Management Devices | |

| By Communication Protocol | Wi-Fi |

| Zigbee | |

| Bluetooth/BLE | |

| Z-Wave | |

| Thread and Matter | |

| Proprietary/Others | |

| By Sales Channel | Online Retail and Marketplaces |

| Telco/ISP Bundles | |

| Home-Improvement and Electronics Stores | |

| Value-added Service Integrators | |

| By Installation Type | Retrofit |

| New-Build Integrated | |

| By Country | Indonesia |

| Thailand | |

| Malaysia | |

| Vietnam | |

| Singapore | |

| Philippines | |

| Others |

Key Questions Answered in the Report

What is the current value of the ASEAN smart homes market?

The ASEAN smart homes market stands at USD 6.11 billion in 2026 and is projected to reach USD 12.56 billion by 2031.

Which product category leads the market today?

Safety, security and access control devices dominate with 31.45% revenue share, driven by urban safety concerns.

Why are telco bundles gaining traction?

Telco/ISP bundles spread hardware costs over monthly bills and leverage existing customer relationships, resulting in a 16.90% CAGR through 2031.

How significant is Thread and Matter adoption in ASEAN?

Thread- and Matter-enabled devices are growing at 16.55% CAGR as chipset vendors such as MediaTek embed native support, easing interoperability barriers.

Which country is growing fastest?

Vietnam is the fastest-rising market, expanding at 16.30% CAGR thanks to urbanization, rising incomes and local brand innovation.

What key barrier still limits adoption?

High upfront device and installation costs remain the largest obstacle, subtracting an estimated 2.8 percentage points from forecast CAGR until hardware prices fall further.

Page last updated on: