Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2020 - 2024 |

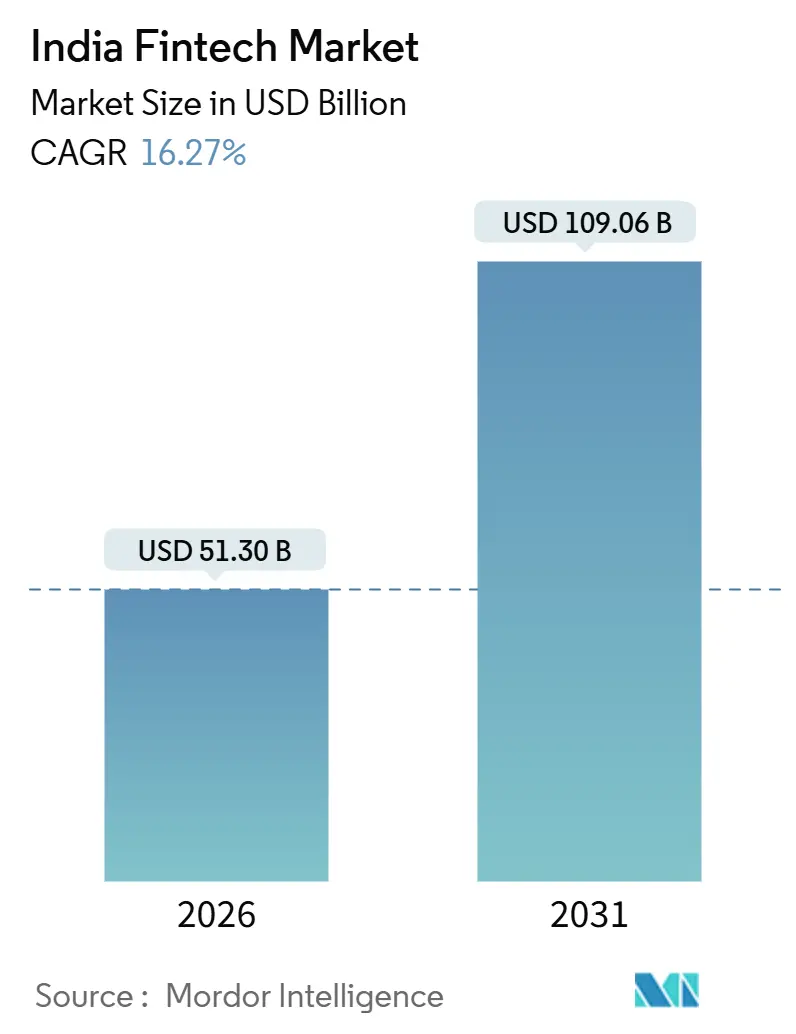

| Market Size (2026) | USD 51.30 Billion |

| Market Size (2031) | USD 109.06 Billion |

| Growth Rate (2026 - 2031) | 16.27% CAGR |

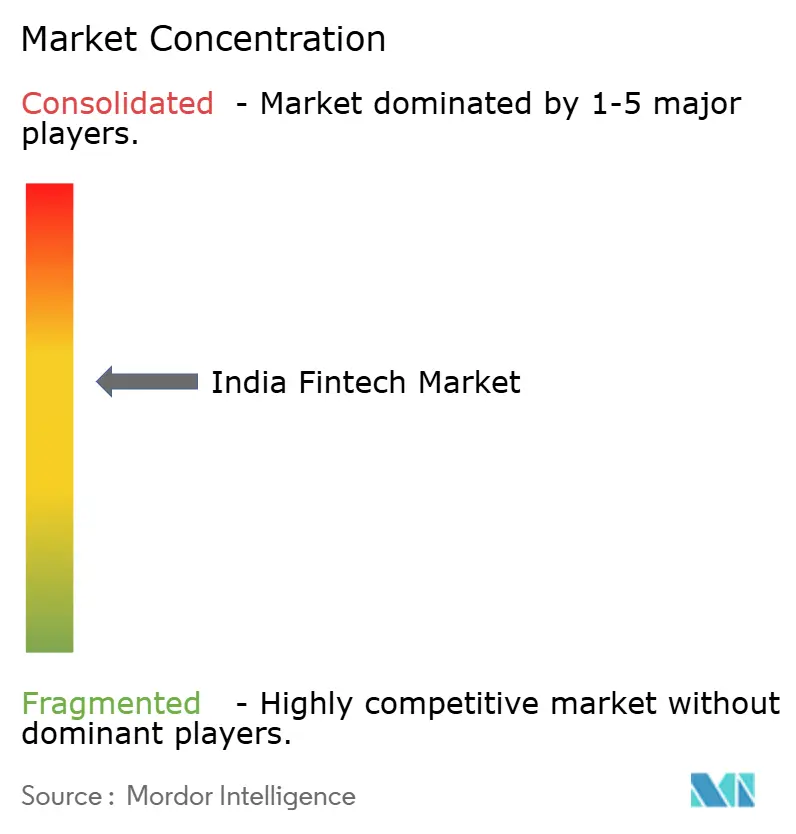

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Fintech Market Analysis by Mordor Intelligence

The India fintech market size is USD 51.30 billion in 2026 and is projected to reach USD 109.06 billion by 2031 at a 16.27% CAGR during the forecast period (2026-2031).

This expansion aligns with accelerating adoption of India’s digital public infrastructure, including UPI for instant payments, Aadhaar for e-KYC, and the Account Aggregator framework for consent-based data sharing that reduces underwriting friction across retail and MSME segments. India accounts for 49% of global real-time payment volumes in 2023, which sustains the transaction scale that anchors monetization across adjacent credit, insurance, and wealth products. Digital payments hold the largest segment share and remain the gateway for cross-sell, while neobanking is the fastest growing as multi-bank UPI and app-first interfaces expand access to deposits, credit, and spending tools. The India fintech market benefits from government incentives on low-value UPI P2M transactions, which drive merchant acceptance and sustain usage habits across small-ticket payments in semi-urban and rural areas. The Account Aggregator ecosystem’s scale-up, combined with Aadhaar authentication reaching near-universal adult coverage, enables faster onboarding and data-rich underwriting models that reduce acquisition costs and improve risk selection for regulated entities and fintech partners.

Key Report Takeaways

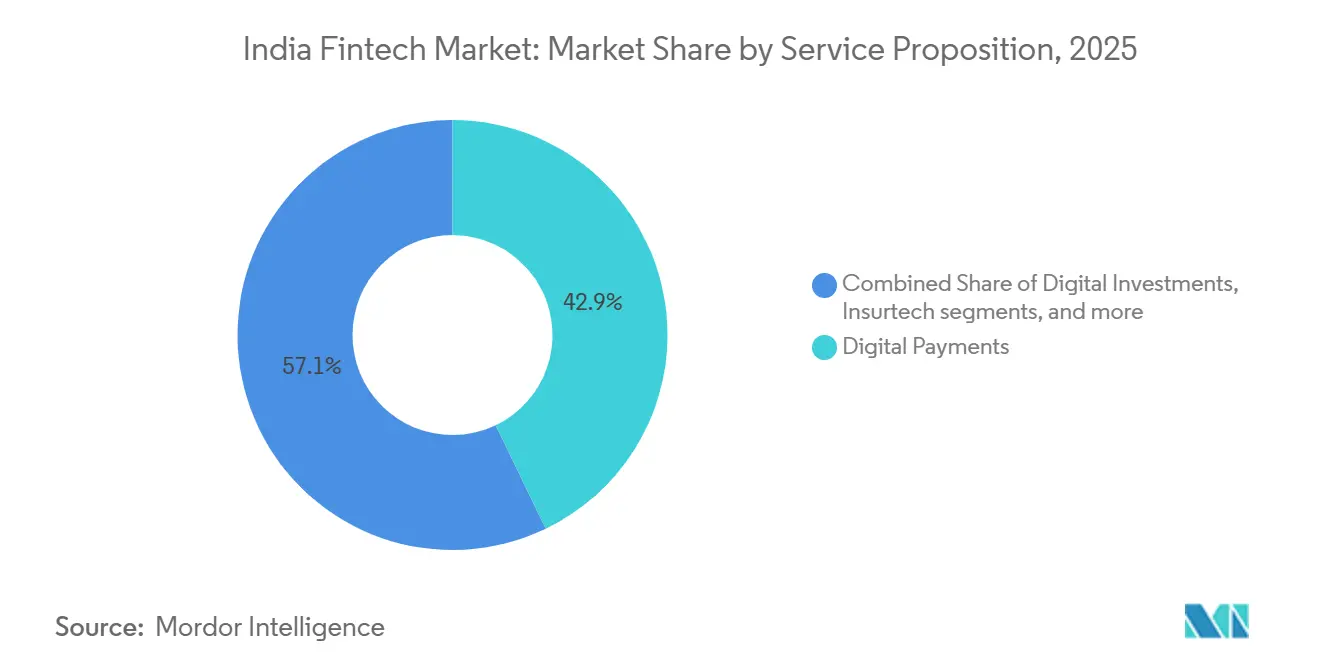

- By service proposition, digital payments led with 42.87% of the India fintech market share in 2025, while neobanking is projected to grow at a 19.64% CAGR during 2026 to 2031.

- By end-user, retail accounted for 66.24% of the India fintech market share in 2025, while business-facing solutions are projected to expand at a 17.52% CAGR through 2031.

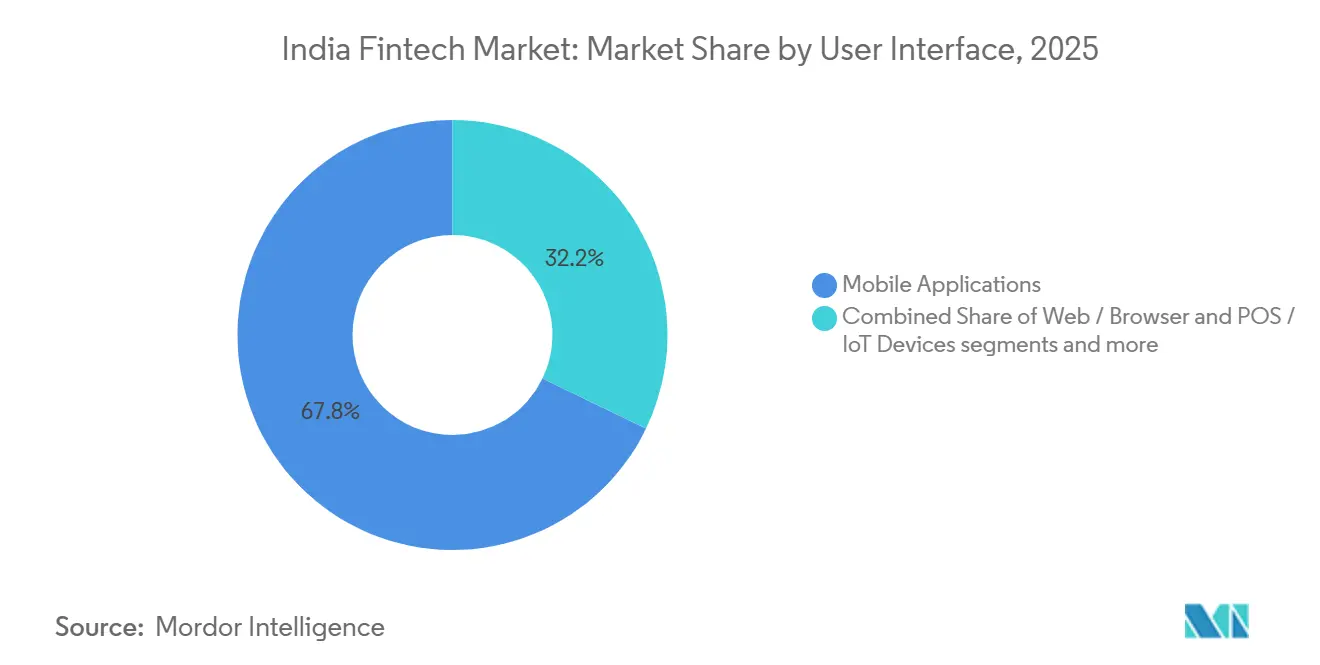

- By user interface, mobile applications commanded 67.83% of the India fintech market share in 2025 and are projected to grow at 18.39% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

India Fintech Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government-Built Digital Public Infrastructure Accelerating Adoption | + 4.2% | National, metros to rural via Aadhaar and UPI voice flows | Medium term (2-4 years) |

| Account Aggregator Framework Enabling Data-Driven Credit | + 2.8% | National, led by urban centres | Medium term (2-4 years) |

| Embedded-Finance Demand from E-commerce and Gig Platforms | + 3.1% | National, metro to tier-2 clusters | Short term (≤ 2 years) |

| Formalization of MSMEs post-GST is Creating New Demand Pools | + 2.5% | National, strong in industrial states | Medium term (2-4 years) |

| Millennial and Gen-Z Wealth Creation Boosting Robo-Advisory | + 1.9% | Urban India with tier-2 spillover | Medium term (2-4 years) |

| Cross-Border UPI Linkages Opening Remittance Revenues | + 1.8% | Corridors with ASEAN and the Middle East | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Government-Built Digital Public Infrastructure (UPI, Aadhaar, OCEN) Accelerating Mass-Market Adoption

India’s real-time payments infrastructure, Aadhaar-based identity, and interoperable data-sharing rails together remove friction that previously slowed onboarding and transactions at scale. India’s share of global real-time payments reached 49% in 2023, which supports recurring payment behaviours and merchant acceptance models that monetize at large daily volumes. Aadhaar authentication hit 2.21 billion in August 2025, with adult coverage at 99.7%, which closes KYC gaps and shortens onboarding in the India fintech market[1]Unique Identification Authority of India, “UIDAI Records 221 Crore Aadhaar Authentication Transactions in August 2025,” UIDAI, uidai.gov.in. The Account Aggregator network has linked consented users to over 2.61 billion enabled accounts, allowing lenders and insurance distributors to retrieve verified financial data within seconds, which compresses underwriting timelines for thin-file customers[2]Department of Financial Services, “Account Aggregator Framework,” Ministry of Finance, financialservices.gov.in. Together, these rails power scale economics that favour embedded journeys across payments, credit, insurance, and investments as the India fintech market deepens coverage in semi-urban and rural districts.

Account Aggregator Framework Unlocking Data-Driven Credit Underwriting

The Account Aggregator framework normalizes consent-based access to financial data and reduces the cost of risk assessment for banks and NBFCs partnering with fintech platforms. With users connecting bank accounts and other financial repositories through licensed AAs, lenders derive a real-time view of cash flows, which supports extensions of small-ticket working capital and personal credit to thin-file customers. RBI’s broader regulatory sandbox and digital lending directions strengthen disclosures and grievance processes, which support sustainable scale for the India fintech market as more lenders shift from screen-scraping to auditable consent models. Standardization across APIs and consent flows lowers manual verification delays that once kept micro-entrepreneurs and gig workers outside formal credit. Over time, underwriting that relies on verified transaction trails improves portfolio quality while increasing access for first-time borrowers in the India fintech market.

Embedded-Finance Demand from E-commerce and Gig-Economy Platforms

E-commerce checkouts, logistics apps, and service marketplaces embed payments, credit, and protection into transaction flows, shifting financial product discovery from standalone journeys to on-platform prompts. Payment aggregators introduced buyer protection and merchant tools such as corporate cards and checkout credit, which lift conversion and create post-transaction monetization paths at scale. Government incentives for low-value UPI P2M transactions encourage merchant acceptance and reduce resistance to digital settlement, which increases the utility of embedded finance across small merchants. Gig platforms that settle earnings digitally create demand for embedded credit and micro-insurance, which extends product reach to new-to-credit cohorts in the India fintech market. As API-led integrations spread, revenue models shift toward revenue sharing and subscription-like bundles that align platform growth with financial product scale in the India fintech market[3]Razorpay, “Everything We Launched at FTX 2025,” Razorpay, razorpay.com.

Formalization of MSMEs Post-GST Creating New SME Fintech Demand Pools

GST compliance and digital invoicing expand verifiable data trails that modern underwriting can use to assess MSME creditworthiness in the India fintech market. Registrations on the Udyam and Udyam Assist platforms create a formal base of micro and small businesses that can be addressed through API-driven lending and payments services. The RAMP program, which is supported by the World Bank and operational through FY 2026-27, supports technology upgrades, digital onboarding, and capacity building for MSMEs, which strengthens demand for embedded fintech in procurement and receivables. Incentives like per-transaction reimbursements under programs that target artisans and micro-entrepreneurs help build enduring digital payment habits among traditional businesses. These interventions shift MSMEs from cash-based informal operations toward bankable behaviours, which enlarges the addressable base for the fintech industry in India.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| RBI Digital-Lending and FLDG Norms Raising Compliance Cost | - 2.3% | National, heavier for smaller NBFCs | Short term (≤ 2 years) |

| Zero-MDR Policy Compressing Payment-Gateway Profit Pools | - 1.7% | National, for aggregators and acquirers | Medium term (2-4 years) |

| Escalating Cyber-Fraud Incidents Undermining Trust | - 1.4% | National, higher in urban centres | Short term (≤ 2 years) |

| Post-2022 Funding Winter Constraining Scale-Up Capital | - 1.3% | National, affecting mid to late stages | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

RBI’s Stricter Digital-Lending and FLDG Norms Raising Compliance Cost

RBI’s digital lending directions strengthen disclosures, escrow segregation, and grievance handling, which increases fixed compliance costs for platforms and their regulated partners in the India fintech market. Clarifications around risk retention and default guarantees shift capital requirements to lenders and co-lenders, which compresses margins for models that depended on risk transfer to bank partners. Larger lenders and well-capitalized platforms can absorb these costs, while smaller entities face exit or consolidation as compliance becomes a scale advantage in the India fintech market. RBI’s sandbox and supervisory focus push product design toward transparency and customer protection, which reduces regulatory risk but slows experimental rollouts. This recalibration prioritizes sustainable origination over rapid growth, which tempers expansion in digital lending before a new equilibrium emerges in the India fintech market.

Zero-MDR Policy Compressing Payment-Gateway Profit Pools

Zero MDR on RuPay debit and UPI transactions removes a direct revenue line for payment aggregators, which pushes monetization to value-added services such as corporate cards, working capital, and business banking in the India fintech market. The government’s UPI P2M incentive cushion supports smaller merchant transactions but does not replace MDR economics for large merchants or high-ticket volumes. Aggregators with credit and software stacks can cross-sell to defend margins, while subscale providers struggle to offset the revenue compression as the India fintech market shifts to bundled services. RBI’s guidance for payment aggregators, including net worth thresholds, increases entry barriers and deepens the need for diversified monetization for players that remain. These moves anchor long-term stability while reducing short-term profitability for pure-play payments in the Indian fintech market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Proposition: Payments Dominate, Neobanking Ascends as Digital-First Banking Matures

Digital payments captured 42.87% of the India fintech market share in 2025, anchored by UPI’s scale and merchant acceptance that sustains habitual usage across daily purchases. India’s real-time rail supports checkout conversion and merchant trust, which anchors cross-sell into protection, loan, and wealth products across the India fintech market. The India fintech industry uses app-first journeys and interoperable rails to reduce acquisition friction and extend reach beyond metros into semi-urban districts. Aggregators ship enterprise and SMB tools, including buyer protection and export settlement accounts, which create monetization beyond MDR in the India fintech market. As regulatory guidance on payment aggregators raises net worth thresholds, scale advantages, and compliance maturity, it drives consolidation within payments.

The India fintech market size for neobanking is projected to expand at a 19.64% CAGR between 2026 and 2031 as multi-bank UPI models and app-centric accounts deepen usage among digital-first customers. Neobanks layer budgeting, credit access, and business banking features on top of existing rails, which improves retention and fee capture in the India fintech market. Digital lending growth moderates in the near term as risk retention norms and disclosure-heavy processes add cost, which encourages co-lending models with banks and more selective origination. Wealth and insurance aggregators scale by combining distribution with service layers, while maintaining customer acquisition through cross-sell on a large payment basis in the India fintech market. Over the forecast period, propositions that bundle payments, credit, and protection into unified interfaces are positioned to capture higher lifetime value per user in the India fintech market.

By End-User: Retail Leads, Yet Business Solutions Accelerate as Enterprises Digitize Treasury Functions

In 2025, retail accounted for a 66.24% share of the fintech market size in India, lifted by smartphone penetration, instant onboarding via Aadhaar e-KYC, and everyday UPI use across P2P and P2M transactions. Consumer journeys through payments, small-ticket credit, and investments continue to widen as app-first experiences simplify onboarding and service. Cross-sell along a large payments base drives growth for platforms that now bundle lending, protection, and wealth inside the same interface in the India fintech market. Over the last year, app-first brokers and aggregators deepened reach, while onboarding costs fell due to interoperable rails and consent-based data flows. Retail scale remains sensitive to income cycles and equity sentiment, yet penetration continues to rise from a low base in the India fintech market.

Business-facing solutions are projected to grow at a 17.52% CAGR from 2026 to 2031 as enterprises embed APIs for payouts, vendor payments, reconciliation, and expense management in the India fintech market. Payment aggregators ship corporate cards and business banking suites that integrate with ERP and accounting software to streamline treasury operations. MSME credit demand expands as GST data and Udyam registrations improve the reliability of underwriting inputs across lenders and co-lenders. Platforms broaden revenue from pure transactions to subscriptions and credit-linked services, which lifts average revenue per business user in the India fintech market. As interoperability gains and product breadth increase, business adoption becomes stickier due to integrations with procurement and reconciliation workflows in the India fintech market.

By User Interface: Mobile Applications Command, Biometric, and Offline UPI Extend Access

Mobile applications commanded 67.83% share of the India fintech market size in 2025 and are projected to grow at 18.39% through 2031, supported by UPI Lite, biometric authentication, and app-first account opening that improve completion rates. UPI’s expansion with low-value incentives supports small-ticket merchant payments and new user cohorts in semi-urban and rural areas. Voice-based 123PAY extends feature phone access, which broadens addressability for payments beyond smartphones in the India fintech market. Payment and business banking suites now include chat-native assistants that execute tasks inside conversations, which reduces drop-offs that occur during context switching. Web dashboards remain central for enterprise administrators who need granular control, while mobile-first remains the primary interface for end users in the India fintech market.

Point-of-sale and IoT devices continue to expand offline acceptance and provide real-time reconciliation through cloud dashboards, which support SMB digitization in the India fintech market. Offline merchant tools such as soundboxes and multi-mode POS become complementary to mobile, especially where bandwidth is variable. RBI’s guidance on payment aggregators clarifies compliance and net worth requirements for device-led acceptance models, which benefits well-capitalized providers over subscale entrants. As biometric and tokenization standards spread, checkout completion rates improve across in-app, web, and in-store contexts for the India fintech market. The combined effect is a hybrid interface strategy that pairs mobile dominance with merchant-point innovation in the India fintech market.

Geography Analysis

The India fintech market concentrates in metro and tier-1 centres where banking density and smartphone adoption are strongest, while policy and infrastructure spread usage outward to semi-urban districts. RBI’s Master Direction on payment aggregators specifies authorization norms and net worth thresholds, which strengthen compliance baselines for providers headquartered in these hubs. Aadhaar authentication at a national scale enables uniform KYC experiences that reduce onboarding delays across states and districts. Payment and insurance aggregators continue to deepen their reach across tier-2 and tier-3 markets through hybrid distribution that blends digital channels with local agents. The India fintech market keeps building on national platforms while local merchant acceptance and customer support adapt to regional contexts.

Semi-urban districts and tier-3 cities show faster adoption velocity as incentives and simplified user flows lower barriers to digital payments. Voice-based UPI improves accessibility in low-bandwidth and feature phone environments, which supports inclusion goals for the India fintech market. Company rollouts of merchant devices, settlement tools, and agent support help onboard small businesses that prefer assisted journeys. Insurance and wealth aggregators expand with localized partner networks that support advisory and claims service in new districts. The result is a broader reach without sacrificing service quality as the India fintech market scales.

Cross-border corridors become an additional growth lever as UPI connectivity expands, which supports exporter settlement and diaspora spending capture in the India fintech market. Exporter accounts tailored for marketplaces and faster settlement help ease liquidity constraints for small sellers who expand sales across borders. Merchant acceptance for inbound travellers and diaspora segments, paired with domestic payout efficiencies, increases the utility of platform-led services beyond India’s borders. Compliance clarity on payment aggregation and data-sharing practices reduces frictions for global enterprises that serve Indian customers. Over time, corridor expansion improves resilience by diversifying revenue beyond domestic transaction volumes for the India fintech market.

Competitive Landscape

The India fintech market shows moderate concentration as large platforms and well-capitalized providers consolidate share in payments, distribution, and embedded finance while leaving room for mid-tier specialists. Multi-bank UPI architectures and device-led merchant acceptance strengthen reliability and retention in payments franchises. Payment aggregators ship corporate cards, buyer protection, and conversational agents to expand monetization and reduce checkout drop-offs. Insurance distribution scale comes from aggregator-led partner networks and improved unit economics in health and term products. AA-driven consent frameworks enable lenders to compete on data-rich underwriting, compressing acquisition costs across retail and MSME cohorts.

Compliance readiness and capital buffers increasingly serve as competitive moats due to RBI directions for digital lending and payment aggregation in the India fintech market. Government incentives encourage adoption in small-ticket P2M transactions, which fuels traffic and drives the need for value-added services to offset zero-MDR. Platforms with broad product suites and device ecosystems can cross-sell with higher conversion, which improves revenue per user in the India fintech market. Aggregators continue to extend into export settlement and automated reconciliation, which modernize treasury operations for SMBs and mid-market firms. The Account Aggregator ecosystem’s limited number of licensed entities underscores the value of partner-ready compliance in data-driven products.

Select players executed notable strategic moves in 2025 that illustrate consolidation, product breadth, and governance readiness. One large platform divested non-core consumer verticals, shifted to a multi-bank UPI model, and highlighted faster settlement and reliability for merchants and users in the India fintech market. A major aggregator launched corporate cards, buyer protection guarantees, and an agentic AI toolkit that executes transactions inside chat, which reduces friction during checkout and post-purchase actions. BharatPe achieved profitability at the PBT level and secured RBI authorization as an online payment aggregator, which enhances its ability to scale acceptance with banks and regulated partners. Across these moves, players align to regulatory direction while expanding into stickier, higher-margin services in the India fintech market.

India Fintech Industry Leaders

Paytm (One97 Communications Ltd)

PhonePe Pvt Ltd

Razorpay Software Pvt Ltd

Pine Labs Pvt Ltd

PayU Payments Pvt Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Paytm completed the divestment of its movies and events business to Zomato, exited certain overseas rights in PayPay Corporation, and moved to a third-party UPI application provider model under a multi-bank arrangement with Axis Bank, HDFC Bank, SBI, and YES Bank.

- June 2025: Fintech startup Slice launched a UPI-linked credit card and opened its first physical bank branch in Bengaluru, signaling its entry into full-stack banking post-merger with North East Small Finance Bank. The “super card” integrates UPI payments with credit access, while the Koramangala branch emphasizes self-service, digital onboarding, and UPI-enabled ATMs, reflecting a hybrid banking model.

- March 2025: The Government announced a renewed UPI incentive program to support low-value P2M transactions, sustaining merchant adoption and small-ticket usage in semi-urban and rural districts.

- February 2025: Razorpay unveiled four product suites, including RazorpayX Corporate Cards with YES Bank, Buyer Protection, the RAY Agentic-AI Toolkit for in-chat transactions, and Engage Gift Cards. The company also launched the MoneySaver Export Account with zero FX markup and 24-hour settlements for exporters.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Indian fintech market as all technology-enabled payment, lending, investment, insurance, and digital banking services delivered directly to retail or business customers and operating under Indian financial-sector regulations.

Scope exclusion: Pure back-office IT outsourcing and generic enterprise software remain outside our boundary.

Segmentation Overview

- By Service Proposition

- Digital Payments

- Digital Lending and Financing

- Digital Investments

- Insurtech

- Neobanking

- By End-User

- Retail

- Businesses

- By User Interface

- Mobile Applications

- Web / Browser

- POS / IoT Devices

Detailed Research Methodology and Data Validation

Primary Research

We spoke with founders of payment gateways, compliance heads of mid-tier banks, retired RBI supervisors, and CFOs of digital lenders across Delhi, Mumbai, and Bengaluru. Online surveys with Gen Z users revealed neobank uptake curves, letting us refine acquisition costs and default assumptions.

Desk Research

Our analysts first compiled Reserve Bank payments bulletins, Ministry of Electronics & IT digital-public-infrastructure dashboards, NPCI UPI statistics, and Securities & Exchange Board circulars. They then complemented them with insights from trade bodies such as the Digital Lenders Association and Insurance Regulatory Development Authority. Foundational company indicators were gathered from D&B Hoovers, while funding and deal flow were tracked through Dow Jones Factiva and open investor presentations. These illustrative sources supply transaction volumes, user counts, and fee ranges; yet many other public documents also informed our work.

Market-Sizing & Forecasting

A calibrated top-down build starts with 2024 digital transaction value and credit outlay and is split by service proposition through observed share ratios and selective bottom-up cross-checks. Sampled active-user counts multiplied by typical annual revenue per user anchor our totals. Key variables include UPI volume growth, digital-lending disbursement, embedded-finance merchant count, smartphone penetration, and regulatory fee caps. Five-year projections use multivariate regression blended with scenario analysis to reflect policy shifts and funding elasticity. Gaps between sampled revenue and survey medians are smoothed by weighted averages.

Data Validation & Update Cycle

Outputs undergo dual analyst review, after which variance against external benchmarks and month-on-month NPCI data triggers recalculation. Reports refresh annually, and an interim sweep follows any material policy change so clients receive the freshest view.

Why Our India Fintech Baseline Commands Reliability

Published estimates often diverge because each firm chooses different service mixes, user-yield assumptions, currency conversion dates, and refresh frequencies. Mordor's disciplined scope definition and scheduled updates temper extremes and deliver a balanced midpoint.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 44.12 B (2025) | Mordor Intelligence | |

| USD 112.75 B (2024) | Regional Consultancy A | Counts enterprise IT platforms and gross payment throughput, inflating totals |

| USD 121.40 B (2024) | Global Consultancy B | Uses revenue multiples on funding data without transaction cross-checks |

| USD 155.67 B (2025) | Trade Journal C | Applies optimistic fee yields and omits RBI lending caps |

The comparison shows how wider scopes and generous yield multipliers can swell totals, whereas Mordor's stepwise variable selection and dual validation keep the baseline dependable for strategic decisions.

Key Questions Answered in the Report

What is the India fintech market size in 2026, and how fast will it grow by 2031?

The India fintech market size is USD 51.30 billion in 2026 and is projected to reach USD 109.06 billion by 2031 at a 16.27% CAGR.

Which service propositions lead and which are growing fastest in the India fintech market?

Digital payments lead with a 42.87% share in 2025, while neobanking records the fastest projected growth at a 19.64% CAGR from 2026 to 2031.

How important are mobile applications in channel adoption for the India fintech market?

Mobile applications command a 67.83% share in 2025 and also hold the fastest growth trajectory at 18.39%, supported by UPI Lite, biometrics, and app-first onboarding.

What are the main regulatory levers shaping the economics in the India fintech market?

RBI's digital lending directions and payment aggregator master direction increase compliance baselines and net worth thresholds, which push monetization toward value-added services and sustainable origination models.

Where is geographic growth strongest within the India fintech market?

Growth originates in metro and tier-1 centres but accelerates in tier-2 and tier-3 districts due to UPI incentives and Aadhaar-enabled e-KYC, while offline devices extend merchant acceptance.

What differentiates leading competitors in the India fintech market today?

Leading platforms combine multi-bank UPI reliability, device-led merchant acceptance, and value-added services like corporate cards and buyer protection, while maintaining a strong compliance posture and cross-sell breadth.

Page last updated on: