Smart Home Installation Service Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 12.73 Billion |

| Market Size (2031) | USD 37.96 Billion |

| Growth Rate (2026 - 2031) | 24.43% CAGR |

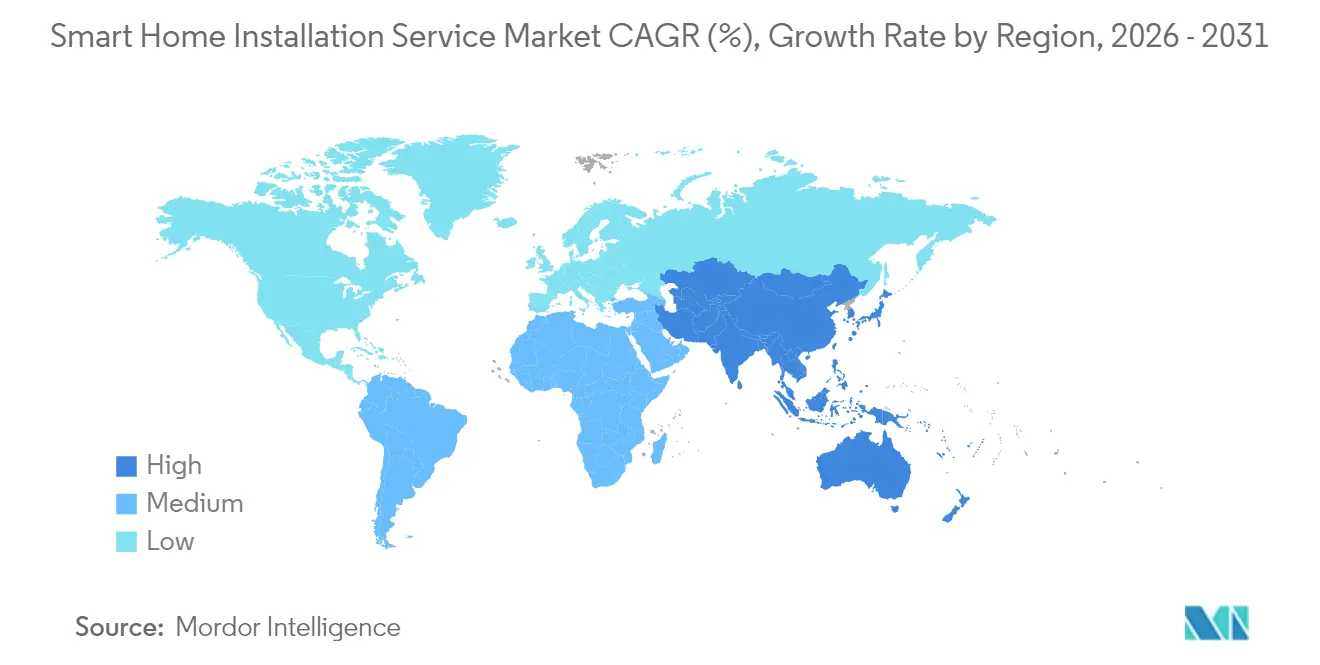

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Smart Home Installation Service Market Analysis by Mordor Intelligence

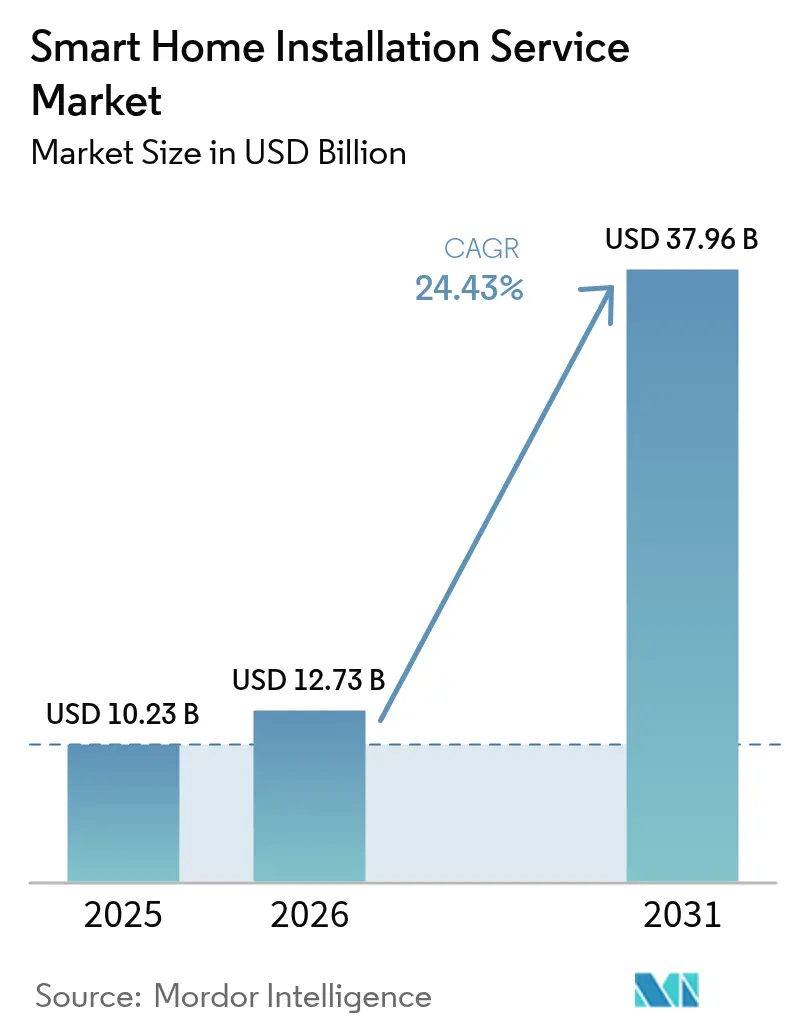

The smart home installation service market size is expected to grow from USD 10.23 billion in 2025 to USD 12.73 billion in 2026 and is forecast to reach USD 37.96 billion by 2031 at 24.43% CAGR over 2026-2031. Falling hardware prices, near-ubiquitous broadband, and energy-retrofit incentives are persuading households and businesses to shift from do-it-yourself devices to professionally configured ecosystems. Insurance premium discounts that favor connected sensors, combined with regulatory encouragement for energy efficiency, are widening the customer base for installers.[1]State Farm, “Smart Home Discount Program,” statefarm.com Telecom and e-commerce players now bundle installation with network subscriptions and same-day delivery, expanding distribution reach. Meanwhile, shortages of certified technicians and persistent data-privacy concerns create operational friction that limits capacity growth. In this environment, the smart home installation service market rewards providers that pair device mounting with network optimization and ongoing firmware management, turning one-off projects into subscription-style revenue streams.

Key Report Takeaways

- By system, home monitoring and security held 45.86% of the smart home installation service market share in 2025, while smart appliance services are forecast to grow at a 26.12% CAGR through 2031.

- By channel, retailers led with a 51.62% revenue share in 2025; e-commerce is projected to advance at a 24.88% CAGR to 2031.

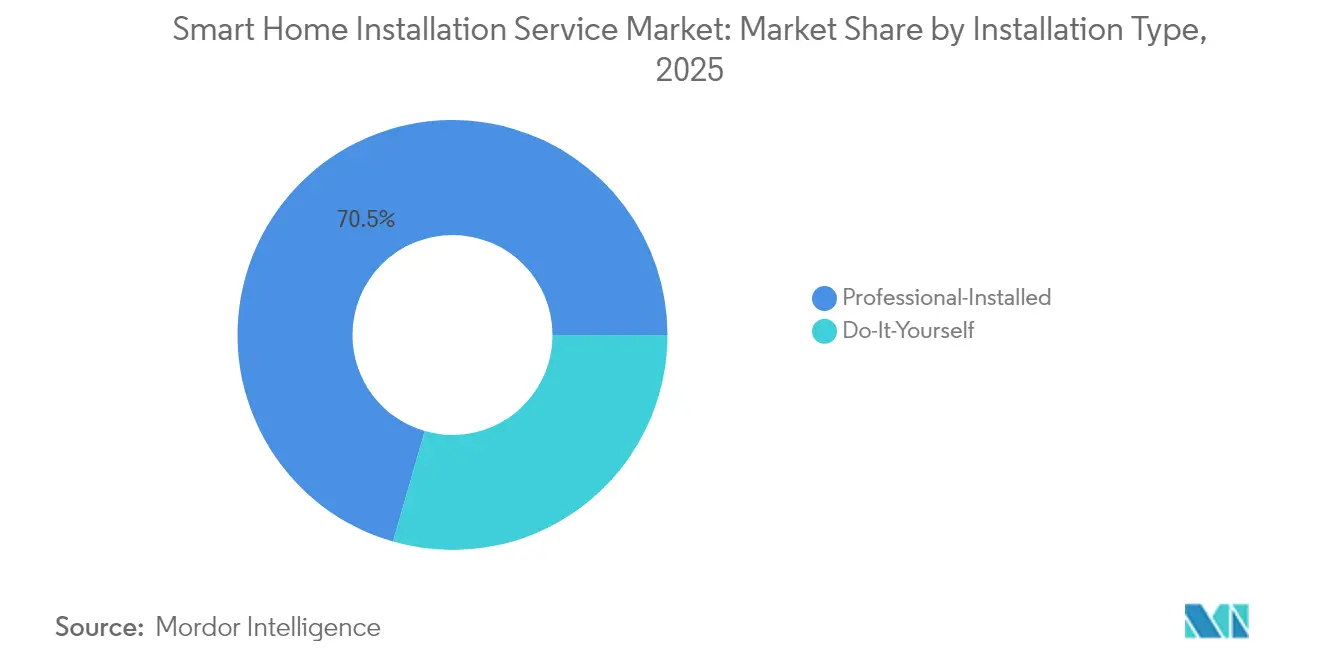

- By installation type, professional services accounted for 70.54% of 2025 revenue; however, DIY kits are expected to expand at a 28.64% CAGR through 2031.

- By customer type, residential clients accounted for 83.72% of 2025 sales, while commercial and small business demand is projected to rise at a 24.96% CAGR to 2031.

- By dwelling type, single-family homes commanded a 53.74% share of the smart home installation service market size in 2025, whereas multi-unit properties are set to climb at a 25.96% CAGR.

- By connectivity, Wi-Fi devices captured a 57.62% share in 2025; meanwhile, Thread protocol installations are projected to accelerate at a 27.18% CAGR through 2031.

- By geography, North America retained a 39.38% share in 2025; the Asia Pacific is the fastest-growing region, with a 25.12% CAGR projected toward 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Smart Home Installation Service Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Disposable Income in Developing Countries | +3.2% | Asia Pacific core, spillover to the Middle East and Latin America | Medium term (2-4 years) |

| Rapid Broadband and 5G Rollouts Enabling Professional Installations | +5.8% | Global, with early gains in South Korea, China, the United States, United Arab Emirates | Short term (≤ 2 years) |

| Declining Average Selling Price of Smart Home Hubs | +4.1% | Global | Short term (≤ 2 years) |

| Government Tax Incentives for Energy-Efficient Retrofits | +4.6% | North America and Europe, emerging in India and Brazil | Medium term (2-4 years) |

| Growth of Insurance-Linked Discounts for Connected Homes | +3.9% | North America and Europe | Medium term (2-4 years) |

| Emerging Demand for Aging-in-Place Assisted-Living Solutions | +4.3% | Japan, Germany, the United States, and Canada | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Broadband and 5G Rollouts Enabling Professional Installations

Fiber-to-the-premises coverage reached 64% of United States households by mid-2024, while India logged 945 million broadband subscriptions the same year. South Korea completed nationwide 5G standalone deployment in early 2024, removing latency barriers for real-time video analytics. These infrastructure gains shift the customer pain point from connectivity to configuration, prompting households to pay for expert network segmentation and traffic prioritization. Professional installers now bundle mesh-router tuning and device commissioning, commanding premium fees in dense urban markets. Apartment managers also rely on installers to centralize access controls and tenant authentication, turning connectivity upgrades into recurring service contracts.

Government Tax Incentives for Energy-Efficient Retrofits

The U.S. Inflation Reduction Act extends a USD 2,000 annual credit for smart HVAC controls through 2032.[2]Internal Revenue Service, “Energy Efficient Home Improvement Credit,” irs.gov Germany set aside EUR 300 million (USD 339 million) in 2024 to fund integrated energy-saving systems. India’s Smart Meter National Programme requires real-time consumption feedback, which in turn drives demand for in-home displays and sub-metering installations. These incentives compress payback periods for smart thermostats and lighting controls, making professional installation economically attractive even in retrofit scenarios. Service providers that navigate rebate paperwork and certification standards secure a trusted-advisor role, deepening customer stickiness.

Growth of Insurance-Linked Discounts for Connected Homes

State Farm offers up to 15% premium reductions for professionally installed water leak sensors and smoke detectors. Liberty Mutual expanded its discount plan in mid-2024 to include video doorbells and motion-triggered lighting.[3]Liberty Mutual, “Smart Home Discount Expansion,” libertymutual.com Allianz reported 22% growth in connected-home policies across Germany and France during 2024. This insurer endorsement converts discretionary purchases into compliance must-haves, guaranteeing installers a stream of referred projects. The model is especially potent in flood or wildfire zones, where coverage hinges on verified sensor deployments.

Emerging Demand for Aging-in-Place Assisted-Living Solutions

Japan’s population aged 65 and older reached 29.1% in 2024, spurring subsidies for fall-detection sensors and voice-activated lighting. In the United States, Medicare now reimburses remote patient monitoring devices installed in private homes. Germany allocated EUR 250 million (USD 283 million) in 2024 for smart locks and emergency alert systems. Installers collaborate with occupational therapists to tailor device placement and caregiver dashboards, commanding higher margins than commodity security work. This demand extends well beyond 2030 as global aging trends accelerate.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data Privacy and Security Concerns | -2.8% | Global, acute in Europe and California | Short term (≤ 2 years) |

| Shortage of Certified Smart Home Installers | -3.1% | North America and Europe | Medium term (2-4 years) |

| Interoperability Issues Among Proprietary Ecosystems | -2.3% | Global | Medium term (2-4 years) |

| Inflation-Driven Slowdown in Residential Construction | -1.9% | North America and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Data Privacy and Security Concerns

The European Data Protection Board classifies installers as data controllers under GDPR, exposing firms to fines of up to EUR 20 million for mishandling sensor data.[4]European Data Protection Board, “Guidelines on Smart Home Data Processing,” edpb.europa.eu California’s Privacy Rights Act demands granular disclosures on data retention and third-party sharing. A 2024 breach involving 1.2 million cameras highlighted the financial risk of weak encryption, prompting insurers to exclude cyber liability coverage for unencrypted installations. Installers now pursue cybersecurity certifications and offer network segmentation, but these add 15-20% to project cost and slow adoption among price-sensitive customers.

Shortage of Certified Smart Home Installers

CEDIA members reported an average of 4.2 unfilled technician positions in 2024, with time-to-hire exceeding 90 days. Certification requires 18 months of fieldwork across networking, audiovisual, and electrical safety, limiting the talent pipeline. U.S. median installation labor reached USD 125 per hour in 2024, up 18% from 2022. Rising rates tempt consumers toward DIY kits, while project backlogs delay conversions for business customers. Some platforms pilot tiered certification that allows junior techs to handle basic pairings, but liability and quality-control hurdles limit its scalability.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By System: Security Dominates, Appliances Propel Growth

Home monitoring and security systems accounted for 45.86% of the smart home installation service market share in 2025, driving overall revenue for installers. Demand stems from persistent concerns about crime, the falling cost of AI-enabled cameras, and the appeal of bundled monitoring contracts that lock in recurring fees. As a result, professional firms position security as the entry point for broader device ecosystems, often returning to the same household later to layer on additional sensors or lighting controls. In contrast, smart appliances represent the fastest-growing use case at a 26.12% CAGR toward 2031, as brands embed Wi-Fi and Thread radios in refrigerators, ovens, and washers that require professional commissioning. Manufacturers now ship appliances with over-the-air update capability, encouraging homeowners to pay technicians for firmware management, warranty validation, and predictive-maintenance setup.

Thread adoption inside connected kitchen and laundry equipment is cutting installation time by simplifying onboarding processes, which further widens installer margins. Matter-certified appliances eliminate the need for proprietary apps, enabling a single commissioning workflow that reduces truck-rolls and post-visit support calls. As the installed base scales, the smart home installation service market size benefits from follow-up visits to integrate appliances into centralized energy dashboards, pushing upsell potential beyond the original project scope. Legacy Zigbee and Z-Wave devices remain in older security panels, so installers maintain dual expertise to avoid stranding earlier investments while shepherding households toward future-proof, Thread-based networks.

By Channel: E-Commerce Carves Share from Storefronts

Retail stores accounted for 51.62% of the smart home installation service market share in 2025, buoyed by live demo displays and in-person advisors who convert shoppers into same-day installation customers. Big-box chains combine point-of-sale financing with white-glove technician dispatch, creating convenience that justifies premium pricing. However, e-commerce platforms are expanding at a 24.88% CAGR thanks to transparent pricing, next-day delivery, and checkout flows that bundle installation services in one click. Online ratings and guaranteed arrival windows improve buyer confidence, eroding the showroom advantage traditional retailers once held.

Installers operating through digital aggregators must accept standardized price lists and 15-25% commissions, which compress gross margins but deliver steady project volume. Some independent firms respond by boosting direct-to-consumer marketing, relying on localized search ads and referral incentives to bypass marketplace fees. Original equipment manufacturers such as integrated security providers still favor vertically aligned sales models, capturing the entire margin stack from hardware to monitoring. The competitive tension among storefronts, e-commerce, and OEM-direct models expands the overall smart home installation service market size by providing consumers with multiple, channel-agnostic paths to professional help.

By Installation Type: DIY Expansion Amid Professional Lead

Professionally installed packages generated 70.54% of 2025 revenue, reflecting consumer reluctance to tackle structured wiring, exterior drilling, and multi-vendor integrations. Installers differentiate by offering design consultations, network optimization, and ongoing maintenance subscriptions that extend revenue beyond a one-time visit. Yet DIY kits are rising at a 28.64% CAGR, propelled by QR-code onboarding, adhesive mounts, and video tutorials that lower entry barriers. Entry-level users often self-install a video doorbell or smart plug first, then hire technicians later for more complex whole-home projects.

This blended behavior shifts the professional focus toward higher-margin design and programming, rather than basic device mounting, thereby protecting profitability even as the DIY segment grows. Hybrid service models, where customers mount devices while technicians perform remote commissioning, are emerging but remain niche due to gaps in broadband quality and liability concerns. The coexistence of DIY and professional tiers keeps the smart home installation service market size robust, as households progress up an adoption ladder that ultimately returns them to experts for more complex integrations.

By Customer Type: Commercial Uptick Complements Residential Core

Residential households accounted for 83.72% of the 2025 revenue for the smart home installation service market, driven by the benefits of safety, energy savings, and voice-assistant convenience. Typical projects cover intrusion detection, smart thermostats, and automated lighting scenes tailored to family routines. In parallel, commercial and small business deployments are growing at a 24.96% CAGR to 2031, driven by energy management mandates, insurance requirements, and employee experience upgrades. Retailers add occupancy sensors to comply with municipal codes, while coworking spaces install smart locks that grant temporary access and log usage data.

Commercial work commands higher average order values but comes with longer payment terms, stricter code compliance requirements, and the need to interface with building management systems. Installers who secure LEED accreditation and collaborate with property managers gain an edge in winning multi-location contracts. As enterprises prioritize sustainability and automation, the commercial segment is expected to widen its share of the smart home installation service market size, even though residential jobs will continue to dominate unit volumes.

By Dwelling Type: Multi-Unit Installations Scale Rapidly

Single-family residences accounted for 53.74% of market revenue in 2025, benefiting from homeowner autonomy and straightforward access to walls, attics, and breaker panels. Detachments typically involve fewer stakeholders, enabling faster approvals and clear accountability for ongoing service. Multi-unit dwellings, however, are expanding at a 25.96% CAGR because property managers see smart locks, leak sensors, and thermostats as value-add amenities that cut operating costs and attract tenants. Bulk rollouts across hundreds of apartments unlock hardware discounts and travel efficiencies, raising installer margins while enlarging the smart home installation service market share captured by specialist multifamily contractors.

Retrofit projects dominate the volume because the existing housing stock far outnumbers new builds; however, new construction offers higher profitability by allowing for pre-wiring and centralized control panel placement. Installers skilled in low-voltage retrofits excel in historic districts where drilling is restricted, relying on battery-powered Thread sensors that reduce wiring time by up to 40%. The convergence of retrofit demand and new-build standards keeps the dwelling-type mix dynamic, ensuring that diversified installers can balance near-term volume with long-term margin expansion to grow their stake in the overall smart home installation service market size.

By Connectivity Standard: Thread Momentum Under Wi-Fi Canopy

Wi-Fi devices commanded 57.62% of the smart home installation service market share in 2025, prized for their high-bandwidth video doorbells and cameras, which dominate consumer awareness. Installers favor Wi-Fi for its ubiquity, but they contend with power-draw limits that restrict the placement of battery-operated sensors. Thread devices are advancing at a 27.18% CAGR through 2031, offering low-power mesh networking that extends battery life and simplifies range extension without extra access points. Apple, Google, and Amazon products now double as Thread border routers, lowering network infrastructure costs for consumers and reducing the need for installer truck rolls for range issues.

Legacy Zigbee and Z-Wave estates still populate early smart homes, so technicians maintain multi-protocol commissioning tools to avoid orphaning older hardware. Matter’s unifying framework points toward fewer compatibility headaches, but the transitional period adds complexity as households blend new Thread devices with legacy gear. Installers that invest in Thread and Matter certifications signal future-proof expertise, positioning themselves as trusted advisors who can shepherd homeowners through protocol evolution. In doing so, they increase the size of the smart home installation service market while reducing future support calls related to obsolescence.

Geography Analysis

North America maintained a 39.38% share of the smart home installation service market in 2025. High broadband penetration, homeowner insurance incentives, and strong retail chains underpin demand in the United States and Canada. Mexico presents an emerging opportunity as fiber rollouts in major metropolitan areas unlock multi-device demand, although installer scarcity outside urban centers limits scale. Growth here is moderating as affluent suburbs reach saturation, prompting installers to shift toward retrofit upgrades and commercial projects.

Asia Pacific is the fastest-growing region with a 25.12% CAGR outlook. China’s mandate for smart-ready construction in new towers compels developers to pre-install conduits and panels. India’s fiber-to-the-home base exceeded 30 million subscribers in 2024, with broadband packages bundling smart-home starter kits and local installation. Japan’s aging population fuels government subsidies for assistive sensors, while South Korea’s 5G backbone supports real-time analytics and remote diagnostics. Language diversity, price sensitivity, and regulatory fragmentation continue to challenge cross-border service standardization; however, urban density creates volume efficiencies for installers.

Europe, the Middle East, and Africa present mixed prospects. Germany and the United Kingdom benefit from energy efficiency mandates and mature e-commerce, but GDPR compliance adds cost and slows down decision-making cycles. Southern European markets grow more slowly due to lower homeownership and fragmented installer bases. In the Middle East, the United Arab Emirates and Saudi Arabia are investing in smart-building certifications as part of their diversification plans, driving high-end installation contracts. Africa remains nascent, with limited development, primarily confined to gated communities in South Africa, Nigeria, and Kenya, where broadband and stable power are available. Currency volatility and import duties prompt installers to partner with local distributors to hedge risk.

Regulatory Landscape

Regulation affecting smart home installation services is tightening around cybersecurity, data protection, and interoperability, which raises compliance expectations for the devices installers deploy and the data they handle. In Europe, installers operating as data controllers under GDPR face elevated obligations for sensor and camera data handling. The EU Cyber Resilience Act also introduces a 24-hour reporting requirement for actively exploited vulnerabilities starting 11 September 2026, which pushes manufacturers and service providers toward stronger post-install monitoring and incident workflows.

Market-access rules are also beginning to reference specific interoperability stacks, shaping what installers can recommend and support at scale. From 1 October 2026, an amendment to the EU Radio Equipment Directive (CE-RED) makes Matter 2.4 compliance a requirement for Wi-Fi 7 IoT end devices. In the United States, the FCC requires a Matter 2.0 interoperability validation report for Wi-Fi 7 IoT terminal devices seeking an FCC ID from the same date. Australia added a security baseline through the Cyber Security (Security Standards for Smart Device) Rules 2025, which commenced on 4 March 2026 for consumer connectable devices. China implemented GB/T 46456.1-2025 on 1 February 2026 and advanced additional interconnection standardization via a MIIT draft plan released on 16 March 2026.

Value Chain Analysis

The value chain starts with device, chipset, and platform providers, including security sensors and cameras, thermostats and HVAC controls, smart appliances, hubs and routers, and cloud or app layers. Certification and onboarding toolchains for Wi-Fi, Thread, and Matter then feed into distribution through OEM-direct channels, retailers, and e-commerce, followed by service delivery from installers, integrators, and telecom-led technician networks. Demand is increasingly pulled by multi-device projects where network quality, identity and access management, and firmware lifecycle management are part of the installation scope rather than add-ons, shifting more value toward pre-configuration, on-site commissioning, and post-install remote support.

Execution depends on orchestration across low-voltage trades and software provisioning, with workforce scheduling, skills certification, and interoperability troubleshooting as key bottlenecks. A builder- and property-led channel is reinforcing an end-to-end model in which a single integration partner manages design, installation, and warranty support, which can reduce post-close service calls and create recurring service revenue. Ecosystem moves that simplify cross-brand integration also compress install time and reduce return visits, including Samsung SmartThings enabling direct integration of IKEA Matter-over-Thread devices (April 2026) and the Silicon Labs and Signify collaboration to enable concurrent Zigbee and Matter over Thread support for Philips Hue (June 2026). Together, these initiatives help installers bridge legacy and Matter-based deployments without stranding existing systems.

Competitive Landscape

No single vendor holds a significant global market share, making the smart home installation service market highly competitive. ADT and Vivint rely on vertically integrated models that pair hardware, installation, and monitoring contracts, lowering churn through multi-year agreements. Retailers such as Best Buy and Amazon harness gig-economy technicians for same-day projects, prioritizing speed and flat pricing. Telecom operators, including Comcast and Cox, embed installation into broadband bundles, using home visits to upsell higher internet tiers. Fragmented local contractors excel in white-glove retrofit work, leveraging word-of-mouth reputations to defend regional niches.

Technology is reshaping service delivery. Augmented-reality guides enable junior technicians to follow step-by-step overlays, thereby reducing training cycles. Resideo filed a patent in 2025 for cloud provisioning that halves on-site time by pre-configuring devices. Matter compliance narrows the knowledge gap across vendor ecosystems, enabling platforms to deploy staff more flexibly, though backward-compatibility demands dual expertise for legacy gear. Regional licensing rules for low-voltage work still favor entrenched contractors in jurisdictions with strict electrical codes, hindering the rapid national rollouts of digital platforms.

Pricing pressure remains acute. Installer labor costs rose 18% between 2022 and 2024, prompting some consumers to opt for DIY solutions. Platforms experiment with subscription models that bundle unlimited installations for a monthly fee, trading margin for predictable revenue. Consolidation is underway: Vivint’s 2025 acquisition of a southeastern installer network added 200 technicians and widened two-hour coverage to 90% of the U.S. population. Yet the market remains open for niche specialists in commercial small business, multi-unit housing, and aging-in-place solutions where tailored expertise commands premium rates.

Smart Home Installation Service Industry Leaders

Calix Inc.

HelloTech Inc.

Red River Electric Inc.

Vivint Inc.

Insteon Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Interoperability and simplified commissioning are broadening what installers can deliver through standardized playbooks across mixed device estates, creating room to package multi-vendor systems with more predictable outcomes. The Connectivity Standards Alliance announcement of Matter 1.6 in June 2026, including NFC-based commissioning and Joint Fabric for cross-platform network management, supports more repeatable setup across ecosystems and encourages service providers to operationalize remote diagnostics, standardized handoffs, and multi-platform support as billable services rather than bespoke troubleshooting.

Recurring service models and higher-assurance security practices are also becoming more prominent differentiators as privacy and cybersecurity obligations intensify and homeowners and small businesses expect ongoing updates. Trade channels focused on integrator operations in 2026 align with installer moves to productize maintenance, firmware management, and network segmentation, particularly for security-heavy deployments that anchor a large share of installation work. Insurer-led smart home discount structures and energy-retrofit incentives, including the US Inflation Reduction Act credit for smart HVAC controls through 2032, reinforce demand for verified installations and documentation. This creates a practical opportunity for providers that can manage rebate and compliance paperwork alongside installation.

Recent Industry Developments

- June 2026: Vivint launched the Vivint Smart Hub Pro 2, expanding touchscreen-led control and customization for connected security and smart home routines. The new hub improves Vivint's ability to standardize in-home commissioning and support across multi-device installs, which can reduce service variability and increase attach rates for ongoing monitoring and service plans.

- February 2026: Vivint introduced Vivint for Builders, an end-to-end smart home solution that manages planning, installation, and setup for homebuilders. This builder-facing delivery model shifts more installations upstream into new construction workflows and creates a repeatable deployment path across housing developments rather than single-home jobs.

- June 2024: Latch (now operating as DOOR Services) announced an agreement to acquire HelloTech to form a foundation for on-demand installation and connected device support. Folding a gig-enabled installation network into a property and access-focused platform broadens routes to market for smart home support, especially in multifamily settings where centralized service dispatch is valued.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market is defined as revenue generated from services that install, configure, and integrate smart home systems in homes and small premises, including on-site labor and related setup work needed to make devices operate together.

Scope exclusions: We exclude the value of smart home devices sold as products, pure software subscriptions, and ongoing security monitoring fees when they are billed separately from installation work.

Segmentation Overview

- By System

- Lighting Control

- Home Monitoring/Security

- Thermostat

- Video Entertainment

- Smart Appliances

- Other Systems

- By Channel

- Retailers

- E-Commerce

- Original Equipment Manufacturer (OEM)

- By Installation Type

- Professional-Installed

- Do-It-Yourself (DIY)

- By Customer Type

- Residential

- Commercial/Small Business

- By Dwelling Type

- Single-Family Homes

- Multi-Unit Dwellings

- New-Build Constructions

- Retrofit Projects

- By Connectivity Standard

- Wi-Fi

- Zigbee

- Z-Wave

- Thread

- Bluetooth Mesh

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Kenya

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build the basic demand map and to set realistic ranges for pricing and service volumes before assumptions were tested. We relied on public sources such as the US Census Bureau housing and construction series, Eurostat housing statistics, national building and energy agencies, ITU connectivity indicators, and customs trade series where relevant to smart home equipment flows. These sources helped us understand where new builds and retrofits are happening, and how connectivity readiness is shifting in key countries.

Alongside official statistics, we reviewed installer association sites, building code and incentive notes, company filings and investor presentations from service providers and ecosystem participants, plus reputable news coverage on home automation adoption. A few paid database subscriptions were used selectively for company financials and intelligence, patent tracking in connected-home standards, and shipment-level import and export checks to sanity-check regional activity. The sources listed here are illustrative only, and many other public documents and datasets were also referenced to collect, validate, and clarify the analysis.

Primary Interviews and Surveys

Primary inputs were collected through expert interviews and structured surveys with installers, channel partners, and solution specifiers. We also used selected end-customer checks to confirm buying triggers and typical job sizes. Since this is a global service market, interviews across Americas, EMEA, and APAC were used to validate how labor rates, device mix, and retrofit share differ, and then to pressure-test the final assumptions used in the model.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 34% | CXOs: 14% | APAC: 45% |

| Mid tier: 50% | Functional/Unit leaders: 39% | EMEA: 35% |

| Smaller Players: 16% | Managers: 47% | Americas: 20% |

Market-Sizing & Forecasting

Sizing starts from a top-down demand pool build where housing activity and connectivity readiness are used to reconstruct addressable installation jobs across regions, followed by applying adoption and professional-install penetration assumptions. The totals were then corroborated with selective bottom-up approximations using sampled installer revenue ranges, channel checks on job counts, and a simple ASP (service ticket) times volume logic, which was used to adjust outliers.

Key inputs in the model include new-build starts and completions, retrofit and renovation intensity, smart home adoption rates by household, share of professional-installed versus DIY setups, typical service ticket size by system complexity, and labor rate movements across major metros. Where data is patchy for smaller countries, we used proxy indicators like broadband and smart speaker penetration alongside housing stock, and then refined the split using primary feedback on actual attach rates.

For forecasting, we used scenario analysis supported by short series trend fitting (exponential smoothing on leading indicators) because adoption and labor pricing can shift quickly after policy changes and macro cycles. Assumptions were stress-tested with experts on how bundles (security, lighting, thermostat, video, and appliances) are evolving, and how interoperability standards are changing the time spent per installation.

Data Validation & Update Cycle

Validation is done through triangulation across independent signals so the final number stays tied to real-world service activity. We check for variance against housing construction trends, connectivity and smart home adoption signals, and known pricing bands from interviews, and then investigate large deviations before sign-off. When a datapoint conflicts with the broader story, it is re-reviewed and, when needed, respondents are re-contacted to confirm whether the issue is timing, scope, or currency conversion.

Each report is refreshed annually, and interim updates are made when material events occur, such as major changes in housing demand or installer labor inflation. Before delivery, an analyst completes a final pass to ensure the latest public releases and interview learnings are reflected in the model outputs.

Mordor Intelligence's Smart Home Installation Service Market Size Versus Other Published Estimates

Published market sizes for smart home installation services can vary widely, even when they appear to be covering the same category. In most cases, the gap comes from what is counted as installation revenue, which customer types are included, and which year is treated as the starting point for the forecast.

The table makes the spread visible, and then the reasons are easier to pinpoint, such as whether DIY-related support services are mixed into the total, whether monitoring and software fees are blended with installation, and how service ticket values are escalated over time. Currency timing and inflation treatment also matter here because labor is a large share of the bill, and some publications apply a flat uplift without checking local wage moves.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 12.73 B (2026) | |

| Trade Journal A | USD 4.68 B (2023) | Uses an earlier base year and may bundle a broader smart home service scope, which can mix installation with adjacent software and monitoring line items, making year-to-year comparisons uneven. |

| Global Consultancy B | USD 4.83 B (2025) | Lower current value likely reflects a narrower definition of paid installation jobs and a different split between professional-installed and DIY, with less clarity on how service ticket prices are carried forward by region. |

The table shows that the biggest differences sit in the current-year starting point and what is allowed inside the service revenue bucket. In Mordor Intelligence's model, the value is built around installation and integration work while keeping device sales and stand-alone monitoring fees outside the total. When scope and pricing mechanics are made explicit, the market size becomes easier to trace back to housing activity, adoption, and service ticket assumptions that can be checked and repeated.

Key Questions Answered in the Report

How big is the smart home installation service market in 2026?

The market generated USD 12.73 billion in 2026 and is forecast to climb to USD 37.96 billion by 2031.

What is the expected CAGR for smart home installation services?

A 24.43% CAGR is projected for 2026-2031, reflecting rising broadband, tax incentives, and insurer discounts.

Which system segment leads current revenue?

Home monitoring and security captured 45.86% of 2025 revenue, supported by AI-enabled intrusion detection.

Which region is growing fastest for professional installations?

Asia Pacific is set to expand at a 25.12% CAGR through 2031 thanks to smart-city mandates and rapid fiber rollouts.

Why are Thread-based devices important for installers?

Thread offers low-power mesh networking and Matter interoperability, cutting installation time and future-proofing deployments.

What challenges limit market growth?

A shortage of certified technicians and heightened data privacy regulations add cost and delay project timelines.

Page last updated on: