Home Automation Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

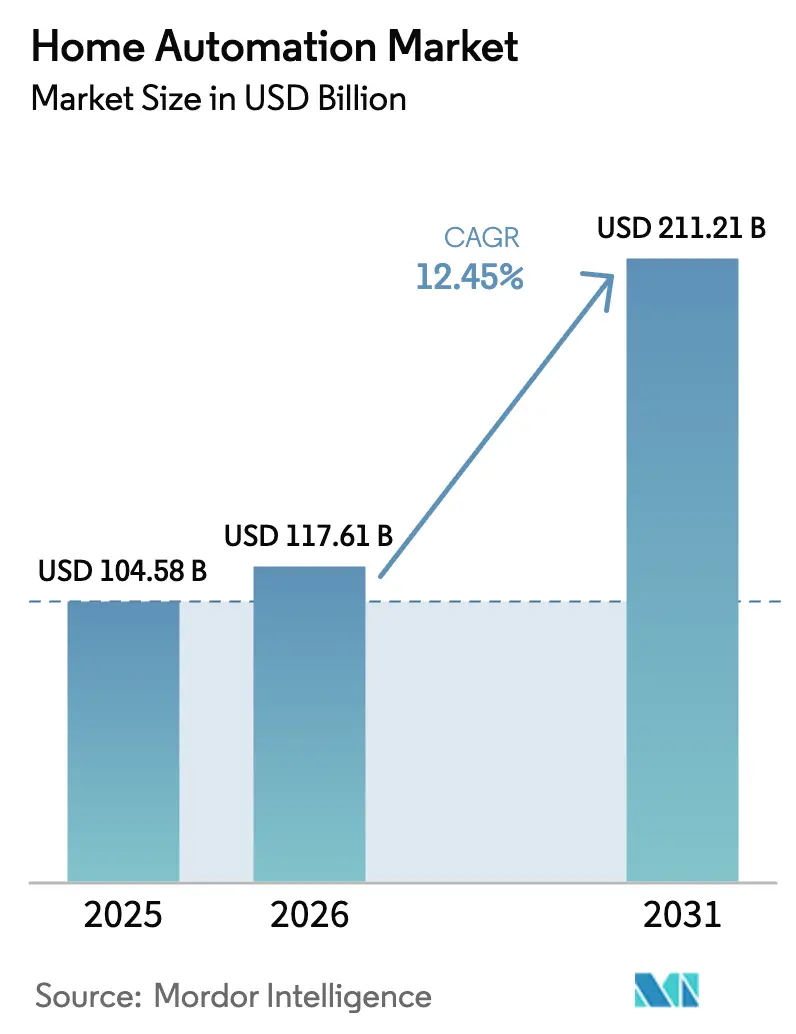

| Market Size (2026) | USD 117.61 Billion |

| Market Size (2031) | USD 211.21 Billion |

| Growth Rate (2026 - 2031) | 12.45% CAGR |

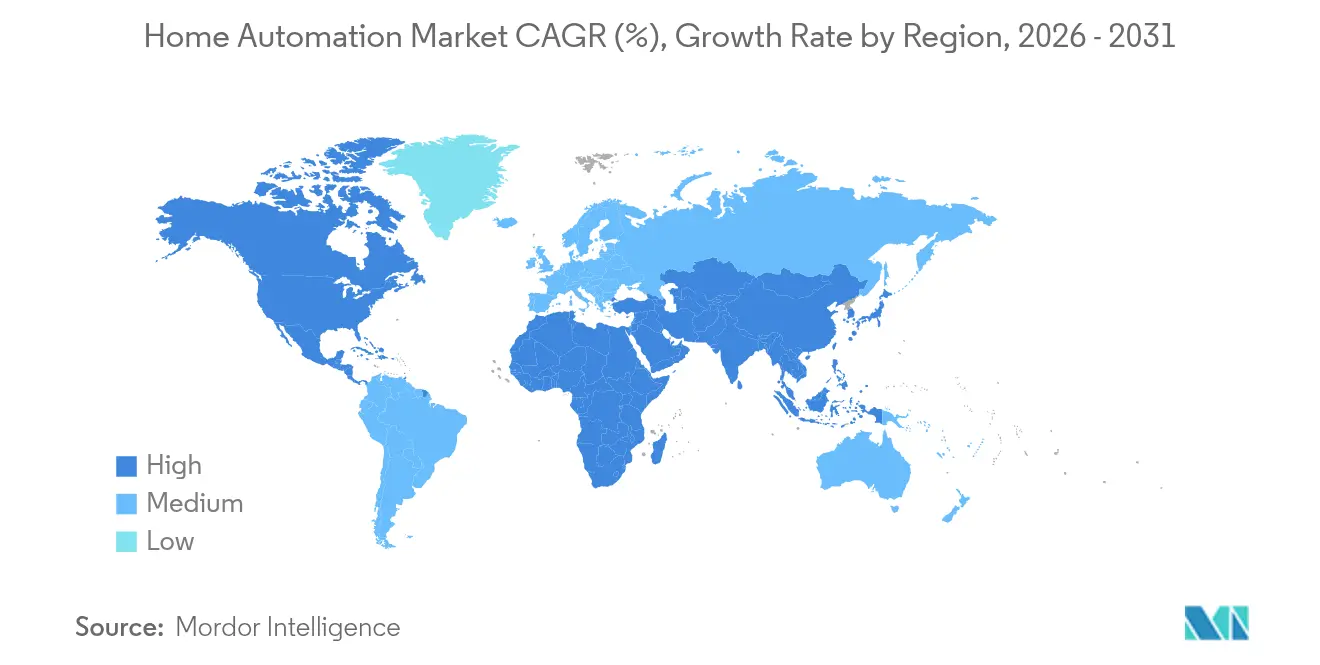

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Home Automation Market Analysis by Mordor Intelligence

The home automation market size was valued at USD 104.58 billion in 2025 and estimated to grow from USD 117.61 billion in 2026 to reach USD 211.21 billion by 2031, at a CAGR of 12.45% during the forecast period (2026-2031). Maturity is accelerating as infrastructure-level innovations—especially the Matter protocol and energy-autonomous sensors—replace flashy one-off device launches as the main growth engine. Government incentives for energy retrofits, aging-in-place healthcare needs, and interoperability breakthroughs combine to widen addressable demand and lower installation friction. North America still leads in revenue today, but Asia-Pacific’s manufacturing muscle and ecosystem depth make it the fastest grower, while Europe’s strict energy and cybersecurity rules steer product design globally. Competitive intensity remains high because incumbents and digital giants pursue divergent revenue models, yet no single firm controls more than a mid-single-digit share, keeping price and feature differentiation fluid.

Key Report Takeaways

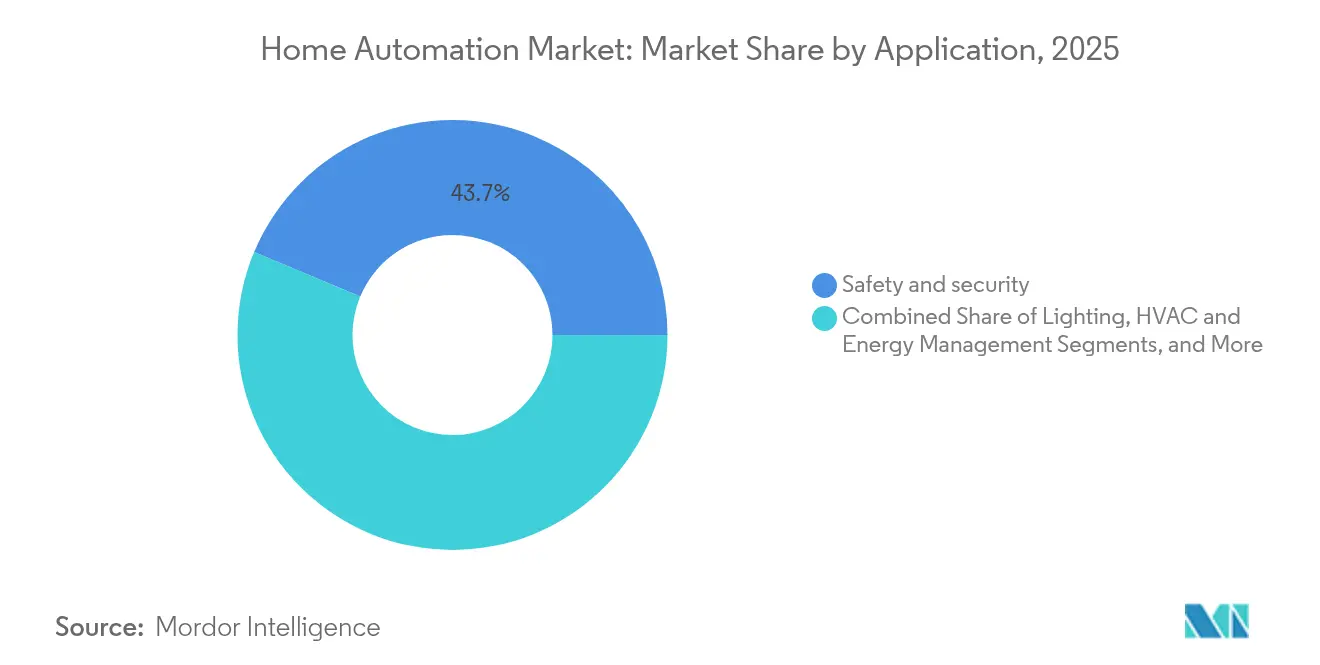

- By application, safety and security led with 43.70% revenue share in 2025; smart kitchen products are projected to expand at a 17.35% CAGR to 2031.

- By connectivity technology, wireless solutions held 61.80% of the home automation market share in 2025, while the same segment is advancing at a 20.85% CAGR through 2031.

- By component, hardware devices accounted for 51.10% of the home automation market size in 2025; software and platforms are expected to post the fastest 16.40% CAGR during 2026-2031.

- By type, mainstream installations captured 52.90% of 2025 revenue, whereas DIY solutions are projected to grow at an 17.90% CAGR to 2031.

- By geography, North America retained 36.05% of 2025 revenue; Asia-Pacific is forecast to lead growth at 14.25% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Home Automation Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for IoT device interoperability | +2.8% | Global, with early adoption in North America and EU | Medium term (2-4 years) |

| Integration of AI and ML in next-gen products | +3.2% | Global, led by North America and China | Short term (≤ 2 years) |

| Emergence of Matter standard for interoperability | +2.1% | Global, with strongest impact in developed markets | Medium term (2-4 years) |

| Energy-autonomous sensors cutting maintenance costs | +1.9% | Global, with highest impact in remote installations | Long term (≥ 4 years) |

| Aging-in-place healthcare automation demand | +1.7% | North America and EU, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Subsidy programs for energy-efficient retrofits | +2.4% | North America, EU, select Asia-Pacific markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising demand for IoT device interoperability

The Thread 1.4 specification published in 2024 removes the need for multiple hubs by enabling devices from different brands to join a single IPv6-based mesh network. Field trials show that Thread-enabled devices sustain connections among hundreds of nodes with lower power draw, thereby tackling both scalability and energy concerns. Manufacturers report 40% higher customer-satisfaction scores for Thread products, confirming user appetite for a seamless ecosystem. As more devices become protocol-agnostic, the home automation market gains momentum from mainstream buyers who previously resisted vendor lock-in.

Integration of AI and ML in next-gen products

Samsung’s Vision AI, unveiled at CES 2025, converts ordinary screens into ambient companions that learn routines and automate tasks without manual programming [1]Samsung Electronics, “Vision AI Unveiled at CES 2025,” news.samsung.com. Google’s Gemini intelligence inside Nest devices performs on-device processing to optimize energy use and security responses in real time. Local inference sidesteps privacy worries tied to constant cloud access and boosts latency-sensitive functions. Continuous learning makes smart homes proactive rather than reactive, improving user experience while raising switching costs in the home automation market.

Emergence of Matter standard for interoperability

Apple joined Samsung and Amazon in extending Matter support to new product categories in 2025, including robotic vacuums and major appliances. Certification data show more than 670 Thread-certified products today, and 58% of Thread Group members plan annual launches, pointing to rapid portfolio refresh cycles. By converging software, connectivity, and device discovery under a single open standard, Matter lowers developer overhead, accelerates time-to-market, and broadens the pie for every participant in the home automation market.

Energy-autonomous sensors cutting maintenance costs

Ambient harvesting modules now draw power from light, thermal gradients, or electromagnetic fields, allowing sensors to operate indefinitely without batteries. Telefónica Tech pilots have demonstrated a 95% reduction in maintenance visits for condition-monitoring nodes powered this way, saving labor and extending coverage to hard-to-reach spots [2]Telefónica Tech, “Condition Monitoring Pilot Cuts Maintenance Visits by 95%,” telefonicatech.com. Self-powered sensing lowers total cost of ownership and unlocks dense deployments that were cost-prohibitive, boosting demand for retrofit packages in the home automation market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront installation costs | -2.1% | Global, with highest impact in price-sensitive markets | Short term (≤ 2 years) |

| Cybersecurity and data-privacy concerns | -1.8% | Global, with strongest impact in EU and North America | Medium term (2-4 years) |

| Fragmented regulatory standards | -1.3% | Global, with regional variations | Long term (≥ 4 years) |

| Semiconductor supply-chain volatility | -1.6% | Global, with highest impact on hardware segments | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High upfront installation costs

Whole-home professional systems start around USD 15,000 and can exceed USD 50,000, a price tag that keeps adoption concentrated among high-income households. Hardware accounts for only a fraction of that total since electrical rewiring, network upgrades, and integrator fees often add 200-300%. DIY kits alleviate the barrier, but mid-market buyers still hesitate. Rebates such as Ontario’s 30% incentive for smart thermostats, effective January 2025, narrow the gap yet cover only energy modules rather than full automation. Cost headwinds push suppliers to modular designs and financing plans, but near-term growth in the home automation market remains sensitive to economic cycles.

Cybersecurity and data-privacy concerns

The UK’s Product Security and Telecommunications Infrastructure Act, enforced since April 2024, bans default passwords and mandates patch commitments. The EU Cyber Resilience Act, due December 2027, imposes similar duties plus mandatory vulnerability disclosure. Compliance raises development expense, especially for small brands, and the risk of data breaches deters cautious consumers. Vendors increasingly bundle security updates as paid services, inflating ownership cost and slowing demand in the home automation market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Security Dominates While Kitchens Cook Up Growth

Safety and security systems commanded 43.70% of 2025 revenue, confirming that peace of mind still tops consumer priorities in the home automation market. Adoption rose as insurers offered premium discounts for certified alarms and smart locks. The segment monetizes through hardware, cloud storage, and emergency response subscriptions, anchoring recurring cash flows. Parallel momentum comes from aging-in-place packages that blend fall detection with intrusion alerts, reinforcing future security revenue streams.

Smart kitchen solutions are forecast to grow at a 17.35% CAGR by 2031. Appliance makers weave AI into ovens that auto-regulate cooking curves and into refrigerators that track inventory and trigger e-grocery orders. GE Appliances’ Flavorly AI platform exemplifies this shift by linking recipe generation with automated restocking. As utility converges with convenience, consumers migrate budget from discretionary gadgets to everyday meal prep, keeping the home automation market diversified across necessity and novelty.

By Connectivity Technology: Thread-Powered Wireless Gains Ground

Wireless networks held 61.80% of 2025 revenue and are projected to clock 20.85% CAGR. Thread meshes extend range when each node doubles as a repeater, which solves dead-spot frustrations and reduces gateway costs. Matter certification cements Thread as the default for low-latency control traffic, while Wi-Fi maintains the pipe for video. As mobile platforms embed Thread radios natively, setup times fall, spurring uptake in the home automation market.

Wired protocols stay relevant for power-hungry or mission-critical endpoints such as shutters and high-draw cameras. Emerging Ultra-Wideband locks deliver centimeter-level presence detection for hands-free entry, enhancing security without sacrificing battery life. BLE continues to bridge smartphones with door access and occupancy triggers. Suppliers therefore pursue multi-radio chips to future-proof designs, balancing bandwidth, energy, and cost targets for the broadening home automation market.

By Component: Platforms Outpace Devices

Hardware still generated 51.10% of 2025 revenue, but software and platforms will rise at 16.40% CAGR as vendors pivot to subscriptions. Samsung’s SmartThings community grew to 350 million registered users by August 2024, illustrating the scale advantages of cloud orchestration. Edge AI lets devices process data locally yet sync improved models to the cloud, creating virtuous cycles of performance gains and user lock-in.

Commoditization is squeezing sensor margins, pushing manufacturers toward integration. Boards now combine sensing, actuation, and compute, trimming bill-of-materials and installation complexity. Gateways gradually disappear because every appliance doubles as a node. Service providers bundle firmware, monitoring, and predictive maintenance for a monthly fee, converting one-time device buyers into annuity streams within the home automation market size for managed offerings.

By Type: DIY Momentum Reconfigures Value Chains

Mainstream professionally installed systems kept 52.90% share in 2025, yet DIY solutions will grow fastest at 17.90% CAGR. Manufacturers release plug-and-play packages with app-guided pairing that mirrors smartphone onboarding. Influencer videos and peer forums reduce perceived risk, and retailers stock cross-brand starter kits to demystify choices. This evolution enlarges the home automation market by meeting middle-income budgets without installers.

Service integrators respond by pivoting to hybrid models: they design the blueprint, ship pre-configured kits, and provide remote commissioning for a fee. Luxury integrators remain safe in ultra-custom theaters and whole-estate controls, but volume shifts toward mass-market bundles. New entrants court do-it-yourselfers with open APIs, hoping community developers extend functionality and cement mindshare across the expanding home automation market.

Geography Analysis

North America accounted for 36.05% of global revenue in 2025. Federal incentives under the USD 8.8 billion Inflation Reduction Act reimburse smart thermostats and load-shifting equipment, amplifying mainstream adoption. Market penetration of 40-plus devices per household in affluent suburbs signals approaching saturation, yet retrofit demand from older housing stock maintains volume. Mexico shows rising sales through big-box retailers that bundle smart lighting with solar panels, hinting at cross-category synergies hot-wiring the home automation market.

Asia-Pacific is expected to record a 14.25% CAGR, the fastest globally. Chinese brands exploit scale economies to price below Western incumbents. Japan channels automation toward eldercare robotics that monitor vitals and send alerts to digital clinics, combining cultural acceptance with demographic urgency. South Korea tests 10 Gbps fiber backbones that remove bandwidth ceilings, letting developers trial mixed-reality overlays inside smart homes. India’s government-backed smart city rollouts seed pilot neighborhoods with subsidized IoT kits, but affordability still dictates stripped-down feature sets, forcing vendors to innovate on cost.

Europe maintains steady mid-single-digit expansion. The UK’s security-by-design law raised compliance costs yet boosted consumer trust and drove a surge in certified device sales. Germany links heat-pump subsidies to smart controls, ensuring that connected HVAC shipments outpace unconnected units. France pilots dynamic electricity tariffs transmitted by Linky smart meters, incentivizing home energy management adoption. The upcoming EU Cyber Resilience Act will propagate European security benchmarks globally, indirectly helping local firms that already design for stringent rules compete in the worldwide home automation market.

Competitive Landscape

Fragmentation defines the current stage because hardware, software, and services still evolve on separate clocks. Honeywell leverages decades of building-automation expertise to win mixed-use projects and high-end residences, reporting 8% organic growth in its building solutions segment for Q1-2025 [3]Honeywell, “Q1 2025 Earnings Presentation,” honeywell.com. Amazon counters by converting its voice assistant installed base into paid software with Alexa+ at USD 19.99 per month, deepening customer data moats and recurring revenue. Samsung broadens SmartThings from phones to appliances, aiming to lock households inside a vertically integrated ecosystem in the home automation market.

Consolidation is accelerating among mid-tier players seeking scale advantages. Resideo’s USD 1.4 billion purchase of Snap One expanded its professional installer channel while adding a catalog of security and AV gear. LG acquired Athom to infuse its appliance lineup with a cloud-agnostic control hub, illustrating the importance of platform independence. Private equity interest rises as predictable subscription cash flows mature, turning former gadget sellers into software-as-a-service portfolios.

Niche innovators hold valuable intellectual property that incumbents lack. Firms specializing in ultra-wideband presence detection, energy-harvesting chips, or edge-native AI algorithms receive strategic funding to plug gaps in broader roadmaps. Thread Group’s 200-plus members coordinate specification updates, ensuring no proprietary stack erects new lock-ins and thereby keeping rivalry centered on experience, not connectivity. Collectively, the top 10 players captured under 30% of 2024 revenue, reinforcing the mid-fragmented profile of the home automation market.

Home Automation Industry Leaders

Honeywell International Inc.

Samsung Electronics Co., Ltd.

Schneider Electric SE

Amazon.com, Inc.

Google LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Panasonic India opened a Smart Home Experience Centre designed around wellness, security, and convenience themes.

- February 2025: Honeywell announced plans to spin off its Automation division into a separate public company by 2026 to sharpen strategic focus.

- January 2025: Universal Electronics Inc. launched QuickSet homeSense technology featuring on-device learning for energy optimization and adaptive security.

- January 2025: Samsung introduced Vision AI at CES 2025, turning screens into AI companions integrated with SmartThings for real-time insights.

Global Home Automation Market Report Scope

Home automation solutions enable devices to trigger one another autonomously, eliminating human intervention. Additionally, users can schedule automated tasks, such as adjusting lighting, regulating temperature, and fine-tuning entertainment systems.

The study tracks the revenue accrued through the sale of home automation products by various players across the globe. The study also tracks the key market parameters, underlying growth influencers, and major vendors operating in the industry, which supports the market estimations and growth rates over the forecast period. The study further analyses the overall impact of COVID-19 aftereffects and other macroeconomic factors on the market. The report’s scope encompasses market sizing and forecasts for the various market segments.

The home automation market is segmented by application (lighting, entertainment (audio and video), heating, ventilation and air conditioning, safety and security, and others), connectivity type (online and offline), and geography (North America, Europe, Asia Pacific, Middle East & Africa, and Latin America). The market sizes and forecasts regarding value (USD) for all the above segments are provided.

| Lighting |

| Safety and Security |

| HVAC and Energy Management |

| Entertainment (Audio and Video) |

| Smart Kitchen |

| Smart Window Coverings |

| Others |

| Wired | |

| Wireless | Wi-Fi |

| Zigbee | |

| Z-Wave | |

| Bluetooth / BLE | |

| Thread |

| Hardware Devices | Sensors |

| Actuators and Controllers | |

| Smart Hubs and Gateways | |

| Software and Platforms | |

| Services | Installation and Integration |

| Managed and Subscription Services |

| Luxury |

| Mainstream |

| DIY |

| Managed |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| By Application | Lighting | ||

| Safety and Security | |||

| HVAC and Energy Management | |||

| Entertainment (Audio and Video) | |||

| Smart Kitchen | |||

| Smart Window Coverings | |||

| Others | |||

| By Connectivity Technology | Wired | ||

| Wireless | Wi-Fi | ||

| Zigbee | |||

| Z-Wave | |||

| Bluetooth / BLE | |||

| Thread | |||

| By Component | Hardware Devices | Sensors | |

| Actuators and Controllers | |||

| Smart Hubs and Gateways | |||

| Software and Platforms | |||

| Services | Installation and Integration | ||

| Managed and Subscription Services | |||

| By Type | Luxury | ||

| Mainstream | |||

| DIY | |||

| Managed | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia and New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the home automation market?

The home automation market was valued at USD 117.61 billion in 2026.

How fast is the home automation market expected to grow?

Between 2026 and 2031, the market is projected to expand at a 12.45% CAGR, reaching USD 211.21 billion.

What connectivity technology will dominate future deployments?

Thread-based wireless meshes paired with the Matter standard are expected to capture the majority of new device shipments.

Why are installation costs still a barrier?

Professional whole-home systems often require electrical rewiring and integrator labor, pushing total costs to USD 15,000–50,000 before rebates.

Page last updated on: