Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 156.31 Billion |

| Market Size (2031) | USD 317.26 Billion |

| Growth Rate (2026 - 2031) | 15.21% CAGR |

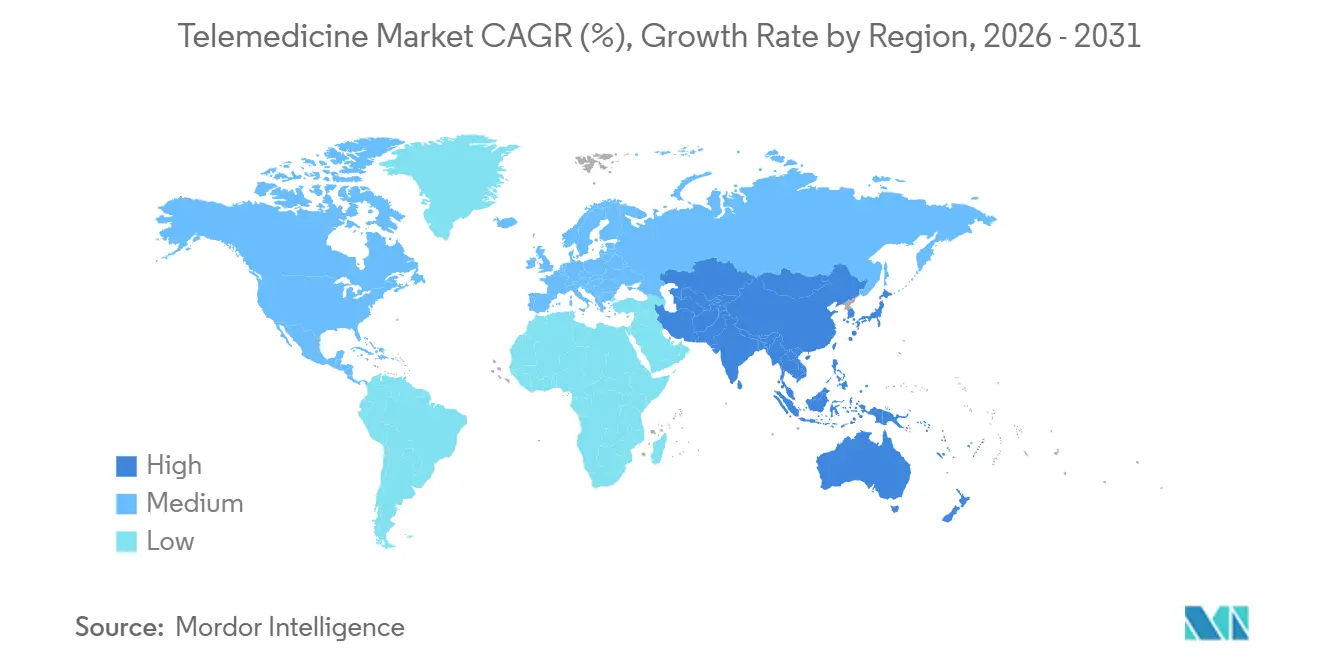

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Telemedicine Market Analysis by Mordor Intelligence

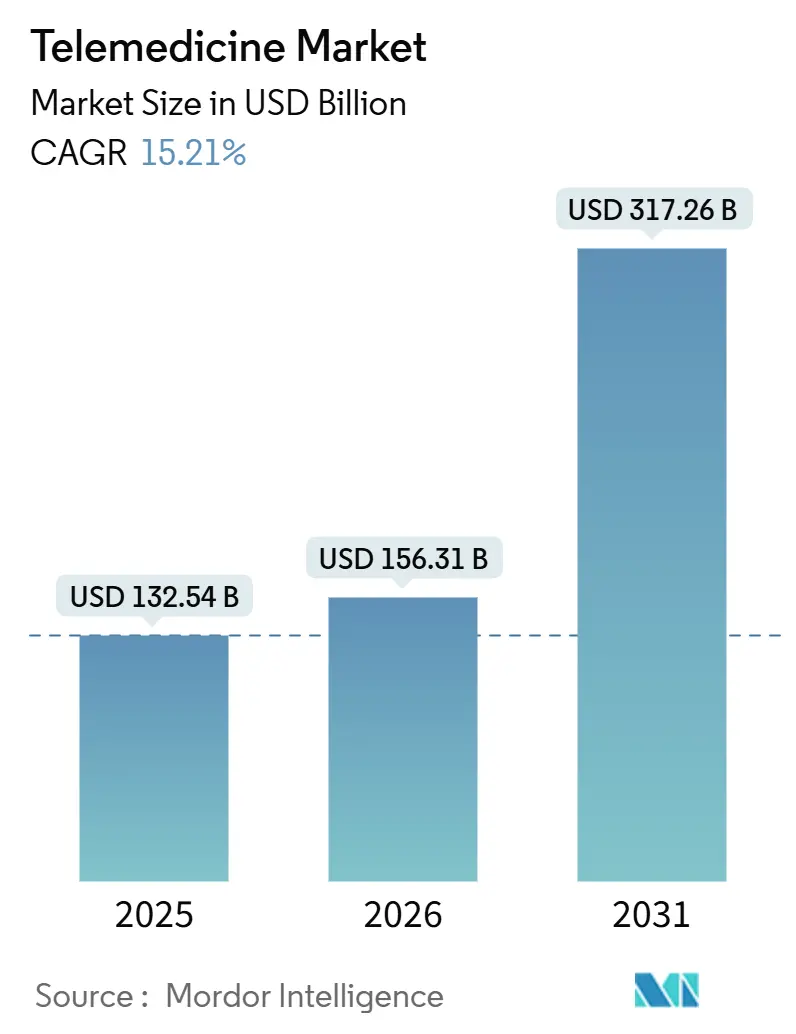

The Telemedicine Market size is projected to be USD 132.54 billion in 2025, USD 156.31 billion in 2026, and reach USD 317.26 billion by 2031, growing at a CAGR of 15.21% from 2026 to 2031.

Sustained reimbursement parity across 43 U.S. states, expanding employer-sponsored virtual primary care contracts, and the broader adoption of 5G networks are anchoring structural growth that transcends the pandemic's uplift. Chronic-disease prevalence among people aged 65 years and older, combined with projected global aging, is reinforcing demand for remote monitoring and specialist access. At the same time, service providers are capturing durable subscription revenue by bundling virtual care into employee benefits and payer programs. Interoperability shortfalls between electronic health records (EHRs) and telehealth modules, coupled with cross-border licensure frictions, continue to constrain capacity utilization. However, the integration of AI-enabled decision support is steadily increasing physician acceptance.

Key Report Takeaways

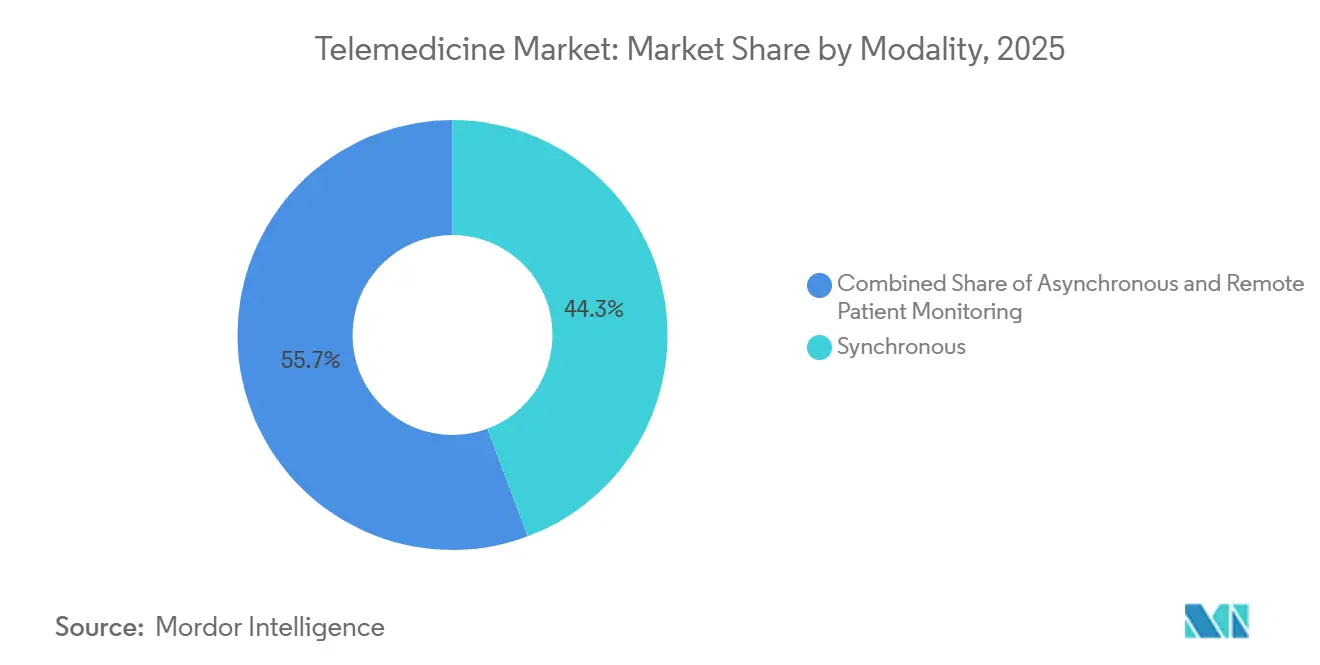

- By modality, synchronous video visits accounted for 44.28% of the telemedicine market in 2025, while remote patient monitoring is projected to expand at a 17.09% CAGR through 2031.

- By component, services and support accounted for 56.73% of the telemedicine market share in 2025; among specialty services, telepsychiatry is tracking the fastest growth at an 18.21% CAGR to 2031.

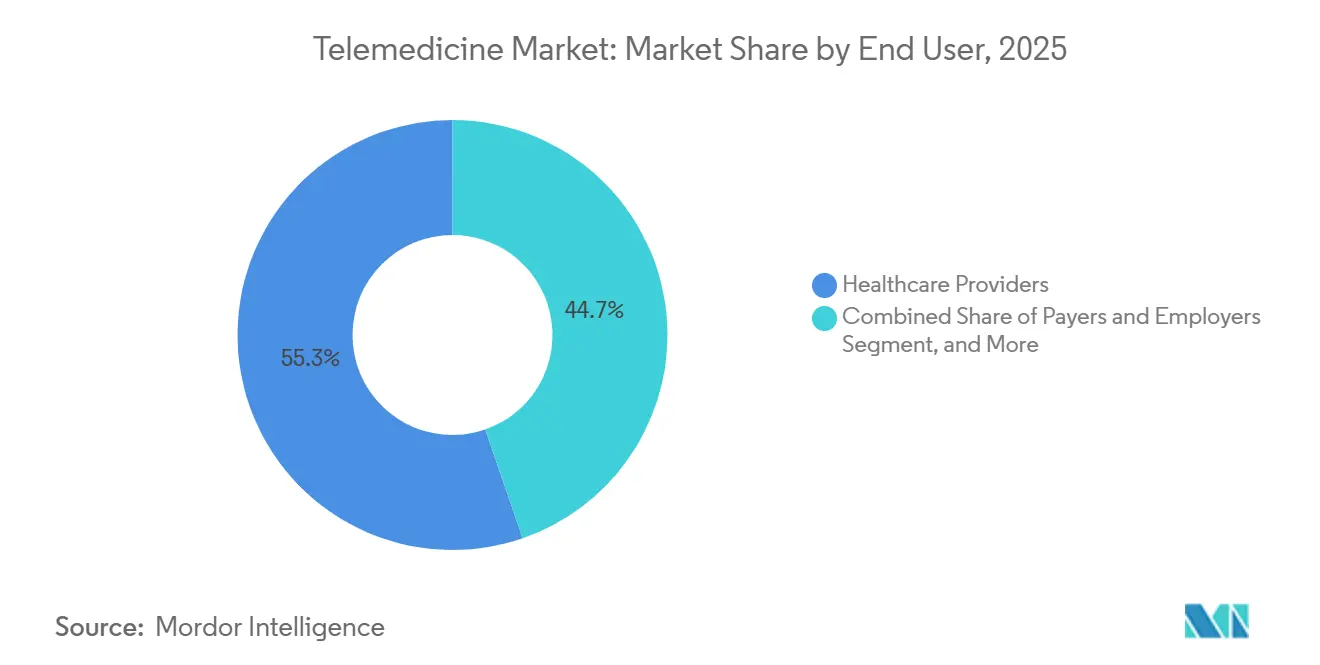

- By end user, healthcare providers accounted for 55.28% of spending in 2025, whereas the patient and home-user segment is projected to grow at a 14.94% CAGR through 2031.

- By geography, North America led with a 38.06% revenue share in 2025; the Asia-Pacific region is projected to log the highest regional CAGR of 19.59% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Telemedicine Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising chronic-disease burden and aging population | +2.8% | North America, Europe, East Asia | Long term (≥ 4 years) |

| Reimbursement parity laws across OECD and BRICS | +3.2% | United States, Canada, Brazil, India, Europe | Medium term (2-4 years) |

| 5G and edge-computing roll-outs | +2.1% | Urban hubs in U.S., China, South Korea, Gulf states | Short term (≤ 2 years) |

| Employer-backed virtual primary-care plans | +2.5% | United States, Western Europe | Medium term (2-4 years) |

| Pandemic-induced consumer preference | +1.9% | High-income OECD markets | Short term (≤ 2 years) |

| AI-driven clinical decision support | +2.6% | United States, Europe, China, India | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging Chronic-Disease Burden And Aging Population

Estimates from the World Health Organization show that the global population aged 65 and older will surpass 1.5 billion by 2050, with more than 60% living with at least one chronic condition.[1]World Health Organization, “Ageing and Health,” who.int Telehealth lowers mobility-related barriers for seniors by enabling remote follow-ups and continuous monitoring of vitals, resulting in earlier interventions that reduce hospital readmissions by 22% among Medicare Advantage enrollees in the United States. Payers favor these outcomes because chronic-disease care accounts for approximately 75% of health expenditures in high-income countries. The alignment of demographic pressure and value-based funding embeds telemedicine market solutions into baseline care workflows. Because these structural forces evolve over decades, demand remains resilient regardless of economic cycles.

Payer Reimbursement Parity Laws Expanding In OECD And BRICS Regions

By the end of 2025, 43 U.S. states mandated private-payer parity for virtual visits, and 24 states extended equivalent payments to Medicaid beneficiaries.[2]American Telemedicine Association, “Parity Tracker 2025,” americantelemed.org Similar frameworks were introduced in France, Germany, India, and Brazil, effectively removing the financial barrier that had previously limited adoption to affluent patients. With tariffs aligned to in-person care, provider groups are confident about revenue continuity, while patients in price-sensitive segments enjoy lower out-of-pocket costs. This regulatory shift normalizes telehealth as a covered benefit, underpinning predictable utilization patterns across multiple insurance cohorts.

5G And Edge-Computing Roll-Outs Enabling Low-Latency Video Consultations

Fifth-generation networks are expected to be live in 120 countries by late 2025, delivering sub-20 millisecond latency that makes high-resolution video and even remote robotic surgery technically viable.[3]International Telecommunication Union, “Measuring Digital Development Facts and Figures 2025,” itu.int Edge-computing nodes placed near the network perimeter process visual data locally, trimming bandwidth needs by 40% according to benchmarks released by Cisco Systems in 2025. China has installed 2,500 5G telemedicine stations in rural townships, facilitating 15 million specialist sessions and reducing the average travel distance by 180 kilometers per visit. These infrastructure upgrades erase the technical constraints that previously confined telemedicine market adoption to low-bandwidth use cases.

Employer-Sponsored Virtual Primary-Care Plans Scaling Rapidly

Kaiser Family Foundation surveys published in 2026 indicate that 30% of mid-sized U.S. firms and 45% of enterprises with 1,000 or more employees now embed virtual primary-care services in their benefit designs. Per-member-per-month contracts averaging USD 50–150 convert episodic encounters into predictable revenue for platform vendors. Large employers, such as Walmart, expanded these programs to include dependent coverage, enrolling over 2 million lives. The employer channel, therefore, provides the telemedicine market with a forward-booked revenue stream insulated from the volatility of fee-for-service reimbursement.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-privacy and licensure fragmentation | -1.8% | European Union, United States, ASEAN | Long term (≥ 4 years) |

| Proposed Medicare reimbursement cuts | -1.3% | United States | Short term (≤ 2 years) |

| Digital divide in low-income rural markets | -1.5% | Sub-Saharan Africa, South Asia, rural Latin America | Long term (≥ 4 years) |

| Clinician platform fatigue from EHR gaps | -1.1% | United States, Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Data-Privacy And Cross-Border Licensure Regulations Remain Fragmented

The European Union’s GDPR restricts cross-border data flows, and enforcement actions between 2024-2025 levied EUR 120 million in penalties on operators that stored patient records outside the bloc. In the United States, only 40 states had joined the Interstate Medical Licensure Compact by late 2025, leaving physicians to secure multiple licenses at fees surpassing USD 1,000 per jurisdiction. India’s pending Digital Personal Data Protection Act requires domestic data residency, which increases infrastructure costs for multinational platforms. These inconsistencies elevate compliance overhead and compress the telemedicine market’s cross-regional scalability.

Physician Reimbursement Cuts In Medicare Draft Rules

The Centers for Medicare & Medicaid Services proposed a 2.8% reduction in the 2027 physician fee schedule, potentially endangering margins for small practices that have shifted significant visit volumes online. Because Medicare funds one-fifth of U.S. healthcare, even marginal rate decreases introduce revenue volatility that complicates capital planning for virtual-first providers. Legislative intervention is possible, but the annual uncertainty still dampens infrastructure investment within the telemedicine market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Modality: Remote Monitoring Surges Ahead

Remote patient monitoring captured accelerating interest, notching a 17.09% CAGR forecast through 2031 as the U.S. FDA cleared successive waves of connected glucose, cardiac, and blood-pressure sensors that stream continuous data to cloud analytics engines. Synchronous video maintained the largest 2025 revenue share at 44.28%, particularly suited for primary-care, urgent-care, and behavioral-health sessions that require real-time interaction. Asynchronous workflows, including store-and-forward imaging and secure messaging, accounted for approximately 25% of spending. Medicare Advantage enrolled 32 million members in RPM programs by the end of 2025, reducing 30-day readmissions by 22% and confirming payer appetite for continuous-care models.

Synchronous utilization is stabilizing at one-quarter of outpatient encounters, down from pandemic highs, yet remains far above pre-COVID levels. Asynchronous modalities benefit from lower bandwidth demands and flexible scheduling, although payment rates tend to lag behind those for live visits. The incorporation of AI triage that prioritizes dermatology images or flags cardiac anomalies is expected to lift asynchronous adoption in bandwidth-constrained regions. Overall, RPM’s always-on data model positions it to redefine chronic-care economics, securing the largest incremental share of telemedicine market revenue over the next decade.

By Component: Telepsychiatry Leads Service Expansion

Services and support generated 56.73% of 2025 revenue, underpinned by telestroke, telecardiology, teleradiology, telepsychiatry, and other specialty lines. The telepsychiatry subsegment is advancing at an 18.21% CAGR through 2031, driven by mental-health parity rules in the United States and the European Union that require equal reimbursement for behavioral health sessions. Software platforms absorbed roughly 30% of spending, while hardware peripherals captured just 14% amid intensifying commoditization pressures.

Telestroke networks reduce door-to-needle times by 18 minutes, according to American Heart Association audits, making them life-saving investments for rural hospitals. Telecardiology and teleradiology supply consultative expertise where on-site specialists are scarce, locking in predictable per-study fees. Peripheral makers face margin compression as smartphone-compatible otoscopes and stethoscopes enter the market at or below USD 100, driving a shift toward integrated software ecosystems that bundle scheduling, documentation, billing, and patient engagement. As a result, vendor differentiation is tilting toward workflow orchestration rather than hardware innovation within the telemedicine market.

By End User: Patients Accelerate Direct-to-Consumer Uptake

Healthcare providers retained the largest share in 2025 at 55.28%, but the patient and home-user segment is forecast to expand at a 14.94% CAGR through 2031, driven by subscription models priced between USD 10 and USD 50 per month. Payers and employers, responsible for roughly one-quarter of the spend, channel members first to virtual visits to curb emergency department utilization. Government entities, although accounting for only 6% of current revenue, fund large public-health deployments, such as India’s eSanjeevani program, which surpassed 300 million consultations by mid-2025.

Provider margins are tightening because platform licensing, broadband, and IT support remain fixed while reimbursement converges with in-person rates, pushing small practices below 5% operating margins. Payers see expense relief: virtual urgent-care visits cost 40–60% less than outpatient emergency encounters, according to recent CMS actuarial filings. The patient segment’s rapid rise signals a consumerization trend that could disintermediate traditional referral networks, forcing incumbents to revamp digital front doors to safeguard downstream procedural revenue.

Geography Analysis

North America contributed 38.06% of global revenue in 2025, driven by well-established reimbursement policies, high broadband penetration, and robust employer adoption. The Asia-Pacific region, however, is projected to deliver the fastest regional CAGR of 19.59% through 2031, driven by government-backed digital health initiatives. India’s eSanjeevani recorded its 300 millionth consultation by mid-2025, while China’s AI-enhanced provincial platforms cover more than 400 million rural residents.

In Europe, France reimburses 100% of chronic-care video follow-ups, Germany’s DiGA program prescribes reimbursable health apps, and the United Kingdom has embedded virtual consults across National Health Service primary-care pathways. Despite structural regulatory support, fragmented EHR infrastructures and language diversity temper pan-European scalability, slowing the uptake compared with the Asia-Pacific region.

Gulf states are installing 5G kiosks in malls and public offices, whereas South Africa’s private payers only recently began funding telepsychiatry. Latin America accounted for approximately 4% of global revenue, with Brazil expanding virtual mental health coverage and Argentina running rural remote monitoring pilots. Regional growth trajectories correlate strongly with broadband availability and government willingness to reimburse, confirming the telemedicine market’s dependence on synchronized policy and infrastructure advances.

Competitive Landscape

The telemedicine market remains moderately fragmented, with the top five vendors collectively controlling a significant portion of the market revenue, indicating ample opportunities for specialty entrants. Teladoc Health and Amwell continue to execute horizontal integration strategies, bundling primary care, mental health, and chronic-disease management for enterprise clients. Teladoc’s 2025 acquisition of Catapult Health strengthens its preventive-care toolset, whereas Amwell’s partnership with Google Cloud embeds AI decision support into clinical workflows.

Interoperability is the sector’s chief pain point. Fewer than 40% of U.S. hospitals realize seamless HL7 FHIR exchange, forcing physicians to juggle multiple interfaces and heightening documentation fatigue. Vendors are countering by embedding AI scribes that auto-populate chart notes, cutting administrative time by around one-third, according to Oracle Health pilots. Edge-computing investments accelerate 4K streaming without buffer delays, a prerequisite for emerging use cases such as remote robotic surgery.

Disruptors are experimenting with blockchain credentialing to bypass licensure bottlenecks and unlock cross-border consults, while patent filings in 2024-2025 clustered around AI triage and secure data-sharing protocols. Private-equity roll-ups gained momentum during 2025, shrinking the pool of independent regional platforms and nudging the market toward higher concentration. Nonetheless, telestroke and telepsychiatry niches continue to attract new entrants that address clinician shortages in rural areas, suggesting that specialization will coexist alongside platform consolidation.

Telemedicine Industry Leaders

Teladoc Health Inc.

Koninklijke Philips N.V.

Amwell (American Well)

Cerner (Oracle Health)

MDLive (Cigna)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Teladoc Health closed its USD 65 million purchase of Catapult Health, adding at-home diagnostic testing to its virtual-care continuum.

- January 2025: Teladoc Health partnered with Amazon to place cardiometabolic programs on Amazon’s Health Benefits Connector, broadening reach among chronic-care patients.

- January 2025: Transcarent agreed to acquire Accolade for USD 621 million, combining AI-driven navigation with virtual services for employer groups.

- January 2025: Avel eCare purchased Amwell Psychiatric Care, extending its behavioral-health footprint to 46 U.S. states.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the global telemedicine market as all revenue generated when licensed clinicians deliver synchronous or asynchronous diagnosis, treatment, monitoring, or follow-up using fixed or mobile telecommunications networks, including peripheral hardware, purpose-built software, and managed telehealth services. The model values only fee-based clinical encounters and paid remote patient-monitoring contracts; it excludes free wellness apps, consumer fitness wearables, and pure electronic health-record platforms.

Scope exclusion: consumer wellness apps and stand-alone EHR systems are not counted.

Segmentation Overview

- By Modality

- Synchronous

- Asynchronous

- Remote Patient Monitoring

- By Component

- Software Platforms

- Hardware & Peripherals

- Services

- Telepathology

- Telecardiology

- Teleradiology

- Teledermatology

- Telepsychiatry

- Telestroke

- Other Services

- By End User

- Healthcare Providers

- Payers & Employers

- Patients / Home Users

- Government Agencies & NGOs

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed hospital network administrators, virtual-care platform executives, payer medical directors, and clinician user groups across North America, Europe, Asia-Pacific, and the Gulf. These conversations validated adoption rates, average reimbursement per video visit, and likely RPM kit refresh cycles, letting us fine-tune assumptions surfaced during desk work.

Desk Research

We began by mapping supply, demand, and pricing signals through authoritative sources such as the World Health Organization, the OECD Health Statistics portal, the International Telecommunication Union, and regional telehealth associations. Trade data from UN Comtrade, reimbursement schedules published by the Centers for Medicare & Medicaid Services, and peer-reviewed journals on chronic-disease prevalence gave us reliable baselines. Subscription databases that Mordor maintains, such as Dow Jones Factiva for deal flow and D&B Hoovers for company revenue splits, helped us benchmark vendor exposure across geographies. This list is illustrative; many additional open and proprietary references were consulted for cross-checks.

Market-Sizing & Forecasting

A top-down demand pool was built from national outpatient visit volumes and tele-penetration ratios, which were then stress-tested against sampled bottom-up indicators such as platform subscriber cohorts, device shipments, and weighted average service prices. Key variables include broadband household penetration, chronic-disease prevalence, specialist wait times, regulatory reimbursement milestones, and average connected-device cost; their trajectories feed a multivariate regression that produces the 2025-2030 outlook. Gaps in supplier roll-ups, especially for emerging markets, were bridged by applying regional price-volume proxies validated during expert calls.

Data Validation & Update Cycle

Outputs pass three layers of analyst review, variance thresholds trigger re-contact with sources, and models refresh annually; interim updates occur when policy or funding shocks materially shift any driver. Clients therefore receive the most current, reconciled view before every delivery.

Why Mordor's Telemedicine Baseline Stands Up to Scrutiny

Published estimates often diverge because firms select dissimilar service scopes, pricing ladders, or update cadences.

Our disciplined scoping and yearly refresh narrow these gaps.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 196.37 B (2025) | Mordor Intelligence | - |

| USD 104.64 B (2024) | Global Consultancy A | counts hardware sales only; excludes RPM services |

| USD 141.19 B (2024) | Industry Journal B | uses pre-pandemic utilization rates and static ASPs |

| USD 135.71 B (2024) | Regional Consultancy C | omits mHealth subscriptions outside hospitals |

Comparison based on publicly stated scopes and methods. The table shows that narrower service definitions and older utilization assumptions drive lower values at other publishers (mordorintelligence.com). By tying forecasts to verified visit volumes, refreshed reimbursement rules, and live price checks, Mordor Intelligence provides a balanced, transparent baseline that decision-makers can replicate.

Key Questions Answered in the Report

What is the current value of the telemedicine market?

The telemedicine market size reached USD 156.31 billion in 2026 and is projected to double to USD 317.26 billion by 2031.

How fast is remote patient monitoring growing?

Remote patient monitoring is forecast to expand at a 17.09% CAGR through 2031, the fastest among all telehealth modalities.

Which region will post the highest growth in virtual care adoption?

The Asia-Pacific region is expected to register a 19.59% CAGR from 2026 to 2031, driven by the growth of large-scale public platforms in India and China.

Why is telepsychiatry attracting investor interest?

Mental-health parity laws now mandate equal reimbursement for virtual sessions, driving telepsychiatry’s 18.21% CAGR forecast to 2031.

What are the biggest challenges limiting cross-border telemedicine?

Fragmented licensure rules and data-residency mandates raise compliance costs and restrict physician availability across jurisdictions.

Page last updated on: