South Korea Integrated Circuits Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

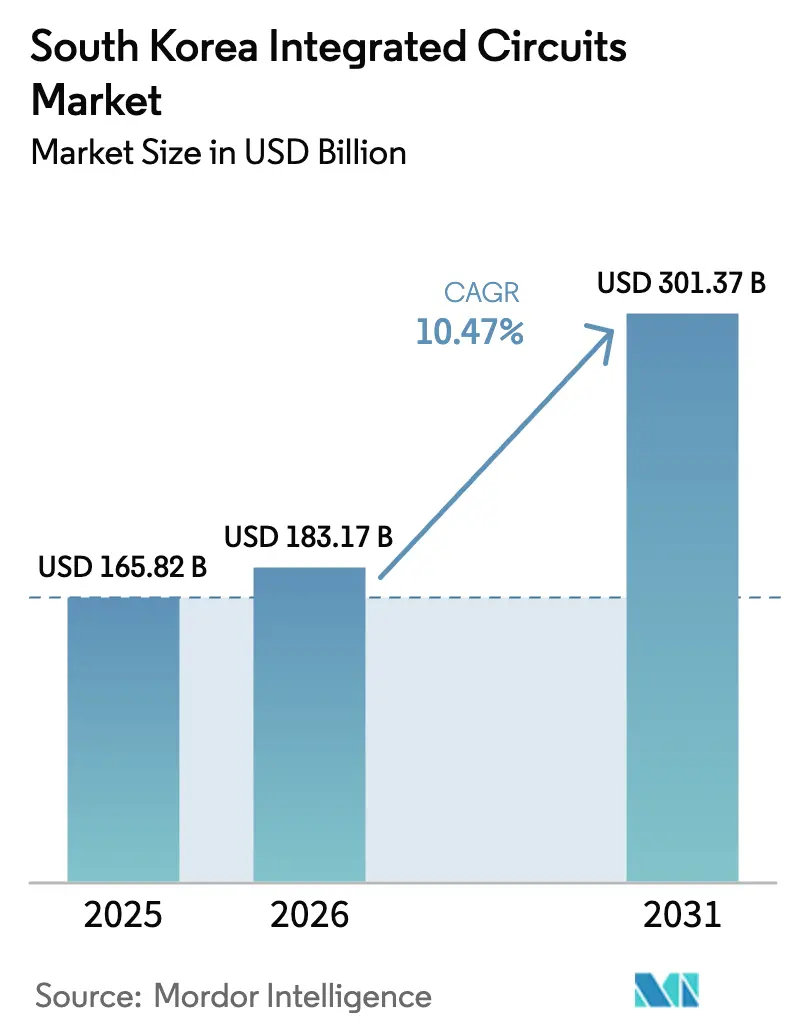

| Base Year Market Size (2025) | USD 165.82 Billion |

| Market Size (2026) | USD 183.17 Billion |

| Market Size (2031) | USD 301.37 Billion |

| Growth Rate (2026 - 2031) | 10.47% CAGR |

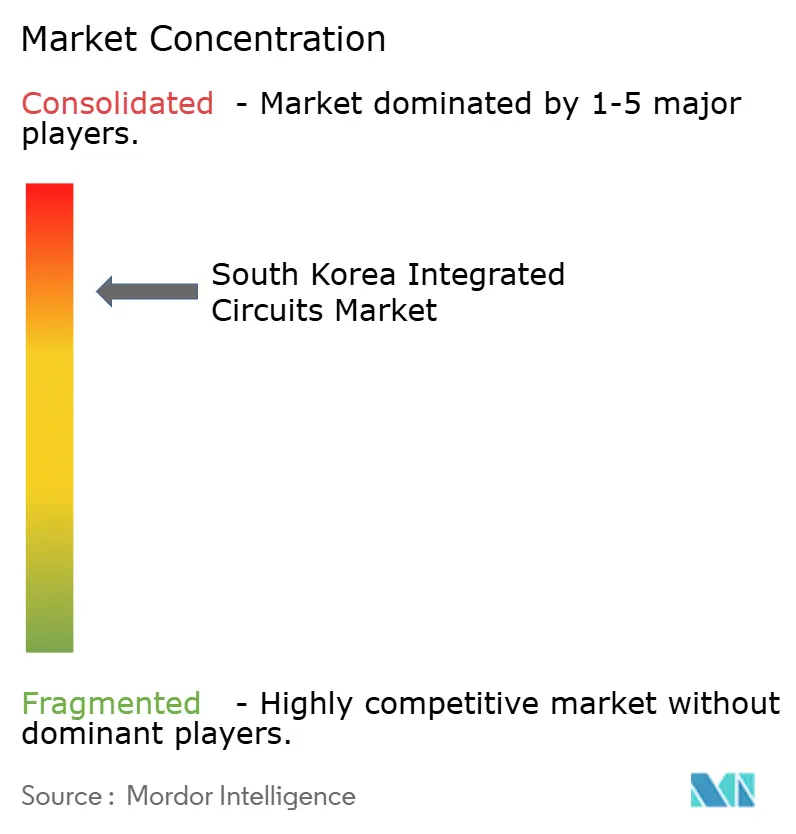

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Korea Integrated Circuits Market Analysis by Mordor Intelligence

The South Korea integrated circuits market size was valued at USD 165.82 billion in 2025 and estimated to grow from USD 183.17 billion in 2026 to reach USD 301.37 billion by 2031, at a CAGR of 10.47% during the forecast period (2026-2031). Strong AI infrastructure spending, the government’s K-Semiconductor Belt program, and domestic leadership in high-bandwidth memory (HBM) underpin this trajectory. Rising logic and system-on-chip demand, driven by Samsung Foundry’s 3 nm and 2 nm nodes, complements the entrenched memory base and keeps the South Korean integrated circuits market tightly linked to global technology cycles. Surging orders from U.S. cloud providers, accelerated adoption in electric vehicles, and government incentives that cover up to 50% of R&D spending further reinforce domestic capacity expansion. Meanwhile, geopolitically motivated supply-chain localization and selective allocation of scarce HBM capacity have created pricing power for SK Hynix and Samsung Electronics, bolstering profitability in the South Korean integrated circuits market.

Key Report Takeaways

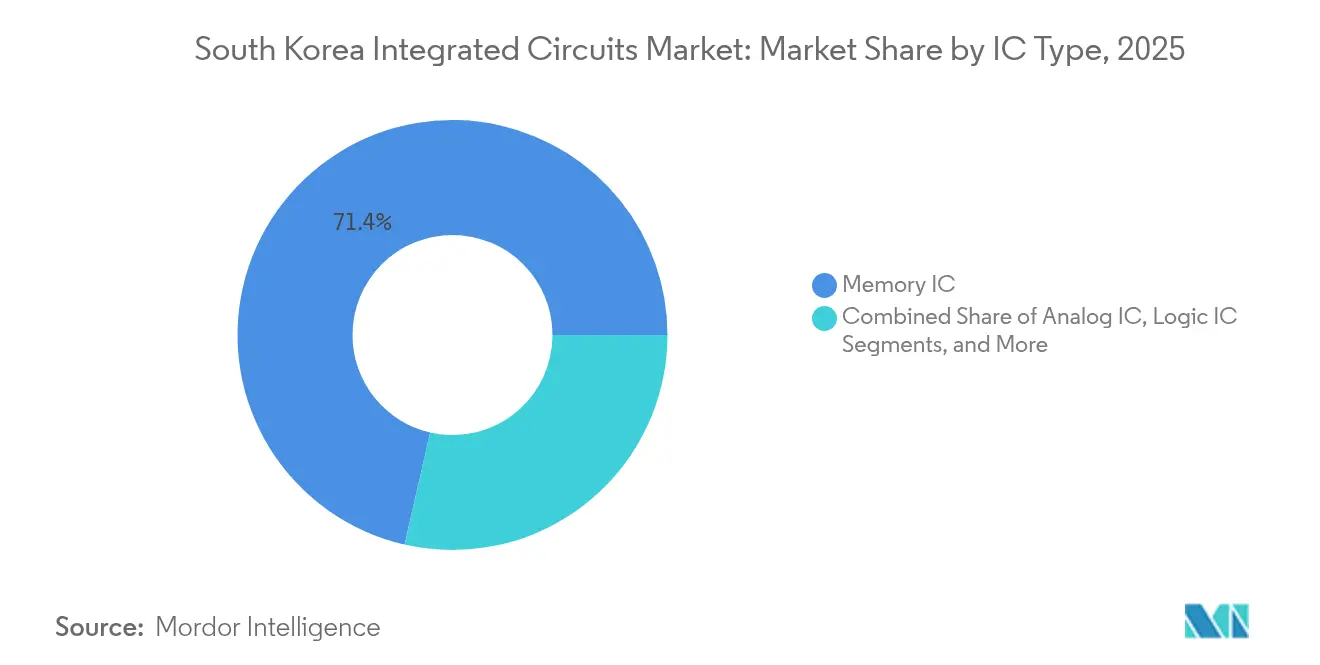

- By IC type, memory devices led with 71.42% revenue share in 2025; logic ICs are projected to expand at a 12.95% CAGR to 2031.

- By wafer size, ≥12-inch substrates commanded 79.86% of the South Korea integrated circuits market share in 2025, while 8-inch wafers recorded the fastest CAGR at 10.72% through 2031.

- By technology node, 10/7 nm processes held 31.65% of the South Korea integrated circuits market size in 2025; ≤5 nm nodes are advancing at a 18.5% CAGR.

- By end-user industry, consumer electronics captured 45.98% revenue share in 2025, whereas automotive applications are set to grow at a 15.92% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global valuation is built by aggregating outputs from multiple countries and regions, with South korea being one of the contributors. Our global integrated circuits market size represents that cumulative total.

South Korea Integrated Circuits Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government "K-Semiconductor" Tax Incentives and 1 trillion KRW R&D Fund | 2.8% | National, concentrated in the Gyeonggi Province cluster | Medium term (2-4 years) |

| Surging HBM Demand from Global AI Cloud Providers | 3.1% | Global, with primary production in South Korea | Short term (≤ 2 years) |

| Localization Push to Mitigate Geo-political Supply-Chain Risks | 1.9% | National, with spillover to allied markets | Long term (≥ 4 years) |

| EV Platform Expansion by Hyundai–Kia Boosting Power IC Uptake | 1.4% | APAC core, expanding to North America and the EU | Medium term (2-4 years) |

| Samsung Foundry's 3 nm GAA Ramp-Up Expanding Domestic Capacity | 2.2% | Global foundry market, anchored in South Korea | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Government “K-Semiconductor” Tax Incentives Drive Unprecedented Industry Mobilization

South Korea deployed a KRW 33 trillion (USD 23.25 billion) support package in April 2025 that raised loan programs and granted up to 50% tax credits on chip R&D outlays.[1]CNBC, “South Korea announces over $23 billion for chip sector as Trump tariffs loom,” cnbc.com The scheme covers power-transmission upgrades, workforce training, and a new 7.28 million m² complex in Yongin, directly lowering capital-intensity barriers for fabs that feed the South Korea integrated circuits market. Samsung and SK Hynix have already earmarked multi-year capex pipelines to leverage these incentives, cementing Korea’s role as a global production hub. The plan also aims to lift the domestic share of system semiconductors from 3% to 10% by 2030, a diversification that widens the addressable base beyond memory. Over the medium term, the fiscal support offsets export-control uncertainties and sustains double-digit growth momentum.

HBM Technology Shortage Creates Unprecedented Pricing Power for Korean Memory Leaders

AI accelerators require multiple HBM stacks per GPU, pushing SK Hynix to report fully allocated HBM output through 2025 with spillover commitments into 2026. The company’s HBM3E can process data equal to 230 full-HD movies each second, a technical moat that underpins a 50% share of the global HBM pool. Samsung holds another 40%, giving Korean firms exceptional leverage over pricing as AI workloads climb 82% annually. Elevated margins from this scarcity funnel new capital into R&D, locking in lead-time advantages for the South Korea integrated circuits market.

Supply Chain Localization Accelerates Amid Export-Control Pressures

Tokyo’s 2019 export curbs on photoresists and etching gases exposed Korea’s reliance on foreign materials. Seoul has since targeted a 50% localization rate by 2030, up from roughly 30%, financing domestic photoresist plants and partnering with ASML on a USD 760 million EUV research center in Seoul. While EUV systems will remain imported, the push minimizes geopolitical bottlenecks. These initiatives reinforce supply security and bolster investment sentiment within the South Korea integrated circuits market.

Automotive Electrification Transforms Power-Semiconductor Demand Dynamics

Hyundai Motor Group committed to 100% localization of automotive chips within three years, opening a sizable domestic market for power ICs. Hyundai Mobis started mass-producing power-integration chips in H1 2025 through a manufacturing partnership with Samsung. The roadmap includes Si-IGBT devices by 2025 and SiC-MOSFET modules by 2029, all of which heighten 8-inch-wafer utilization. Growing electrification lifts content per vehicle from under USD 500 to well above USD 1,500, injecting a new demand pillar into the South Korea integrated circuits market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Dependency on Imported EUV and Sub-systems | -1.8% | National, affecting advanced node production | Long term (≥ 4 years) |

| Semiconductor Talent Shortage and Brain-Drain | -1.2% | National, with a concentration in the Seoul-Gyeonggi region | Medium term (2-4 years) |

| Rising Electricity Costs Under Net-Zero Targets | -0.9% | National, particularly affecting energy-intensive fabs | Long term (≥ 4 years) |

| Export-Control Frictions with Japan and the U.S. | -1.6% | Global supply chain, centered on South Korea operations | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Semiconductor Talent Wars Intensify as Global Competition Escalates

Korea needs 88,000 chip engineers by 2029, far exceeding present training capacity. Samsung responded with a 64-hour workweek for its chip R&D units in April 2025, underscoring labor scarcity. Government-backed programs at Sungkyunkwan, Yonsei, and Korea universities plan to train 36,000 specialists this decade. Yet, persistent brain drain to the U.S. and Chinese firms jeopardizes these targets, risking production delays and higher labor costs across the South Korean integrated circuits market.

Energy Transition Costs Threaten Manufacturing Competitiveness

Only 9.64% of Korean power generation came from renewables in 2023. Fabs consume large volumes of electricity, and premium tariffs for green energy could erode cost advantages relative to peers in the U.S. and Europe who can procure cheaper renewables. The government’s target of 21.6% renewables by 2030 may not align with short-term fab expansion, creating uncertainty for investors in the South Korea integrated circuits market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By IC Type: Memory Dominance Faces Logic Acceleration

Memory devices captured 71.42% of the South Korean integrated circuits market size in 2025 as SK Hynix and Samsung reaped gains from AI-driven HBM demand. Logic ICs, however, are set to post a 12.95% CAGR in 2026-2031, powered by Samsung’s 2 nm gate-all-around roadmap and rising system-on-chip complexity in handsets and vehicles. Analog and micro-category chips enjoy steady growth from power-management and edge-AI tasks, balancing the product mix within the South Korea integrated circuits market.

HBM revenues climbed from 5% of SK Hynix’s memory sales in 2023 to over 40% in Q4 2024. In micro-devices, automotive microcontrollers and digital signal processors gain share as on-board AI expands. Samsung’s stated goal to triple system-chip sales by 2030 underscores the pivot toward logic, even as yield hurdles persist. The combined shifts diversify revenue streams in the South Korean integrated circuits industry without diluting memory leadership.

By Wafer Size: 12-inch Dominance with 8-inch Renaissance

≥12-inch wafers generated 79.86% of South Korea's integrated circuits market revenue in 2025, serving leading-edge DRAM and mobile processor nodes. Yet 8-inch capacity is advancing at an 10.72% CAGR as automotive and power-IC demand favor mature nodes that run economically on 200 mm lines. DB HiTek’s 49% operating margin in 2022 showcased the profitability of this legacy segment, supporting incremental investments in the South Korean integrated circuits market.

SK Hynix’s evaluation of Key Foundry aims to lift 8-inch output from 100,000 to 180,000 wafers per month. The decision balances the risk of cyclicality at advanced nodes with the dependable revenue stream from automotive and industrial customers. Meanwhile, ≤6-inch substrates remain a niche for RF and compound semiconductors. This bimodal strategy helps smooth revenue volatility within the South Korean integrated circuits industry.

By Technology Node: Advanced Nodes Drive Premium Growth

10/7 nm technologies accounted for 31.65% South Korea's integrated circuits market share in 2025, aligning with high-volume smartphone and AI workloads. ≤5 nm processes lead growth at a 18.5% CAGR, propelled by Samsung’s 2 nm GAA yield improvements and premium pricing for advanced logic. The South Korea integrated circuits market size linked to ≤5 nm is forecast to quadruple by 2030 as AI chips prioritize transistor density.

Legacy 65 nm nodes remain relevant for cost-focused automotive and IoT products. Samsung’s consideration of cancelling its 1.4 nm project due to rising costs illustrates how R&D risk escalates beyond 2 nm. Consequently, Korean firms are optimizing capital allocation to sustain profitability while preserving technological leadership.

By End-user Industry: Consumer Electronics Leadership with Automotive Acceleration

Consumer electronics delivered 45.98% of 2025 revenue, reflecting the embedded demand from smartphones, PCs, and tablets. Automotive chips will expand at 15.92% CAGR to 2031 as Hyundai–Kia electrify their fleets and adopt software-defined architectures. IT and telecom infrastructure and industrial automation offer additional demand midpoints for the South Korea integrated circuits market.

Samsung Electro-Mechanics’ USD 436 million camera-module contract for a U.S. EV maker highlights the convergence between consumer-device technology and vehicle applications. Semiconductor content per vehicle is projected to quintuple by 2030, providing a durable engine of growth for domestic fabs and packaging houses. These shifts widen the application spread of the South Korea integrated circuits market and reduce dependence on cyclical handset demand.

Geography Analysis

South Korea supplied 21.1% of global memory output in 2025, up from 13.8% in 2024, owing to unrivaled HBM capability and the scale advantages of the Gyeonggi cluster. The Semiconductor Industry Association forecast that Korea will be the world’s second-largest overall chip producer by 2032, benefiting from USD 471 billion earmarked for 16 new fabs through 2047. Within the South Korea integrated circuits market, memory specialization contrasts with a decreasing share of sub-10 nm logic, where TSMC’s capacity expansion keeps Taiwanese foundries ahead.

Asia-Pacific ex-Korea recorded strong demand for Korean IC exports, led by China’s massive electronics ecosystem and Taiwan’s integrated supply chains. Ongoing U.S.–China tensions encourage Korean firms to deepen supply-chain links with Southeast Asia and India, hedging geopolitical risks. North America and Europe remain key end-markets; Samsung’s pledged USD 192 billion over two decades for U.S. fabs underscores strategic diversification. These moves extend the reach of the South Korea integrated circuits market into high-value regional hubs while preserving at-home technology leadership.

Emerging regions such as Southeast Asia and Latin America welcome Korean equipment vendors and materials suppliers, opening ancillary revenue streams. Domestically, heavy production concentration in the Seoul–Gyeonggi corridor necessitates robust infrastructure. Government plans include reinforced power grids and high-speed freight links for the Yongin complex, mitigating single-point-of-failure risk and sustaining the growth engine of the South Korean integrated circuits market.

Coverage of the integrated circuits market by Mordor Intelligence spans a wide geographic footprint, with regional analysis available for Europe, alongside detailed country-level intelligence for Taiwan, China, and United States, each shaped by local operating conditions.

Competitive Landscape

The South Korean integrated circuits market is highly concentrated, with SK Hynix and Samsung Electronics holding roughly 75% of the leading-edge wafer capacity alongside Micron. These memory giants exploit vertical integration to lock in AI cloud customers and drive economies of scale in both DRAM and NAND. Chinese entrants, however, are closing the gap; a 2025 Korean think-tank study identified China surpassing Korea in selected memory-chip technologies, intensifying competitive pressure.[4]South China Morning Post, “South Korean think tank finds China ahead in key semiconductor technologies,” scmp.com

Samsung Foundry trails TSMC with an estimated 12% share of global foundry revenue, prompting a strategic pivot toward AI and HPC chips rather than generalized capacity spills. The firm targets four-fold AI/HPC customer growth and nine-fold revenue expansion by 2028, channeling resources to solve yield bottlenecks at 3 nm and 2 nm. SK Hynix, for its part, allocated 80% of its USD 75 billion capex pipeline to HBM, leveraging strong ties with Nvidia to remain indispensable to AI server supply chains.

Government initiatives nurture an ecosystem of fabless startups such as ASIC Land, which secured a KRW 17.5 billion (USD 13 million) chiplet project in June 2025, and packaging specialists like Hana Micron that showcased 2. xD stacking for AI devices. While these firms are small today, they fill innovation niches and diversify a market still dominated by two memory titans. Continued policy support and access to domestic foundry lines are expected to expand the competitive fabric of the South Korean integrated circuits industry.

South Korea Integrated Circuits Industry Leaders

STMicroelectronics N.V.

Texas Instruments Inc

NXP Semiconductors N.V.

Samsung Electronics Co. Ltd.

SK hynix Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Amazon Web Services and SK Group agreed to build an AI data center in Korea, boosting local demand for HBM and advanced processors.

- June 2025: Samsung and SK Hynix reorganized equipment supply chains ahead of HBM4 mass production.

- June 2025: Hana Micron sponsored the 2025 Electronic Components Technology Conference, unveiling HIC™ 2. xD packaging for AI workloads.

- June 2025: ASIC Land won a KRW 17.5 billion national project to develop chiplet-based design verification technology.

South Korea Integrated Circuits Market Report Scope

Integrated circuits (ICs) are compact electronic devices that integrate multiple components—such as transistors, resistors, capacitors, and diodes—onto a single piece of semiconductor material, typically silicon. This integration facilitates the creation of complex circuits capable of performing various functions within a small physical footprint. For market estimation, the revenue generated from sales of various types of integrated circuits that are used in various industries, such as consumer electronics, automotive, IT & telecommunication, manufacturing, and automation, across South Korea has been tracked.

The market trends are evaluated by analyzing the investments made in product innovation, diversification, and expansion. The enhancements in 5G, energy efficiency, artificial intelligence, autonomous systems, and biomedical devices are also crucial in determining the growth of the market.

The South Korean integrated circuits market is segmented by type (analog IC, logic IC, memory, and micro [microprocessor, microcontrollers, and digital signal processors]) and end-user industry (consumer electronics, automotive, IT & telecommunications, manufacturing & automation, and other end-user industries). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Analog IC | |

| Logic IC | |

| Memory IC | |

| Micro IC | Microprocessors (MPU) |

| Microcontrollers (MCU) | |

| Digital Signal Processors (DSP) |

| ≤ 6-inch |

| 8-inch (200 mm) |

| 12-inch and Above (300 mm +) |

| >65 nm |

| 45 / 40 nm |

| 32 / 28 nm |

| 22 / 20 nm |

| 16 / 14 nm |

| 10 / 7 nm |

| ≤5 nm |

| Consumer Electronics |

| Automotive |

| IT and Telecommunications |

| Industrial and Automation |

| Healthcare |

| Aerospace and Defense |

| By IC Type | Analog IC | |

| Logic IC | ||

| Memory IC | ||

| Micro IC | Microprocessors (MPU) | |

| Microcontrollers (MCU) | ||

| Digital Signal Processors (DSP) | ||

| By Wafer Size | ≤ 6-inch | |

| 8-inch (200 mm) | ||

| 12-inch and Above (300 mm +) | ||

| By Technology Node | >65 nm | |

| 45 / 40 nm | ||

| 32 / 28 nm | ||

| 22 / 20 nm | ||

| 16 / 14 nm | ||

| 10 / 7 nm | ||

| ≤5 nm | ||

| By End-user Industry | Consumer Electronics | |

| Automotive | ||

| IT and Telecommunications | ||

| Industrial and Automation | ||

| Healthcare | ||

| Aerospace and Defense | ||

Key Questions Answered in the Report

What is the current size of the South Korea integrated circuits market?

The South Korea integrated circuits market reached USD 183.17 billion in 2026 and is forecast to grow to USD 301.37 billion by 2031.

How fast is the South Korea integrated circuits market expected to grow?

The market is projected to expand at a 10.47% compound annual growth rate from 2026 to 2031.

Which product segment holds the largest share of the South Korea integrated circuits market?

Memory devices accounted for 71.42% of market revenue in 2025, driven by strong demand for high-bandwidth memory used in AI servers.

What is the fastest-growing technology node in South Korea’s chip sector?

≤5 nm processes are advancing at a 18.5% CAGR through 2031, supported by Samsung’s 2 nm gate-all-around roadmap.

How are government incentives supporting chip expansion in South Korea?

The K-Semiconductor Belt initiative offers tax credits of up to 50% on R&D spending and a KRW 33 trillion support package for infrastructure and loans, reducing capital barriers for new fabs.

Why is automotive demand important for Korea’s semiconductor industry?

Hyundai–Kia electrification plans are lifting power-IC requirements, pushing automotive semiconductor revenue to a projected 15.92% CAGR and stimulating 8-inch wafer utilization.

Page last updated on: