China GPU Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

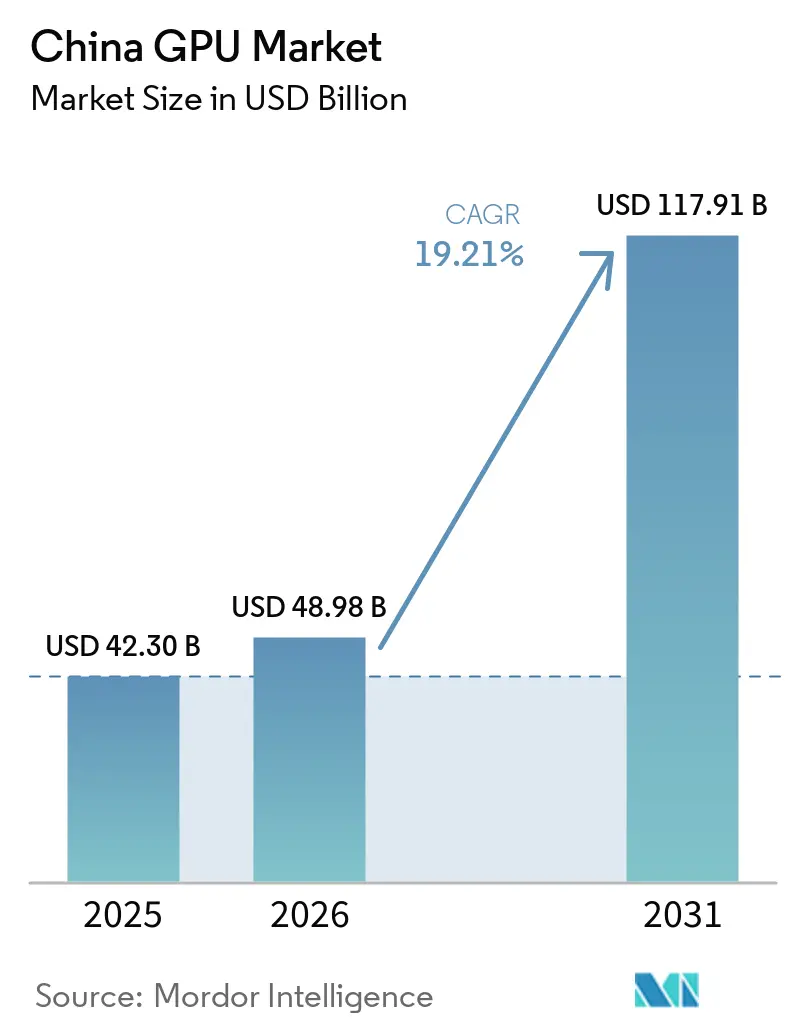

| Base Year Market Size (2025) | USD 42.30 Billion |

| Market Size (2026) | USD 48.98 Billion |

| Market Size (2031) | USD 117.91 Billion |

| Growth Rate (2026 - 2031) | 19.21% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China GPU Market Analysis by Mordor Intelligence

The China GPU market size is projected to be USD 42.30 billion in 2025, USD 48.98 billion in 2026, and reach USD 117.91 billion by 2031, growing at a CAGR of 19.21% from 2026 to 2031. Continued export-control pressure, a wave of domestic chip IPOs, and record hyperscaler capital spending collectively anchor this expansion. Hyperscalers pushed daily inference volumes up by more than 260% in 2025, tightening both local and imported accelerator supply. Provincial subsidies for power and land improved datacenter economics, while a parallel surge in automotive ADAS silicon diversified demand beyond cloud workloads. As discrete accelerators captured a significant share of 2025 revenue, the China GPU market demonstrated clear preference for high-bandwidth, rack-scale deployments over integrated alternatives.

Key Report Takeaways

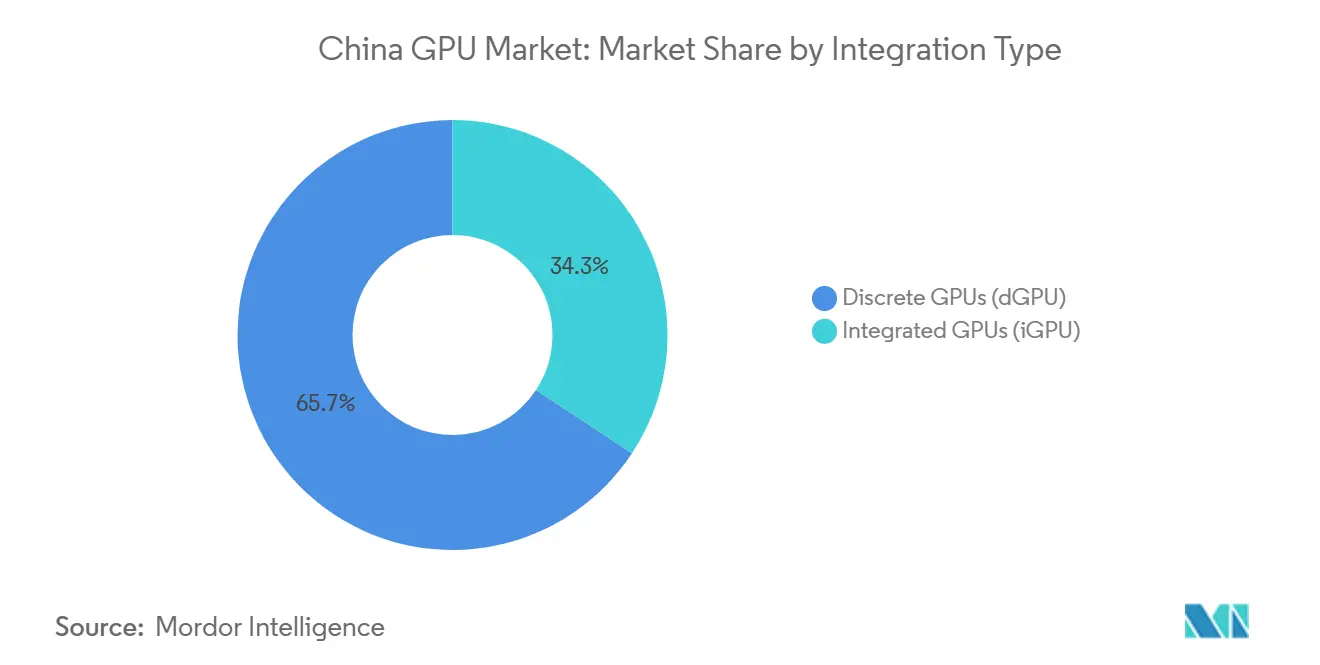

- By integration type, discrete GPUs held 65.73% of the China GPU market share in 2025 and are forecast to expand at a 19.88% CAGR through 2031.

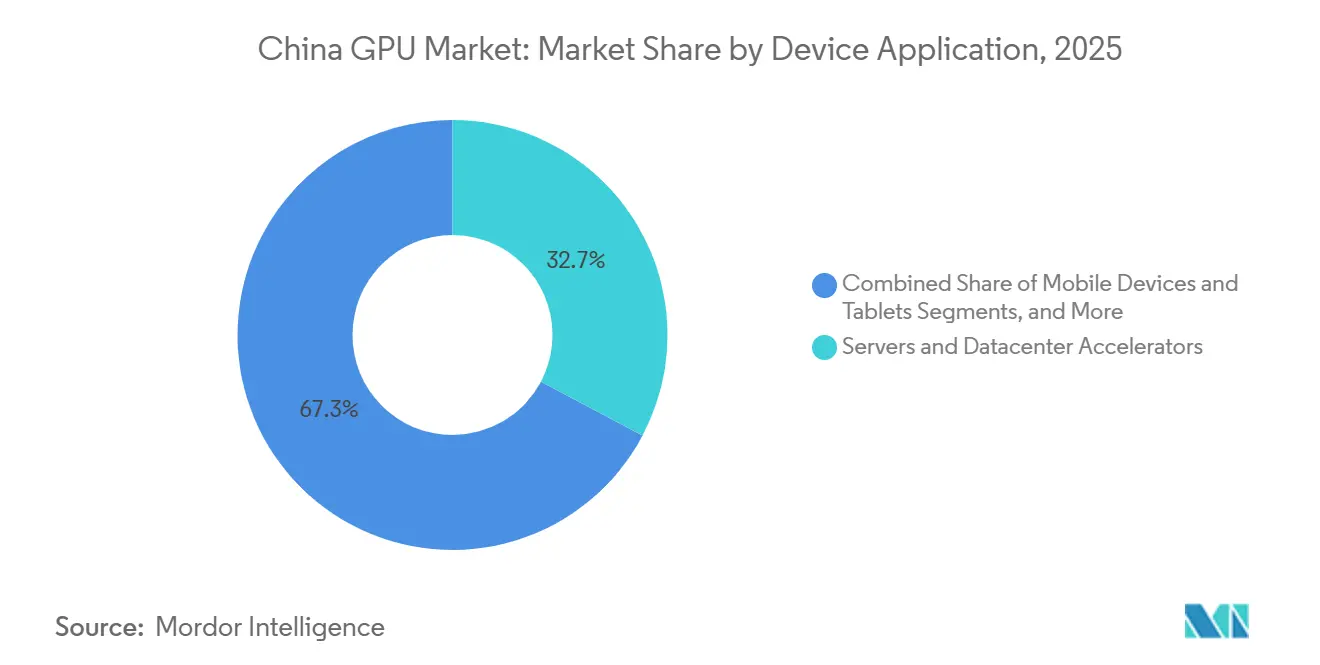

- By device application, servers and datacenter accelerators accounted for 32.74% of the China GPU market in 2025 and are projected to grow at a 19.94% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

China GPU Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Explosive Demand for AI/ML Training Workloads | +6.2% | National, clustered in Beijing, Hangzhou, Shenzhen | Medium term (2–4 years) |

| Surging Cloud and Colocation Datacenter Builds | +5.5% | Eastern provinces, Inner Mongolia, Guizhou | Medium term (2–4 years) |

| Government Semiconductor Self-Reliance Incentives | +4.8% | National, with strong programs in Shanghai, Beijing, Guangdong | Long term (≥ 4 years) |

| Rapid Expansion of Domestic Gaming Ecosystem | +3.1% | Tier-1 and tier-2 cities nationwide | Short term (≤ 2 years) |

| Automaker Shift to GPU-Centric ADAS Simulation | +2.3% | Guangdong, Shanghai, Anhui manufacturing hubs | Medium term (2–4 years) |

| Rise of Home-grown RISC-V Based GPU Start-ups | +1.9% | Beijing, Shanghai, Shenzhen research and development clusters | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Explosive Demand for AI/ML Training Workloads

Chinese hyperscalers consumed nearly 4 million AI accelerators in 2025, dwarfing shipments elsewhere combined. ByteDance’s USD 14 billion outlay on GPUs outstripped several mid-tier global clouds, while Alibaba’s USD 52.7 billion infrastructure program spans power, cooling, and building shells tuned for dense racks.[1]Financial Times, “Alibaba Unveils USD 52.7 Billion AI Infrastructure Budget,” ft.com Daily inference traffic leaped from 10.2 trillion tokens in 1H 2025 to 37 trillion in 2H 2025, forcing both domestic and foreign vendors to ration supply. Alibaba’s T-Head Zhenwu 810E shipped 470,000 units by February 2026, each with 96 GB HBM2e and 700 GB/s bandwidth, and generated more than RMB 10 billion (USD 1.4 billion) annualized sales.[2]South China Morning Post, “Zhenwu 810E Reaches 470,000 Units in Breakneck Ramp,” scmp.com Persistent accelerator scarcity enabled a 5–34% price uplift announced in April 2026.

Surging Cloud and Colocation Datacenter Builds

Hangzhou’s USD 3.7 billion multiyear GPU procurement underpins clusters expected to top 100,000 cards by mid-2026. Alibaba and China Telecom activated a Guangdong site housing 10,000 Zhenwu chips that deliver 1.2 exaflops of FP16 throughput to more than 400 enterprises. The Future Network Test Facility linked Beijing, Shanghai, and Shenzhen with a 1,243-mile fiber backbone that reduced inter-city latency to below 5 ms, enabling federated model training workflows. National data center power consumption is projected to increase by 2030, compelling operators to colocate near renewable energy assets in Qinghai and Gansu. Baidu and Huawei exploited proprietary Kunlunxin and Ascend silicon to offer cloud GPU instances, securing a significant share of domestic GPU-as-a-Service revenue.

Government Semiconductor Self-Reliance Incentives

Central and provincial budgets allocated USD 70 billion to chip programs in 2025, with RMB 15 billion (USD 2.1 billion) explicitly earmarked for GPU architecture, packaging, and HBM alternatives. Shanghai granted 50% electricity subsidies to users of domestic GPUs, trimming operating costs by roughly RMB 0.35 (USD 0.05) per kWh and lowering the total cost of ownership by nearly one-fifth. A 30% R&D tax rebate slashed effective rates to below 10% for qualifying design houses, accelerating senior-talent recruitment from Taiwan and Silicon Valley. Guangdong set aside RMB 8 billion (USD 1.1 billion) in milestone payments for 7 nm tape-outs, compressing design cycles from 36 months to around 24 months. These incentives fortified the China GPU market against foreign supply shocks and fueled a surge of IPO activity.

Rapid Expansion of Domestic Gaming Ecosystem

In Q3, gaming GPU shipments climbed as consumers upgraded ahead of expected RTX 5060 launches. The national PC market added growth, with gaming desktops and high-refresh-rate laptops topping discrete attach metrics. Colorful preserved board-partner status through humidity-optimized cooling solutions and extended warranties tailored to southern provinces. Provincial governments spent on esports venues, stimulating demand for ray-tracing-capable mid-range GPUs in tier-1 cities. Although December saw a shipment drop due to RTX 5060 stock-outs, first-quarter allocations rebounded as Nvidia prioritized China to defend its share.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| US Export Controls on Advanced GPU Nodes | −3.8% | Nationwide, most acute for hyperscalers | Short term (≤ 2 years) |

| Foundry Capacity Tightness for 7 nm and Below | −2.9% | Shanghai and Shenzhen fabs, reliance on overseas nodes | Medium term (2–4 years) |

| Stricter Power-Use Quotas for Hyperscale Sites | −1.6% | Inner Mongolia, Guizhou, Ningxia hubs | Medium term (2–4 years) |

| Shortage of Senior GPU Architecture Talent | −1.2% | Beijing, Shanghai, Shenzhen design centers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

US Export Controls on Advanced GPU Nodes

October 2023 rules eliminated H100 and A100 shipments to China, forcing Nvidia to launch lower-bandwidth H20, L20, and L2 variants. AMD booked a USD 800 million MI300X writedown when licenses were denied, redirecting focus to the down-spec MI308 line. Beijing later cleared 400,000 H200 units for select hyperscalers but imposed a 25% tariff, raising landed costs to USD 10,000 per card. NVIDIA’s brief H200 production pause in late 2025 underscored ongoing policy volatility. Performance gaps force domestic labs to deploy about 5 Huawei Ascend 910C boards to match a single H100, inflating rack density and power budgets.

Foundry Capacity Tightness for 7 nm and Below

TSMC’s 3 nm lead times stretched past 50 weeks by Q4 2025, while CoWoS packaging slots were booked until mid-2026. SMIC targets 100,000 wafers per month at 7 nm and 5 nm by end-2026, but still runs yields below cost-competitive levels. Domestic startups, therefore, rely on chiplet designs such as Biren’s BR100, which links four 7 nm compute dies around a 14 nm I/O hub to sidestep the risk of single-die defects. Hua Hong’s 7 nm pilot line will not reach commercial volumes before 2027. The China Large Fund Phase III earmarked RMB 15 billion (USD 2.1 billion) for advanced packaging to relieve leading-edge shortages, but the near-term constraint continues to temper the China GPU market growth trajectory.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Integration Type: Discrete GPUs Dominate Datacenter Spend

Discrete accelerators controlled 65.73% of the China GPU market share in 2025 and are forecast to grow at a 19.88% CAGR through 2031. Nearly all hyperscaler training clusters use high-bandwidth memory and dedicated interconnects, features unavailable in integrated solutions, reinforcing the revenue weight of discrete silicon in the China GPU market. Alibaba’s February 2026 milestone of 470,000 Zhenwu 810E units underscores the scale advantage of rack-ready cards. ByteDance mirrored this trend by allocating its USD 14 billion budget almost exclusively to discrete H20 and A800 boards, while Tencent earmarked the bulk of its USD 5 billion AI envelope for similar rack configurations.

Integrated GPUs, meanwhile, advanced inside the mobile ecosystem. MediaTek’s Dimensity 8500, launched in January 2026, introduced hardware ray tracing to mid-price smartphones, and Qualcomm’s Snapdragon 8 Gen 4 brought Adreno 850 graphics to premium handsets.[3]MediaTek Press Release, “Dimensity 8500 Brings Ray Tracing to Mid-Tier Phones,” mediatek.com Integrated silicon captured a significant share of unit shipments but kept the China GPU market size tilted toward discrete parts. Business laptops use integrated cores to reduce procurement costs, yet datacenter deployments remain more than 95% discrete because integrated GPUs cannot deliver the memory bandwidth required for large language model training.

By Device Application: Servers and Datacenter Accelerators Lead Growth

Servers and datacenter accelerators accounted for 32.74% of 2025 revenue and are expected to post a 19.94% CAGR through 2031, the fastest trajectory in the China GPU market. Alibaba and China Telecom’s 10,000-card Guangdong cluster exemplifies the scale, achieving 1.2 exaflops of FP16 compute and spotlighting the adoption of liquid cooling. Hangzhou’s municipal contract for 100,000 cards by mid-2026 further cements servers as the demand core. Baidu and Huawei exploit Kunlunxin and Ascend silicon to undercut Nvidia-based cloud pricing by up to 30%, winning 70% of the GPU-as-a-Service segment.

PCs and workstations make up the second-largest application block, buoyed by strong demand from creative professionals. NVIDIA’s workstation-oriented RTX 6000D, released in early 2026, caters to CAD and simulation users seeking domestic supply continuity.[4]Nvidia Corporation, “RTX 6000D Workstation GPU Datasheet,” nvidia.com Automotive ADAS adoption is accelerating: Xpeng’s Turing chip delivers 750 TOPS, and NIO’s Shenji NX9031 surpasses 1,000 TOPS, together shipping into more than 460,000 vehicles by early 2026. Although gaming consoles and handhelds remain niche, industrial vision and smart-city devices are emerging footholds for low-power domestic GPUs.

Geography Analysis

In 2025, datacenter deployments concentrated heavily in Beijing, Hangzhou, and Shenzhen. These cities drew closer to talent-rich headquarters and high-bandwidth backbones. Eastern provinces like Zhejiang, Jiangsu, and Guangdong provided land and renewable energy, bolstered by provincial subsidies, enhancing the total cost of ownership. Notably, Guangdong contributed significant funding to chip milestone initiatives. While Inner Mongolia and Guizhou offered electricity at competitive rates, attracting hyperscalers despite latency issues, grid bottlenecks limited their share.

Shanghai's incentive of an electricity rebate for domestic GPU users successfully attracted Biren and Moore Threads to set up production hubs in Pudong, reinforcing a clustering trend in the Yangtze River Delta. Meanwhile, tier-2 cities like Chengdu, Xi’an, and Wuhan captured a share of shipments by offering land grants and tax holidays. However, ongoing talent shortages slowed the migration of nodes. In the automotive sector, silicon demand was concentrated in Guangdong, Shanghai, and Anhui, aligning with the locations of BYD, NIO, and XPeng plants. Gaming GPUs saw the highest consumption in tier-1 cities, especially where per capita income was higher, and esports arenas were abundant.

In 2025, the western provinces of Xinjiang, Qinghai, and Gansu represented a smaller share of GPU deployments. Driven by renewable mandates, new solar-powered clusters are emerging. A case in point is Baidu's installation of Kunlunxin units in Ningxia, which boasts a commendable power-usage-to-effectiveness ratio. With improving fiber density and relaxed latency budgets for inference tasks, these western regions are poised to capture a larger share, albeit without overshadowing the coastal powerhouses.

Competitive Landscape

Between 2024 and 2026, the once foreign-dominated China GPU market became a battleground for domestic players. NVIDIA's market share decreased significantly. Meanwhile, over 15 local vendors entered the market. IPOs from companies like Moore Threads, Biren, Muxi, Iluvatar CoreX, and Kunlunxin provided capital for software stacks, with a focus on bridging the CUDA-compatibility divide. Alibaba directed a portion of its 2025 chip procurement towards domestic sources. Tencent is planning a balanced split by 2027. These maneuvers underscore a growing trend toward dual sourcing as a risk-management strategy.

Emerging suppliers differentiate through cluster-level packages that bundle orchestration and cooling. Moore Threads landed a CNY 660 million (USD 91 million) turnkey order in March 2026, signaling buyer appetite for integrated stacks. Xiwang, spun from SenseTime, and Cambricon are pioneering inference-optimized INT4 and INT8 parts to serve a domestic token load that now doubles U.S. volumes.

Patent activity supports this momentum: filings for GPU-related inventions surged 42% in 2025, with Huawei, Alibaba, and Biren accounting for more than one-third of the applications.[5]China National Intellectual Property Administration, “Annual Patent Statistics 2025,” cnipa.gov.cn Memory innovation remains a battleground, as Cambricon adopts 64 GB HBM2e while Tianshu Zhixin leverages cost-friendly GDDR6X to target lower ASP segments.

China GPU Industry Leaders

NVIDIA Corporation

Advanced Micro Devices, Inc.

Intel Corporation

Huawei Technologies Co., Ltd. (HiSilicon)

Biren Technology

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Alibaba T-Head raised Zhenwu 810E prices by up to 34%, citing persistent supply constraints and confirming shipment of 470,000 units by February 2026.

- March 2026: Moore Threads won a CNY 660 million AI-cluster contract that packages hardware, cooling, and multi-year support for enterprise clients.

- March 2026: Muxi partnered with DuoDian Shuzhi to roll out GPU-powered retail AI across 5,000 stores nationwide.

- March 2026: Muxi secured RMB 550 million to scale edge-inference GPU production.

China GPU Market Report Scope

The China GPU Market Report is Segmented by Integration Type (Integrated GPUs and Discrete GPUs), and Device Application (Mobile Devices and Tablets, PCs and Workstations, Servers and Datacenter Accelerators, Gaming Consoles and Handhelds, Automotive and ADAS, and Other Embedded and Edge Devices). The Market Forecasts are Provided in Terms of Value (USD).

| Integrated GPUs (iGPU) |

| Discrete GPUs (dGPU) |

| Mobile Devices and Tablets |

| PCs and Workstations |

| Servers and Datacenter Accelerators |

| Gaming Consoles and Handhelds |

| Automotive / ADAS |

| Other Embedded and Edge Devices |

| By Integration Type | Integrated GPUs (iGPU) |

| Discrete GPUs (dGPU) | |

| By Device Application | Mobile Devices and Tablets |

| PCs and Workstations | |

| Servers and Datacenter Accelerators | |

| Gaming Consoles and Handhelds | |

| Automotive / ADAS | |

| Other Embedded and Edge Devices |

Key Questions Answered in the Report

What is the projected value of the China GPU market in 2031?

The market is forecast to reach USD 117.91 billion by 2031.

How fast is the market expected to grow between 2026 and 2031?

It is projected to expand at a 19.21% CAGR over that period.

Which segment held the largest share in 2025?

Discrete GPUs led with 65.73% of market revenue in 2025.

Which application category will post the fastest growth?

Servers and datacenter accelerators are expected to grow at a 19.94% CAGR to 2031.

How are export controls affecting suppliers?

U.S. restrictions reduced access to top-end GPUs, leading vendors to create down-spec versions and Chinese buyers to diversify toward domestic chips.

Why are cloud operators investing in inland provinces?

Lower electricity prices and renewable-energy mandates make regions like Inner Mongolia and Guizhou attractive for large clusters despite latency trade-offs.

Page last updated on: