Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

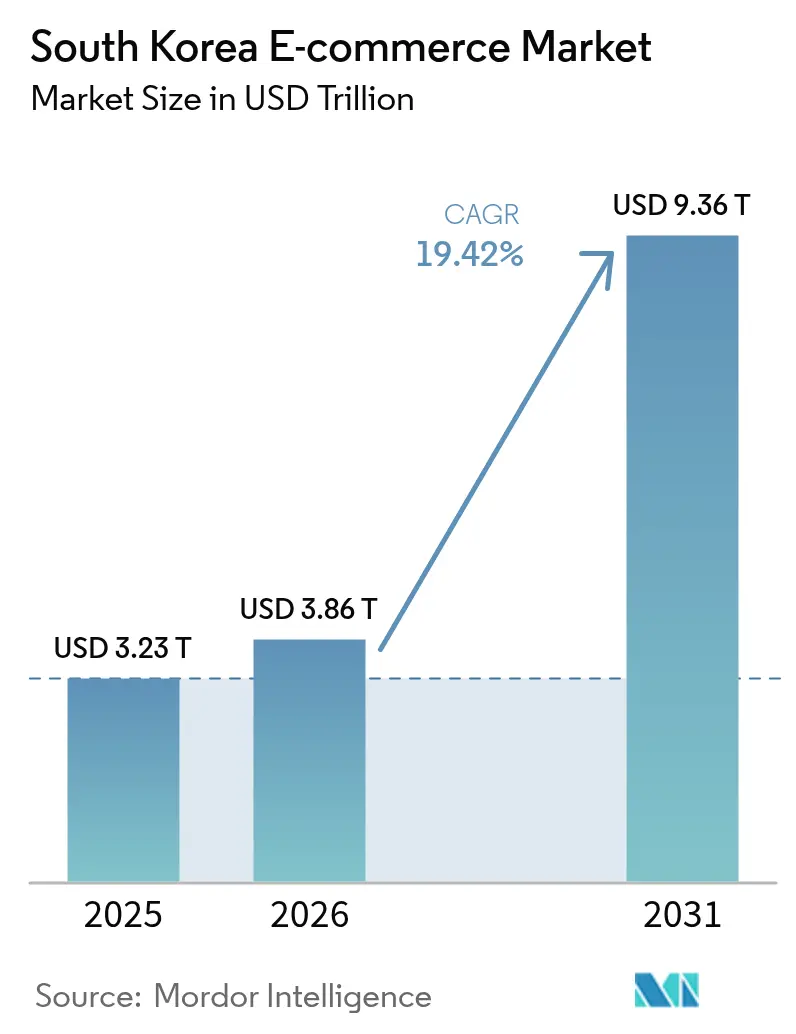

| Base Year Market Size (2025) | USD 3.23 Trillion |

| Market Size (2026) | USD 3.86 Trillion |

| Market Size (2031) | USD 9.36 Trillion |

| Growth Rate (2026 - 2031) | 19.42% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Korea E-commerce Market Analysis by Mordor Intelligence

The South Korea E-commerce Market size was valued at USD 3.23 trillion in 2025 and estimated to grow from USD 3.86 trillion in 2026 to reach USD 9.36 trillion by 2031, at a CAGR of 19.42% during the forecast period (2026-2031). This almost three-fold growth underscores the country’s status as a digital commerce powerhouse anchored by 96% internet penetration and one of the world’s highest smartphone ownership rates.[1]Ministry of Science and ICT, “Digital New Deal Press Releases,” msit.go.kr Logistics innovation, government-backed digital programs and the proliferation of mobile-only super-apps are widening the addressable consumer base and raising service expectations, especially in dense urban corridors. Intensifying competition from Chinese marketplaces, expanding BNPL adoption and rising cross-border demand for Korean beauty and grocery staples are reshaping platform strategies. Meanwhile, surging fulfillment costs, stricter data-localization rules and occasional delivery-worker labor actions highlight the operational risks that leading platforms must navigate.

Key Report Takeaways

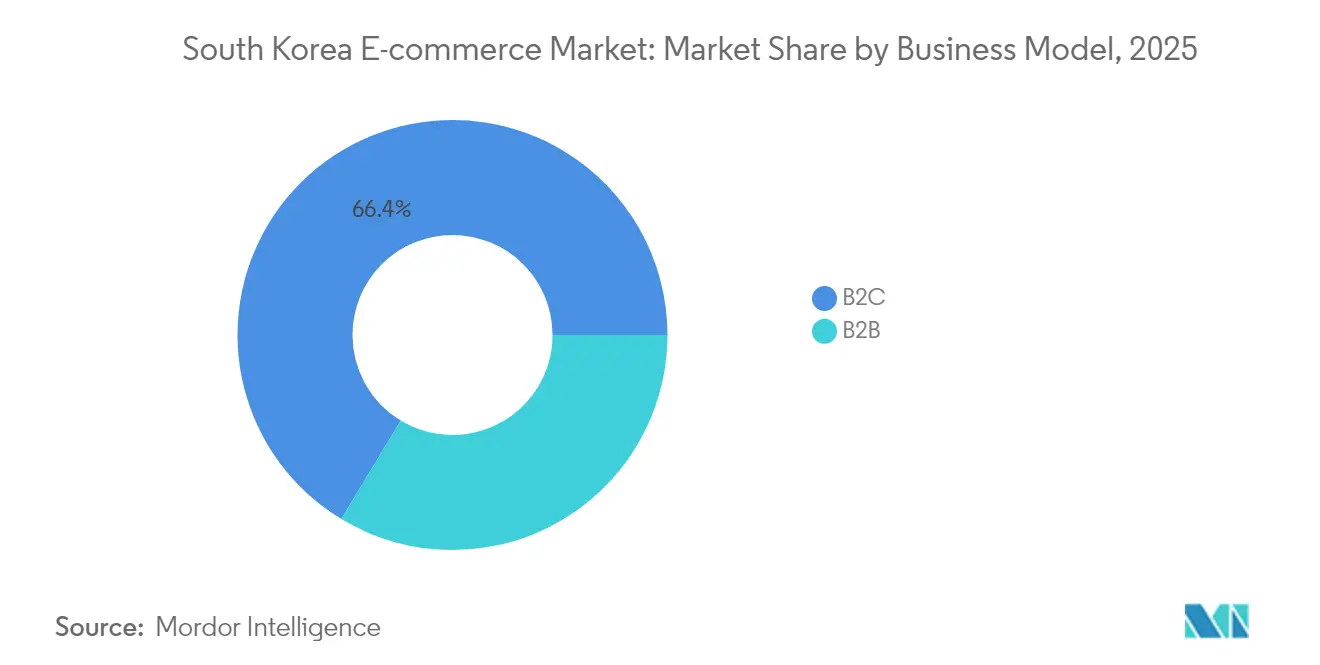

- By business model, the B2C segment held 66.35% of the South Korean e-commerce market share in 2025, while B2B is forecast to grow at a 23.45% CAGR to 2031.

- By device type, smartphones accounted for 73.40% of transactions in 2025; the “other devices” class, covering smart speakers, connected appliances, and AR/VR hardware, is expanding at a 31.10% CAGR through 2031.

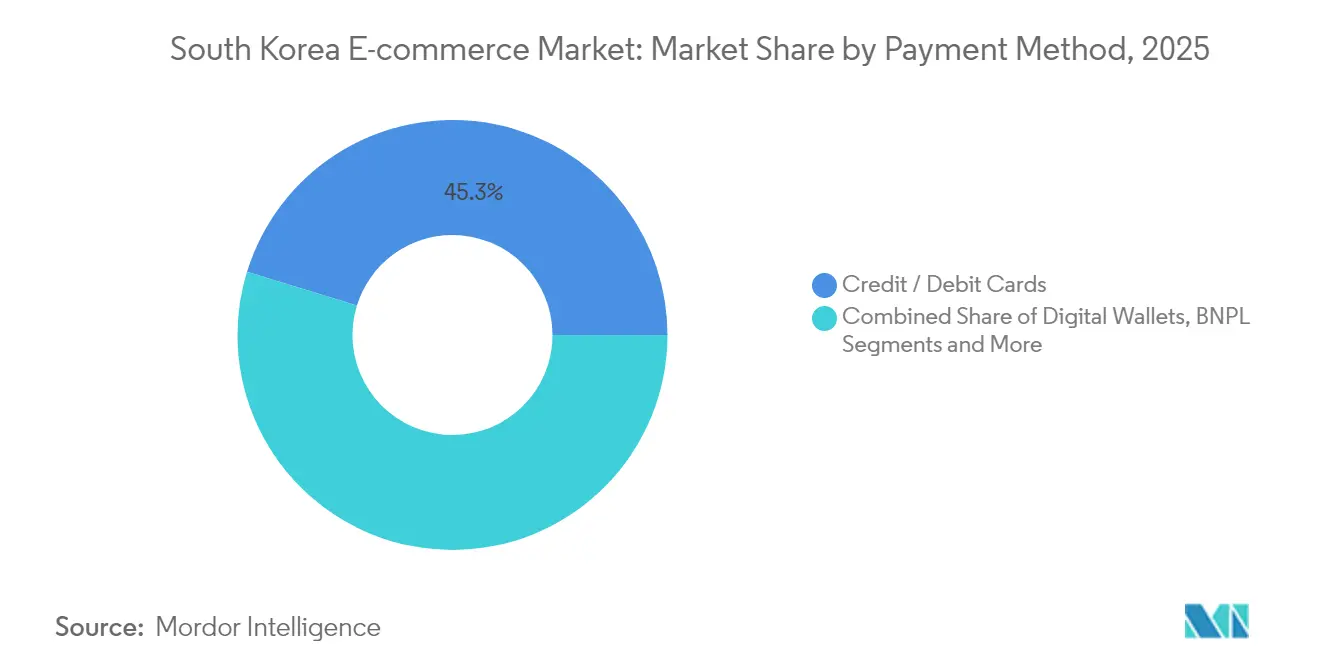

- By payment method, credit and debit cards dominated with 45.25% share in 2025, whereas BNPL is set to surge at a 33.00% CAGR, reaching USD 9.12 billion by 2031.

- By B2C product category, consumer electronics led with 20.60% share in 2025; food & beverages is forecast to advance at a 27.30% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

South Korea E-commerce Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Soaring Same-day & Dawn-delivery Expectations among Seoul-metro Consumers | + 5.5% | Seoul metropolitan area, with spillover to Busan and other major cities | Short term (≤ 2 years) |

| Social-commerce Boom Fueled by Naver LIVE & TikTok Shop Integration | + 4.2% | National, with concentration in urban centers | Medium term (2-4 years) |

| Rapid Expansion of Mobile-only 'Super-apps' | + 3.8% | National, with higher adoption among 20-39 age demographic | Medium term (2-4 years) |

| Government-backed Smart-Logistics Hubs Drives the Market | + 3.1% | National, with concentration in logistics corridors near Seoul, Incheon, and Busan | Long term (≥ 4 years) |

| Aging-society Demand for Quick-commerce of Rx-less Health Products | + 2.7% | National, with higher impact in regions with larger elderly populations | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Soaring Same-day & Dawn-delivery Expectations among Seoul-metro Consumers

Rapid normalization of ultra-fast delivery has reframed online shopping behavior; 44.3% of Korean shoppers now rank speed as the top buying criterion. Coupang’s Rocket Delivery sets the pace with same-day fulfillment covering 70% of residents, prompting rivals such as CJ OnStyle and NS Home Shopping to slash cut-off windows to match. Dense population clusters in Seoul enable cost-efficient route density, encouraging fulfillment centers within 7 miles of most households. Competitive logistics spending is accelerating automation, while the ripple effect of metropolitan benchmarks is pushing next-tier cities to raise service standards.

Social-commerce Boom Fueled by Naver LIVE & TikTok Shop Integration

Live-stream retail is forecast to capture one-fifth of online revenue by 2025 as browsing shifts from keyword search to content-led discovery. Naver’s “Discovery” tab merges short-form video with one-click checkout, vital for fashion and beauty where impulse purchases thrive. Livestream conversion rates exceed static listings, and 60% of Koreans have already bought through live shopping formats. Early-mover brands leverage influencer partnerships to shorten the trust gap, while platforms monetize engagement through tipped commissions and advertising slots.

Rapid Expansion of Mobile-only ‘Super-apps’

Kakao, Naver and Coupang are stitching social, payment, entertainment and logistics into unified ecosystems that deepen user stickiness. Super-app shoppers transact 2.3x more frequently than single-purpose users, pushing mobile commerce toward a projected 77% share of online spending by 2026. Seamless cross-service identity management lets platforms exploit data moats for hyper-personalized offers. Regulatory scrutiny is rising but the ability to cross-subsidize new verticals continues to elevate barriers for late entrants.

Government-backed Smart-Logistics Hubs Drive the Market

The National Logistics Basic Plan and Digital New Deal funnel KRW 58.2 trillion into automation and urban logistics hubs through 2025. Certified smart-logistics centers receive incentives to deploy AI routing, high-density storage and low-emission vehicles that collectively cut turnaround times and carbon footprints. Policy alignment with infrastructure spending stimulates private co-investment, reinforcing the physical backbone essential for next-hour delivery commitments.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-localization Mandates Raising Compliance Costs | -2.1% | National, with particular impact on international platforms | Medium term (2-4 years) |

| Saturated Urban Customer-Acquisition Costs Outpacing AOV Growth | -1.8% | Seoul, Busan, and other major urban centers | Short term (≤ 2 years) |

| Cross-border Customs Delays on K-beauty Returns | -1.5% | Global, with particular impact on North American and European markets | Medium term (2-4 years) |

| Delivery-worker Labor Actions Affecting Last-mile Capacity | -1.2% | National, with concentration in urban delivery networks | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Data-localization Mandates Raising Compliance Costs

Domestic storage and explicit transfer consent requirements elevate cloud and cybersecurity spending by up to 55% for platforms that previously centralized data abroad. Smaller foreign marketplaces face disproportionate burdens, dampening competitive intensity and potentially slowing feature rollouts reliant on global SaaS stacks.

Saturated Urban Customer-Acquisition Costs Outpacing AOV Growth

Post-pandemic demand normalization slashed nationwide e-commerce growth from nearly 20% to 6.6% in 2024, yet ad rates in metro Seoul surged 35-40%. Conversion lags relative to rising bid prices have forced cost-discipline pivots; large platforms are re-routing budgets to loyalty programs and exploring offshore expansion to restore ROI.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Business Model: B2B Segment Outpaces Consumer Market

The South Korean e-commerce market size for B2C transactions stood at 66.35% share in 2025, powered by Coupang’s USD 22.4 billion revenue engine and Naver’s marketplace breadth. Robust consumer logistics and entrenched mobile habits anchor B2C leadership, yet procurement digitalization is pivoting B2B from niche to growth driver. Venture investment totaling USD 79.7 million across 35 start-ups signals capital confidence, and marketplaces such as EC21 and Trade Korea expand catalog depth for industrial buyers.

Digital invoicing and government-backed uTradeHub further compress paperwork cycles, encouraging manufacturing SMEs to shift routine ordering online. As B2B adoption gears up, the segment’s 23.45% CAGR exceeds the overall South Korean e-commerce market size trajectory, hinting at value-chain realignment where distributors increasingly rely on virtual storefronts for lead generation.

By Device Type: Emerging Technologies Disrupt Mobile Dominance

Smartphones generated 73.40% of 2025 transaction value, cementing their role as the core interface of the South Korean e-commerce market. App-centric design, biometric payment security and push-notification marketing drive weekly purchase rates more than 14 percentage points above the global average. Still, the “other devices” cluster smart speakers, smart TVs and AR/VR headsets advances at a 31.10% CAGR, spurred by Samsung’s connected-home ecosystem and retailers’ voice-ordering APIs.

Desktop workflows persist in corporate procurement and high-consideration consumer segments, but omnichannel authentication enables shoppers to juggle research and checkout across screens. Platforms increasingly optimize session continuity rather than individual device funnels, reducing friction when a user adds an item via smart fridge and completes payment on mobile. The trend redefines UI priorities from screen-specific tailoring to data fabric uniting every endpoint.

By Payment Method: BNPL Disrupts Traditional Payment Dominance

Cards remained the staple, handling 45.25% of 2025 online spend, reflecting mature credit infrastructure and loyalty integration with super-apps. BNPL’s 33.00% CAGR, however, positions it as the payment method to watch; Naver Financial, Toss Bank and Hyundai Card extend interest-free splits to diversify younger consumer inflows. The Financial Services Commission now mandates suitability checks and clearer fee disclosure, introducing credit-like oversight to the nascent category.

Digital wallets such as Samsung Pay ride NFC ubiquity and super-app integration, holding 42% share within mobile wallet payments. Back-end tokenization, combined with single-sign-on protocols, boosts checkout velocity and lowers abandonment, ensuring wallets remain integral even as BNPL heads up-market into higher-ticket baskets.

By B2C Product Category: Food & Beverages Leads Growth Revolution

Consumer electronics retained a 20.60% share in 2025, but fresh and packaged food is rewriting growth charts with a 27.30% CAGR. Kurly’s dawn-delivery model illustrates margin potential when perishables meet precisely timed fulfillment. A 30% share of online sales now comes from grocery and meal kit baskets, steering logistics investment toward cold-chain capabilities.

Beauty & personal care leverages K-beauty’s global resonance; brands use livestream tutorials to demonstrate application techniques, smoothing conversion across borders. Fashion marketplaces pivot to re-commerce, evidenced by Naver’s USD 1.2 billion Poshmark acquisition aimed at global closet-clean-out trends. Furniture, once hindered by tactile hesitancy, benefits from AR visualization tools, shrinking return rates and supporting upselling of décor accessories triggered by virtual room scans.

Geography Analysis

Seoul’s metropolitan corridor accounts for 44.50% of national online turnover, enabled by dense fulfillment grids that compress last-mile distances and justify premium same-day surcharges. The South Korean e-commerce market thrives on this urban nucleus where disposable income and mobile adoption converge. Busan and Incheon trail yet show outsized momentum as smart-logistics hubs come online under government certification programs.

Cross-border activity has intensified, with Korean shoppers spending USD 3.1 billion on Chinese platforms in 2024, registering an 84% jump year-on-year. Price-competitive electronics and fashion imports enjoy rapid customs clearance via enhanced airfreight lanes at Incheon, although domestic players lobby for reciprocity on data-localization grounds. Accelerating overseas expansions by Korean titans offset domestic saturation; Coupang’s Taiwanese arm grew SKU count fivefold in early 2025, validating replication of Rocket Delivery abroad.

Rural penetration, though lower, is benefiting from drone-trial pilots and automated parcel lockers at convenience stores. Government subsidies for broadband in remote counties extend addressable demand, progressively diluting the urban-rural service gap that historically limited same-day feasibility outside major cities.

Competitive Landscape

Market leadership coalesces around Coupang and Naver, whose combined 42% stake delivers scale advantages in logistics and data analytics. Coupang’s vertically integrated model maximizes control of inventory and fulfillment, driving 90% of sales through owned stock and sustaining its Rocket WOW loyalty program. Naver prefers an asset-light marketplace approach, earning commission revenue while leveraging search dominance and AI recommendation engines to deepen basket size.

Specialist challengers carve durable niches: Kurly targets premium grocery, Musinsa anchors youth fashion and Oasis Corp. eyes value grocery segments through proposed 11Street acquisition. Their category focus safeguards differentiation against sprawling super-app rivals.

Chinese entrants elevate pricing pressure; AliExpress and Temu exploit supply-side economies to undercut domestic listings, compelling Korean incumbents to accelerate private-label sourcing and cross-border seller recruitment. Rumors of a Shinsegae-Alibaba logistics venture suggest mounting interest in pooling physical assets to match Coupang’s delivery promise. Strategic M&A, exemplified by Coupang’s USD 500 million Farfetch purchase, highlights a sharpening pivot toward high-margin luxury inventory.

South Korea E-commerce Industry Leaders

Coupang Corp.

Naver Shopping

eBay Inc.

Amazon.com Inc.

EMart

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Kurly Inc. reported its first-ever quarterly profit, marking a milestone for dawn-delivery grocery models KED Global.

- May 2025: Coupang’s Q1 2025 revenue reached USD 7.9 billion, up 11.1% year-on-year, buoyed by Taiwanese operations and Coupang Eats KED Global.

- April 2025: Naver confirmed an AI-driven shopping app featuring a Discovery tab for content-led browsing Retail Talk.

- March 2025: Naver unveiled faster delivery options, including same-day and next-day fulfillment MK News.

South Korea E-commerce Market Report Scope

E-commerce refers to selling clothing, electronics, furniture, books, cosmetics, and other items over the Internet. Companies that provide home delivery services, such as e-commerce and m-commerce, are included in this industry. Retailers and their consumers conduct sales transactions using information technology, such as the telephone and the Internet, and merchandise is often delivered via mail or courier. Direct mailers that sell their merchandise and retail through online websites are also included in the e-commerce industry.

The e-commerce market for the study defines the revenues generated from B2C e-commerce and B2B e-commerce in South Korea. The study is segmented by type (B2C e-commerce {application [beauty and personal care, consumer electronics, fashion and apparel, food and beverages, furniture and home, and other applications]}, and B2B e-commerce). The market sizes and forecasts are provided in terms of value in USD billion for all the segments. The analysis is based on the market insights captured through secondary research and the primaries. The report tracks key market parameters, underlying growth influencers, and major vendors operating in the industry, which supports market estimations and growth rates over the forecast period. The market sizes and forecasts are provided in terms of value (USD) for all the segments.

By Business Model

| B2C |

| B2B |

By Device Type

| Smartphone / Mobile |

| Desktop and Laptop |

| Other Device Types |

By Payment Method

| Credit / Debit Cards |

| Digital Wallets |

| BNPL |

| Other Payment Method |

By B2C Product Category

| Beauty and Personal Care |

| Consumer Electronics |

| Fashion and Apparel |

| Food and Beverages |

| Furniture and Home |

| Toys, DIY and Media |

| Other Product Categories |

| By Business Model | B2C |

| B2B | |

| By Device Type | Smartphone / Mobile |

| Desktop and Laptop | |

| Other Device Types | |

| By Payment Method | Credit / Debit Cards |

| Digital Wallets | |

| BNPL | |

| Other Payment Method | |

| By B2C Product Category | Beauty and Personal Care |

| Consumer Electronics | |

| Fashion and Apparel | |

| Food and Beverages | |

| Furniture and Home | |

| Toys, DIY and Media | |

| Other Product Categories |

Key Questions Answered in the Report

What is driving the rapid growth of the South Korean e-commerce market?

Exceptional digital infrastructure, aggressive same-day logistics, super-app ecosystems and rising cross-border activity underpin a 19.42% CAGR outlook.

Which business model is expanding fastest within Korean online retail?

The B2B segment is projected to grow at 23.45% annually through 2031 as manufacturers digitize procurement.

How significant is BNPL in South Korea?

BNPL is the fastest-growing payment method, heading toward USD 9.12 billion by 2031 on a 33.00% CAGR.

Why are food and beverages surging online?

Dawn-delivery pioneers such as Kurly pair cold-chain logistics with fresh-produce demand, propelling the category at a 27.30% CAGR.

How big is mobile’s share of Korean e-commerce?

Smartphones accounted for 73.40% of transactions in 2025, and mobile commerce is projected to reach 76.10% share by 2026.

What risks could slow e-commerce momentum?

Data-localization compliance costs, soaring customer acquisition expenses and periodic delivery-worker labor actions collectively shave over 5% off potential long-term CAGR.

Page last updated on: