India Discrete GPU Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

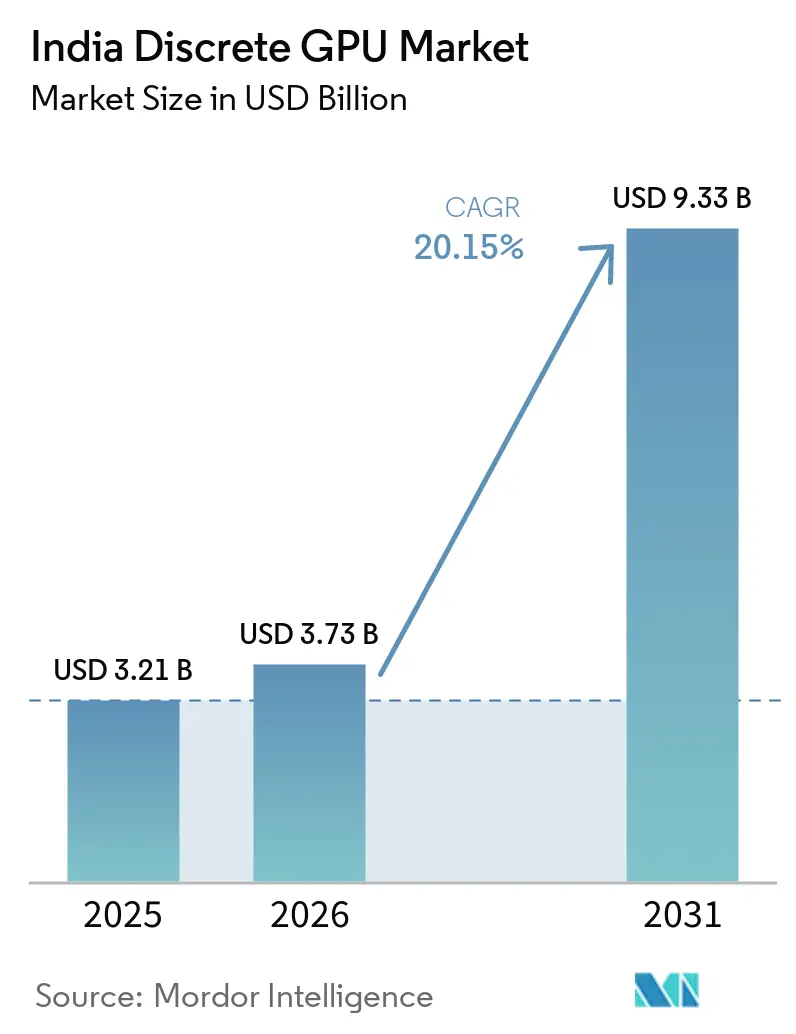

| Base Year Market Size (2025) | USD 3.21 Billion |

| Market Size (2026) | USD 3.73 Billion |

| Market Size (2031) | USD 9.33 Billion |

| Growth Rate (2026 - 2031) | 20.15% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Discrete GPU Market Analysis by Mordor Intelligence

The India discrete GPU market size is expected to increase from USD 3.21 billion in 2025 to USD 3.73 billion in 2026 and reach USD 9.33 billion by 2031, growing at a CAGR of 20.15% over 2026-2031. Enterprises are re-architecting compute stacks around accelerated processing, hyperscalers are pre-ordering multi-year GPU allocations, and government AI missions are amplifying baseline demand. The pivot from gaming-centric sales toward rack-scale accelerators is visible as servers and datacenter GPUs already out-earn consumer cards. Memory bandwidth rather than raw core count is now the bottleneck, pushing buyers toward high-bandwidth memory (HBM) while GDDR retains a cost advantage for mainstream tiers. Import tariffs, volatile exchange rates, and regional power constraints remain brake pads on the otherwise steep growth curve.

Key Report Takeaways

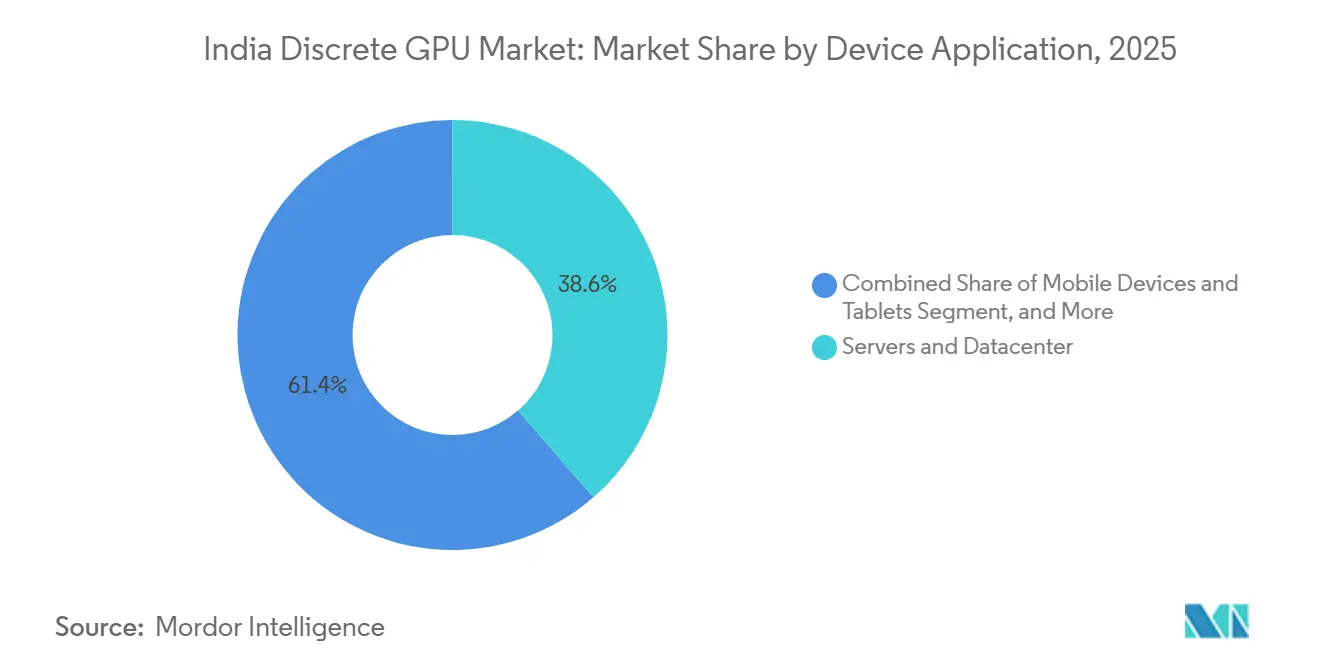

- By device application, servers and datacenter accelerators led with 38.62% of India's discrete GPU market share in 2025 and will advance at a 20.45% CAGR through 2031.

- By memory type, GDDR-based boards commanded 68.94% share of the India discrete GPU market size in 2025, while HBM-based variants are projected to rise at a 20.73% CAGR to 2031.

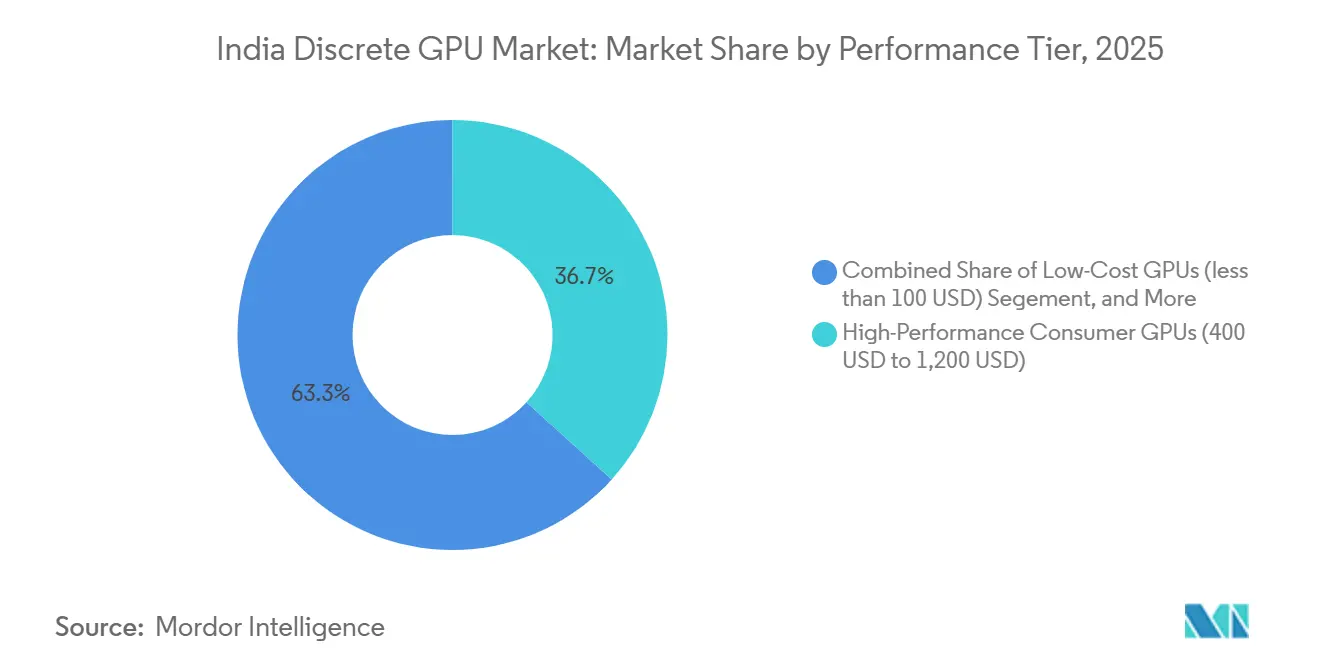

- By performance tier, high-performance consumer GPUs captured 36.73% of India's discrete GPU market share in 2025, whereas data center and AI accelerators priced above USD 1,200 will post the fastest 20.68% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

India Discrete GPU Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact |

|---|---|---|---|

| Rising AI workloads demanding GPU acceleration in Indian data centers | +6.8% | Mumbai, Bengaluru, Hyderabad, Chennai, Pune clusters | Medium term (2-4 years) |

| Booming PC-gaming culture among Gen-Z and millennials | +4.2% | Metro and tier-1 cities nationwide | Short term (≤ 2 years) |

| Government initiatives such as Make-in-India boosting local GPU manufacturing | +3.5% | Gujarat fab corridor, Assam OSAT hub | Long term (≥ 4 years) |

| Proliferation of OTT video creation tools needing real-time rendering | +2.1% | Mumbai, Delhi NCR, Bengaluru content hubs | Short term (≤ 2 years) |

| Web3 start-ups building on-chain graphics engines | +1.8% | Bengaluru and Delhi NCR | Medium term (2-4 years) |

| Adoption of GPU-powered on-device medical imaging in semi-urban hospitals | +1.5% | Tier-2 and tier-3 cities across 21 states | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising AI Workloads Demanding GPU Acceleration

India’s hyperscale operators have moved from pilot clusters to multi-gigawatt campuses, each lined with AI racks that swallow 80-150 kilowatts. Microsoft earmarked USD 17.5 billion, and Google pledged USD 15 billion for new regional zones, both optimized around dense GPU fabrics. Government procurement is no longer peripheral; the IndiaAI Mission alone has ordered 38,000 GPUs and targets 63,000 units by 2027, tightening an already strained supply chain. Operators now lock in multi-year allocations to avoid spot-market premiums, effectively pulling forward demand. The upshot is a structural shift where AI workloads overshadow traditional virtualization, anchoring long-run growth for the India discrete GPU market.

Booming PC-Gaming Culture Among Gen-Z and Millennials

Notebook shipments climbed 8.1% year over year in Q1 2025 as gaming laptops outpaced mainstream models. Custom PC builders report triple-digit expansion over five years, driven by esports tournaments that stream to millions on YouTube and JioCinema. Qualcomm’s Snapdragon 8 Elite added a three-core Adreno GPU clocked at 1.1 GHz, the first mobile silicon to handle Unreal Engine 5 Nanite assets in real time.[1]Qualcomm Inc., “Snapdragon 8 Elite Launch Highlights,” qualcomm.comThis convergence between mobile and desktop experiences expands the addressable base for discrete graphics beyond PCs into handheld devices. Cloud gaming services coexist rather than cannibalize hardware demand because competitive players still prefer local rendering for latency-sensitive titles.

Government Initiatives Such as Make-in-India Boosting Local GPU Manufacturing

Semicon India 2.0 raised incentives to INR 76,000 crore (USD 9.1 billion), and Tata Electronics broke ground on a USD 11 billion fab in Gujarat set for 50,000 wafer starts per month across 110-nm to 28-nm nodes. Design-linked subsidies already produced 16 tape-outs and seven silicon spins by 2025, showing that the ecosystem extends from EDA to OSAT. Though volume GPU output is unlikely before 2028, policy clarity signals a roadmap for tariff relief once domestic yield ramps, promising lower total cost of ownership for buyers in the India discrete GPU market.

Proliferation of OTT Video Creation Tools Needing Real-Time Rendering

RTX 50-series cards now encode and decode 4:2:2 10-bit streams, delivering 75% faster UltraNR noise reduction than the prior generation.[2]Intel Corp., “Intel and Tata Electronics Sign Foundry MOU,” intel.com Adobe Premiere Pro exports shorten by 30% on RTX 5090 laptops, allowing editors to hit same-day deadlines.[3]Nvidia Corp., “Introducing RTX 50 Series,” nvidia.comWith Hotstar, Zee5, and SonyLIV ordering thousands of hours of regional shows annually, post-production studios in Mumbai, Hyderabad, and Chennai have standardized on discrete GPUs for 4K timelines. The creative push keeps workstation demand buoyant even as consumer gaming saturates.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent import tariffs inflating BOM costs | -3.2% | Nationwide, hits all imported cards and components | Short term (≤ 2 years) |

| Power infrastructure deficits limiting high-end GPU deployment | -2.8% | Acute in tier-2 and tier-3 grids | Medium term (2-4 years) |

| Scarcity of PCIe Gen5 supply-chain nodes in India | -1.5% | Datacenter and workstation segments | Medium term (2-4 years) |

| Fragmented after-sales service network for workstation-grade GPUs | -1.1% | Tier-2 and tier-3 city coverage gaps | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Persistent Import Tariffs Inflating BOM Costs

Graphics boards under HS 85439000 attract 7.5% customs duty, 10% social-welfare cess, and 18% IGST, pushing retail tags 15-20% above landed cost. Currency drift from INR 82 to INR 85 per USD by early 2026 adds another 3-4% to invoices. Hyperscalers mitigate the hit with direct OEM deals, but small system builders lack that leverage. Until local assembly scales, tariff uncertainty will keep mainstream buyers on the fence, shaving points off the India discrete GPU market CAGR.

Power Infrastructure Deficits Limiting High-End GPU Deployment

AI racks drawing 150 kilowatts collide with grids designed for 20-kilowatt legacy servers. Deloitte forecasts data center demand hitting 40-45 TWh by 2030, the equivalent of a midsize state’s annual consumption. Operators resort to captive generators, which raise capex by double digits and complicate ESG reporting. Without accelerated transmission upgrades, deployments in secondary cities may stall, tempering the long-run expansion of the India discrete GPU market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Application: Datacenter Accelerators Anchor Growth

Servers and datacenter accelerators represented 38.62% of India discrete GPU market share in 2025, and the segment is poised for a 20.45% CAGR through 2031. Yotta’s USD 2 billion order for 20,736 Nvidia Blackwell Ultra modules exemplifies hyperscaler preference for purpose-built AI silicon. The India discrete GPU market size tied to PCs and workstations remains robust as esports and content creation flourish, yet growth tails off compared with rack-scale deployments. Mobile devices leverage integrated GPUs like Snapdragon 8 Elite’s Adreno, blurring category lines but contributing modest revenue slices. Automotive ADAS and edge robotics emerge as niche adopters, introducing new verticals that broaden demand but will not outrun datacenter volume this decade.

The strategic calculus is clear: deploying one H100-class board offsets the need for a dozen consumer GPUs, saving rack space and power. Consequently, enterprise budgets are tilting toward AI accelerators, accelerating the revenue shift even if unit volumes skew to mid-tier parts. The India discrete GPU industry continues to cultivate enthusiast communities, but hyperscale orders will dominate supplier roadmaps. Integrators that co-design full AI fabrics, as TCS does with AMD MI455X clusters, are raising the bar for turnkey performance and displacing traditional OEM configurations.

By Memory Type: HBM Gains Share Despite GDDR Dominance

GDDR parts commanded 68.94% of India discrete GPU market share in 2025 because they strike the optimal price-performance balance for gaming and mainstream AI inference. Yet HBM-equipped devices will register a 20.73% CAGR to 2031 as model sizes vault past the 100 billion-parameter line. AMD Instinct MI455X and Nvidia Blackwell Ultra both wire in HBM3 or HBM3e, supplying up to 8 TB/s of bandwidth. The India discrete GPU market size linked to HBM is constrained by supply: SK Hynix, Samsung, and Micron allocate early-run volumes to the largest cloud buyers, leaving smaller firms in the queue. Cost deltas of USD 500-1,000 per GPU keep GDDR compelling for mid-tier cards while GDDR7 promises bandwidth boosts to 1.5 TB/s by 2027.

Operators navigate a trade-off: pack more GDDR boards per rack or fewer high-bandwidth cards with faster time-to-train. Large buyers like Yotta and TCS opt for HBM despite sticker shock, betting on future-proofing, while regional clouds wait for prices to normalize. This bifurcation should persist, with GDDR-centric SKUs dominating unit shipments and HBM clustering around premium revenue slices of the India discrete GPU market.

By Performance Tier: AI Accelerators Outpace Consumer Segments

High-performance consumer boards in the USD 400-1,200 band held 36.73% market share in 2025, catering to gamers and creators. But accelerators priced above USD 1,200 will grow faster at a 20.68% CAGR through 2031, powered by enterprise AI budgets. Intel’s Gaudi 3 claims 50% better throughput than Nvidia H100 and has already signed Airtel, Infosys, and Ola Krutrim. NVIDIA’s RTX 50 family compresses professional features into gamer cards, blurring traditional tiers, yet the price-performance edge still favors datacenter SKUs for large-scale deployments.

Mainstream GPUs under USD 400 continue to sell in volume among price-conscious buyers, but razor-thin margins limit channel enthusiasm. Low-cost sub-USD 100 boards serve legacy refreshes yet contribute little revenue. Overall, the India discrete GPU market size may register more units at mid-range prices, but dollar growth funnels toward AI accelerators.

Geography Analysis

Metropolitan clusters, Mumbai, Bengaluru, Hyderabad, Chennai, and Pune, accounted for roughly 60% of the India discrete GPU market size in 2025. Hyperscaler megaprojects, such as Microsoft’s USD 17.5 billion expansion and Google’s USD 15 billion southern campus, install GPU-dense racks that dwarf consumer demand. Tier-2 centers are catching up: DeepTek.ai’s 650-plus radiology deployments spread across 21 states, and Achala Health fine-tunes Med Gemini models in semi-urban hospitals, introducing professional GPUs to underserved regions.

Gujarat and Assam are emerging semiconductor hubs, with Tata Electronics’ USD 11 billion fab at Dholera and an Intel-linked OSAT in Jagiroad, signaling supply-chain localization plans. After-sales coverage still skews to metros; ASUS, Gigabyte, and Zotac run carry-in models that leave customers in smaller cities waiting more than 10 days for RMA turnaround. North and East India trail South and West in datacenter density, but the IndiaAI Mission intends to spread 63,000 GPUs nationwide by 2027, easing the geographic concentration of compute.

Decentralized platforms such as GPU.Net aggregate idle cards across secondary cities, renting cycles to AI startups at rates below hyperscaler lists. Although reliability hurdles persist, these models hint at future elasticity for the India discrete GPU market. Grid constraints remain a wild card: without accelerated transmission projects, growth may continue to cluster where power is stable, slowing rural penetration.

Competitive Landscape

NVIDIA maintains a dominant datacenter share, but AMD lifted its India footprint to roughly 20-25% of deployments in 2025, while Intel’s Gaudi 3 targets parity on training and inference metrics. Add-in-board vendors, ASUS, Gigabyte, MSI, Zotac, Colorful, Sapphire, Palit, Galax, and Leadtek- compete on warranty extensions and regional service but concede direct hyperscaler deals to GPU makers. The September 2025 Nvidia-Intel USD 5 billion cross-investment underscores a trend toward vertically integrated silicon roadmaps.

Startups like GPU.Net, Pictor Network, and Lumora AI harvest idle desktop cards into decentralized clouds, squeezing hyperscaler pricing for burst inference workloads. TCS-AMD Helios stacks illustrate how integrators co-design full racks to maximize ROCm performance, bypassing legacy server OEMs. Mobile GPU suppliers, Qualcomm, Apple, and MediaTek, chip away at light AI and creative workloads, but discrete boards still dominate high-end performance corridors. Regulatory clarity remains patchy; BIS handles electromagnetic compliance, while tariff codes drive import friction, leaving room for policy harmonization that could reshape competitive dynamics.

India Discrete GPU Industry Leaders

NVIDIA Corporation

Advanced Micro Devices Inc.

Intel Corporation

ASUS Tek Computer Inc.

Arm Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: TCS and AMD unveiled the Helios rack-scale architecture, powered by Instinct MI455X GPUs, across a 200-megawatt footprint at the HyperVault AI Data Center.

- February 2026: NVIDIA launched AI factory partnerships with India’s leading manufacturers and academic labs to scale Nemotron model adoption.

- January 2026: Yotta Data Services committed USD 2 billion for 20,736 Nvidia Blackwell Ultra GPUs, with deployment slated by Aug 2026.

India Discrete GPU Market Report Scope

A discrete GPU, or discrete graphics processing unit, is a dedicated hardware component designed exclusively to handle graphics rendering and parallel computational tasks, operating independently from the central processing unit (CPU) with its own dedicated video memory (VRAM) and power circuitry.

The India Discrete GPU The Germany Discrete GPU Market Report is Segmented by Device Application (Mobile Devices and Tablets, PCs and Workstations, Servers and Datacenter Accelerators, Gaming Consoles and Handhelds, Automotive/ADAS, and Other Embedded and Edge Devices), Memory Type (GDDR-based GPUs, and HBM-based GPUs), Performance Tier (Low-Cost GPUs (less than 100 USD), Mainstream GPUs (100 USD to 400 USD), High-Performance Consumer GPUs (400 USD to 1,200 USD), and Data Center / AI Accelerator GPUs (greater than 1,200 USD)). The Market Forecasts are Provided in Terms of Value (USD).

| Mobile Devices and Tablets |

| PCs and Workstations |

| Servers and Datacenter Accelerators |

| Gaming Consoles and Handhelds |

| Automotive / ADAS |

| Other Embedded and Edge Devices |

| GDDR-based GPUs |

| HBM-based GPUs |

| Low-Cost GPUs (less than 100 USD) |

| Mainstream GPUs (100 USD to 400 USD) |

| High-Performance Consumer GPUs (400 USD to 1,200 USD) |

| Data Center / AI Accelerator GPUs (greater than 1,200 USD) |

| By Device Application | Mobile Devices and Tablets |

| PCs and Workstations | |

| Servers and Datacenter Accelerators | |

| Gaming Consoles and Handhelds | |

| Automotive / ADAS | |

| Other Embedded and Edge Devices | |

| By Memory Type | GDDR-based GPUs |

| HBM-based GPUs | |

| By Performance Tier | Low-Cost GPUs (less than 100 USD) |

| Mainstream GPUs (100 USD to 400 USD) | |

| High-Performance Consumer GPUs (400 USD to 1,200 USD) | |

| Data Center / AI Accelerator GPUs (greater than 1,200 USD) |

Key Questions Answered in the Report

How fast will AI accelerators grow within India’s GPU segment?

The data center and AI accelerator tier priced above USD 1,200 is projected to log a 20.68% CAGR between 2026 and 2031 as hyperscalers and government AI programs favor purpose-built silicon.

Which memory technology is gaining share in Indian data centers?

High-bandwidth memory (HBM) GPUs will rise at a 20.73% CAGR through 2031, driven by the need for multi-terabyte-per-second bandwidth to train large language models.

What share do servers and accelerators hold today?

Servers and datacenter accelerators already account for 38.62% of 2025 revenue, making them the largest device application slice.

Are import tariffs likely to change soon?

Policy drafts under PLI 2.0 hint at lower duties once domestic assembly ramps, but no firm timeline has been issued, keeping near-term pricing volatile.

Page last updated on: