Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 23.14 Billion |

| Market Size (2026) | USD 24.44 Billion |

| Market Size (2031) | USD 32.12 Billion |

| Growth Rate (2026 - 2031) | 5.62% CAGR |

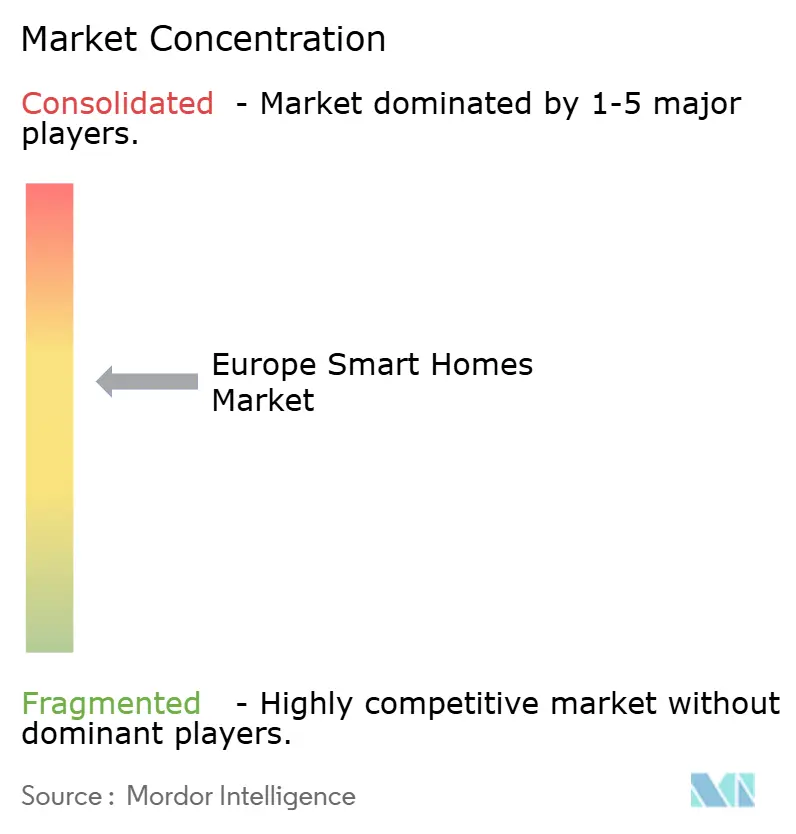

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Smart Homes Market Analysis by Mordor Intelligence

The Europe smart homes market size is projected to expand from USD 23.14 billion in 2025 and USD 24.44 billion in 2026 to USD 32.12 billion by 2031, registering a CAGR of 5.62% between 2026‐2031. Mandated zero-emission construction rules, subsidy-linked heat-pump rollouts, and dynamic power tariffs are repositioning connected devices as regulatory necessities rather than discretionary gadgets. Grid operators across the Nordics and the Netherlands now expose tariff APIs that reward automated load-shifting, accelerating uptake of demand-responsive thermostats and smart chargers. Meanwhile, the halogen-lamp phase-out and rising burglary claim severities are steering households toward networked lighting and security bundles. Vendor rivalry remains intense as building-automation incumbents defend installer channels while direct-to-consumer specialists capture do-it-yourself upgrades. Compliance-anchored demand, a maturing Matter standard, and falling component prices collectively underpin the Europe smart homes market’s medium-term momentum.

Key Report Takeaways

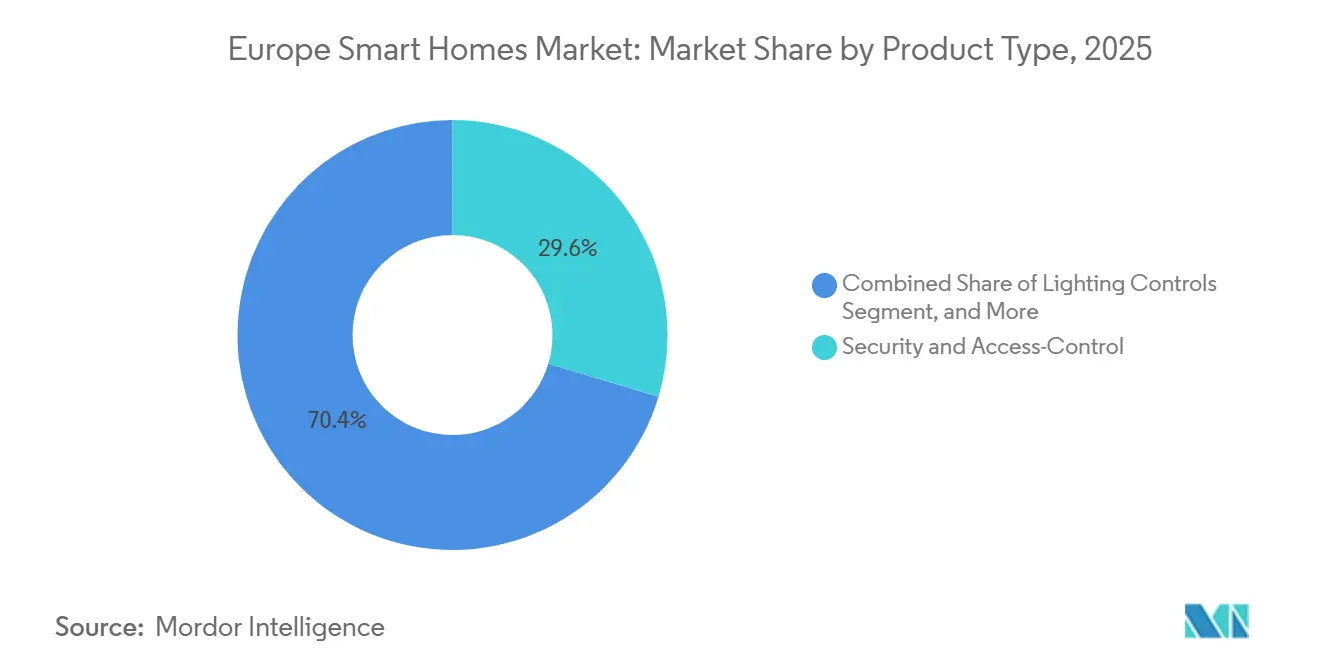

- By product type, security and access-control held 29.63% of the Europe smart homes market share in 2025. HVAC and climate-control is forecast to advance at a 6.73% CAGR through 2031.

- By installation type, retrofit projects captured 63.41% of the Europe smart homes market size in 2025. New-build integrated systems are projected to expand at a 5.94% CAGR from 2026-2031.

- By distribution channel, retail and e-commerce led with 57.86% revenue share in 2025. The professional and installer channel is set to grow at a 5.21% CAGR to 2031.

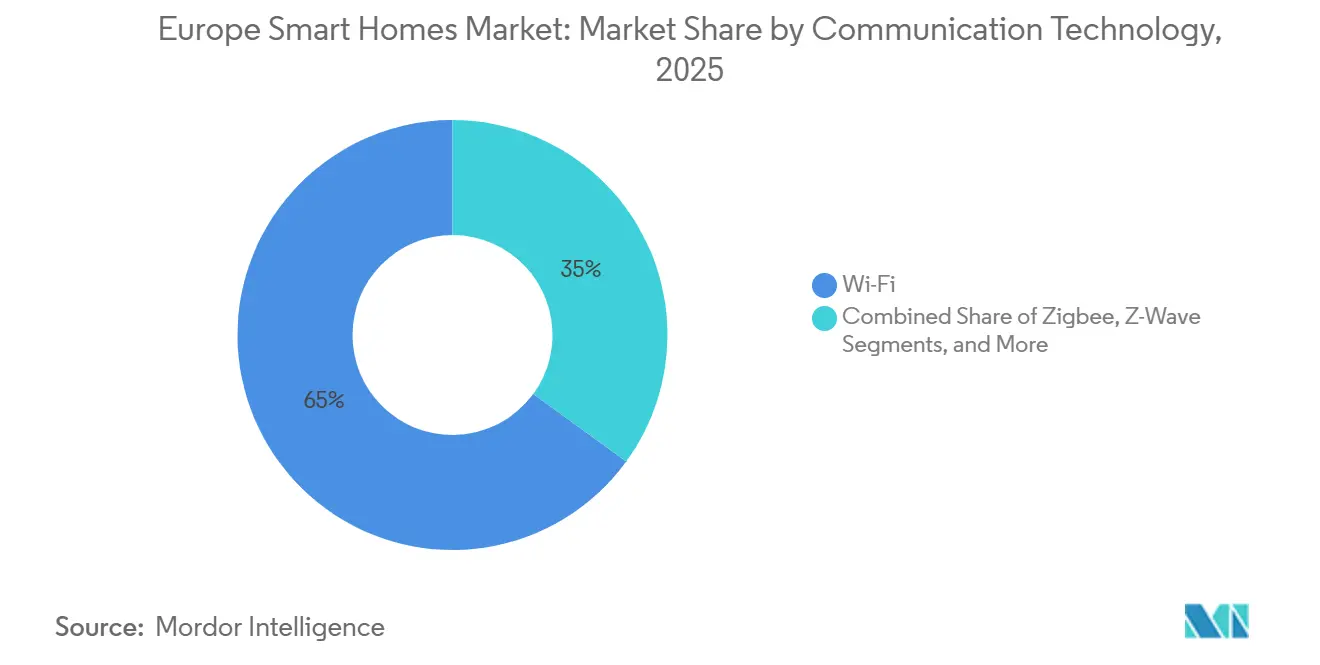

- By communication technology, Wi-Fi dominated with 64.98% share in 2025. Thread devices are expected to post the fastest 6.63% CAGR through 2031.

- By application, security and safety commanded 34.16% share of the Europe smart homes market size in 2025. Health and assisted living is projected to grow at a 6.42% CAGR to 2031.

- By geography, Germany accounted for 26% of 2025 revenue, while Norway will be the fastest-growing country at 6% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Smart Homes Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU-wide Energy-Performance Mandates for Residential Buildings | +1.8% | Global (EU-27, UK, Norway, Switzerland) | Medium term (2-4 years) |

| Surge in Security and Lighting Upgrades Among Existing Homeowners | +1.2% | Germany, UK, France, Netherlands, Nordics | Short term (≤ 2 years) |

| Rising Consumer Preference for Integrated, Voice-Controlled Ecosystems | +0.9% | Germany, UK, France, Spain, Italy | Medium term (2-4 years) |

| Smart-Appliance Subsidies Under National Electrification Programs | +0.7% | Germany, France, Netherlands, Belgium | Short term (≤ 2 years) |

| Growth of Retrofit-Ready Modular Kits for Heritage Housing | +0.5% | Italy, Spain, France (historic districts) | Long term (≥ 4 years) |

| Dynamic-Tariff Driven Demand for Home Energy-Management Platforms | +0.5% | Spain, Netherlands, Nordic countries | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

EU-wide Energy-Performance Mandates For Residential Buildings

The revised Energy Performance of Buildings Directive compels every member state to transpose zero-emission standards by 2026, forcing developers and homeowners to embed automation for heating, lighting, and ventilation into project scopes. Germany’s draft law requires smart thermostats on all new heating systems after January 2026, while France extends mandatory lighting controls to large multifamily blocks, effectively enlarging the addressable Europe smart homes market. Vendors with end-to-end platforms benefit because compliance assessments now score “automation readiness”, nudging buyers toward integrated ecosystems rather than single-purpose gadgets.[1]International Energy Agency, “Energy Efficiency 2025,” iea.org

Surge In Security And Lighting Upgrades Among Existing Homeowners

Insurers across Germany, France, and the United Kingdom offer 5-15% premium rebates for certified smart-security packages, turning doorbells and smart locks into quick-return investments.[2]European Insurance and Occupational Pensions Authority, “Premium Structures for Smart-Home Security,” eiopa.europa.eu Concurrently, the EU halogen ban is accelerating LED adoption, giving smart bulbs a natural entry point. Signify reported that one-third of its 2025 luminaires included connectivity modules, up from just over one-fifth in 2023. Together these forces amplify retrofit demand and sustain the Europe smart homes market beyond early adopters.

Rising Consumer Preference For Integrated, Voice-Controlled Ecosystems

Voice-assistant penetration hit 41% of European homes in 2025, and Matter 1.3 now permits cross-brand control for 22 device categories. Bosch observed that over two-thirds of its 2025 sales were multi-device bundles anchored by a voice hub. Major retailers respond with ecosystem-themed zones that demystify setup, a tactic lifting conversion rates and deepening brand lock-in. Platform agnosticism is fast becoming a table stake for suppliers pursuing the Europe smart homes market.

Smart-Appliance Subsidies Under National Electrification Programs

Germany, France, and the Netherlands jointly earmarked EUR 2.1 billion (USD 2.35 billion) in 2025 for rebates on connected heat pumps, thermostats, and water heaters. Subsidy eligibility hinges on connectivity to demand-response platforms, effectively converting connected functions from luxuries into baseline specifications. Schneider Electric stated that 41% of its 2025 residential energy-management sales accompanied subsidy paperwork, more than double 2023 levels. This incentive architecture turbocharges the Europe smart homes market during the forecast horizon.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront Hardware and Installation Costs | -0.9% | Southern Europe (Italy, Spain, Portugal), Eastern Europe | Short term (≤ 2 years) |

| Persistent Data-Privacy and Cyber-Security Concerns | -0.6% | Germany, France, Netherlands, Nordics | Medium term (2-4 years) |

| Fragmented Protocol Standards Hinder Interoperability | -0.4% | Global (EU-27, UK, Norway, Switzerland) | Medium term (2-4 years) |

| Shortage of Certified Smart-Home Installers | -0.3% | Germany, UK, France, Spain | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Upfront Hardware And Installation Costs

Comprehensive smart-home packages average EUR 3,500-8,000 (USD 3,920-8,960) and professional labor adds EUR 1,200-2,500 (USD 1,344-2,800). Payback stretches beyond nine years in some Southern markets where tariffs are lower, deterring middle-income households. Modular starter kits below EUR 500 (USD 560) soften entry barriers but often lack the interoperability necessary for whole-home automation, tempering immediate growth in the broader Europe smart homes market.

Persistent Data-Privacy And Cyber-Security Concerns

A March 2025 disclosure showed 18% of smart locks transmitted credentials in plaintext, triggering recalls of 340,000 units and reigniting consumer doubts.[3]European Union Agency for Cybersecurity, “EN 303 645 Certification,” enisa.europa.eu Although EN 303 645 became mandatory in 2025, one-fifth of audited products failed first-round certification. GDPR consent hurdles further restrict data-driven services, slowing the shift toward subscription revenue. These trust deficits impose a drag on the Europe smart homes market until vendors and regulators demonstrate enduring security improvements.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: HVAC Gains Speed As Energy Mandates Tighten

Security and access-control delivered USD 6.86 billion of 2025 revenue, equal to 29.63% of the Europe smart homes market share, yet HVAC and climate-control leads growth with a 6.73% CAGR. Subsidy-eligible heat pumps that must couple with smart thermostats position HVAC as the centerpiece of compliance spending. Retrofit-friendly wireless thermostats, predictive boiler controllers, and sensor-rich air handlers now outsell traditional single-zone units. Energy-management devices ride similar tailwinds as dynamic tariffs spread, while lighting controls surge on the back of the halogen withdrawal timetable and Matter certification. Smart appliances and entertainment linger behind because replacement cycles are longer and perceived incremental utility remains thin.

The competitive map is shifting accordingly. Schneider Electric and Bosch integrate HVAC, energy, and security under single dashboards, capturing bundle premiums. Conversely, camera specialists face margin pressure as generic Wi-Fi silicon lowers entry hurdles. Vendors that weld HVAC, lighting, and metering into coherent packages stand to win the next wave of Europe smart homes market demand.

By Installation Type: Retrofit Still Rules But New-Build Gains Traction

Retrofit projects tallied 63.41% of 2025 spending because more than 220 million European dwellings predate 1990. Wireless Thread and Zigbee kits reduce drilling requirements in heritage structures and cut labor costs by nearly one-third. Nevertheless, zero-emission directives and smart-ready building codes propel new-build smart systems at a brisk 5.94% CAGR. Germany and the Netherlands, buoyed by healthy construction pipelines, already see new-build share crest 40%.

Professional wholesalers stock differentiated lines for the two formats. Legrand and ABB aim retrofit ranges at electricians lacking networking expertise, while Bosch packages premounted rails for developers. Through 2031 retrofit will remain the volume anchor of the Europe smart homes market, yet the revenue gap will narrow as smart-ready construction becomes the continental norm.

By Distribution Channel: E-Commerce Widens Lead While Installers Face Labor Gaps

Retail and e-commerce commanded 57.86% of Europe smart homes market share in 2025, reflecting consumers’ preference for plug-and-play devices and next-day delivery options. Amazon alone captured 34% of online sales, helped by ecosystem storefronts that simplify cross-device bundling. Brick-and-mortar chains such as MediaMarkt and Fnac are repurposing floor space into ecosystem-branded zones, pairing in-store demonstrations with extended return windows to reduce perceived complexity. These experiential formats, together with AR-based setup guides, lower the knowledge barrier and expand the customer base beyond early adopters. Price transparency online also pressures margins, forcing vendors to differentiate through software updates and cloud services rather than hardware alone.

The professional and installer channel held 42.14% of 2025 revenue but grows more slowly at a 5.21% CAGR, limited by a 22% technician vacancy rate across Germany, France, and the United Kingdom. Complex HVAC retrofits and multi-camera security systems still favor certified contractors, yet labor shortages lengthen project lead times and suppress conversion rates. Vendors now ship pre-terminated wiring looms, self-commissioning hubs, and remote diagnostics to cut onsite hours, narrowing the cost gap with DIY offerings. Utilities piloting demand-response schemes increasingly accredit installers who can integrate smart meters, battery storage, and EV chargers under one platform, creating a premium niche. As labor pipelines strengthen through vocational programs, installer capacity should rebound, but digital channels will retain the volume advantage inside the Europe smart homes market.

By Communication Technology: Thread Surges Under Matter While Wi-Fi Maintains Anchor Role

Wi-Fi delivered 64.98% of 2025 node shipments, underpinned by ubiquitous home routers and video-camera bandwidth demands. Its high throughput supports firmware updates and edge analytics, keeping vendors of security cameras and smart displays loyal to the protocol. Still, congestion on 2.4 GHz bands and power-draw penalties curb suitability for low-duty sensors. Dual-band chipsets that toggle between 2.4 GHz and 5 GHz alleviate interference but add bill-of-materials cost, pressuring entry-level price points.

Thread posts the fastest 6.63% CAGR through 2031 because Matter names it the default low-power mesh, extending sensor battery life to five years and enabling self-healing networks. Signify’s firmware upgrades that convert legacy Zigbee bulbs to dual-stack operation illustrate a migration path that protects installed bases while unlocking multi-ecosystem compatibility. Z-Wave stabilizes at 8.7% share in door-lock and alarm niches where sub-GHz penetration matters, whereas Bluetooth Low Energy gains traction in proximity-based access control by leveraging smartphones as hubs. Proprietary radios retreat as retailers insist on Matter logos to reduce customer support calls. Protocol choice is therefore converging on a Wi-Fi plus Thread duality, and suppliers capable of shipping combo radios at scale will set de facto standards for the Europe smart homes market.

By Application: Health and Assisted Living Rises as Security Holds Prime Position

Security and safety contributed 34.16% of 2025 revenue, supported by insurance premium discounts of up to 15% for certified systems and falling camera prices. Networked doorbells, locks, and perimeter sensors remain first-purchase favorites because benefits are easy to explain and quantify. Partnerships between insurers and device makers further accelerate adoption, embedding monitoring fees into policy renewals and creating service annuities for vendors. As these bundles proliferate, feature differentiation shifts toward AI-driven anomaly detection that reduces false alarms and cuts monitoring costs.

Health and assisted living expands at a 6.42% CAGR, the fastest among all use cases, as national insurers in Germany and France reimburse fall-detection sensors and medication reminders. Europe’s aging population 24% will be 65 or older by 2030 fuels demand for technologies that enable aging in place, easing pressure on care facilities. Vendors integrate ambient motion data with vitals captured by wearables to create holistic wellness dashboards, blurring lines between medical and consumer devices. Energy and utilities management follows closely, fueled by dynamic tariffs that reward automated load shifting, while comfort lighting benefits from the halogen lamp phase-out. Together these shifts diversify spending across multiple needs, ensuring the compliance-anchored growth trajectory of the Europe smart homes market.

Geography Analysis

Northern and Western Europe account for roughly three-quarters of current spending, anchored by Germany’s USD 6.02 billion tally and the United Kingdom’s USD 4.48 billion slice. These nations combine strict building codes, wide broadband availability, and mature retail channels, positioning them as launch pads for new device classes. Norway, Denmark, and Sweden, while smaller in absolute volume, boast the highest device per-home ratios because real-time tariffs and electric-vehicle penetration amplify energy-automation payoffs.

Southern Europe trails on purchasing power but is catching up through EU Recovery and Resilience Facility grants that underwrite deep retrofits. Spain has already connected 38% of households to dynamic tariffs, accelerating smart HVAC and battery adoption despite relatively lower electricity prices. Italy benefits from heritage-safe wireless kits that comply with preservation rules, reducing retrofit friction.

Eastern Europe remains under 5% of total expenditure yet represents a medium-term expansion frontier. Rising disposable incomes and ongoing smart-meter rollouts lay the groundwork for connected appliances, particularly in Poland and the Czech Republic. Cohesion financing earmarked for residential efficiency upgrades should close affordability gaps and enlarge the accessible Europe smart homes market in the latter half of the forecast window.

Competitive Landscape

The ten largest suppliers held nearly 42% of 2025 revenue, implying a moderate concentration. Schneider Electric, Legrand, and ABB defend installer channels by embedding connectivity into switchgear, breakers, and HVAC controllers, leveraging long-standing contractor networks. Signify, Bosch, and Somfy extend their reach via Matter compatibility, ensuring bulbs, sensors, and motors function seamlessly inside heterogeneous homes. Direct-to-consumer innovators, tado°, Nuki, and Eve Systems, court do-it-yourself buyers with app centric simplicity and subscription analytics, willingly accepting lower gross margins for recurring income streams.

Health-centric white space invites cross-sector alliances. Netatmo partners with insurers for air-quality programs, while Bosch pilots elder-care bundles with German sickness funds. Private-label devices from IKEA and Lidl exploit Matter to skip custom integrations, intensifying price competition in lighting and plugs.

At the protocol level, Thread vendors gain a head start as Matter matures, but Wi-Fi incumbents protect video doorbells and indoor cameras where bandwidth appetite is highest. Mergers will likely rise as smaller brands struggle with certification overheads, nudging the Europe smart homes market toward a tighter top-tier over the next five years.

Europe Smart Homes Industry Leaders

Signify N.V.

Robert Bosch GmbH (Bosch Smart Home)

Schneider Electric SE

Legrand SA

Somfy SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Schneider Electric invested EUR 120 million (USD 134 million) to enlarge its Grenoble plant for Matter-certified energy-management gear.

- January 2026: Nuki unveiled Smart Lock Pro and Go with built-in Matter and Thread, targeting GDPR-compliant local processing.

- December 2025: Bosch Smart Home released SensorPro Thread sensors offering five-year battery life and tri-ecosystem support.

- November 2025: Nuki raised EUR 45 million (USD 50 million) to craft a bridge-free Matter smart lock and expand into Southern Europe.

Europe Smart Homes Market Report Scope

The Europe Smart Homes Market Report is Segmented by Product Type (Lighting Controls, Energy-Management Devices, Security and Access-Control, Smart Entertainment, Smart Appliances, HVAC and Climate-Control), Installation Type (New-Build Integrated Systems, Retrofit and Existing-Home Upgrades), Distribution Channel (Professional and Installer Channel, Retail and E-commerce), Communication Technology (Wi-Fi, Zigbee, Z-Wave, Bluetooth and BLE, Thread, Others), Application (Security and Safety, Energy and Utilities Management, Comfort and Lighting, Entertainment and Lifestyle, Health and Assisted Living), and Geography (United Kingdom, Germany, France, Italy, Spain, Netherlands, Rest of Europe). The Market Forecasts are Provided in Terms of Value (USD).

By Product Type

| Lighting Controls |

| Energy-Management Devices |

| Security and Access-Control |

| Smart Entertainment |

| Smart Appliances |

| HVAC and Climate-Control |

By Installation Type

| New-Build Integrated Systems |

| Retrofit/Existing-Home Upgrades |

By Distribution Channel

| Professional/Installer Channel |

| Retail and E-commerce (DIY) |

By Communication Technology

| Wi-Fi |

| Zigbee |

| Z-Wave |

| Bluetooth and BLE |

| Thread |

| Other Communication Technologies (EnOcean, Matter, RF, etc.) |

By Application

| Security and Safety |

| Energy and Utilities Management |

| Comfort and Lighting |

| Entertainment and Lifestyle |

| Health and Assisted Living |

By Country

| United Kingdom |

| Germany |

| France |

| Italy |

| Spain |

| Netherlands |

| Rest of Europe |

| By Product Type | Lighting Controls |

| Energy-Management Devices | |

| Security and Access-Control | |

| Smart Entertainment | |

| Smart Appliances | |

| HVAC and Climate-Control | |

| By Installation Type | New-Build Integrated Systems |

| Retrofit/Existing-Home Upgrades | |

| By Distribution Channel | Professional/Installer Channel |

| Retail and E-commerce (DIY) | |

| By Communication Technology | Wi-Fi |

| Zigbee | |

| Z-Wave | |

| Bluetooth and BLE | |

| Thread | |

| Other Communication Technologies (EnOcean, Matter, RF, etc.) | |

| By Application | Security and Safety |

| Energy and Utilities Management | |

| Comfort and Lighting | |

| Entertainment and Lifestyle | |

| Health and Assisted Living | |

| By Country | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Netherlands | |

| Rest of Europe |

Key Questions Answered in the Report

How big will connected devices spending be in European homes by 2031?

The Europe smart homes market is forecast to reach USD 32.12 billion by 2031, expanding at a 5.62% CAGR from 2026-2031.

Which product category is growing fastest in European households?

HVAC and climate-control devices, boosted by subsidy-linked heat-pump mandates, are projected to post a 6.73% CAGR through 2031.

Why is Norway advancing more quickly than other countries?

Real-time electricity tariffs and high electric-vehicle penetration push automated load-shifting solutions, driving a 6% CAGR in Norway.

What policy changes most influence adoption rates?

The EU Energy Performance of Buildings Directive, which requires zero-emission new builds and deep retrofits, embeds automation into compliance pathways across the region.

How are retailers countering installer shortages?

E-commerce giants offer plug-and-play ecosystems, while brick-and-mortar chains create ecosystem zones with on-site setup help, sustaining retail and online sales growth at a 5.96% CAGR.

Which communication protocols will dominate future devices?

Wi-Fi remains pervasive, but Thread is the fastest riser because Matter names it the preferred low-power mesh, attracting over 400 certified devices in 2025.

Page last updated on: