United States Smart Homes Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

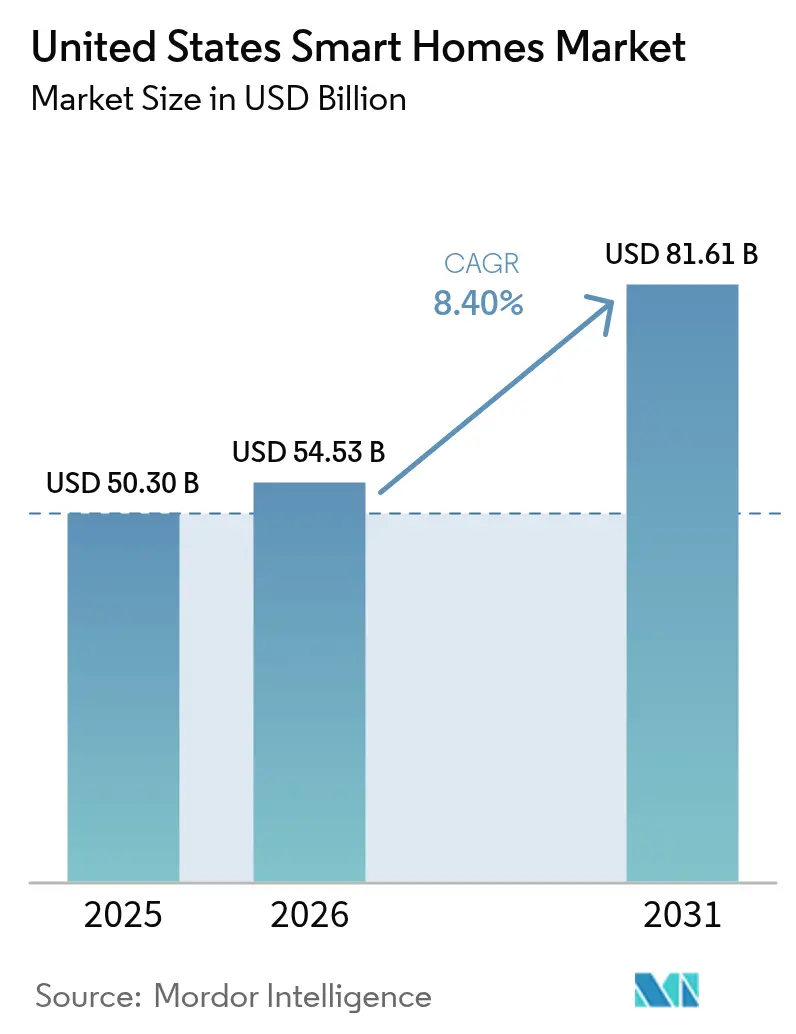

| Base Year Market Size (2025) | USD 50.30 Billion |

| Market Size (2026) | USD 54.53 Billion |

| Market Size (2031) | USD 81.61 Billion |

| Growth Rate (2026 - 2031) | 8.40% CAGR |

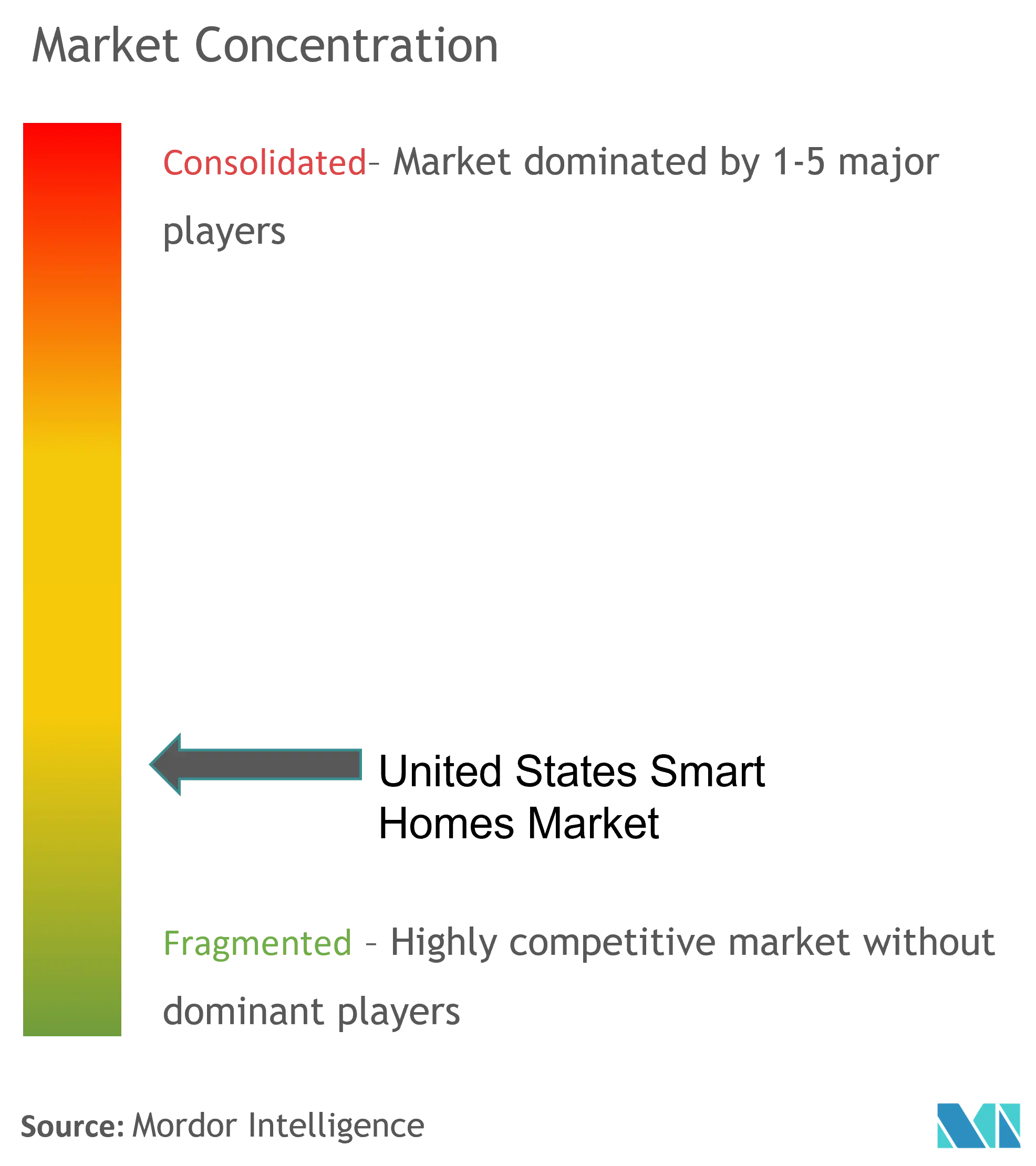

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Smart Homes Market Analysis by Mordor Intelligence

The United States Smart Homes Market size in 2026 is estimated at USD 54.53 billion, growing from 2025 value of USD 50.30 billion with 2031 projections showing USD 81.61 billion, growing at 8.4% CAGR over 2026-2031.

Growth is fueled by a confluence of federally funded energy-efficiency rebates, the rapid institutionalization of the Matter interoperability protocol, and demographic momentum toward aging-in-place solutions. Federal support—most visibly the FCC’s new Cyber Trust Mark and the Department of Energy’s Home Energy Rebates—has elevated consumer confidence in device security while directly lowering acquisition costs. Connectivity breakthroughs, such as Thread 1.4’s unified mesh networking, are dissolving long-standing adoption barriers by allowing border routers from multiple brands to join existing networks seamlessly. At the same time, insurance carriers are pairing premium reductions with verified security installations, creating a clear economic incentive for first-time adopters. Platform vendors are responding with aggressive portfolio realignments; Amazon’s subscription-based Alexa+ model and Apple’s delayed but expanded HomeOS roadmap show that ecosystem control now matters more than single-device margins.

Key Report Takeaways

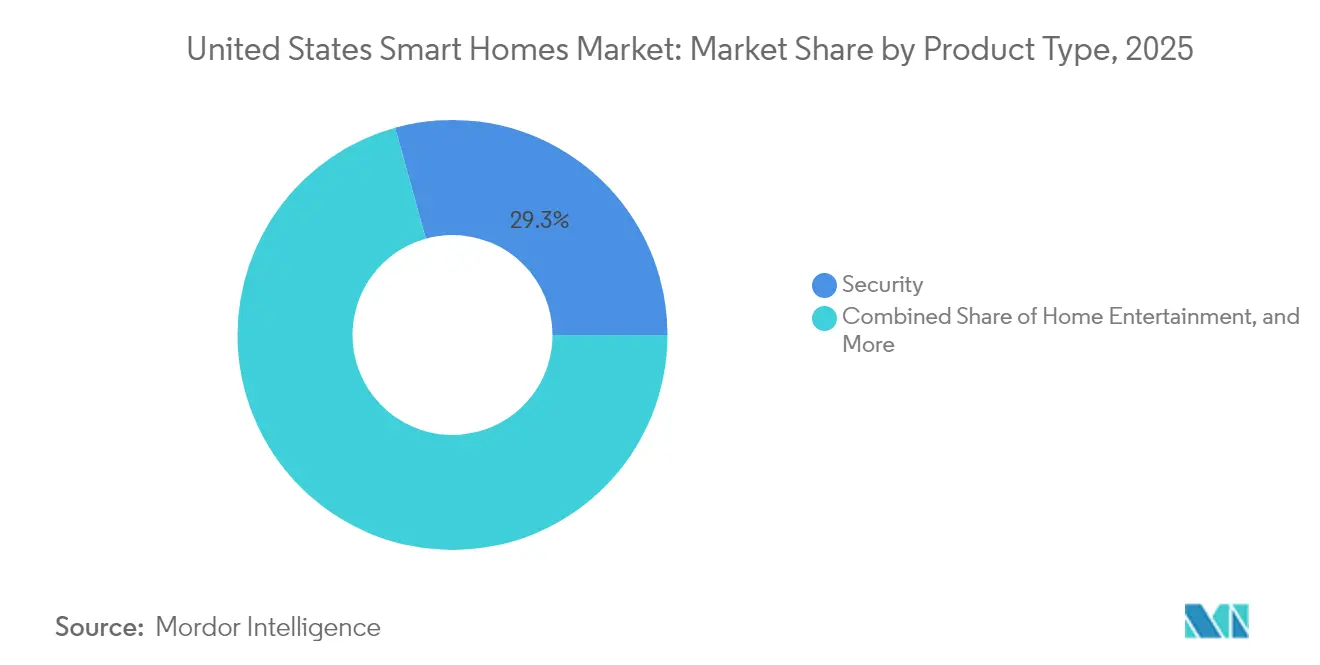

- By product type, security captured 29.30% of the United States smart homes market share in 2025; smart appliances are projected to grow at a 14.25% CAGR through 2031.

- By connectivity, Wi-Fi devices held 60.35% share of the United States smart homes market size in 2025, while Thread-enabled products are set to expand at an 18.1% CAGR to 2031.

- By installation, DIY deployments controlled 67.35% of the United States smart homes market in 2025, but professionally installed systems are advancing at a 10.05% CAGR to 2031.

- By sales channel, online retail accounted for 52.60% of revenue in 2025; telecom-utility bundles are forecast to post a 12.8% CAGR through 2031.

- By component, hardware represented 76.30% of 2025 revenue, whereas subscription and monitoring services will climb at an 10.95% CAGR over the forecast.

- Amazon, Google, Apple, Honeywell, and Schneider Electric collectively commanded roughly 45% of 2024 revenue.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United States Smart Homes Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Utility-backed energy-efficiency incentives | +2.1% | Nationwide; strongest in CA, NY, HI, NM | Medium term (2-4 years) |

| Rapid Matter-based multi-brand bundles | +1.8% | Global; peak effect in North America | Short term (≤ 2 years) |

| Aging-in-place retrofit demand | +1.4% | Nationwide; suburban and rural concentrations | Long term (≥ 4 years) |

| Insurance discounts for smart security | +0.9% | Nationwide; pilots in six states | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Utility-backed Energy-Efficiency Rebates and Dynamic-Pricing Programs

The Department of Energy’s USD 8.8 billion Home Energy Rebates program—already live in California, Hawaii, New Mexico, and New York—has placed unprecedented purchasing power directly in homeowners’ hands.[1]U.S. Department of Energy, “Home Energy Rebate Programs,” energy.govNew York’s May 2024 roll-out set the tone for states eager to capture federal dollars for smart thermostats, heat pumps, and connected water heaters. Southern California Edison now offers USD 75 bill credits for enrolling certified thermostats in demand-response schemes, while PSEG Long Island earmarked USD 92.45 million for 2025 efficiency measures focused on connected devices. [2]New York State Public Service Commission, “PSEG Long Island 2025 Energy Efficiency Plan,” dps.ny.govWisconsin’s USD 149 million allocation under its Focus on Energy program shows that even colder climates are leaning heavily on connected equipment to curb peak loads. Utilities then recycle the savings they achieve on peak-generation costs into broader rebate pools, thereby creating a virtuous adoption cycle.

Rapid Adoption of Matter Protocol Driving Multi-brand Device Bundles

Matter’s 1.4 specification, published in November 2024, was the watershed moment when unified multi-admin control, expanded device classes, and native Thread mesh support converged. Over 670 Thread-based products had cleared certification by mid-2025, and major retailers pledged dedicated shelf space to Matter-ready gear. [3]CNBC, “Retailers double down on Matter smart home standard,” cnbc.com Apple reversed course, shifting from HomeKit exclusivity to full Matter compliance, a move that signaled ecosystem consensus. Self-healing Thread networks now allow devices from different brands to join without re-commissioning, erasing historical complexities that drove high return rates. Version 1.5, expected in late 2025, will embed grid-interactive energy APIs, positioning residences as dispatchable demand-response nodes rather than passive loads.

Aging-in-Place and “Age-Tech” Demand Accelerating Retrofit Spending

Four in five seniors possess at least one connected device to support independent living, according to AARP’s 2025 survey. California’s Lead Locally pilot demonstrated an 11% yearly drop in household energy use once heat pumps and smart water heaters were combined with automation suite. Medicare Advantage plans are progressively reimbursing remote-patient-monitoring sensors that integrate directly with mainstream smart-home hubs, shrinking out-of-pocket costs for seniors. Voice-first interfaces, buoyed by sharp advances in natural-language models, remove the intimidation factor for older adults who once shunned technology. The result is a sizable retrofit wave reaching well beyond emergency pendants into whole-home environmental controls and predictive safety analytics.

Insurance Premium Discounts for Smart Security Installations

Liberty Mutual’s Smart Home Verified Discount launched across six states in 2024, offering rate cuts when customers share Nest device health data. Early claims data suggest double-digit declines in fire- and break-in-related payouts, encouraging expansion into additional states. Insurers have progressed from static discounts to dynamic risk-mitigation services: water-leak detectors that auto-shut valves, AI-enabled cameras that trigger pre-emptive intervention, and device telematics that auto-populate claims. Professional monitoring firms leverage these partnerships to justify monthly fees, while carriers gain continuous actuarial visibility into risk conditions inside the home.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent data-privacy & surveillance fears | -1.3% | National; acute in CA and Northeastern US | Long term (≥ 4 years) |

| High pro-install cost for legacy housing | -0.8% | National; older metro areas | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Persistent Data-Privacy and Surveillance Concerns

Although the FCC unveiled the Cyber Trust Mark in 2025, labeling remains voluntary, leaving device makers free to adopt tiered approaches that consumers often find opaque. California’s Consumer Privacy Act requires explicit disclosure of data use, elevating public awareness about what smart cameras, speakers, and sensors collect. Voice-assistant defaults drew renewed scrutiny when Amazon introduced an opt-in voice data retention policy in March 2025, igniting social-media backlash. Professional-grade IP cameras remain outside the FCC label’s scope, perpetuating concerns among security-sensitive households. Family dynamics further complicate matters: younger residents may welcome automation, while older or privacy-conscious members view 24-hour monitoring as intrusive.

High Professional-Installation Cost for Legacy Housing Stock

Many pre-1990 homes feature outdated wiring, thick masonry walls, and HVAC systems incompatible with modern automation kits. Whole-home retrofits often exceed USD 10,000 once electrical upgrades, structural adjustments, and pro labor are included, deterring mass uptake in older metro regions. Contractor shortages add scheduling delays and premium labor costs, especially in cities where renovation backlogs already stretch months. Thread and Wi-Fi do mitigate wiring needs, yet plaster, reinforced concrete, and metal conduits can attenuate signals, forcing homeowners to choose between expanded repeater nodes or costly rewiring to achieve blanket coverage.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Security Dominance Meets Appliance Innovation

Security systems accounted for a 29.30% share of 2025 spending within the United States smart homes market, underlining consumers’ instinctive prioritization of personal safety and property protection. Early adoption often begins with cameras or video doorbells bundled into insurance discount programs, which then serve as launchpads for broader ecosystems. Smart appliances, however, are poised for the fastest lift, tracking a 14.25% CAGR on the strength of Matter-enabled cross-brand compatibility and escalating utility rebates on energy-star units. Energy-management packages—particularly smart thermostats linked to dynamic pricing schemes—continue benefiting from federal and state incentives. Home-entertainment devices, while maturing, still find incremental gains by acting as centralized automation dashboards on large-screen displays.

Consumer emphasis on unified control is closing the gap between historically siloed categories. Cameras now embed AI analytics that cooperate with lighting scenes, while refrigerators surface real-time dynamic-pricing prompts that mesh with energy-management routines. All told, hardware convergence reinforces the view that product labels will blur over the next five years as platform capabilities outpace single-function devices.

By Connectivity Technology: Thread Disrupts Wi-Fi Dominance

Wi-Fi controlled 60.35% of device shipments in 2025, buoyed by widespread router penetration and low incremental setup friction. Yet the Thread specification is on pace to carve out a substantial share, growing at an 18.1% CAGR to 2031. The latest 1.4 build delivers unified mesh capability, enabling multiple vendor border routers to form a single network without user intervention. Thread’s low-power, IPv6-based architecture allows sensors to sustain multi-year battery life even while participating in real-time communication loops essential for security and energy management.

The convergence between Thread and Wi-Fi is now complementary: high-bandwidth applications such as streaming cameras still rely on Wi-Fi, whereas low-bandwidth door sensors, leak detectors, and buttons migrate to Thread. Apple’s tvOS 26, Google’s Fuchsia-based Nest hubs, and Amazon’s Echo Hub firmware all ship with Thread border-router functionality, signaling mainstream endorsement. The Thread Group surpassed 670 certifications by June 2025, confirming that the ecosystem has passed a critical maturity threshold.

By Installation Type: DIY Preference Challenges Professional Integration

DIY kits captured 67.35% of 2025 revenue, as consumers gravitated toward plug-and-play devices requiring no drilling or code compliance. Retailers curate step-by-step app onboarding and bundle QR-coded quick-start cards to shorten install times. Nonetheless, the professionally installed segment is advancing at a 10.05% CAGR, largely in luxury builds, multifamily residences, and aging-in-place retrofits where code-driven electrical changes are unavoidable. Integrators differentiate by delivering whole-home scene programming, structured wiring, and warranty backing that outstrip the capacity of most end users.

The divide is not absolute. Amazon’s Echo Show 21 and forthcoming 15-inch variant illustrate a hybrid direction: an approachable touchscreen hub with optional pro commissioning for HVAC zoning, security panels, and unified voice control. The United States smart homes market is therefore likely to see sustained coexistence of DIY simplicity and pro-grade depth.

By Sales Channel: Online Retail Leads Telecom Bundle Growth

At 52.60% of 2025 turnover, online storefronts remain the buying venue of choice, primarily for self-install kits. Detailed listings, algorithmic recommendation engines, and extensive user reviews simplify compatibility checks. Telecom and utility bundles, growing at a 12.8% CAGR, are reshaping distribution economics. Verizon has extended 5G Home Internet coverage to 20 million households, coupling service contracts with starter kits that waive upfront hardware fees. AT&T’s 30 million-location fiber roadmap and T-Mobile’s fixed-wireless footprint likewise integrate smart-home hubs to anchor multi-service retention plays. Utilities add a further layer by embedding thermostat rebates directly into monthly billing cycles, shrinking payback periods for consumers.

By Component: Hardware Dominance Shifts Toward Services

Hardware still commands 76.30% of 2025 spending, reflecting the one-time capital nature of cameras, sensors, and hubs. Yet services—subscription monitoring, AI-driven automation tiers, and data analytics dashboards—are projected to rise 10.95% annually as vendors pivot from razor-thin device margins to recurring revenue. Amazon’s USD 19.99 Alexa+ plan provides predictive task automation, while Google’s forthcoming Home Assist will bundle generative AI scripts for cross-device orchestration. Apple’s HomeOS, delayed to spring 2026, prioritizes private-edge processing plus optional cloud upgrades. This monetization shift ensures that future platform viability rests less on unit sales and more on long-term engagement.

Geography Analysis

California continues to anchor the United States' smart homes market due to stringent energy-code mandates and instant rebates under the Golden State program, which offers USD 75 credits for demand-response thermostat enrollment. High electricity tariffs combined with progressive sustainability attitudes lead to above-average adoption of security, energy management, and appliance categories. New York, the first state approved for IRA-funded home energy rebates, has mobilized a dense network of local contractors to accelerate installations in aging housing stock. Retrofit complexity drives professional-install service growth in the Northeast, where brick and brownstone construction complicate wireless propagation and electrical upgrades.

Southern and Southwestern states, notably Texas, Florida, and Arizona, leverage high new-build rates to pre-wire dwellings, minimizing incremental smart-home costs. Heat-pump integration and solar PV coupling are especially popular where extreme temperatures or abundant sunlight raise the ROI on energy savings. The Mountain West—Colorado, Utah, and Idaho—combines technology-savvy demographics with utility incentive stacks targeting security and leak-detection devices that mitigate wildfire and freeze risks.

Rural America is entering a new adoption phase as 5G fixed-wireless access breaks broadband dead zones. The USD 42.5 billion BEAD fund earmarked for last-mile fiber augments this connectivity surge, making cloud-based smart-home platforms feasible in regions that historically lacked reliable backhaul. Utilities craft rural-specific programs, such as prepaid thermostats and remote water-shutoff incentives, acknowledging the longer service-truck rolls and limited contractor density typical of these communities.

Competitive Landscape

Competitive intensity in the United States smart homes market is medium-high, with five leading platform providers accounting for an estimated 45% share yet leaving ample room for specialized entrants. Amazon and Google dominate voice-assistant ecosystems; each sells multimodal smart displays that double as Thread border routers. Apple’s brand equity and privacy stance carve out a premium segment despite its slower release cadence. Honeywell, Schneider Electric, and Johnson Controls leverage decades of building-automation expertise to secure professional-install and light-commercial niches.

Strategic focus has shifted decisively toward ecosystem breadth. Amazon’s USD 25 billion Alexa investment, despite years of losses, underscores the bet that subscription revenue will cover past deficits and future R&D . Google’s acquisition of Wiz strengthens its lighting portfolio while unlocking user-behavior data for cross-device optimization. Apple’s HomeOS delay reflects its insistence on edge-processed intelligence to differentiate on privacy. Meanwhile, white-space innovators like OhmConnect (now merged with Google Nest Renew) and Athom (80% stake acquired by LG) are positioning energy services and cross-vendor dashboards as the next battlegrounds.

Patent filings highlight voice-command disambiguation, context-aware scene control, and low-power edge AI as priority themes, with Meta, Samsung, and Sony all vying for foundational IP. Utilities and insurers are quietly amassing proprietary datasets that could fuel new underwriting and demand-response products, signaling another competitive front beyond traditional device makers.

United States Smart Homes Industry Leaders

ABB Ltd.

Schneider Electric SE

Honeywell International Inc.

LG Electronics Inc.

Cisco Systems Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Apple delayed its HomeOS platform to spring 2026 to refine Siri’s contextual AI and bolster Thread mesh capabilities.

- April 2025: Honeywell posted USD 9.82 billion Q1 revenue and detailed a three-way split that will form Honeywell Automation for residential te

- March 2025: The FCC formally launched the Cyber Trust Mark labeling scheme for consumer IoT, with Amazon, Best Buy, and Google pledging preferential shelf placement for certified devices.

- February 2025: Amazon introduced Alexa+, a USD 19.99 monthly subscription featuring generative-AI routines and concierge-style task automation.

United States Smart Homes Market Report Scope

Smart home devices are suitable for a home setup where devices can be automatically controlled remotely from any internet-connected place, using a mobile or other networked device. A smart home has devices connected through the internet, and the customer can regulate functions, such as security access to the house, temperature, lighting, and home theater. The scope of the market includes various smart home segments as below: energy management, comfort and lighting, home entertainment, control and connectivity, security, and smart appliances.

The United States smart home market is segmented by product type (comfort and lighting, control and connectivity, energy management, home entertainment, security, and smart appliances).

The market sizes and forecasts are provided in terms of value (USD million) for all the above segments.

| Comfort and Lighting |

| Control and Connectivity |

| Energy Management |

| Home Entertainment |

| Security |

| Smart Appliances |

| Wi-Fi-enabled devices |

| Thread-enabled devices |

| DIY / Self-installed |

| Professionally installed integrated systems |

| Online retail (Amazon, direct-to-consumer) |

| Telecom / Utility bundles (5G-FWA, demand-response kits) |

| Hardware (devices and hubs) |

| Subscription and monitoring services |

| By Product Type | Comfort and Lighting |

| Control and Connectivity | |

| Energy Management | |

| Home Entertainment | |

| Security | |

| Smart Appliances | |

| By Connectivity Technology | Wi-Fi-enabled devices |

| Thread-enabled devices | |

| By Installation Type | DIY / Self-installed |

| Professionally installed integrated systems | |

| By Sales Channel | Online retail (Amazon, direct-to-consumer) |

| Telecom / Utility bundles (5G-FWA, demand-response kits) | |

| By Component | Hardware (devices and hubs) |

| Subscription and monitoring services |

Key Questions Answered in the Report

What is the current value of the United States smart homes market?

The market stands at USD 54.53 billion in 2026 and is projected to reach USD 81.61 billion by 2031

Which product category leads spending?

Security solutions dominate with a 29.30% revenue share, largely due to insurance-linked discounts and the perception of immediate safety benefits.

Why is Thread technology receiving so much attention?

Thread 1.4 enables low-power, self-healing mesh networks that allow devices from multiple brands to interoperate without user intervention, solving historic reliability gaps.

How do federal incentives influence smart home adoption?

Programs such as the USD 8.8 billion Home Energy Rebates lower upfront costs for thermostats, heat pumps, and connected appliances, directly accelerating purchase decisions.

Are privacy concerns still a major barrier?

Yes. Despite the FCC’s voluntary Cyber Trust Mark, data-sharing apprehension—especially surrounding voice assistants and cameras—continues to curb adoption rates, shaving an estimated 1.3% off long-term CAGR.

How are service revenues changing the competitive landscape?

Subscription offerings like Amazon’s Alexa+ illustrate an industry shift toward recurring revenue, with services forecast to grow at an 10.95% CAGR through 2031, outpacing hardware growth.

Page last updated on: