Smart Home Security Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

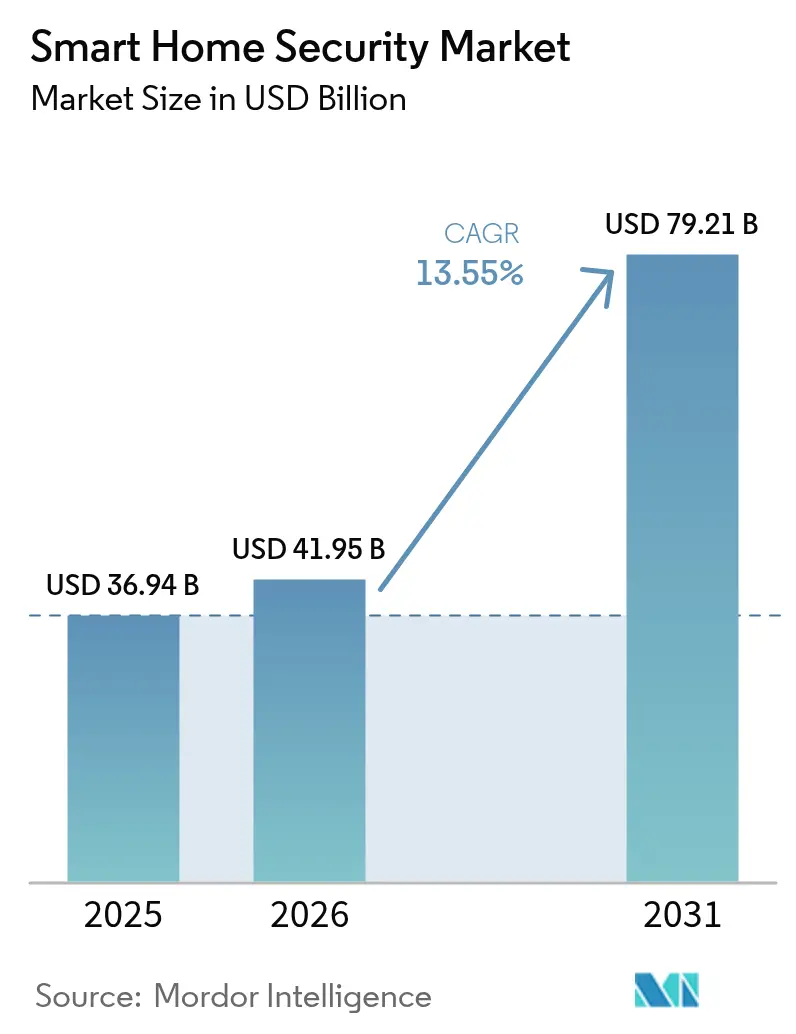

| Market Size (2026) | USD 41.95 Billion |

| Market Size (2031) | USD 79.21 Billion |

| Growth Rate (2026 - 2031) | 13.55% CAGR |

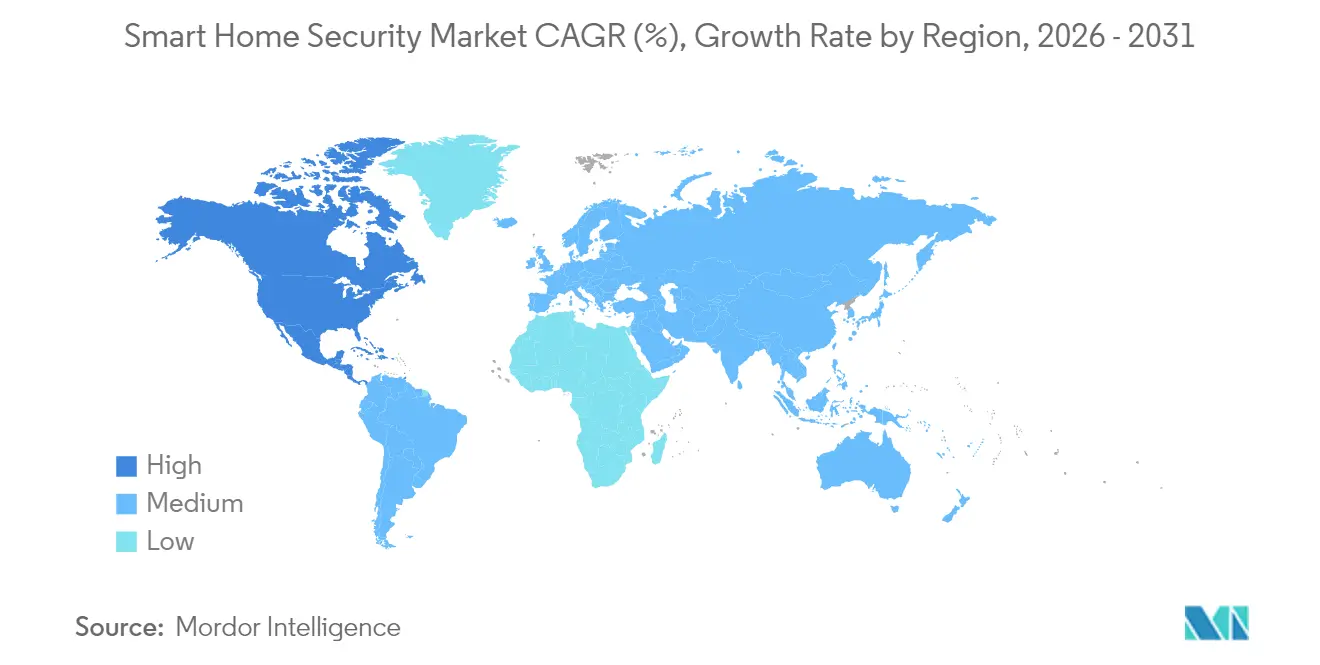

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Smart Home Security Market Analysis by Mordor Intelligence

The Smart Home Security market size was valued at USD 36.94 billion in 2025 and estimated to grow from USD 41.95 billion in 2026 to reach USD 79.21 billion by 2031, at a CAGR of 13.55% during the forecast period (2026-2031). Growth accelerates as edge-based artificial intelligence trims false alarms, insurance carriers embed premium discounts for connected devices, and Matter-enabled interoperability reshapes product ecosystems. Device makers now bundle computer-vision analytics that learn household routines, while carriers such as Nationwide reward policyholders who adopt professionally monitored packages. Government trade-in incentives in China and 5G fixed-wireless deployments in North America further widen the addressable base. Competitive intensity remains moderate because leading brands strike a balance between subscription innovation and privacy compliance, yet cost pressures from spikes in rare-earth input and cyber-insurance surcharges temper margins. Together, these forces underpin a demand cycle that places integrated doorbell and lock cameras, along with cloud analytics, at the center of residential protection strategies.

Key Report Takeaways

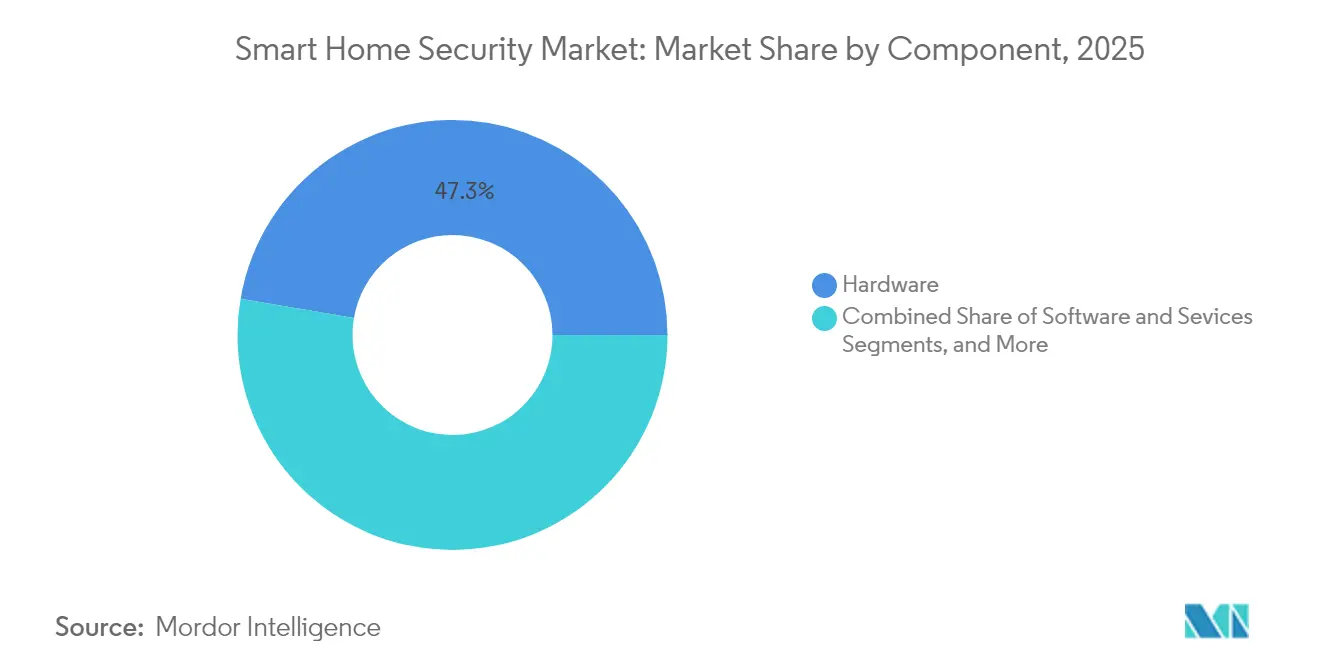

- By component, hardware led the Smart Home Security market with a 47.30% share in 2025, while services are projected to expand at a 13.66% CAGR through 2031.

- By device type, smart cameras accounted for 51.45% of the Smart Home Security market size in 2025; combined doorbell and lock cameras are forecasted to advance at a 13.59% CAGR through 2031.

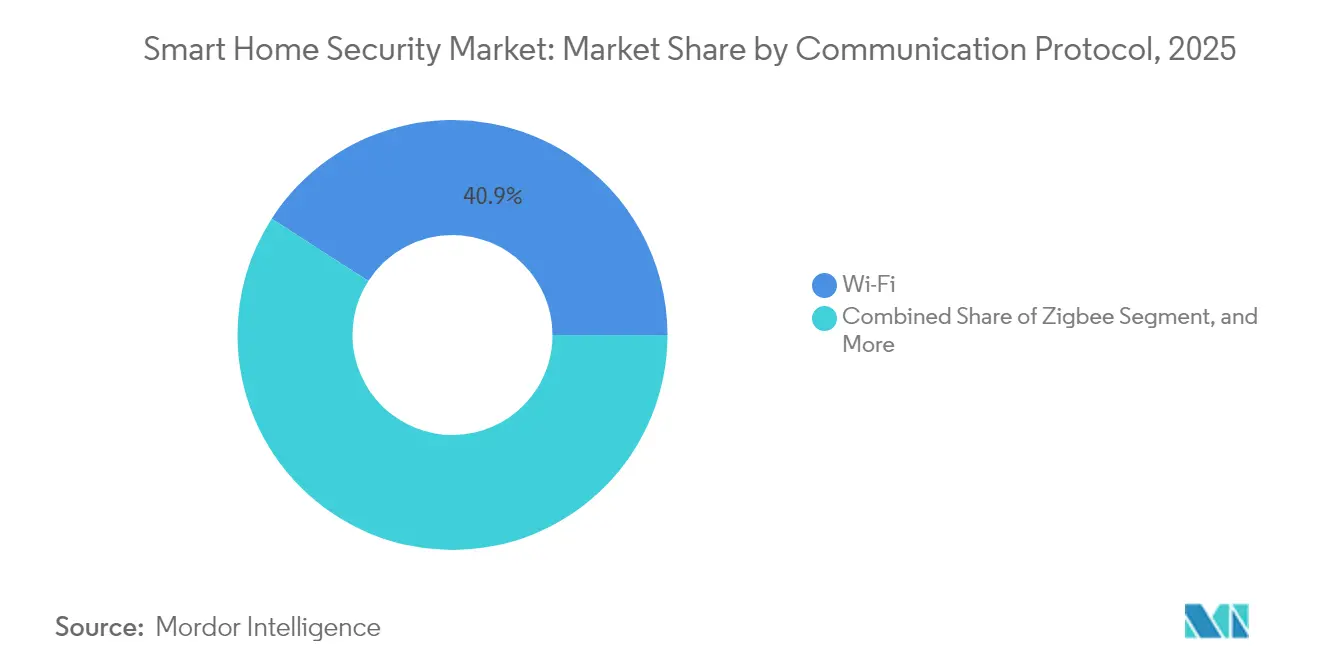

- By communication protocol, Wi-Fi protocols accounted for 40.90% of the revenue in 2025, whereas Thread-Matter devices are expected to grow at a 13.74% CAGR during the outlook period.

- By dwelling type, independent homes accounted for 45.55% of the revenue in 2025, but condominiums and MDUs are projected to log the fastest growth rate of 13.82% from 2025 to 2031.

- By geography, North America retained 61.40% of the revenue in 2025, while the Asia Pacific is on track for the strongest 14.05% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Smart Home Security Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| AI-enabled edge analytics cut false alarms | +2.1% | Global, with early adoption in North America and Europe | Medium term (2-4 years) |

| Insurance-linked device rebates spur installs | +1.8% | North America and Europe, expanding to Asia Pacific | Short term (≤ 2 years) |

| Matter/Thread interoperability lowers vendor lock-in | +1.5% | Global, led by North America and Europe | Medium term (2-4 years) |

| Crime-to-solution datasets accelerate predictive policing partnerships | +1.2% | North America and Europe, with selective Asia Pacific adoption | Long term (≥ 4 years) |

| Energy-aware security devices tap rising sustainability budgets | +0.9% | Europe and North America, emerging in Asia Pacific | Medium term (2-4 years) |

| 5G FWA roll-outs boost bandwidth for cloud-video plans | +1.4% | Global, with faster deployment in Asia Pacific and North America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

AI-Enabled Edge Analytics Cut False Alarms

Smart cameras equipped with on-device neural processors now recognize pets, vehicles, and familiar faces, slashing nuisance alerts that once eroded user trust. Synaptics’ 2025 SoCs demonstrate how edge inference trims latency and curbs cloud egress, improving response times while lowering bandwidth fees.[1]Synaptics, “Smart Security,” synaptics.comArlo layers this capability with custom detection modes that adapt to household routines, encouraging longer subscription tenure. Insurers observe fewer false dispatches and approve deeper discounts, reinforcing a virtuous cycle of adoption. The shift also raises barriers to entry because rivals must integrate sophisticated models and maintain frequent firmware updates, thereby escalating R&D outlays while producing sticky, recurring revenue once deployed.

Insurance-Linked Device Rebates Spur Installs

Homeowners can secure up to 10% premium reductions when they install qualified smart sensors, leak detectors, or monitored alarm packs under programs offered by carriers such as Nationwide and Amica. Similar incentives are also evident in Canada through Sonnet-TELUS tie-ups, signaling a North American blueprint for rapid scale. For insurers, connected hardware mitigates loss frequency by detecting perils at inception, improving loss-ratio economics. Vendors, in turn, leverage underwriting data to segment prospects and upsell service tiers. Regulatory clarity from the National Association of Insurance Commissioners on bundling removes compliance doubts, unlocking multiyear affinity deals that seed device shipments at scale

Matter-Thread Interoperability Lowers Vendor Lock-in

Matter 2.3.0 unifies device onboarding, encryption, and multi-radio routing, allowing mixed-brand security kits to operate across Thread, Wi-Fi, and Ethernet backbones. Consumers sidestep proprietary hubs, while integrators enjoy simplified commissioning. Although IPv6 multicast quirks occasionally hinder discovery in complex networks, firmware updates and border router best practices are reducing field failures. Platform neutrality pressures incumbents to compete on service quality rather than ecosystem captivity, accelerating device refresh cycles as households freely blend doorbell cams, smart locks, and flood sensors.

Crime-to-Solution Datasets Accelerate Predictive Policing Partnerships

Municipalities increasingly tap anonymized alert feeds from residential devices to refine patrol scheduling and incident triage. Early pilots in U.S. suburbs indicate double-digit declines in break-ins where analytics overlay historical precinct data with live sensor pings. Providers monetize these feeds through data licensing or co-branded community safety dashboards, positioning themselves as civic tech partners. Privacy advocates remain vigilant; however, encryption and opt-in consent frameworks have tempered legislative pushback, enabling vendors to expand predictive modules that could be applied in international markets with high urban density.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging cyber-breach insurance premiums on insecure devices | -1.9% | Global, with highest impact in North America and Europe | Short term (≤ 2 years) |

| IPv6 multicast instability in Thread Matter 1.4 networks | -1.3% | Global, affecting early Matter/Thread adopters | Medium term (2-4 years) |

| Rare-earth and Li-Ion price spikes hit battery-camera BOM costs | -1.1% | Global, with supply chain concentration in Asia Pacific | Short term (≤ 2 years) |

| AI-bias litigation limits facial-recognition deployments | -0.8% | North America and Europe, with regulatory spillover effects | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging Cyber-Breach Insurance Premiums on Insecure Devices

Underwriters have tightened their scoring models following high-profile IoT botnet events, requiring vendors to provide detailed penetration test results and SOC 2 attestations. The 2024 Betterley report notes double-digit rate hikes for manufacturers with porous firmware update pipelines, which elevates total product cost and elongates the time to profitability. Brands that embed secure boot, hardware root of trust, and coordinated vulnerability disclosure earn favorable terms and market their coverage status as a differentiator. Conversely, startups lacking mature security programs face capital constraints and retail pushback as distributors weigh liability exposure.

IPv6 Multicast Instability in Thread-Matter 1.4 Networks

Border routers often stumble when consumer gateways mishandle multicast forwarding, causing orphaned sensors that appear offline without warning to the user.[2]ndom91, “Getting Started with Matter + Thread,” ndo.dev Installers report an increase in truck rolls, which can inflate lifetime service costs and lead to negative reviews. Firmware tuning and router certification programs are mitigating incidents, yet the learning curve curtails near-term velocity for standard-only deployments. To hedge, many brands still ship dual-stack Wi-Fi options, diluting the simplicity ethos that Matter champions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Monetization Accelerates

Hardware retained 47.30% of the revenue in 2025, anchored by demand for cameras and sensors, but the Smart Home Security market anticipates a pronounced shift to cloud subscriptions as users adopt value-added AI alerts. Services are on track for a 13.66% CAGR, with platforms such as Arlo Secure 6 bundling forensic video search, object classification, and emergency response escalation into tiered plans. This trajectory boosts average revenue per user and mitigates seasonality, as recurring fees decouple cash flow from holiday device cycles. Software occupies a bridging layer, linking firmware, APIs, and mobile dashboards that orchestrate multisensor ecosystems. Vendors that master cross-sell journeys—device sale, trial, paid tier—optimize lifetime value while cultivating data moats that fortify churn barriers.

The growth of services also seeds channel diversification. Telecom operators bundle monitoring into broadband bills, whereas insurers co-sponsor installation vouchers. For hardware-centric incumbents, the task becomes embedding over-the-air upgradability, robust cloud pipelines, and multilingual AI models to sustain competitive positioning. Consequently, roadmap planning now intertwines silicon design with feature-as-a-service milestones, blurring the traditional delineations between product and service within the Smart Home Security market.

By Device Type: Cameras Lead While Integration Drives Growth

Smart cameras and monitoring units delivered 51.45% of 2025 revenue, underscoring consumer familiarity with visual deterrents and event verification. Growth, however, gravitates toward converged doorbell-lock cameras that deliver a 13.59% CAGR by collapsing entry control and surveillance into a single installation point. The Lockly Guard Vision exemplifies this shift, layering HD optics, fingerprint access, and RFID fallback in a form factor that streamlines both contractor labor and mobile app clutter. Standalone locks remain relevant for retrofit scenarios, while alarms gain new life when paired with multi-sensor rules that activate sirens, strobe lights, and automated door locks on authenticated threats.

Feature density brings thermal management, power efficiency, and antenna design challenges that reward vertically integrated players with in-house RF and ASIC teams. Furthermore, insurers are increasingly treating water-leak detectors and smoke sensors as loss-prevention extensions of security bundles, nudging camera-first brands to diversify. In the Smart Home Security market, the path to differentiation thus hinges on unified UX, battery endurance, and AI inference accuracy rather than isolated hardware specs.

By Communication Protocol: Wi-Fi Dominance Faces Standards Challenge

Wi-Fi’s 40.90% share reflects its ubiquity and bandwidth, ideal for 4K cloud video. Yet Matter-Thread nodes, projected at a 13.74% CAGR, promise self-healing mesh coverage and sub-milliwatt idle draw, meeting insurance and sustainability criteria for always-on perimeter sensors. The Connectivity Standards Alliance underpins this momentum with cryptographic attestation and multi-admin control policies, easing integrator concerns over mixed-vendor deployments. Zigbee and Z-Wave persist in battery-sipping use cases, and Bluetooth Mesh remains favored for low-latency door access and provisioning tasks.

Ecosystem fluidity forces vendors to dual-source radio modules and abstract network stacks through OTA-updatable SDKs, raising engineering complexity but future-proofing portfolios. Retailers respond with compatibility labeling that simplifies shelf navigation, while professional installers develop protocol-agnostic dashboards. In aggregate, the Smart Home Security market tilts toward hybrid radios that shield consumers from protocol obsolescence.

By End-User Dwelling Type: MDUs Drive Adoption

Independent homes contributed 45.55% revenue in 2025, yet the 13.82% CAGR in MDUs highlights property managers’ appetite for amenity-driven differentiation. Bulk procurement lowers unit economics, allowing centralized command centers to monitor lobbies, garages, and individual units within one pane. Subscription consolidation further reduces churn because tenants inherit pre-configured services upon lease turnover. Vendors tune offerings with privacy partitions that provision unit-level control while granting managers situational awareness over common areas.

Apartments, especially in renter-dense urban cores, are edging upward as telecom-security bundles widen their reach. Landlords negotiate volume pricing and integrate keyless entry with existing proptech stacks for maintenance ticketing and parcel delivery. The Smart Home Security market rewards players capable of delivering scalable APIs, remote diagnostics, and firmware fleet management that suit enterprise-grade residential operations without overextending unit economics.

Geography Analysis

North America generated 61.40% revenue in 2025 by leveraging a mature insurance ecosystem, robust broadband penetration, and a culture of professional monitoring. Carriers such as American Family incentivize installations through premium discounts, while 5G fixed-wireless access ensures uplink headroom for multi-camera households. Strategic M&A, typified by Resideo’s USD 1.4 billion acquisition of Snap One, signals a trend toward vertically integrated models that stitch distribution, hardware, and recurring services into a single stack.Tariff volatility and evolving state privacy statutes create cost and compliance uncertainties; however, high disposable income helps preserve baseline demand as the Smart Home Security market broadens beyond early adopters.

The Asia Pacific outpaces all regions at a 14.05% CAGR through 2031, driven by China’s Ministry of Commerce trade-in vouchers, MIIT 5G initiatives, and Japan’s leadership in IEC standardization, which shapes safety benchmarks. Rising middle-class awareness around burglary and elder care, alongside urban densification, pushes device penetration into condominiums. Partnerships like Zigbang and SK Shieldus demonstrate localized service models that integrate proptech platforms with AI-powered CCTV and emergency dispatch, unlocking scalability in high-rise complexes. Foreign entrants must tailor their firmware to regional languages, cloud sovereignty, and e-commerce logistics to capture a share.

Europe maintains steady expansion, underpinned by GDPR-driven trust in data stewardship and a regulatory push toward energy-aware electronics. Sustainability budgets support multifunction sensors that integrate security with HVAC optimization. Vendors differentiate through privacy-by-design engineering, earning certification badges that resonate with consumers wary of facial-recognition litigation. Latin America and the Middle East, and Africa remain nascent yet promising, provided improvements in broadband affordability and payment infrastructure keep pace with falling device ASPs.

Regulatory Landscape

Cybersecurity and data-governance requirements are tightening for connected home devices, directly shaping smart cameras, locks, sensors, and their companion apps and cloud services. In the United States, the FCC IoT Labeling Program (U.S. Cyber Trust Mark) formalizes a voluntary security label using a QR code linked to a public registry of product security information. It pushes vendors to document update policies and vulnerability handling to keep shelf and channel acceptance. NIST IoT cybersecurity guidance also acts as a common reference point for vendors, insurers, and enterprise residential buyers evaluating readiness for secure boot, patchability, and coordinated vulnerability disclosure.

In the European Union, the Cyber Resilience Act (CRA) introduces product security-by-design obligations for products with digital elements. Smart home security devices such as smart locks and security cameras are treated as higher-criticality categories (Important Class I), which can bring stricter conformity assessment requirements. A key operational anchor is the CRA reporting obligation effective September 11, 2026, requiring manufacturers to notify ENISA and relevant national CSIRTs of actively exploited vulnerabilities or severe incidents within 24 hours. Standards development also shapes compliance pathways, with ETSI advancing harmonized work (for example, EN 304 632) focused on smart home products with security functionalities.

Value Chain Analysis

The value chain begins with semiconductor and module suppliers (MCUs/SoCs, image sensors, radios for Wi-Fi, Zigbee, Z-Wave, and Thread, and secure elements). Hardware is increasingly built with hardware-rooted security to support device attestation and secure onboarding requirements. OEMs and ODMs then integrate optics, batteries, antennas, and enclosures with firmware stacks that must support over-the-air updates and identity lifecycle management. The Connectivity Standards Alliance (CSA) ecosystem influences upstream design choices through Matter security capabilities such as certificate management and revocation.

Certification and assurance steps, including Matter certification and security verification programs, add an additional gate between engineering and volume production. They can affect BOM structure and time-to-market when device attestation certificates and secure provisioning are required during manufacturing. On the downstream side, distribution runs through retail and e-commerce, professional installers, telecom operators bundling security into broadband bills, and insurers that sponsor qualified device installs. Cloud infrastructure providers and analytics platforms enable subscription services that increasingly define vendor economics. The EU Data Act becoming applicable on September 12, 2025 adds a data-access and sharing layer that influences how device telemetry, event video, and account data are exposed to users and authorized third parties. As interoperability expands, value shifts toward software and service layers, including mobile apps, cloud video storage, AI detection models, professional monitoring, and integration middleware used for mixed-brand households and multi-dwelling unit deployments.

Competitive Landscape

Market concentration is moderate as legacy alarm companies, pure-play camera brands, and telecom aggregators jostle for household mindshare. Arlo reinforces its analytics edge through an exclusive Origin AI agreement that brings Wi-Fi RF sensing for verified human presence, thereby widening differentiation without the need for additional cameras. Ring leverages Amazon’s ecosystem to bundle camera and smart speaker leverage points, while Resideo’s Snap One integration merges installer networks with hardware IP, positioning the group for distribution-led growth. Boutique integrators respond by white-labeling Matter-certified hubs, coupled with concierge monitoring, to retain their margin against retail giants.

Subscription innovation is the competitive fulcrum. Arlo Secure 6 debuts AI captions and multimodal detection, creating service stickiness that rivals must match. Privacy litigation risk prompts companies to strengthen consent flows; Arlo’s BIPA class action highlights brand exposure when biometrics rules shift. On the hardware front, innovations in battery technology, advanced edge AI silicon, and sustainable materials sourcing differentiate premium tiers from value devices. Strategic deals for chipset supply and cloud credits influence cost curves, highlighting supply-chain resilience as a latent competitive weapon in the Smart Home Security market.

Channel orchestration increasingly determines share capture. Telecom operators bundle security to curb churn, insurers co-market devices to trim claims, and retailers curate interoperable product aisles under Matter trust marks. Vendors that master multi-channel alignment acquire distribution breadth without undercutting partner economics, sustaining a balanced competitive landscape that rewards ecosystem savvy over brute hardware specs.

Smart Home Security Industry Leaders

ADT Inc.

Arlo Technologies Inc.

Blink Home Inc.

Dahua Technology Co., Ltd.

Canary Connect Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Interoperability and platform-level AI are creating whitespace for cross-brand security experiences that are easier to install and operate in mixed ecosystems, particularly in multi-device homes and MDUs. Matter 1.6 (June 2026) introduces Joint Fabric for multi-ecosystem device management and expands standardized capability communication. This reduces friction for service providers and installers supporting heterogeneous security stacks. CSA Product Security 1.1 (June 2026) also extends certification coverage beyond the device to include apps, remote processes, and gateways, giving vendors room to differentiate with system-level assurance packages that align to evolving compliance expectations and buyer due diligence.

Service-led expansion is further reinforced by major ecosystem players enabling AI-enabled camera workflows at the platform layer. Google announced Gemini for Home (May 2026) alongside camera-driven automations through Google Home, while Apple highlighted Apple Intelligence-driven video search and event summaries for Apple Home at WWDC 2026. These efforts strengthen opportunities for vendors and monitoring providers to bundle premium tiers around verified alerts, notification management, and multi-service packages that combine security with adjacent needs such as wellness and aging-in-place, with privacy-by-design controls intended to stay aligned with tighter security labeling and EU reporting obligations.

Recent Industry Developments

- June 2026: Blink introduced Single Event Alert for subscribers, grouping multiple motion alerts into a single notification to reduce notification fatigue. The feature targets a common churn driver in camera-heavy homes where frequent motion events overwhelm users. It also reinforces subscription value beyond basic video capture by adding AI-assisted event management.

- May 2026: ADT launched ADT Blu, a self-installed security system managed via the ADT+ app and sold through Amazon and ADT.com. The move expands ADT deeper into DIY channels while keeping a pathway to professional monitoring and recurring services. Wider e-commerce availability strengthens reach into price-sensitive segments that avoid installer-led deployments.

- April 2026: Arlo completed the acquisition of Aloe Care Health, adding AI-powered medical alert and fall-prevention capabilities to Arlo's platform. The transaction broadens Arlo beyond traditional security into aging-in-place and wellness use cases that can be delivered via subscription services. It also creates cross-sell routes for camera and sensor bundles into home-care provider networks.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the smart home security market covers revenue earned from connected residential security devices, the related software that enables control and alerts, and paid services such as monitoring and installation.

Scope exclusions: We exclude non-connected, purely mechanical security products, and broader smart home systems that do not have a security purpose as the primary function.

Segmentation Overview

- By Component

- Hardware

- Software

- Services

- By Device Type

- Smart Cameras and Monitoring Systems

- Smart Locks

- Smart Alarms

- Smart Sensors and Detectors

- Combined Doorbell-Lock Cameras

- Other Device Types

- By Communication Protocol

- Wi-Fi

- Zigbee

- Z-Wave / Z-Wave LR

- Thread / Matter

- Bluetooth LE / Mesh

- By End-User Dwelling Type

- Independent Homes

- Apartments

- Condominiums / MDUs

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Singapore

- South korea

- Australia

- Rest of Asia Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set market boundaries, build initial assumptions, and collect reference indicators that can be checked year after year. We relied on public and official sources such as U.S. Census Bureau housing data, Eurostat housing statistics, and UN Comtrade trade flows for relevant device categories. For connectivity adoption signals, we referenced IEEE and other standards bodies, and we also reviewed peer reviewed papers on smart camera and sensor performance trends.

We then reviewed company annual reports, earnings call transcripts, investor presentations, reputable news coverage, and product certification or standards documentation that explains what functions are enabled by Wi-Fi, Zigbee, Z-Wave, Thread, and Matter. When useful, paid subscriptions were used for company financials and intelligence, import-export shipment level context, and patent databases to understand where new features are being commercialized. The sources listed above are illustrative rather than exhaustive, and other public documents were also used to validate and clarify assumptions across the coverage scope.

Primary Interviews and Surveys

Primary interviews and surveys focused on validating what households actually buy, and how revenue is recognized across devices, software, and services. Since bundles and subscriptions can move value across product lines, respondent input helped stress test attach rates, replacement cycles, and average selling price assumptions. We spoke with a mix of device suppliers, monitoring and installation partners, channel participants, and informed buyers across major regions so the model inputs could be adjusted where real buying patterns differed from initial desk assumptions.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 35% | CXOs: 16% | APAC: 37% |

| Mid tier: 49% | Functional/Unit leaders: 29% | EMEA: 36% |

| Smaller Players: 16% | Managers: 55% | Americas: 27% |

Market-Sizing & Forecasting

The core model uses a top-down demand pool build that starts from occupied housing stock and connected home penetration trends, then translates those totals into security system adoption and the resulting device mix by region. To keep the totals realistic, we corroborated the results with selective bottom-up checks, such as sampled pricing by device type, channel checks on bundle pricing, and a light roll-up of service revenue where monitoring subscriptions are common.

Key inputs include smart home penetration by geography, the split between professionally monitored and self-monitored setups, average devices per installed home (cameras, sensors, locks, alarms), replacement and upgrade cycles, and average selling price movement as AI features and interoperability standards become more widely adopted. Forecasts were built using scenario analysis, with the base case guided by expected housing completions, connectivity module trends, and expert views on subscription attach rates. We then ran sensitivity checks on ASPs and adoption pacing. Where coverage was thin for smaller countries or niche dwelling types, we applied proxy ratios from comparable markets and corrected them using primary feedback so the final series remained consistent with observed demand signals.

Data Validation & Update Cycle

Outputs are triangulated across independent checks, including housing and household counts, connectivity adoption signals, and the implied spend per installed home. This last check helps flag values that do not make practical sense given regional device intensity and monitoring participation. Outliers are reviewed in steps, first at the regional level, then at the device and service level, before final analyst sign-off.

Reports are refreshed annually, and interim updates are triggered when material events occur, such as major standards shifts, pricing shocks, or notable regulatory changes that affect monitoring or data privacy. Before delivery, a fresh validation pass is performed using the latest available indicators, so the published numbers reflect updated market context and clarified assumptions.

Mordor Intelligence's Smart Home Security Market Size Compared With Other Published Estimates

Published estimates for smart home security often do not align because each publisher draws the line differently on what counts as security revenue. They also vary in how they treat subscriptions versus one-time device sales. Differences can appear when one study uses a shorter forecast window or applies a different currency conversion timing for multi-region totals.

The table shows a spread, and in Mordor Intelligence's model the value includes residential security hardware, software, and services together. Monitoring is split by professionally monitored versus self-monitored, rather than being treated as a separate services-only market. Other figures sometimes narrow scope to selected device categories, or they lean more heavily on shipment-style indicators without fully adjusting for bundle pricing, subscription attach rates, and replacement cycles.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 41.95 B (2026) | |

| Global Consultancy A | USD 62.40 B (2025) | Often uses a broader smart home safety framing that can fold in adjacent categories and faster ASP uplift assumptions, which can raise the starting value versus a security-only scope. |

| Trade Journal B | USD 0.92 B (2024) | Commonly reflects a narrow definition that resembles selected smart security system devices, and it may undercount services and software revenue from monitoring, installation, and ongoing subscriptions. |

Taken together, the gap is largely explained by scope breadth and how recurring service revenue is counted over time. By tying the build to household adoption, device mix, and monitoring participation, the final market size stays traceable to clear inputs that can be rechecked when conditions change.

Key Questions Answered in the Report

What is the projected value of the Smart Home Security market in 2031?

The Smart Home Security market is forecast to reach USD 79.21 billion by 2031.

Which component category is growing the fastest?

Services are expanding at a 13.66% CAGR through 2031 as consumers adopt subscription monitoring and AI analytics.

Why is Matter important for smart home security devices?

Matter unifies onboarding and encryption across brands, lowering vendor lock-in and simplifying installation.

Which region will experience the highest growth rate?

Asia Pacific leads with a 14.05% CAGR thanks to government incentives and rising middle-class demand for home protection.

How are insurers influencing device adoption?

Carriers offer premium rebates of up to 10% for qualified monitored systems, reducing payback periods for homeowners.

What technology reduces false alarms in smart cameras?

On-device edge AI distinguishes pets, vehicles, and known faces, improving alert accuracy and user satisfaction.

Page last updated on: