Japan GPU Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 11.98 Billion |

| Market Size (2026) | USD 13.77 Billion |

| Market Size (2031) | USD 31.68 Billion |

| Growth Rate (2026 - 2031) | 18.13% CAGR |

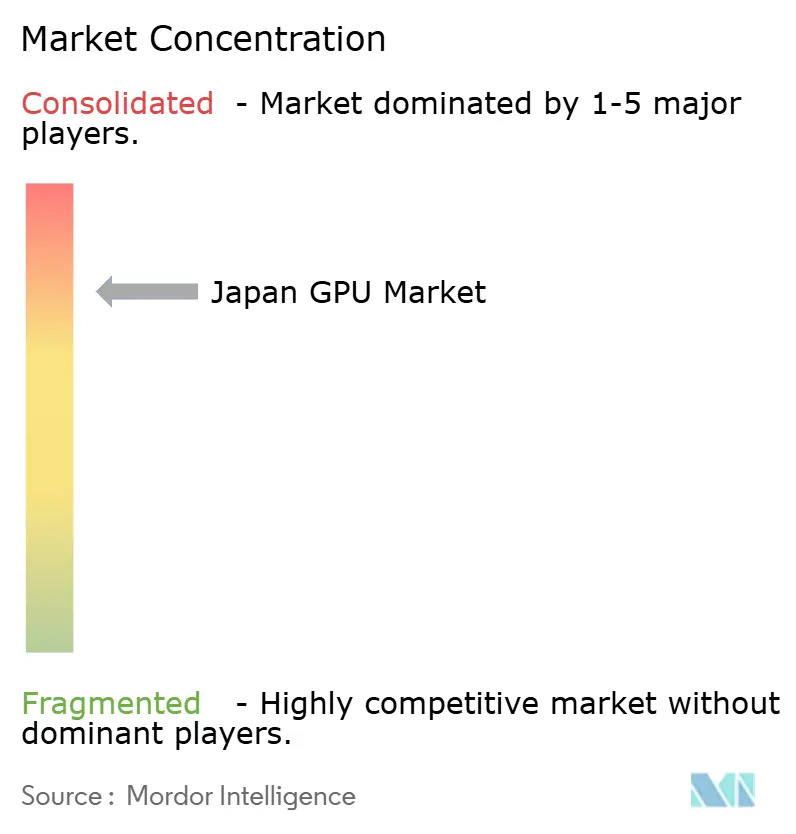

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Japan GPU Market Analysis by Mordor Intelligence

The Japan GPU market size is expected to increase from USD 11.98 billion in 2025 to USD 13.77 billion in 2026 and reach USD 31.68 billion by 2031, growing at a CAGR of 18.13% over 2026-2031. Strong sovereign-AI spending, hefty corporate investments in on-premises training clusters, and a flourishing esports culture are combining to lift unit volumes and average selling prices. Ministry-backed subsidies lower the cost of new datacenter deployments, while Microsoft’s multi-billion-dollar build-out signals long-run hyperscale appetite. Automotive makers are now embedding GPU-centric vision processors in mass-market vehicles, broadening use cases beyond the cloud. At the same time, yen depreciation raises import prices, keeping retail revenue growth ahead of shipments and intensifying the push for local wafer output.

Key Report Takeaways

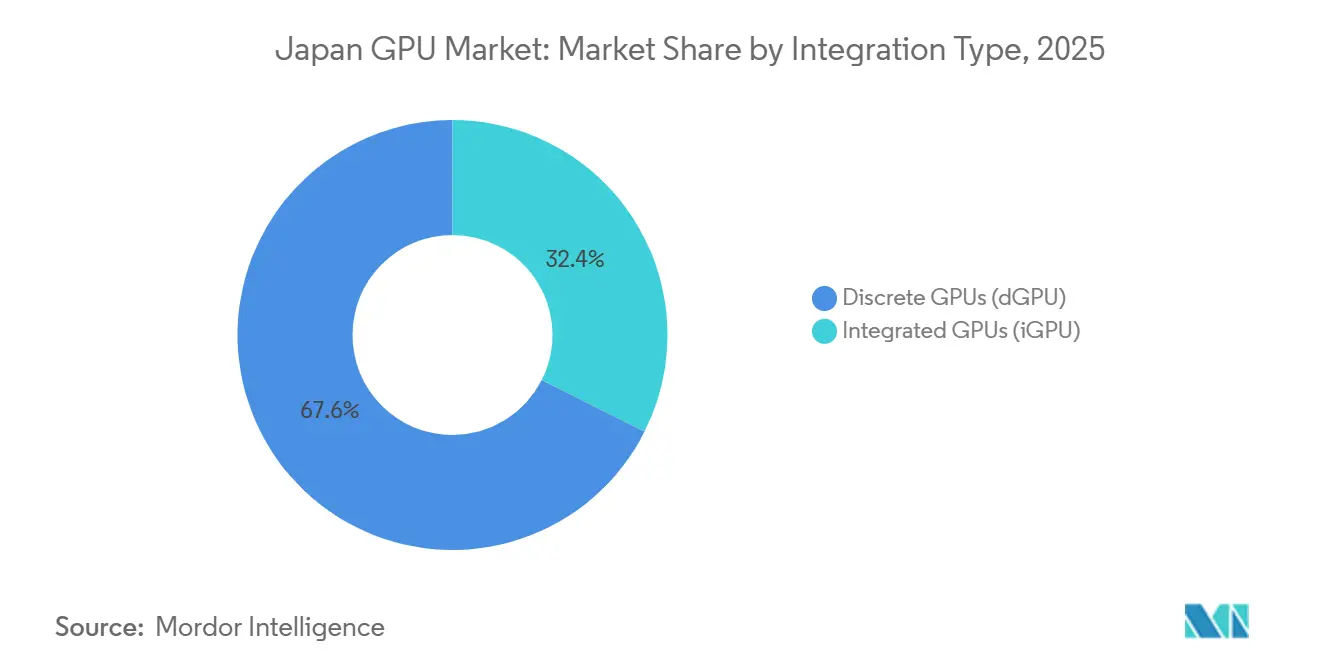

- By integration type, discrete GPUs led with 67.59% revenue share in 2025; integrated GPUs are advancing at an 18.55% CAGR through 2031.

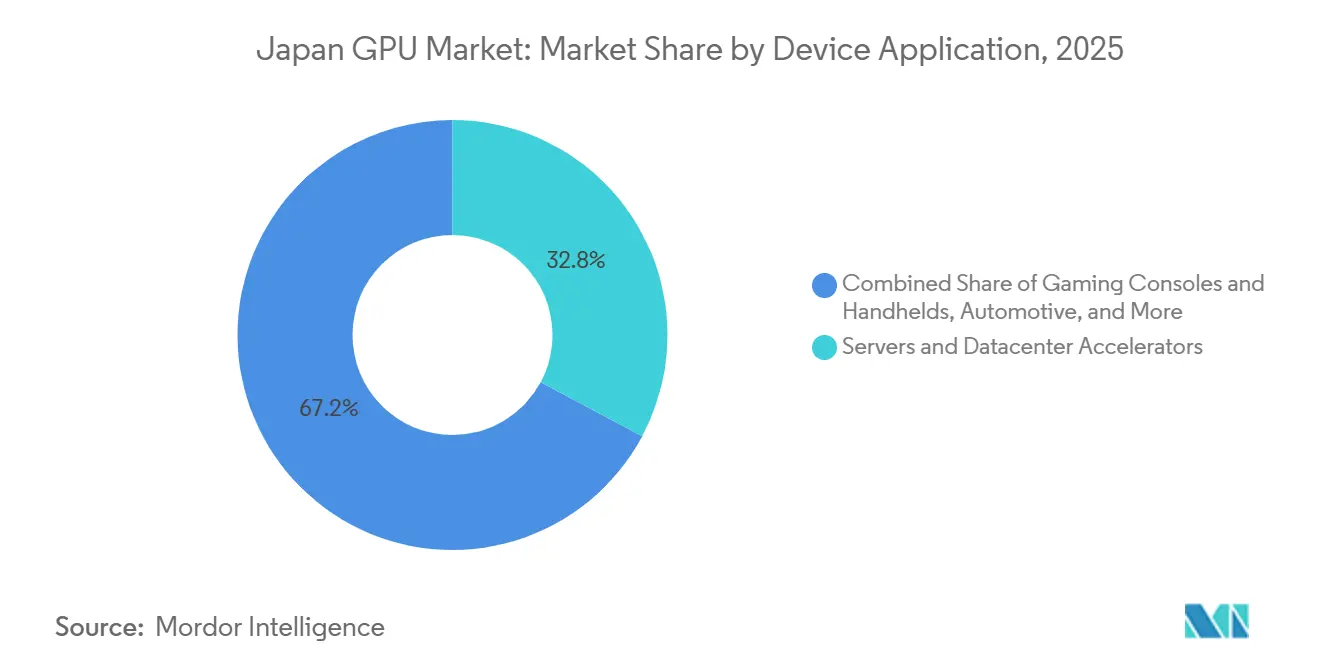

- By device application, servers and datacenter accelerators accounted for 32.81% of the Japan GPU market share in 2025 and are expanding at an 18.51% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Japan GPU Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging AI/ML Training Workloads Across Japanese Enterprises | +4.20% | National – Tokyo, Osaka, Nagoya | Medium term (2-4 years) |

| Government Subsidies for Domestic Semiconductor Supply Chain Re-Shoring | +3.80% | National – Kumamoto, Hokkaido, Miyagi | Long term (≥ 4 years) |

| Expansion of Automotive SoCs Integrating GPU-Based Vision for ADAS | +3.10% | National – Aichi, Tochigi, Kanagawa | Medium term (2-4 years) |

| Rapid Uptake of Generative-AI-Enabled Mobile Apps | +2.60% | National – major urban youth segments | Short term (≤ 2 years) |

| Esports-Led Boom in High-Frame-Rate PC Gaming Cafés | +2.10% | Tokyo, Osaka, Fukuoka | Short term (≤ 2 years) |

| Growth of Immersive 3D Design Tools in Manufacturing | +1.90% | Aichi, Shizuoka, Osaka, Hiroshima | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surging AI/ML Training Workloads Across Japanese Enterprises

Compliance with the Act on the Protection of Personal Information is steering banks, automakers, and life-science firms toward sovereign datacenters equipped with high-end accelerators. Subsidies under the GENIAC program cut capital outlays, letting regional cloud providers such as SAKURA Internet and KDDI deploy racks of NVIDIA H200 cards without offshoring sensitive data.[1] METI, “Semiconductor Support Measures,” meti.go.jp SoftBank’s 1,000-GPU cluster and Microsoft’s USD 10 billion infrastructure pledge further anchor demand. Toyota’s Woven City simulation hub alone consumed more than 500 A100S in 2025, underscoring how R&D workloads now hinge on domestic capacity.[2]MM Research Institute, “Generative AI App Penetration Survey 2025,” m2ri.jp

Government Subsidies for Domestic Semiconductor Supply Chain Re-Shoring

The Ministry of Economy, Trade and Industry has earmarked JPY 1.23 trillion (USD 7.97 billion) for wafer fabs, channeling JPY 732 billion into TSMC’s Kumamoto site and JPY 920 billion into Rapidus’ 2-nm line. TSMC began 3-nm output in late 2025, shipping substrates for AMD Instinct MI300 cards, while Rapidus targets 2-nm production by 2027. JP. Although yields will take years to mature, the roadmap promises mid-decade relief from overseas dependency, positioning local integrators to capture supply closer to home.

Expansion of Automotive SoCs Integrating GPU-Based Vision for ADAS

Renesas R-Car V4H, delivering 34 TOPS, entered Toyota’s 2025 RAV4 to manage 3D panoramic vision.[3]Renesas Electronics, “R-Car V4H Product Guide,” renesas.comHonda and Nissan have queued similar deployments, and the forthcoming R-Car Gen 5 lifts performance to 400 TOPS, propelling Level 3 functionality by 2027. Automakers prefer integrated GPUs to discrete cards to curb BOM cost and energy draw, pushing unit shipments into double-digit growth across domestic assembly plants.

Rapid Uptake of Generative-AI-Enabled Mobile Apps

MM Research data show ChatGPT penetration reached 36.2% of smartphone users by late 2025, with Google Gemini at 25%. Qualcomm’s Snapdragon 8 Gen 3 and Apple’s M4 chips now support INT8/FP16 inference at trillions-ops-per-second, shifting part of the compute load from cloud to edge.[4]Qualcomm Inc., “Snapdragon 8 Gen 3 Technical Brief,” qualcomm.comThe Digital Agency plans guardrails around on-device AI, encouraging handset vendors to embed even more capable GPUs for privacy-preserving generative workloads.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ongoing 2 nm/3 nm Process Node Capacity Shortages | -2.80% | Global – acute for Japan | Medium term (2-4 years) |

| Energy-Efficiency Regulations Limiting Datacenter Power Budgets | -1.70% | National – Tokyo, Osaka | Long term (≥4 years) |

| Yen Volatility Raising Imported GPU ASPs | -1.40% | Nationwide SMEs | Short term (≤2 years) |

| Export-Control Restrictions on High-End AI Accelerators | -0.90% | Nationwide cloud and research | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Ongoing 2 nm/3 nm Process Node Capacity Shortages

TSMC’s CoWoS lines now run at near-full load, stretching lead times for Blackwell and Hopper GPUs to as long as 78 weeks. Apple, NVIDIA, and AMD have already block-booked 2-nm slots through 2027, denying Japanese fabless start-ups early access. Samsung’s 3-nm yields remain under 85%, deterring customers from diversifying supply. Until Rapidus ramps, integrators must elongate product cycles or revert to prior-generation silicon.

Energy-Efficiency Regulations Limiting Datacenter Power Budgets

From 2029, new Japanese datacenters must post a PUE of 1.3 or lower, driving a wholesale shift to liquid cooling and waste-heat recovery. Each H200 card draws about 700 W, lifting rack densities above 40 kW, and adding USD 150,000-200,000 per rack in cooling hardware. Time-of-use tariffs from Tokyo Electric Power further skew economics, forcing AI operators to batch jobs overnight. Smaller regional clouds face cash-flow strain, meeting both efficiency and capacity mandates.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Integration Type: Discrete GPUs Anchor Datacenter Expansion

Discrete GPUs captured 67.59% of 2025 revenue, highlighting their primacy in large-scale AI training within the Japan GPU market share. Ongoing migration to NVIDIA’s Blackwell platform, with 208 billion transistors and 10 TB/s NVLink, cements this lead as hyperscalers fill racks with upgradeable add-in boards. AMD’s MI350X provides a cost-advantaged option for inference, helping cloud challengers diversify vendor exposure. Meanwhile, integrated GPUs prevail in thermally constrained environments such as ultraportable notebooks and automobiles. Renesas R-Car Gen 5 will propel integrated units into higher tiers of driver-assistance from 2027, albeit without threatening the performance gulf that datacenter workloads demand.

Budget-sensitive workstations and esports cafes still prefer discrete cards to hit 400-Hz frame rates, while mobile and tablet designs rely on SoC-embedded graphics to balance battery life. Apple’s M4 and Qualcomm’s Snapdragon X Elite chipsets now match entry-level discrete throughput, signaling eventual convergence in low-power segments. Nevertheless, memory bandwidth ceilings keep integrated architectures from replacing dedicated accelerators at the top end. Therefore, discrete units will remain the principal revenue engine for the Japan GPU market size through 2031.

By Device Application: Servers and Datacenters Lead AI Infrastructure Build-Out

Servers and datacenter accelerators delivered 32.81% of 2025 sales and are projected to log an 18.51% CAGR, underscoring sovereign-cloud momentum inside the Japan GPU market. Fujitsu’s sovereign-AI servers, built around H200 GPUs and domestic MONAKA-X CPUs, give regulated industries a compliant alternative to foreign regions. SAKURA Internet and KDDI added more than 3,000 nodes under GENIAC subsidies, while Microsoft’s multi-site expansion will introduce 5,000 additional GPU boards by 2027.

Consumer PCs and pro workstations remain a sizable secondary outlet, buoyed by content creation, CAD, and high-frame-rate gaming demand. Gaming consoles, handhelds, and automotive ADAS grow off smaller bases, yet they diversify unit mix and encourage silicon vendors to tune power-efficiency road maps. Edge devices in retail and healthcare further broaden the total addressable market, making AI inference a pervasive workload across Japan GPU industry endpoints.

Geography Analysis

Tokyo dominates the Japan GPU market, hosting the bulk of hyperscale datacenters and half of all sovereign-AI server installations. Financial services, fintech start-ups, and media firms congregate around the city’s fiber backbone, prioritizing ultra-low latency to cloud zones. Osaka ranks second, propelled by Microsoft’s under-construction campus and a cluster of manufacturing giants running GPU-accelerated simulations. Nagoya’s automotive ecosystem absorbs workstation-class cards for CAD and digital twin modeling, underpinned by Toyota, Honda, and Nissan engineering hubs.

Kumamoto’s emergence as a wafer-fab locale positions the prefecture to influence upstream supply dynamics by 2027, once TSMC’s second phase adds 6-nm capacity. Hokkaido follows with Rapidus’ future 2-nm site, expected to attract packaging and EDA tool vendors. Local governments in Fukuoka, Sendai, and Hiroshima are tapping Digital Rural City Initiative grants to subsidize mini-datacenters, seeding demand for mid-range accelerators in secondary cities. Rural prefectures adopt edge GPUs for smart agriculture and disaster monitoring, demonstrating early dispersion beyond megacities even as absolute volumes stay modest.

Competitive Landscape

The Japan GPU market is highly concentrated, scoring a 9 on a 10-point scale, with NVIDIA holding 94% of add-in boards in Q4-2025. CUDA’s entrenched developer base, plus multi-year CoWoS supply agreements, grant the firm near-monopoly status in AI training workloads. AMD counters with open-source ROCm and diamond-cooled platforms that trim power by 20%, playing to operators grappling with PUE limits. Intel re-enters discrete graphics via Arc Pro while positioning Gaudi 3 for deep-learning inference, yet ecosystem inertia hinders swift uptake.

Renesas and Broadcom carve out embedded opportunities in automotive and IoT by integrating GPU cores in SoCs that sidestep discrete card cost. Domestic cloud upstarts Rutilea and Highreso exploit H100 clusters to undercut hyperscalers by 15-20% on GPU-hours, appealing to SMEs wary of foreign data residency. Datacenter builders now view liquid cooling and direct-to-chip solutions as table stakes, pushing vendors to co-innovate on thermal management rather than raw flops alone. Compliance with privacy statutes shapes purchase criteria as much as throughput, steering solutions toward sovereign manufacture and local support.

Japan GPU Industry Leaders

NVIDIA Corporation

Advanced Micro Devices, Inc.

Intel Corporation

Sony Group Corporation

Qualcomm Incorporated

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: NVIDIA partnered with Kagawa Prefecture to open an AI R&D center using 200 H200 GPUs for typhoon prediction and crop analytics.

- March 2026: AMD rolled out diamond-cooled Instinct MI300X servers, cutting TDP by 20% for Japanese datacenters.

- March 2026: Lenovo launched ThinkStation P5 Gen 2 workstations with Blackwell GPUs priced at JPY 1.8 million (USD 11,613).

- February 2026: Fujitsu introduced sovereign-AI servers integrating H200 GPUs and MONAKA-X CPUs, built in Ishikawa.

Japan GPU Market Report Scope

The Japan GPU Market Report is Segmented by Integration Type (Integrated GPUs, Discrete GPUs) and Device Application (Mobile Devices and Tablets, Pcs and Workstations, Servers and Datacenter Accelerators, Gaming Consoles and Handhelds, Automotive/ADAS, Other Embedded and Edge Devices). The Market Forecasts are Provided in Terms of Value (USD).

| Integrated GPUs (iGPU) |

| Discrete GPUs (dGPU) |

| Mobile Devices and Tablets |

| PCs and Workstations |

| Servers and Datacenter Accelerators |

| Gaming Consoles and Handhelds |

| Automotive / ADAS |

| Other Embedded and Edge Devices |

| By Integration Type | Integrated GPUs (iGPU) |

| Discrete GPUs (dGPU) | |

| By Device Application | Mobile Devices and Tablets |

| PCs and Workstations | |

| Servers and Datacenter Accelerators | |

| Gaming Consoles and Handhelds | |

| Automotive / ADAS | |

| Other Embedded and Edge Devices |

Key Questions Answered in the Report

How fast is the Japan GPU market growing through 2031?

Revenue is forecast to rise from USD 13.77 billion in 2026 to USD 31.68 billion by 2031, implying an 18.13% CAGR.

Which segment contributes the most to Japan’s GPU demand?

Servers and datacenter accelerators lead, accounting for 32.81% of 2025 revenue and growing at an 18.51% CAGR through 2031.

Who holds the dominant share of GPU add-in boards in Japan?

NVIDIA commanded 94% of the add-in board segment in Q4-2025, far ahead of AMD and Intel.

What government initiatives support domestic GPU supply?

METI has committed more than JPY 1 trillion to TSMC’s Kumamoto plant and Rapidus’ 2-nm foundry to localize advanced logic production.

Page last updated on: