Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 103.78 Billion |

| Market Size (2026) | USD 105.87 Billion |

| Market Size (2031) | USD 116.95 Billion |

| Growth Rate (2026 - 2031) | 2.01% CAGR |

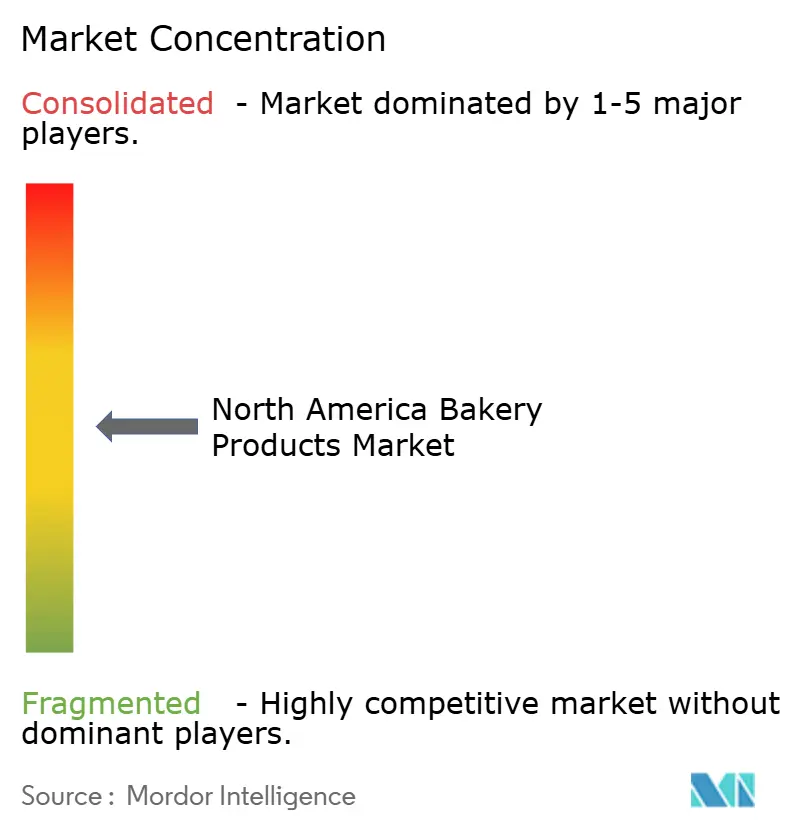

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

North America Bakery Products Market Analysis by Mordor Intelligence

The North America bakery products market size is expected to grow from USD 103.78 billion in 2025 to USD 105.87 billion in 2026 and is forecast to reach USD 116.95 billion by 2031 at 2.01% CAGR over 2026-2031. The adoption of premiumization strategies drives this growth, the consistent demand for staple foods, and manufacturers’ efforts to develop healthier product formulations. Manufacturers are focusing on frozen bakery products and organic options, which help extend shelf life while catering to the rising demand for health-conscious products. Cross-border trade plays a crucial role in maintaining efficient supply chains, with Mexico emerging as a key contributor to regional growth. Wealthier consumers are willing to pay more for products with high-protein content or clean-label ingredients. These trends highlight the dynamic nature of the North America bakery products market as it adapts to evolving consumer needs and economic conditions. The competitive landscape of the North America bakery products market is moderately concentrated. Leading players such as Grupo Bimbo S.A.B. de C.V., Flowers Foods Inc., and Mondelez International Inc. are utilizing their extensive manufacturing capabilities and distribution networks to maintain their market positions.

Key Report Takeaways

- By product type, breads held 51.03% of the North American bakery products market share in 2025; cakes and pastries are expected to advance at a 3.91% CAGR through 2031.

- By form, fresh offerings dominated the North American bakery products market share in 2025, whereas frozen products are forecast to grow at a 4.44% CAGR through 2031.

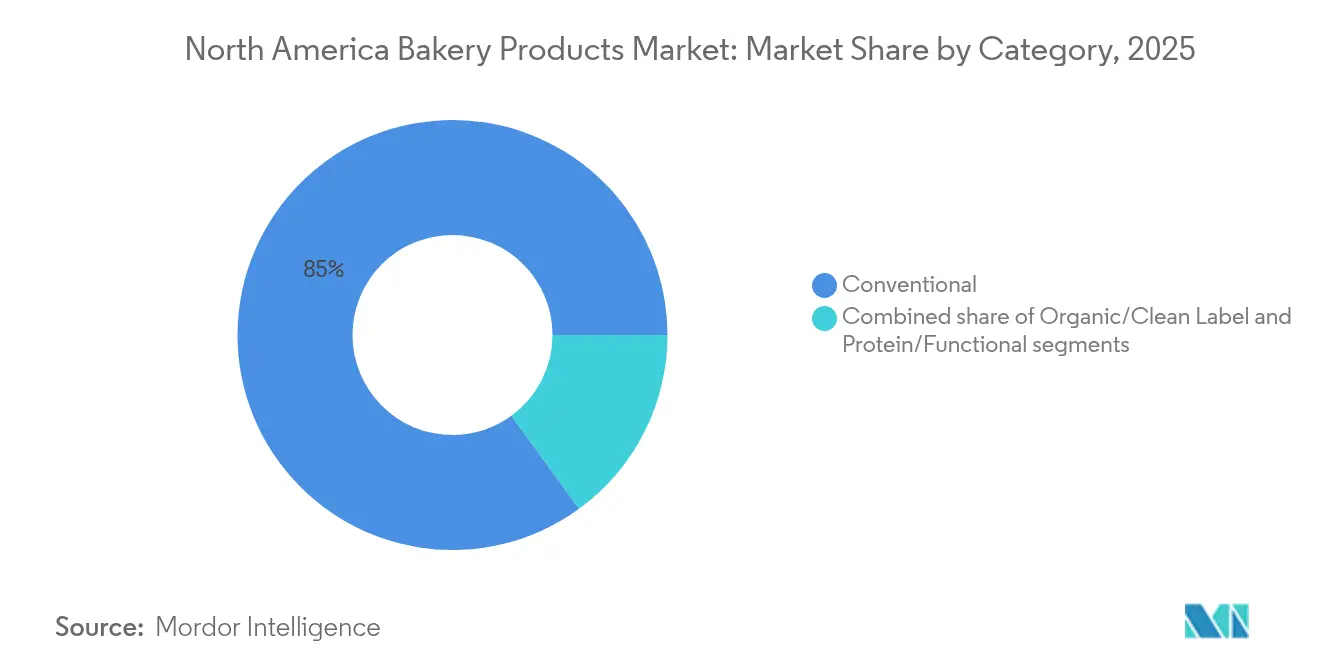

- By category, conventional lines accounted for 85.02% of the North America bakery products market share in 2025; organic/clean-label products are set to expand at a 5.61% CAGR.

- By distribution channel, supermarkets/hypermarkets captured 53.02% share of the North America bakery products market in 2025; online retail is rising at a 4.93% CAGR.

- By geography, the United States led the North American bakery products market with 47.88% of the market share in 2025, while Mexico is projected to achieve a 5.90% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Bakery Products Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Convenience-driven breakfast demand | +0.4% | North America, with the strongest impact in the United States urban markets | Medium term (2-4 years) |

| Increasing demand for packaged and processed foods | +0.3% | particular strength in Canada and Mexico | Long term (≥ 4 years) |

| Product innovation and flavor diversification | +0.5% | North America, led by the United States innovation centers | Short term (≤ 2 years) |

| Surging seasonal and festive demand | +0.2% | North America, with regional variations by cultural preferences | Short term (≤ 2 years) |

| Rising preference for multigrain and high-fiber bakery products | +0.3% | North America, concentrated in health-conscious demographics | Medium term (2-4 years) |

| Snackification trend among millennials and youth | +0.4% | North America, strongest in the United States and urban Canadian markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Convenience-driven breakfast demand

Demand for convenient breakfast options is changing the North American bakery market. Busy urban lifestyles and more commuter traffic mean less time for home-cooked meals, leading consumers to choose portable options like pastries, breads, and doughnuts. As of 2025, World Population Review lists biscuits and doughnuts as some of the most popular breakfast items in the United States, showing the strong role of baked goods in morning routines[1]Source: World Population Review, "Breakfast by Country 2025", worldpopulationreview.com. Reflecting this trend, in February 2025, NuStef Baking, the maker of reko pizzelles, introduced TeaFusions waffle cookies, a tea-infused snack designed for consumers looking for convenience and a treat. The rising demand for grab-and-go options in convenience stores, cafes, and workplace cafeterias highlights the need for quick and portable breakfast choices.

Increasing demand for packaged and processed foods

Packaged bakery products are becoming more popular as consumers move away from fresh bakery counters to pre-packaged options that are easier to store, carry, and use. Large-scale producers benefit from lower costs, less waste, and better distribution, ensuring these products are widely available in stores. In 2024, the United States leads in consuming ultra-processed foods (UPFs), which make up about 60% of daily calorie intake, as per MedRxiv, showing how packaged and processed foods are a big part of everyday diets[2]Source: MedRXIV Org, "Ultra-processed food staples dominate mainstream United States supermarkets", medrxiv.org. Younger consumers, especially Gen Z and millennials, are driving this trend by choosing packaged bakery snacks, resealable packs, and long-lasting breads that fit their busy lifestyles and need for quick, affordable options. The increased availability of these products in supermarkets and convenience stores further supports their growing popularity among younger households.

Snackification trend among millennials and youth

The North American bakery products market is experiencing steady growth as more people shift from traditional meals to smaller, convenient snacks. According to the 2024 International Food Information Council (IFIC) Survey, 56% of consumers now replace full meals with snacks, with this trend being particularly common among Gen Z, millennials, women, and single individuals[3]Source: International Food Information Council, "2024 IFIC Food and Health Survey", ific.org. Busier lifestyles and the need for quick, easy-to-consume options drive this change in eating habits. As a result, bakery manufacturers are focusing on creating ready-to-eat, portion-controlled, and flavorful products that cater to on-the-go consumption. These products not only save time but also offer variety and convenience, making them appealing to a wide range of consumers. This growing preference for convenience-driven eating is reshaping the market, boosting demand, and creating opportunities for innovation in bakery product offerings across the region.

Product innovation and flavor diversification

Flavor innovation plays a crucial role in driving growth in the North American bakery market, helping brands stand out and avoid becoming too generic. For example, in December 2024, Entenmann's introduced big chunk soft-baked cookies in flavors like chocolate, mint chocolate, and salted caramel chocolate. These cookies combine indulgent flavors with the convenience of individually wrapped portions, making them appealing for on-the-go consumers. Similarly, in October 2024, Banquet d'Or launched a pistachio-filled croissant, featuring layers of buttery pastry filled with a rich pistachio center. This product caters to consumers looking for a mix of indulgence and sophistication. These examples show how brands are using shorter research and development cycles to quickly create and launch products that align with current trends. As a result, retailers are also focusing on stocking items that offer unique flavors and drive strong sales.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Short shelf life of fresh bakery products | -0.3% | North America, particularly affecting local and regional producers | Long term (≥ 4 years) |

| Consumer shift toward healthier alternatives | -0.4% | North America, strongest in urban and affluent markets | Medium term (2-4 years) |

| Volatility in raw material prices | -0.5% | regional variations based on agricultural conditions | Short term (≤ 2 years) |

| Regulatory pressure on additives and labeling | -0.2% | North America, with increasing compliance costs and complexity | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Consumer shift toward healthier alternatives

Health-conscious consumers are increasingly moving away from traditional sugary pastries and opting for healthier alternatives like high-protein bars, fruit snacks, and gluten-free breads. According to the American Heart Association, as of 2024, 68% of Americans recognized the importance of healthy eating for long-term well-being[4]Source: American Heart Association, "Alarming trends call for action to define the future role of food in nation’s health", heart.org. The 2024 International Food Information Council (IFIC) Survey reveals that 66% of consumers were actively trying to reduce their sugar intake, a noticeable increase from 61% in previous years. To meet this growing demand, bakery manufacturers are reformulating their products by reducing sugar content and adding more fiber. They are also incorporating ingredients like whole grains, plant-based proteins, and functional additives to create healthier options. However, these changes require significant research and development efforts, as altering recipes can impact taste and consumer satisfaction. Brands that successfully balance health benefits with indulgent flavors are more likely to retain customer loyalty.

Regulatory pressure on additives and labeling

The North American bakery market is under growing regulatory pressure, especially regarding additives, preservatives, and product labeling. Started in April 2025, the Food and Drug Administration's updated “healthy” labeling criteria will push manufacturers to reformulate their products to meet new standards[5]Source: Food and Drug Administration, "FDA Finalizes Updated 'Healthy' Nutrient Content Claim", fda.gov. Moreover, on January 14, 2025, the Food and Drug Administration proposed a front-of-package (FOP) nutrition label. This label aims to provide consumers with quick and clear information about key nutrients like saturated fat, sodium, and added sugars, which are linked to chronic health issues when consumed excessively. The goal is to make it easier for consumers to identify healthier food options at a glance, complementing the existing nutrition facts label. While these regulations are designed to promote healthier eating habits, they also pose challenges for manufacturers. Reformulating products to comply with these rules can increase research and development costs and may impact the taste and texture of familiar bakery items.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Bread Dominance Faces Premium Shift

Breads remain the most popular category in the North American bakery market, holding 51.03% of the market share in 2025. Their popularity comes from their versatility, convenience, and role in everyday meals like breakfast, sandwiches, and snacks. Consumers are increasingly choosing whole-grain, high-fiber, and protein-enriched options, reflecting a growing focus on health and wellness. Retailers dedicate significant shelf space to breads, making them easily accessible and frequently purchased. This steady demand highlights the category’s strength, even as consumers explore new bakery products and trends.

Although breads lead in volume, cakes and pastries are expected to grow faster, with a projected 3.91% CAGR from 2026 to 2031. This growth is driven by consumer interest in unique flavors, indulgent treats, and their role in celebrations. Innovations like fusion pastries and single-serve options are particularly appealing to millennials, Gen Z, and urban households. Premium and seasonal offerings also encourage repeat purchases and support higher price points. As consumers balance indulgence with health concerns, manufacturers are introducing cleaner, functional, or portion-controlled options to maintain interest and drive market growth.

By Form: Fresh Maintains Lead Despite Frozen Growth

Fresh bakery products held a major share in the North American market in 2025, accounting for 72.45% of the total market share. Their fresh aroma, taste drive their popularity, and the overall experience of buying directly from in-store bakeries. Consumers often prefer freshly baked breads, pastries, and specialty items because they associate these products with higher quality and better flavor. Retailers enhance this appeal by offering open bakery counters and on-site baking, which creates a more engaging shopping experience. These strategies not only attract customers but also encourage impulse purchases and build long-term customer loyalty.

Frozen bakery products are expected to grow at a faster pace, with a 4.44% CAGR from 2026 to 2031, nearly double the growth rate of fresh items. Advances in freezing technology have significantly improved the quality of frozen products, helping them retain their taste, texture, and appearance. This makes frozen bakery items a convenient option for busy consumers, especially those in urban areas who may not have time for frequent shopping trips. Frozen products also offer the advantage of a longer shelf life, which appeals to households looking for practical and time-saving solutions. Manufacturers are responding to this demand by expanding their frozen product lines to include ready-to-bake breads, pastries, and desserts.

By Category: Organic Growth Accelerates Despite Conventional Dominance

Conventional bakery recipes remained dominant in North America in 2025, accounting for 85.02% of the market share. This reflects the preference of price-conscious consumers who value affordability and familiar flavors. Products like classic breads, cakes, and pastries continue to be staples for households looking for reliable and consistent quality. Retailers also depend on these high-demand items to maintain steady sales. Promotions, in-store displays, and value packs further strengthen the appeal of conventional bakery products, making them widely available across supermarkets, hypermarkets, and convenience stores.

In the coming years, organic and clean-label bakery products are expected to grow significantly, with a strong 5.61% CAGR projected between 2026 and 2031. This growth is driven by increasing consumer interest in healthier options, transparency in ingredients, and minimally processed foods. More households are seeking products made with non-genetically modified organism ingredients, organic flours, natural sweeteners, and recipes free from artificial preservatives. Manufacturers are responding to this demand by developing innovative products that maintain great taste and texture while meeting these health-focused criteria. This trend offers brands an opportunity to attract health-conscious and environmentally aware consumers.

By Distribution Channel: Online Gains Despite Supermarket Strength

Supermarkets/hypermarkets continued to dominate the North American bakery market in 2025, holding 53.02% of the total market share. These retail channels are popular because they cater to a wide variety of consumer needs, offering everything from affordable value packs to premium bakery items. Shoppers often visit these stores for their weekly groceries, making them a convenient choice for purchasing bakery products. In-store bakery sections, which provide freshly baked goods, attract customers with their aroma and visual appeal, encouraging impulse purchases. Promotions, discounts, and loyalty programs further strengthen the role of supermarkets and hypermarkets as the go-to option for bakery products.

On the other hand, online retail is growing rapidly and is expected to achieve a 4.93% CAGR by 2031. The convenience of ordering bakery products online, combined with doorstep delivery, is appealing to busy consumers, especially those in urban areas. E-commerce platforms also offer unique advantages, such as access to specialty or niche bakery items that may not be available in physical stores. Features like subscription services, personalized recommendations, and exclusive online discounts are helping online channels attract more customers. As a result, online retail is becoming an increasingly important part of the bakery market, particularly for tech-savvy and time-conscious shoppers.

Geography Analysis

The United States accounted for 47.88% of the bakery market revenue in 2025, driven by its large-scale production capabilities, innovation hubs, and diverse consumer base. United States bakery exports reached USD 4.31 billion in 2023, as per the International Trade Centre, with Canada and Mexico being the primary importers, highlighting strong regional trade ties. Investments in manufacturing, such as Nature's Bakery's USD 240 million smart baking production facility in Utah in July 2025, reflect the industry's commitment to growth and modernization. The adoption of ethnic flavors and the increasing presence of private-label bread in discount stores indicate evolving consumer preferences and heightened competition in the market.

Mexico is experiencing rapid growth in its bakery market, with a projected CAGR of 5.90%, fueled by urbanization, population growth, and the cultural importance of baked goods. The bakery and tortilla segments contribute the majority of the value of Mexico's food processing sector, showcasing their significant role in the economy. Cross-border ingredient sourcing strengthens ties with United States suppliers, while domestic manufacturers are upgrading facilities to meet the rising quality expectations of the growing middle class. While traditional sweet breads remain a staple, premium packaged snacks are gaining popularity, particularly among younger, urban professionals seeking convenience and variety.

Canada's bakery market demonstrates steady growth through 2026, driven by demand for gluten-free and organic products. The alignment of Canadian food safety regulations with United States standards facilitates seamless trade, with exports accounting for major share of the country's bakery production. Government policies encouraging innovation have enabled manufacturers to experiment with new recipes and product lines. However, the market faces challenges due to its saturated retail landscape, which limits opportunities for significant volume growth. Smaller markets in the Caribbean and Central America provide additional export opportunities, offering a platform for unique flavors, though these markets operate on a smaller scale compared to North America.

Competitive Landscape

The North American bakery products market is moderately competitive, with the top five companies controlling approximately 50% of the market share. Major players like Grupo Bimbo, Flowers Foods, and Mondelez International benefit from extensive manufacturing facilities and strong distribution networks. However, the rise of private-label products is creating pressure on branded goods, leading to increased mergers and acquisitions. For instance, Flowers Foods’ acquisition of Simple Mills for USD 795 million has expanded its portfolio of health-focused products. Similarly, Mars’ ongoing USD 2 billion investment in United States manufacturing highlights the growing importance of automation in reducing costs and improving sustainability.

Technological advancements are playing a key role in helping companies maintain a competitive edge. Leading firms are adopting AI-driven demand forecasting to minimize waste and using robotic systems to enhance production efficiency. Meanwhile, smaller disruptors are entering the market with direct-to-consumer models, offering niche products like keto, paleo, and allergen-free baked goods. These innovations are pushing established players to adapt quickly. Regulatory changes, such as the Food and Drug Administration's updated labeling requirements set for 2028, are increasing the need for companies to reformulate recipes without compromising on taste or quality. Firms that can meet these demands are likely to secure premium shelf space in retail stores.

As the market evolves, companies are focusing on balancing innovation with consumer preferences. The adoption of advanced technologies and the ability to cater to health-conscious consumers are becoming critical success factors. At the same time, regulatory compliance and sustainability initiatives are shaping the strategies of market leaders. While established players continue to dominate, emerging brands are carving out a niche by addressing specific dietary needs and leveraging online sales channels. This dynamic environment is expected to drive further competition and innovation in the North American bakery products market over the coming years.

North America Bakery Products Industry Leaders

-

Flowers Foods, Inc.

-

Mondelēz International, Inc

-

Grupo Bimbo, S.A.B. de C.V.

-

Campbell Soup Company

-

The J.M. Smucker Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Flowers Foods announced its agreement to acquire Simple Mills in a deal valued at USD 795 million. This acquisition was aimed at strengthening Flowers Foods' portfolio by integrating Simple Mills' innovative and health-focused product offerings.

- September 2024: Rise Baking Co. acquired by Platinum Equity and Butterfly Equity. This acquisition was aimed at strengthening the company's market position and expanding its operational capabilities.

- May 2024: Bimbo Bakeries USA, a subsidiary of Grupo Bimbo SAB de CV, added Hawaiian bakery bread and buns to its Sara Lee Artesano portfolio. The two new bread products are made without any artificial flavors, preservatives, or high-fructose corn syrup.

- February 2024: New Jersey’s Bread manufacturer, Anthony & Sons Bakery Inc., launched the Avocado Bread Company brand, making it the first bakery to utilize avocados in the line of plant-based innovations.

North America Bakery Products Market Report Scope

Bakery products are everyday staples consisting of bread, cakes, cookies, rolls, and pastries. They are usually prepared from flour or meal derived from some form of grain and provide nutrients in the human diet.

The North American bakery products market is segmented by product type, distribution channel, and geography. By product type, the market is segmented into cakes and pastries, biscuits, bread, morning goods, and others. By distribution channel, the market is segmented into hypermarkets/supermarkets, convenience stores, specialty stores, online retailers, and other distribution channels. The report also analyzes the bakery market in emerging and established markets across North America, including the United States, Canada, Mexico, and the Rest of North America. The market sizing has been done based on value terms (USD) for all the above-mentioned segments.

By Product Type

| Breads |

| Cakes and Pastries |

| Biscuits and Cookies |

| Morning Goods |

| Other Product Types |

By Form

| Fresh |

| Frozen |

By Category

| Conventional |

| Organic/Clean Label |

| Protein/Functional |

By Distribution Channel

| Supermarkets/Hypermarkets |

| Convenience Stores |

| Specialty/Bakery Stores |

| Online Retail Stores |

| Other Distribution Channels |

By Geography

| United States |

| Canada |

| Mexico |

| Rest of North America |

| By Product Type | Breads |

| Cakes and Pastries | |

| Biscuits and Cookies | |

| Morning Goods | |

| Other Product Types | |

| By Form | Fresh |

| Frozen | |

| By Category | Conventional |

| Organic/Clean Label | |

| Protein/Functional | |

| By Distribution Channel | Supermarkets/Hypermarkets |

| Convenience Stores | |

| Specialty/Bakery Stores | |

| Online Retail Stores | |

| Other Distribution Channels | |

| By Geography | United States |

| Canada | |

| Mexico | |

| Rest of North America |

Key Questions Answered in the Report

What is the current value of the North America bakery products market?

The market stands at USD 105.87 billion in 2026 and is projected to reach USD 116.95 billion by 2031.

Which product segment is expanding fastest?

Cakes and pastries are growing at a 3.91% CAGR through 2031, outpacing other categories.

Why are frozen bakery goods gaining popularity?

Frozen items offer longer shelf life, reduced retail waste, and quality parity with fresh goods, driving a 4.44% CAGR.

Which country is the growth engine within the region?

Mexico leads with a 5.90% CAGR through 2031 due to urbanization, rising incomes, and strong cultural affinity for baked goods.

Page last updated on: