Air Quality Monitoring Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

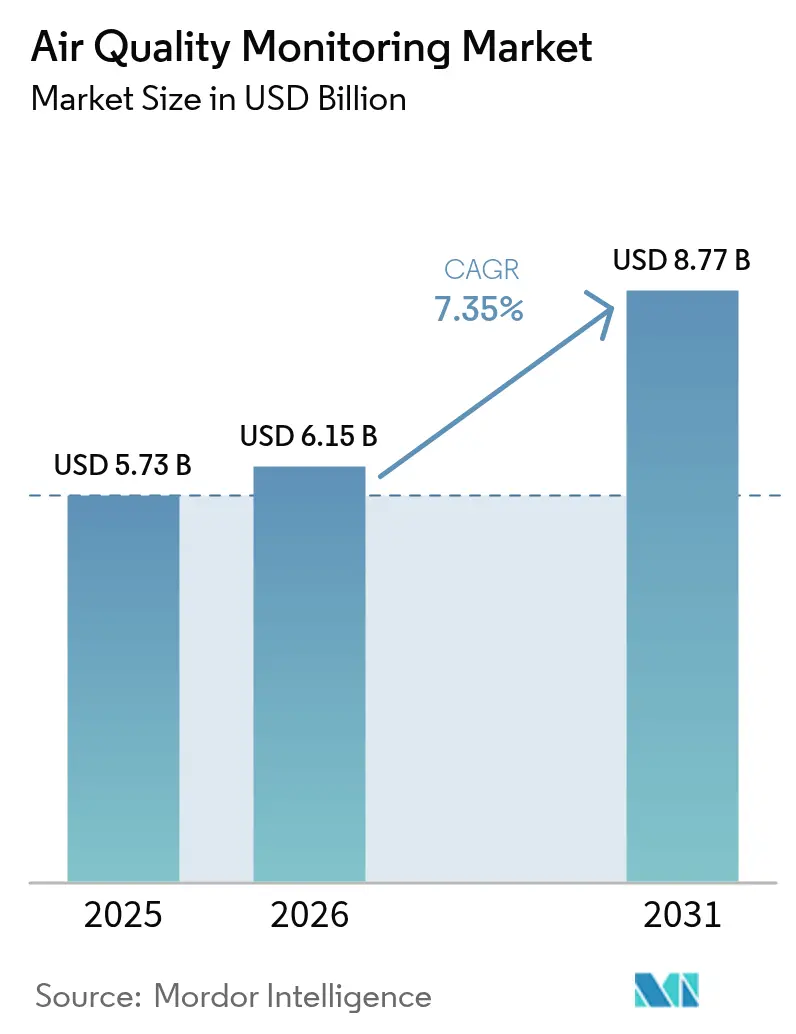

| Market Size (2026) | USD 6.15 Billion |

| Market Size (2031) | USD 8.77 Billion |

| Growth Rate (2026 - 2031) | 7.35% CAGR |

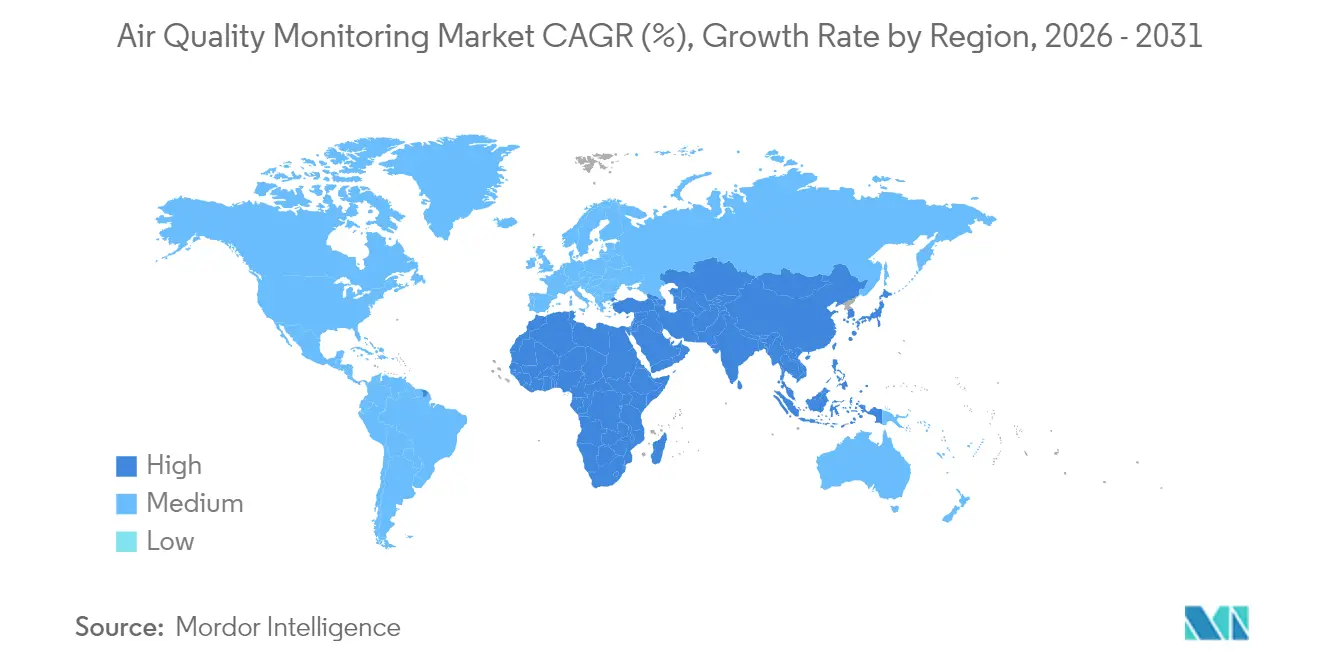

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

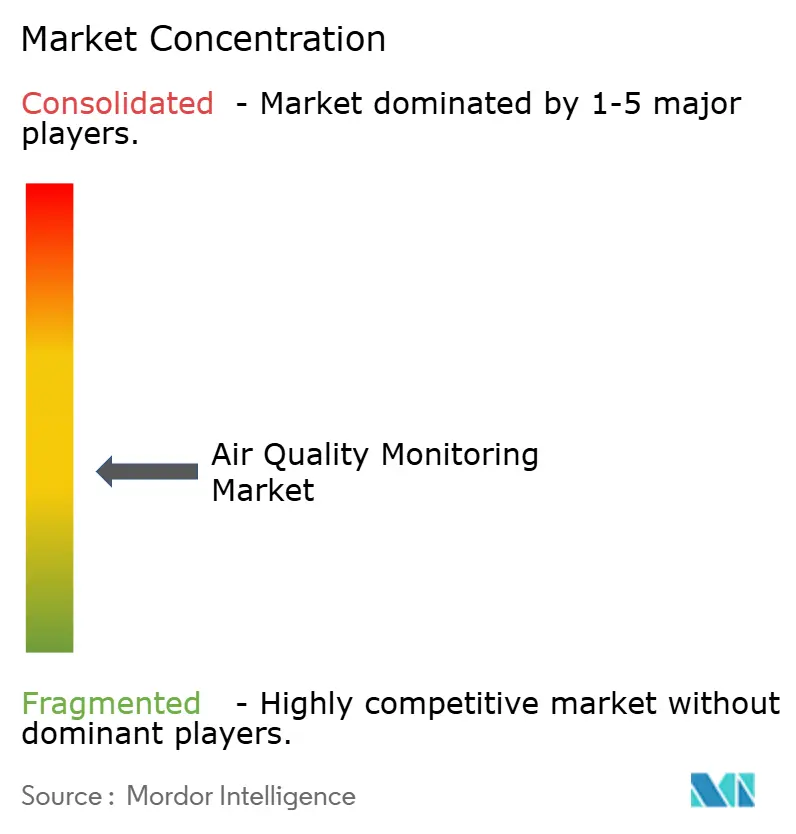

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Air Quality Monitoring Market Analysis by Mordor Intelligence

The Air Quality Monitoring Market size was valued at USD 5.73 billion in 2025 and estimated to grow from USD 6.15 billion in 2026 to reach USD 8.77 billion by 2031, at a CAGR of 7.35% during the forecast period (2026-2031).

Tightened regulatory standards, rising corporate sustainability disclosures, and continuous technological innovation in sensors, IoT, and analytics are converging to lift demand for end-to-end ambient and indoor monitoring solutions. Implementation momentum is strongest where regulations now mandate daily or real-time reporting—such as the United States’ strengthened PM2.5 rule and the EU’s Corporate Sustainability Reporting Directive—while smart-city grants across Asia-Pacific add further scale. Hardware still anchors most procurements, yet software platforms that transform raw measurements into regulatory-ready analytics are scaling fast. Competition remains moderate as long-established reference-grade instrument suppliers defend their share against low-cost sensor specialists and cloud-native entrants.

Key Report Takeaways

- By product type, outdoor monitors held 62.40% of the air quality monitoring market share in 2025, whereas indoor monitors are poised for a 9.10% CAGR through 2031.

- By sampling method, continuous accounted for 55.30% of the market share in 2025 and is projected to grow by 8.25% CAGR through 2031.

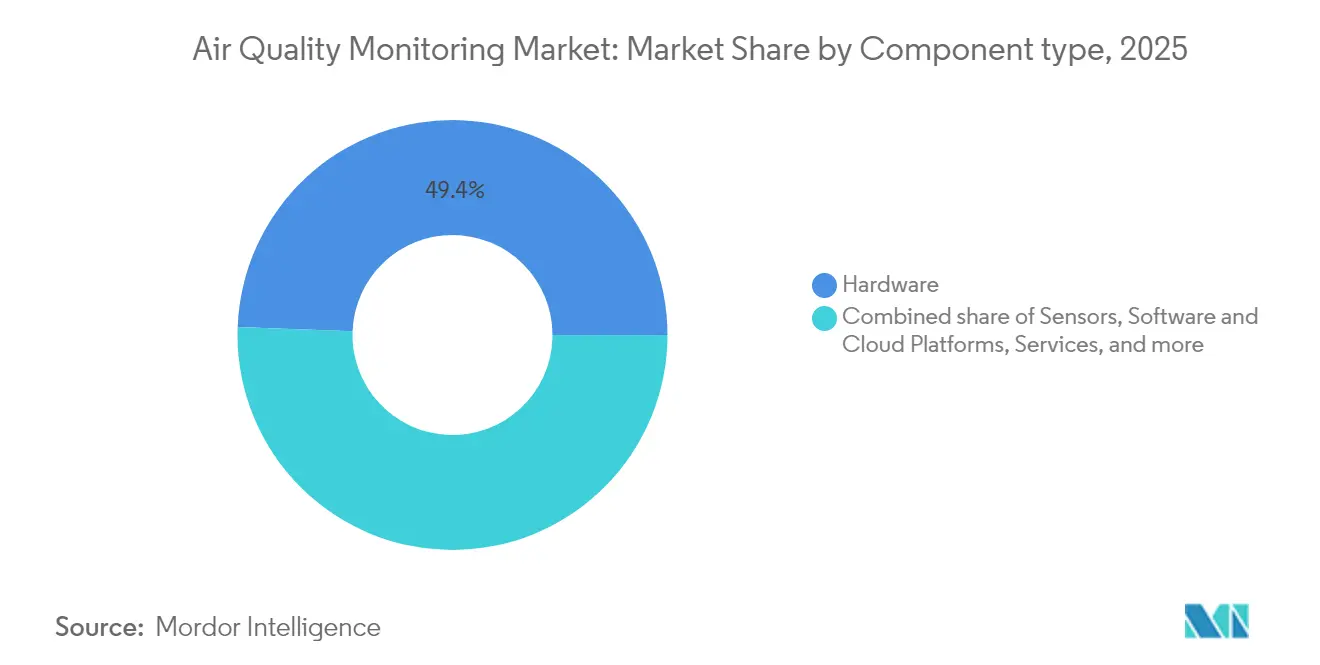

- By component, hardware captured 49.40% revenue share in 2025, while software and cloud platforms are set to expand at a 9.55% CAGR by 2031.

- By pollutant parameter, particulate pollutants held 56.20% of the air quality monitoring market share in 2025, whereas biological pollutants are poised for a 8.95% CAGR through 2031.

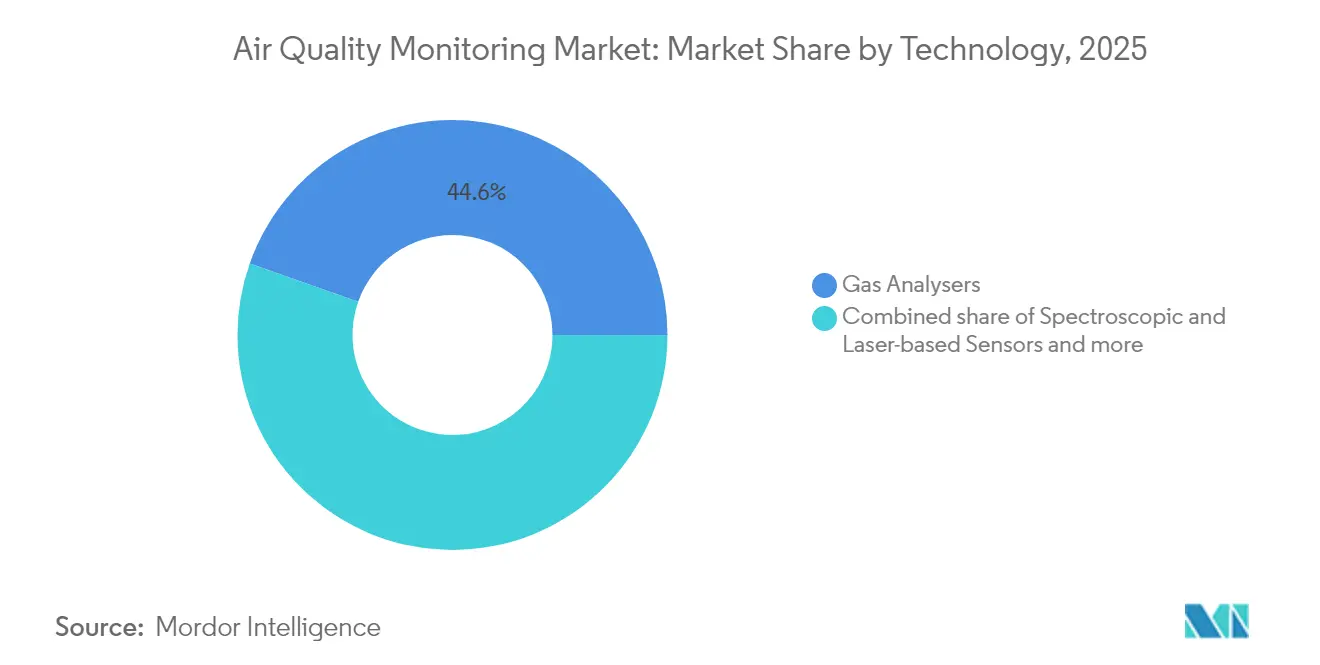

- By technology, gas analysers accounted for 44.60% of the market share in 2025, whereas spectroscopic and laser-based sensors are projected to grow by 8.60% CAGR through 2031.

- By deployment mode, fixed monitoring stations captured 64.20% revenue share in 2025, while drone-mounted and mobile platforms are set to expand at a 9.15% CAGR by 2031.

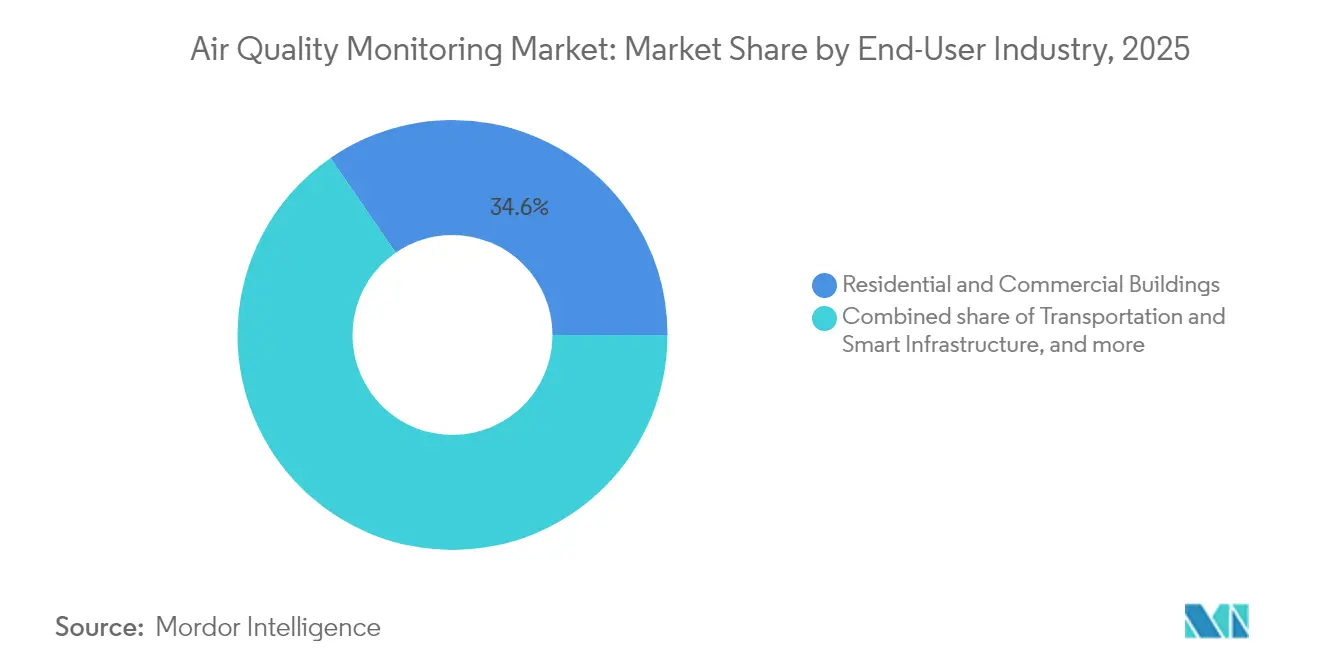

- By end-user, residential and commercial buildings accounted for 34.60% of the air quality monitoring market in 2025; residential and commercial buildings applications are advancing at an 7.75% CAGR through 2031.

- By geography, Asia-Pacific led with 37.50% revenue share in 2025 and is forecast to register the fastest 8.55% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Air Quality Monitoring Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| National-level roll-outs of low-cost sensor networks in Asian smart-city programs | +1.20% | Asia-Pacific core, spill-over to MEA | Medium term (2-4 years) |

| Corporate ESG disclosure mandates in EU requiring real-time ambient data for Scope 3 reporting | +0.80% | Europe & North America, expanding to APAC | Short term (≤ 2 years) |

| Rise of wildfire smoke events in North America driving demand for distributed PM sensors | +0.60% | North America, with spillover to Australia | Short term (≤ 2 years) |

| Integration of AQ data into HVAC automation in commercial buildings post-COVID | +0.50% | Global, with early gains in North America & EU | Medium term (2-4 years) |

| Mandatory fence-line monitoring around US petrochemical clusters after EPA OOOOa rule | +0.40% | North America, with regulatory spillover to EU | Long term (≥ 4 years) |

| Deployment of drone-based monitoring for methane & VOC detection in O&G assets | +0.30% | Global, concentrated in major O&G regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

National-level roll-outs of low-cost sensor networks in Asian smart-city programs

Extensive smart-city budgets across China, India, and Japan are underwriting dense sensor deployments that fill spatial data gaps left by sparse reference-grade stations. China’s Blue Sky Protection Campaign now covers 269 cities and leverages digital integration to cut PM2.5 levels in resource-heavy municipalities.(1)Systems Journal, “Digital Technology Improves Air Quality in Chinese Cities,” sysj.pku.edu.cnHyderabad’s 49-node grid spanning 4 km² illustrates how granular data surfaces seasonal PM patterns missed by legacy networks.(2)Frontiers in Internet of Things, “Low-Cost Sensor Network in Hyderabad,” frontiersin.orgJapanese researchers apply AI algorithms—AIRTrans—to satellite inputs, lowering aerosol optical thickness errors and guiding local compliance programs. Bulk procurement volumes push sensor prices down, accelerating adoption and giving policymakers evidence to direct targeted emission controls.

Corporate ESG disclosure mandates in EU requiring real-time ambient data for Scope 3 reporting

Roughly 50,000 companies must now file granular emissions accounts under the EU Corporate Sustainability Reporting Directive, spurring investments in continuous ambient monitoring to support Scope 3 calculations. Banks follow European Banking Authority rules that embed air quality risks into credit assessments.(3)European Banking Authority, “Guidelines on ESG Risk Management,” eba.europa.eu California’s Climate Corporate Data Accountability Act and Australia’s incoming disclosure penalties reinforce the global trend, compressing compliance timelines and lifting demand for automated monitoring networks that integrate directly with greenhouse gas inventories.

Rise of wildfire smoke events in North America driving demand for distributed PM sensors

Wildfires that blanketed the Midwest and Eastern Seaboard in 2023 raised emergency room visits and highlighted gaps in real-time smoke data. Rapid-deployment projects such as Caltech’s PHOENIX network install low-cost PM sensors within days of ignitions, feeding local alerts. Satellite-driven smoke algorithms presented at the American Geophysical Union meeting classify city-level exposure hot spots, prompting municipalities to adopt permanent sensor arrays for community warnings. Portable multi-parameter kits for first responders extend protection to frontline personnel.

Integration of AQ data into HVAC automation in commercial buildings post-COVID

Building owners increasingly link IAQ sensors to BMS platforms that modulate ventilation in real-time. Siemens’ Smart Air Quality offering supports the US EPA Clean Air in Buildings Challenge and demonstrates combined IAQ gains and energy savings. Quebec’s 47,000-sensor school network transmits readings every five minutes via LoRaWAN, enabling timely ventilation changes while capturing more than 7 million messages daily. Academic pilots show CO₂-based occupancy detection can drive demand-controlled ventilation strategies that lower energy bills without sacrificing air quality.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Calibration-drift & accuracy issues of low-cost sensors limiting bulk procurements | -0.90% | Global, particularly affecting developing markets | Short term (≤ 2 years) |

| Delays in 5G/LPWAN roll-outs in rural Africa hindering remote-station connectivity | -0.40% | Sub-Saharan Africa, with spillover to rural Asia | Medium term (2-4 years) |

| High maintenance cost of reference-grade analyzers for cash-strapped municipalities | -0.30% | Global, concentrated in emerging markets | Long term (≥ 4 years) |

| Complex multi-jurisdictional certification (EPA EQOA, EU CEN) slowing time-to-market | -0.20% | North America & Europe, affecting global suppliers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Calibration-drift & accuracy issues of low-cost sensors limiting bulk procurements

Field trials show that machine-learning recalibration can improve NDIR CO₂ sensor accuracy by 65%, yet inter-model variability remains wide, and temperature or humidity swings still skew particulate readings.(4)MDPI Sensors, “Machine Learning Calibration of NDIR CO2 Sensors,” mdpi.com Agencies such as the US EPA and European AirSensEUR project are drafting harmonized calibration protocols, but until those frameworks mature, city planners often cap purchase volumes or keep sensors in pilot mode. Quantile mapping and other statistical corrections add cost and complexity, tempering near-term uptake in budget-sensitive regions.

Delays in 5G/LPWAN roll-outs in rural Africa hindering remote-station connectivity

Studies from GSMA highlight the lag in 5G coverage across sub-Saharan markets, making real-time uploads from remote monitors unreliable. LoRaWAN backbones solve some power and cost issues but still need dense gateway placement, a hurdle for sparsely populated areas. Cellular router workarounds—such as Teltonika’s RUT-series deployments—perform well in Europe yet depend on local network quality. Without communications and power resilience, project scale-up in rural districts slows, limiting data visibility where public health needs are acute.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Outdoor dominance maintains regulatory backbone

Outdoor analyzers delivered 62.40% of 2025 revenues as federal rules, including the US EPA’s stricter PM2.5 limit of 9 µg/m³, imposed round-the-clock compliance checks. Fixed stations equipped with Federal Reference Method instruments form the air quality monitoring market size cornerstone for government networks. Complementing them are mobile platforms, including university-developed drones that sample plume constituents in three-dimensional profiles.

Indoor monitors are the fastest risers, expanding at 9.10% CAGR by catering to post-pandemic ventilation mandates and healthy-building certifications. Portable badges and room sensors connect over BLE, Wi-Fi, or LoRaWAN, streaming data into BMS dashboards for real-time HVAC adjustments. Feature integration—temperature, RH, PM, TVOC, and eCO₂ in one board—cuts deployment friction and enhances uptake across offices, classrooms, and healthcare settings.

By Sampling Method: Continuous monitoring secures compliance confidence

Continuous systems account for 55.30% of the air quality monitoring market size, championed by EPA Performance Specification 19 for ethylene oxide CEMS and parallel NSPS logic that require automatic data capture at one-minute intervals. Industrial operators prefer laser-based continuous analyzers that auto-zero and self-calibrate, cutting maintenance downtime.

Continuous methods grow 8.25% annually thanks to their cost advantage for dense grids. Cartridge-based passive samplers at petrochemical fence lines and battery-powered mini-stations on urban lampposts gather legally defensible snapshots where 24 × 7 power is infeasible, broadening spatial coverage without heavy capital outlays.

By Component: Hardware foundation enables software-led value creation

Hardware retained a 49.40% share in 2025. Compliance projects still specify chemiluminescence or FDMS PM modules to match statutory uncertainty thresholds.

Software and cloud platforms, projected to scale 9.55% CAGR, transform raw signals into insights through AI-enabled calibration, forecasting, and compliance dashboards. The UAE’s 31-station National Air Quality Platform feeds a machine-learning model that predicts three-day episodes and informs traffic planning. Multitenant SaaS architectures also simplify enterprise Scope 3 reporting, driving subscription stickiness.

By Pollutant Parameter: Particulate standards tighten, biology emerges

Regulators’ focus on PM2.5 and PM10 underpins 56.20% share for particulate sensors. Europe’s new directive will add mandatory ultrafine particle counts by 2030, steering demand to condensation particle counters and SMPS units.

Biological monitoring is the quickest-growing slice at 8.95% CAGR as research links bioaerosols with haze events and allergenic burdens. Sensors that trap spores and RNA fragments are moving from labs into municipal stations, enabling health departments to warn vulnerable populations more precisely.

By Technology: Spectroscopy lifts accuracy ceiling

Gas analyzers still lead with a 44.60% share, leveraging decades of chemiluminescence and NDIR reliability. Yet spectroscopic and laser-based modalities, advancing at 8.60% CAGR, now meld FTIR, UV-DOAS, and LiDAR in compact footprints. Chinese-developed SkyLidar systems produce three-dimensional scans of PM2.5, while AI-enhanced satellite retrievals like AIRTrans shrink aerosol error margins for policymakers.

By Deployment Mode: Fixed grids anchor, drones accelerate

Fixed stations contribute 64.20% of the 2025 value, delivering long-term baselines required for NAAQS attainment plans. New procurement favors modular huts with integrated gas, PM, meteorology suites, and redundant power.

Drone and other mobile platforms expand 9.15% annually. Systems such as Botlink’s 7-kg multicopter measure NO₂, SO₂, CO, and O₃ over a 15-mile radius, useful in wildfire smoke mapping and pipeline leak surveys. Hybrid networks that fuse fixed, portable, and drone data streams provide fuller spatial granularity.

By End-User Industry: Residential and commercial buildings spearhead new growth

Residential and commercial buildings remained the largest buyers, holding a 34.60% share, due to the growing construction activities in the developing countries.

Residential and commercial buildings log the fastest 7.75% CAGR. Thanks to regulatory mandates, smart buildings, LEED/green certifications, and HVAC/BMS integration, commercial buildings are driving the market. In addition, Residential is fueled by smart-home demand, consumer health awareness, and higher adoption of portable & integrated monitors.

Geography Analysis

Asia-Pacific delivered 37.50% of 2025 revenue, and the fastest 8.55% CAGR through 2031, buoyed by China’s 269-city Blue Sky grid and India’s district-level pilots that reveal hyper-local pollution nuances. Japan’s AI-powered satellite analytics further elevate regional technical sophistication. Manufacturing depth lowers per-unit sensor costs, tilting global supply chains toward the region and helping governments roll out thousands of nodes in compressed timeframes.

The Middle East is the second fastest growing region through 2030 due to sovereign commitments to smart-city livability targets. The UAE operates 31 AI-enabled stations and funds USD 500 million for new mobile units, while Saudi Arabia equips 7,000 industrial sites for continuous emissions checks. Offshore research cruises and carbon-based sensor R&D underscore regional scientific ambition.

North America remains regulation-driven, anchored by the EPA’s updated PM2.5 standard that obliges daily Air Quality Index reporting in all metros above 350,000 residents. Wildfire smoke episodes spanning from British Columbia to the Mid-Atlantic catalyze community sensor deployments and emergency service toolkits. Europe’s growth is shaped by ESG mandates and the 2024 Ambient Air Quality Directive that introduces ultrafine particle metrics. South America and Africa seize pilot funding yet face telecom and power gaps that slow remote-station rollout, though LoRaWAN and solar kits begin to close the divide in urban clusters.

Mordor Intelligence provides coverage of the air quality monitoring market across other key regional markets, including Asia, South America, Europe, and Middle East and Africa, each with their regulatory frameworks and demand patterns.

Competitive Landscape

The market structure is moderately fragmented. Thermo Fisher Scientific, Teledyne Technologies, and Siemens guard installed bases thanks to EPA Federal Reference Method certifications, while Sensirion, Bosch Sensortec, and PurpleAir monetize low-cost sensor volumes for citizen science and IoT stacks. Consolidation is underway: SICK transferred about 800 staff into a joint venture with Endress+Hauser to strengthen gas analysis portfolios, and DwyerOmega’s 2024 acquisition of Process Sensing Technologies widened vertical reach into pharma and energy.

Competitive advantage increasingly hinges on software differentiation. Teledyne’s ACES aircraft suite pairs laboratory-grade analyzers with cloud ingestion for flight safety analytics. Mobile Physics pioneers consumer cellphone sensing to crowd-source urban exposure maps. Vendors with ready pathways through multi-jurisdictional certifications protect premium pricing, whereas analytics-first newcomers target subscription margins above commoditized hardware. Opportunities also open in biological monitoring and drone platforms, where reference standards are still nascent and early movers can set de facto benchmarks.

Air Quality Monitoring Industry Leaders

Siemens AG

Thermo Fisher Scientific Inc.

Horiba Ltd

Emerson Electric Co.

MicroJet Technology Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: SICK and Endress+Hauser completed their partnership, forming Endress+Hauser SICK GmbH+Co. KG to scale gas analysis for waste-to-energy and O&G projects

- November 2024: Process Sensing Technologies was acquired by DwyerOmega, expanding combined reach into environmental sensors for pharma and utilities

- October 2024: The EU approved a stronger Ambient Air Quality Directive that mandates ultrafine particle monitoring by 2030.

- September 2024: Honeywell and Samsung E&A agreed to market carbon-capture solutions to mitigate 320 million tCO₂e by 2030.

Global Air Quality Monitoring Market Report Scope

An air quality monitoring system is a sensor-based instrument that detects and monitors the levels of pollutants, such as sulfur dioxide, nitrous oxide, particulate matter, carbon monoxide, and volatile organic compounds, in indoor and outdoor environments.

The air quality monitoring market is segmented by product type, sampling method, pollutant type, end user, and geography. By product type, the market is segmented into indoor monitors and outdoor monitors. By sampling method, the market is segmented into continuous, manual, and intermittent. By pollutant type, the market is segmented into chemical pollutants, physical pollutants, and biological pollutants. By end user, the market is segmented into residential and commercial, power generation, petrochemicals, and other end users. The report also covers the market size and forecasts for the air quality monitoring market across major regions. For each segment, the market sizing and forecasts have been done based on revenue (USD billion).

| Indoor Monitors (Fixed/Stationary Indoor and Portable/Wearable Indoor) |

| Outdoor Monitors (Fixed/Stationary Outdoor and Portable/Mobile Outdoor) |

| Continuous |

| Manual |

| Intermittent/Passive |

| Hardware |

| Sensors |

| Samplers and Pumps |

| Data Loggers and Analysers |

| Software and Cloud Platforms |

| Services (Calibration, Maintenance, Data Subscriptions) |

| Particulate Pollutants (PM1, PM2.5, PM10, UFP) |

| Gaseous Pollutants (NOx, SO?, O?, CO, VOCs) |

| Toxic Metals and Radionuclides (Pb, Hg, Radon) |

| Biological Pollutants (Pollen, Mould Spores, Bacteria) |

| Gas Analysers (Chemiluminescence, NDIR, FID) |

| Particle Counters (Optical, Gravimetric, Beta-attenuation) |

| Spectroscopic and Laser-based Sensors (FTIR, UV-DOAS, LiDAR) |

| Fixed Monitoring Stations |

| Portable Detectors |

| Wearable AQ Sensors |

| Drone-mounted and Mobile Platforms |

| Residential and Commercial Buildings |

| Industrial Facilities (Power Generation, Oil, Gas and Petrochemicals, Mining and Metallurgy, and Discrete and Process Manufacturing) |

| Government and Academic Research |

| Healthcare Facilities |

| Transportation and Smart Infrastructure (Airports, Tunnels, Smart-City Networks) |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Nordic Countries | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Malaysia | |

| Thailand | |

| Indonesia | |

| Vietnam | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Product Type | Indoor Monitors (Fixed/Stationary Indoor and Portable/Wearable Indoor) | |

| Outdoor Monitors (Fixed/Stationary Outdoor and Portable/Mobile Outdoor) | ||

| By Sampling Method | Continuous | |

| Manual | ||

| Intermittent/Passive | ||

| By Component | Hardware | |

| Sensors | ||

| Samplers and Pumps | ||

| Data Loggers and Analysers | ||

| Software and Cloud Platforms | ||

| Services (Calibration, Maintenance, Data Subscriptions) | ||

| By Pollutant Parameter | Particulate Pollutants (PM1, PM2.5, PM10, UFP) | |

| Gaseous Pollutants (NOx, SO?, O?, CO, VOCs) | ||

| Toxic Metals and Radionuclides (Pb, Hg, Radon) | ||

| Biological Pollutants (Pollen, Mould Spores, Bacteria) | ||

| By Technology | Gas Analysers (Chemiluminescence, NDIR, FID) | |

| Particle Counters (Optical, Gravimetric, Beta-attenuation) | ||

| Spectroscopic and Laser-based Sensors (FTIR, UV-DOAS, LiDAR) | ||

| By Deployment Mode | Fixed Monitoring Stations | |

| Portable Detectors | ||

| Wearable AQ Sensors | ||

| Drone-mounted and Mobile Platforms | ||

| By End-User Industry | Residential and Commercial Buildings | |

| Industrial Facilities (Power Generation, Oil, Gas and Petrochemicals, Mining and Metallurgy, and Discrete and Process Manufacturing) | ||

| Government and Academic Research | ||

| Healthcare Facilities | ||

| Transportation and Smart Infrastructure (Airports, Tunnels, Smart-City Networks) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Nordic Countries | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Malaysia | ||

| Thailand | ||

| Indonesia | ||

| Vietnam | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the air quality monitoring market?

The air quality monitoring market stands at USD 6.15 billion in 2026.

How fast will the air quality monitoring market grow by 2031?

It is projected to grow at a 7.35% CAGR to reach USD 8.77 billion by 2031.

Which region leads the air quality monitoring market?

Asia-Pacific commands 37.50% of 2025 revenues due to expansive smart-city programs and industrial demand.

What segment (Deployment mode) is expanding the quickest?

Drone-mounted and other mobile platforms show the highest 9.15% CAGR thanks to wildfire, oil-and-gas and remote-area monitoring needs.

Why are software platforms gaining share?

AI-based calibration and analytics turn raw sensor streams into compliance-ready insights, driving a 9.55% CAGR for software and cloud services.

How strict are new PM2.5 regulations?

The US EPA lowered the annual PM2.5 standard to 9 µg/m³ in 2024, requiring daily AQI updates for all metros above 350,000 residents.

Page last updated on: