Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

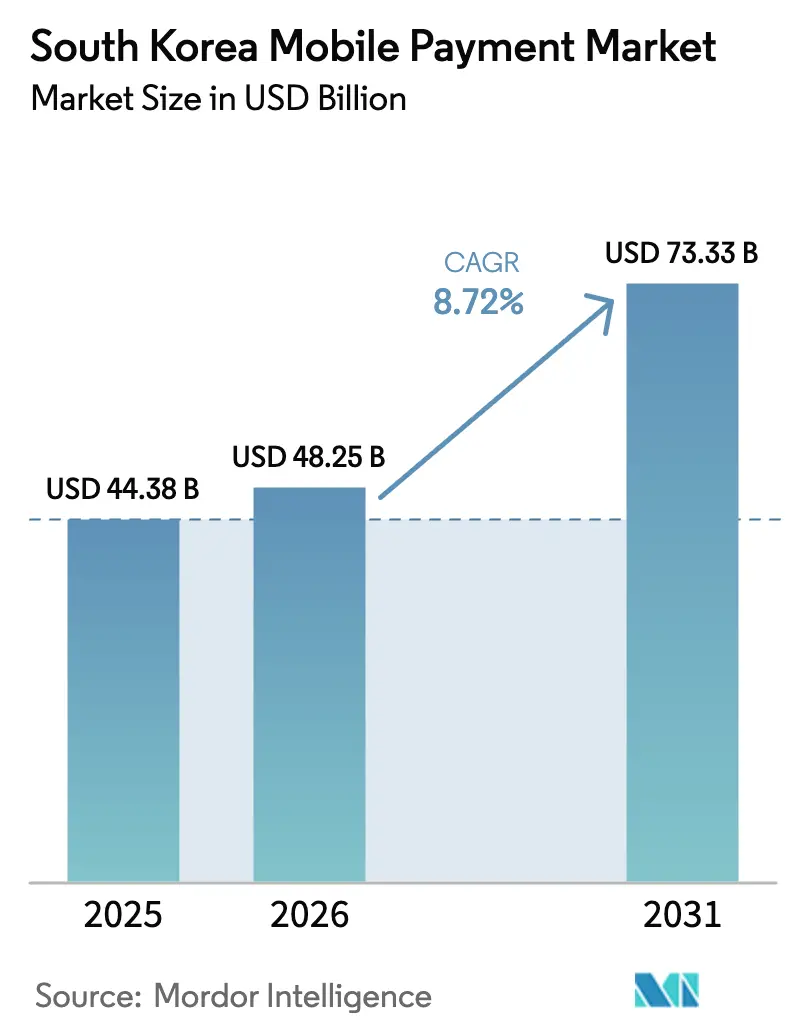

| Base Year Market Size (2025) | USD 44.38 Billion |

| Market Size (2026) | USD 48.25 Billion |

| Market Size (2031) | USD 73.33 Billion |

| Growth Rate (2026 - 2031) | 8.72% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Korea Mobile Payment Market Analysis by Mordor Intelligence

The South Korea mobile payment market size is expected to grow from USD 44.38 billion in 2025 to USD 48.25 billion in 2026 and is forecast to reach USD 73.33 billion by 2031 at 8.72% CAGR over 2026-2031. Structural change from card-centric purchasing to biometric-authenticated, super-app-embedded checkout continues as nationwide 5G coverage improves, interchange-fee caps favor QR-code rails, and proximity terminals reach quick-service outlets and mass-transit hubs. Samsung Pay’s retreat from Magnetic Secure Transmission (MST) toward tokenized NFC, combined with facial authentication, signals a broader pivot toward higher-security form factors. Super-apps Kakao Pay, Naver Pay, and Toss consolidate payments, mobility, and entertainment into single interfaces, pushing daily wallet transactions to 29.71 million in H1 2024. Government incentives, such as ZeroPay’s 0% merchant fees and VAT refunds, lower acceptance costs for micro-merchants, accelerating QR-code deployment in rural provinces.[1]ZeroPay Foundation, “Merchant Enrollment Dashboard,” zeropay.or.kr

Key Report Takeaways

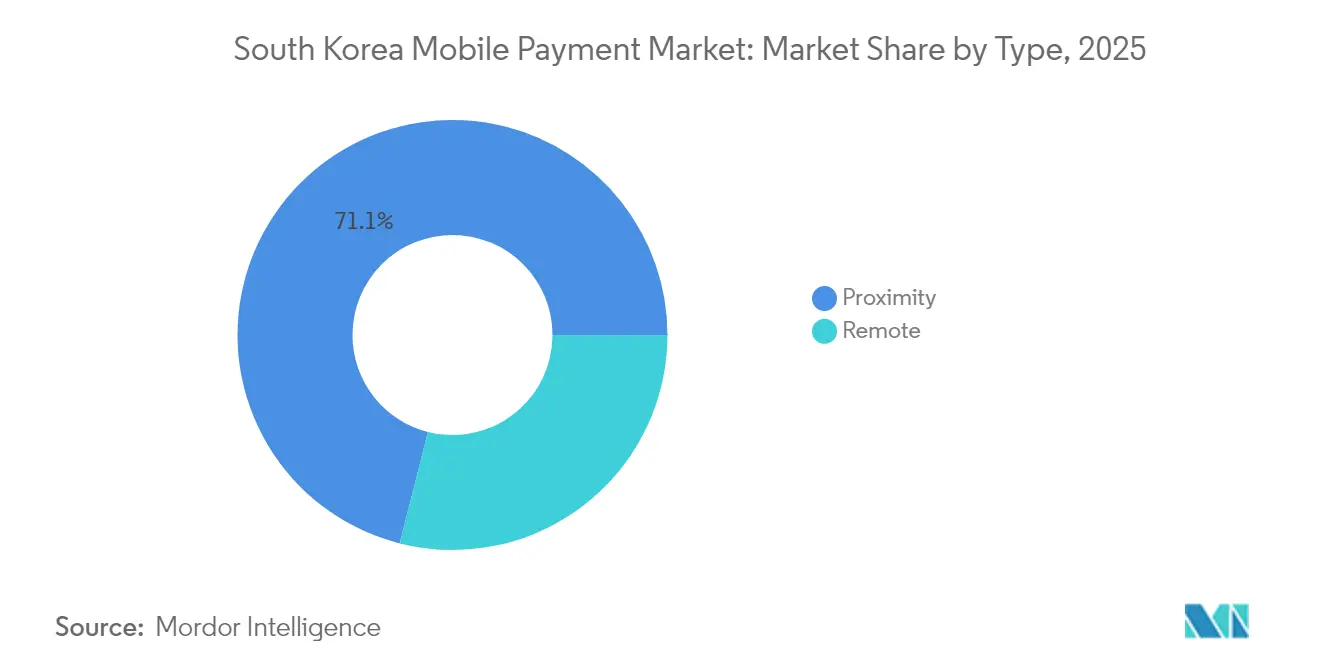

- By type, proximity payments accounted for 71.05% of the South Korea mobile payment market share in 2025, while the same segment is expanding at a 10.74% CAGR through 2031.

- By technology, NFC held 54.20% share of the South Korea mobile payment market size in 2025; QR-code payments are projected to grow at 10.21% CAGR to 2031.

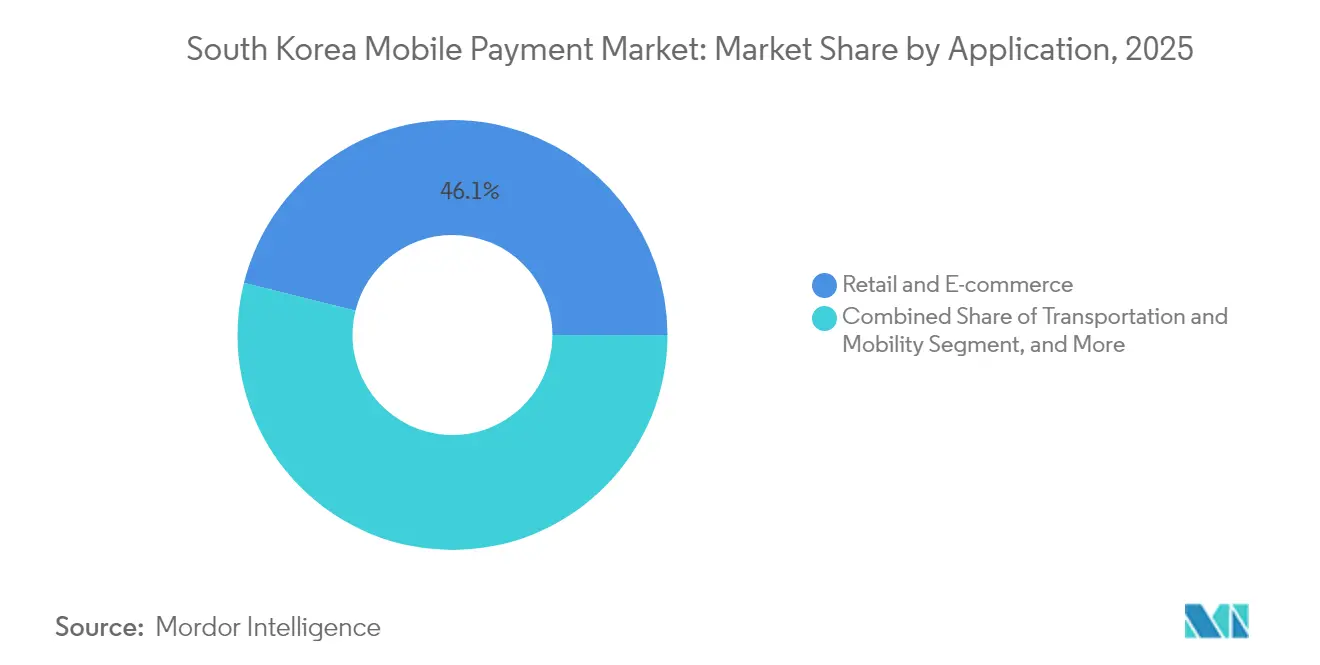

- By application, retail and e-commerce led with 46.10% revenue share in 2025; transportation and mobility is advancing at a 9.86% CAGR through 2031.

- By end-user, millennials and Gen-Z represented 58.05% of transaction volume in 2025, while enterprises and SMEs show the highest projected growth at 10.05% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

South Korea Mobile Payment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging 5G-enabled smartphone penetration | +2.1% | National, with early gains in Seoul Capital Area, Gyeonggi, Incheon | Short term (≤ 2 years) |

| E-commerce and quick-commerce boom | +1.8% | National, concentrated in Seoul Capital Area, Gyeonggi | Medium term (2-4 years) |

| Government incentives (ZeroPay VAT refunds, fee caps) | +1.5% | National, targeting SME-dense provinces (Chungcheong, Gyeongsang, Jeolla) | Medium term (2-4 years) |

| Super-app ecosystem integration (mobility, finance) | +1.9% | National, led by Seoul Capital Area, Gyeonggi | Long term (≥ 4 years) |

| Biometric authentication enabling high-ticket mobile payments | +1.3% | National, early adoption in Seoul Capital Area | Medium term (2-4 years) |

| Cross-border K-content micro-transactions | +0.7% | Global, with spillover to Asia-Pacific, North America, Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging 5G-Enabled Smartphone Penetration

5G subscriptions surpassed 35 million in 2024, covering 67% of mobile lines and providing the low-latency backbone necessary for biometric-secured proximity payments.[2]SK Telecom, “2024 5G Coverage Report,” sktelecom.com The bandwidth allows real-time fraud scoring in milliseconds, lowering chargebacks and encouraging merchants to accept high-value wallet transactions. Samsung Wallet’s 2024 integration of mobile driver’s licenses showcases how fast networks merge identity and payments into one tap. PASS consortium data shows that 45 million mobile IDs have been issued, turning phones into government-recognized credentials. Compliance with the Personal Information Protection Act forces end-to-end encryption, raising entry barriers for new wallets yet building consumer trust.

E-Commerce and Quick-Commerce Boom

Mobile commerce reached USD 101 billion in 2023 and is on track for USD 185.4 billion by 2028, outpacing GDP and routing traffic toward in-app wallets. Coupang’s Rocket Delivery guarantees sub-2-hour drop-offs, so Kakao Pay and Naver Pay are embedded directly in product pages for one-click checkout. Food-delivery aggregators Baemin and Yogiyo have extended wallet acceptance to 200,000 restaurants, and BNPL users are forecast to double to 17.3 million by 2028, easing friction from high-ticket purchases.

Government Incentives (ZeroPay VAT Refunds, Fee Caps)

ZeroPay enrolled 1.2 million merchants by mid-2024, promising 0% transaction fees and 40% income-tax deductions for small businesses. Interchange caps at 0.5% for small sellers shrink issuer margins but democratize acceptance. The differential explains QR-code volumes growing faster than NFC, especially for low-ticket street-food and traditional-market transactions.[3]Financial Services Commission, “Interchange-Fee Cap Guidelines,” fsc.go.kr Automated VAT refunds through wallets further lighten administrative load for SME owners in rural provinces.

Super-App Ecosystem Integration

Kakao Pay processed KRW 167.3 trillion in payments in Q4 2024 by integrating ride-hailing, parking, and insurance services within its app. Naver Pay logged KRW 22.7 trillion in Q3 2025, boosted by Naver Webtoon’s 160 million monthly users who pay for digital comics and micropayments. Toss blends payment, brokerage, and crypto trading for 9.5 million users, enabling instant movement of investment gains into retail spend. These bundled services lock users in, raising friction for multi-homing.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising cyber-fraud sophistication | -1.2% | National, with higher incidence in Seoul Capital Area due to transaction density | Short term (≤ 2 years) |

| Regulatory interchange-fee caps squeezing margins | -1.0% | National, acute pressure on card issuers (Shinhan, KB, Hana) | Medium term (2-4 years) |

| Demographic digital divide among seniors | -0.8% | National, concentrated in Gangwon, Jeju, rural Jeolla provinces | Long term (≥ 4 years) |

| Domestic market saturation limiting transaction-growth headroom | -0.9% | National, most pronounced in Seoul Capital Area, Gyeonggi | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Cyber-Fraud Sophistication

Phishing, SIM-swap, and deepfake voice scams climbed in 2024, leading the Financial Security Institute to mandate real-time anomaly detection and multi-factor checks for all wallets. Kakao Pay’s 2024 privacy inquiry heightened scrutiny on data-sharing practices. Platforms now assume liability for reimbursing fraud victims within 30 days, tightening margins for thin-capitalized fintechs. Behavioral biometrics countermeasures raise operational costs that only scale players can absorb.

Regulatory Interchange-Fee Caps Squeezing Margins

Caps of 0.5% for small merchants and 1.0% for mid-sized retailers removed KRW 1.2 trillion in issuer revenue in 2024. Card brands cut NFC terminal subsidies, accelerating the pivot to QR-code rails among street vendors. Fintechs that monetize through lending or insurance cope better with compressed payment yields, but smaller issuers face consolidation pressure as the Financial Services Commission signals deeper cuts in 2025.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Proximity Dominance Fueled by Transit Integration

Proximity payments controlled 71.05% of the South Korea mobile payment market in 2025 and will expand at 10.74% CAGR to 2031, buoyed by Seoul Metro’s smartphone-tap turnstiles and the 50,000 quick-service outlets that now accept contactless transactions. The South Korea mobile payment market size for proximity channels is therefore scaling faster than remote methods, whose mobile-browser checkout abandonment remains above 25%.

Remote payments still matter for cross-border and subscription use cases but lose share as super-apps auto-populate credentials inside native environments. Samsung Pay’s sunsetting of MST clarifies market direction toward EMV-grade NFC and biometrics, with luxury merchants recording average mobile tickets of KRW 500,000 in 2024.

By Technology: QR-Code Gains Ground on Fee Arbitrage

NFC retained 54.20% South Korea mobile payment market share in 2025, yet QR-code volumes are pacing at 10.21% CAGR on the back of ZeroPay’s free-to-merchant model. The South Korea mobile payment market size tied to QR acceptance is especially strong among micro-merchants that cannot fund NFC terminals.

Daily wallet transactions reached 29.71 million in H1 2024, with QR usage high in traditional markets, while NFC dominates high-value retail, where EMV tokenization cuts fraud. Samsung Wallet’s biometric NFC and the FSC’s plan for a single national QR standard illustrate a convergence path, though competing specs keep universal acceptance on hold.

By Application: Transportation Surges as Mobility Integrates

Retail and e-commerce led with 46.10% share in 2025, yet transportation and mobility display the fastest 9.86% CAGR, driven by Kakao Mobility rides, Seoul Metro taps, and parking-fee wallets. As a result, the South Korea mobile payment market size tied to commuting is catching up with retail.

Quick-service food, digital content, and gaming segments deepen wallet penetration by embedding one-click flows that trim cart abandonment by 18% versus credit cards. Municipalities are now piloting wallet payments for taxes and fines, hinting at a next leg of institutional adoption.

By End-User Segment: Enterprises Accelerate B2B Adoption

Millennials and Gen-Z generated 58.05% of 2025 transaction volume, but enterprises and SMEs post the highest 10.05% CAGR after Visa and KOTRA rolled out real-time export settlements. Consequently, the South Korea mobile payment market size for B2B flows is expanding faster than the consumer base.

Integrate Business and Kakao Pay for Business plug wallets into payroll and invoice systems, providing instant visibility into cash positions. Senior adoption remains limited, yet government-sponsored tutorials and larger-font interfaces are helping to close the gap.

Geography Analysis

The Seoul Capital Area generates over 50% of the transaction value, thanks to a 90% smartphone penetration rate and an early 5G rollout. Kakao Pay and Naver Pay derive 65% of their volumes from this region, utilizing it as a live lab for features such as face authentication and mobile IDs. Seoul Metro’s wallet-ready turnstiles act as an onboarding funnel for new users every rush hour.

Incheon’s Songdo business district pilots Alipay+ interoperability, allowing Chinese tourists to scan the same code at duty-free stores, resulting in KRW 450 billion in cross-border spending in 1H 2024. Gyeonggi’s factory belts push B2B wallet settlements through Visa’s KOTRA platform for just-in-time component payments. Chungcheong, Gyeongsang, and Jeolla provinces leverage ZeroPay to leapfrog card terminals in traditional markets.

Jeju and Gangwon lag due to aging populations, but tourism creates niche wallet use cases such as wearable wristbands at ski resorts and duty-free shops. Kakao Pay reports Jeju’s cross-border wallet spend jumped 28% year-over-year in 2024, reflecting rising tourist traffic.

Competitive Landscape

The top four providers, Kakao Pay, Naver Pay, Samsung Pay, and Toss, command most of the transaction volume, leaving 25% to 21 smaller wallets, so the South Korean mobile payment market remains moderately concentrated. Super-apps gain stickiness by bundling finance, mobility, and content, while card issuers such as Shinhan and KB integrate their rails into third-party apps to remain visible.

Retail-backed wallets, such as Coupang Rocket Pay and SSG Pay, leverage first-party data to offer personalized cashback, effectively turning payments into retention levers. Start-ups, including Karrot Pay and Yanolja Pay, focus on vertical niches such as second-hand goods and travel bookings. Samsung’s 2024 biometric card patents hedge against device concentration by moving fingerprint sensors onto EMV cards, creating a device-agnostic fallback.

Regulatory oversight from the Financial Services Commission ensures fee transparency and interoperability, which raises compliance costs that favor capital-rich incumbents. White-space lies in cross-border remittances, wholesale tokenization pilots under BIS Project Agora, and Web3-based micropayments.

South Korea Mobile Payment Industry Leaders

Kakao Pay

Naver Corporation ( Naver Pay)

Samsung Electronics (Samsung Pay)

Viva Republica Co., Ltd. (Toss Payments)

NHN PAYCO Corp. (PAYCO)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Visa and SK Telecom launched an eSIM-based tokenized mobile wallet for connected cars, allowing drivers of Hyundai’s 2026 models to authorize fuel, toll, and parking payments directly from the in-vehicle dashboard.

- July 2025: Kakao Pay agreed to acquire BNPL specialist Finnq for KRW 620 billion (USD 470 million), aiming to integrate installment financing into its super-app and expand credit services to younger consumers and SMEs.

- April 2025: Samsung Electronics and Shinhan Bank began a closed-loop pilot of biometric payment cards that embed fingerprint sensors within EMV chips, enabling contactless transactions without a smartphone at 500 Seoul retail locations.

- January 2025: The Financial Services Commission issued the final technical specification for a unified national QR-code standard, mandating compatibility across Kakao Pay, Naver Pay, Toss, and card-issuer wallets to streamline merchant acceptance.

South Korea Mobile Payment Market Report Scope

The South Korea mobile payment market report is segmented by Type (Proximity, and Remote), Technology (NFC, QR-Code, MST, Tokenised Card and Other Technology), Application (Retail and E-commerce, Food and Quick-Service Delivery, Transportation and Mobility, Entertainment and Digital Content, Utilities and Government Payments), End-User Segment (Millennials and Gen-Z Consumers, Gen-X Consumers, Baby-Boomer Consumers, Enterprises and SMEs). Market Forecasts are Provided in Terms of Value (USD).

By Type

| Proximity |

| Remote |

By Technology

| NFC (Near-Field Communication) |

| QR-Code |

| MST (Magnetic Secure Transmission) |

| Tokenised Card and Other Technology |

By Application

| Retail and E-commerce |

| Food and Quick-Service Delivery |

| Transportation and Mobility |

| Entertainment and Digital Content |

| Utilities and Government Payments |

By End-User Segment

| Millennials and Gen-Z Consumers |

| Gen-X Consumers |

| Baby-Boomer Consumers |

| Enterprises and SMEs (B2B Mobile Pay) |

| By Type | Proximity |

| Remote | |

| By Technology | NFC (Near-Field Communication) |

| QR-Code | |

| MST (Magnetic Secure Transmission) | |

| Tokenised Card and Other Technology | |

| By Application | Retail and E-commerce |

| Food and Quick-Service Delivery | |

| Transportation and Mobility | |

| Entertainment and Digital Content | |

| Utilities and Government Payments | |

| By End-User Segment | Millennials and Gen-Z Consumers |

| Gen-X Consumers | |

| Baby-Boomer Consumers | |

| Enterprises and SMEs (B2B Mobile Pay) |

Key Questions Answered in the Report

What is the current value of the South Korea mobile payment market?

The market is valued at USD 48.25 billion in 2026.

How fast is the sector growing?

It is forecast to expand at a 8.72% CAGR through 2031.

Which payment type holds the largest share?

Proximity payments, with 71.05% share in 2025.

Why are QR-code payments expanding quickly?

ZeroPay’s 0% merchant fees and low hardware costs drive adoption among micro-merchants.

Which region records the highest transaction volume?

The Seoul Capital Area contributes more than half of national wallet transaction value.

Page last updated on: