South Korea Mining Equipment Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

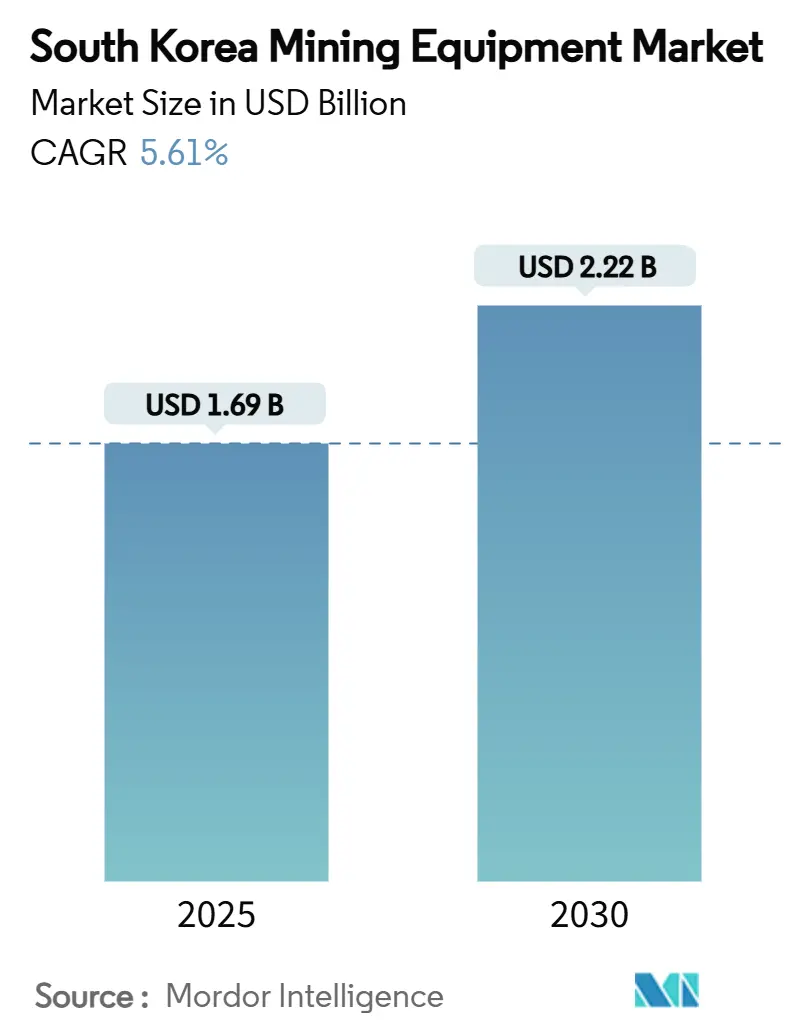

| Market Size (2025) | USD 1.69 Billion |

| Market Size (2030) | USD 2.22 Billion |

| Growth Rate (2025 - 2030) | 5.61% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Korea Mining Equipment Market Analysis by Mordor Intelligence

The South Korea mining equipment market size is currently valued at USD 1.69 billion and is projected to reach USD 2.22 billion by 2030, delivering a 5.61% CAGR over 2025-2030. Persistent import-substitution goals, a widening critical-minerals gap, and escalating autonomy mandates position the South Korea mining equipment market for steady mid-single-digit expansion. Excavators, surface operations, and metal mining continue to anchor revenues, yet the fastest growth stems from battery-electric powertrains, underground deployments, and fully autonomous systems. POSCO and HD Hyundai, leaders in heavy industry, are spearheading equipment upgrades by localizing their lithium, nickel, and tungsten supply chains. Meanwhile, 5G-enabled private networks, Tier-4 final engine retrofits, and KRW 55 trillion in state exploration subsidies underpin a favorable investment climate even as operator shortages and used-equipment inflows weigh on near-term margins.

Key Report Takeaways

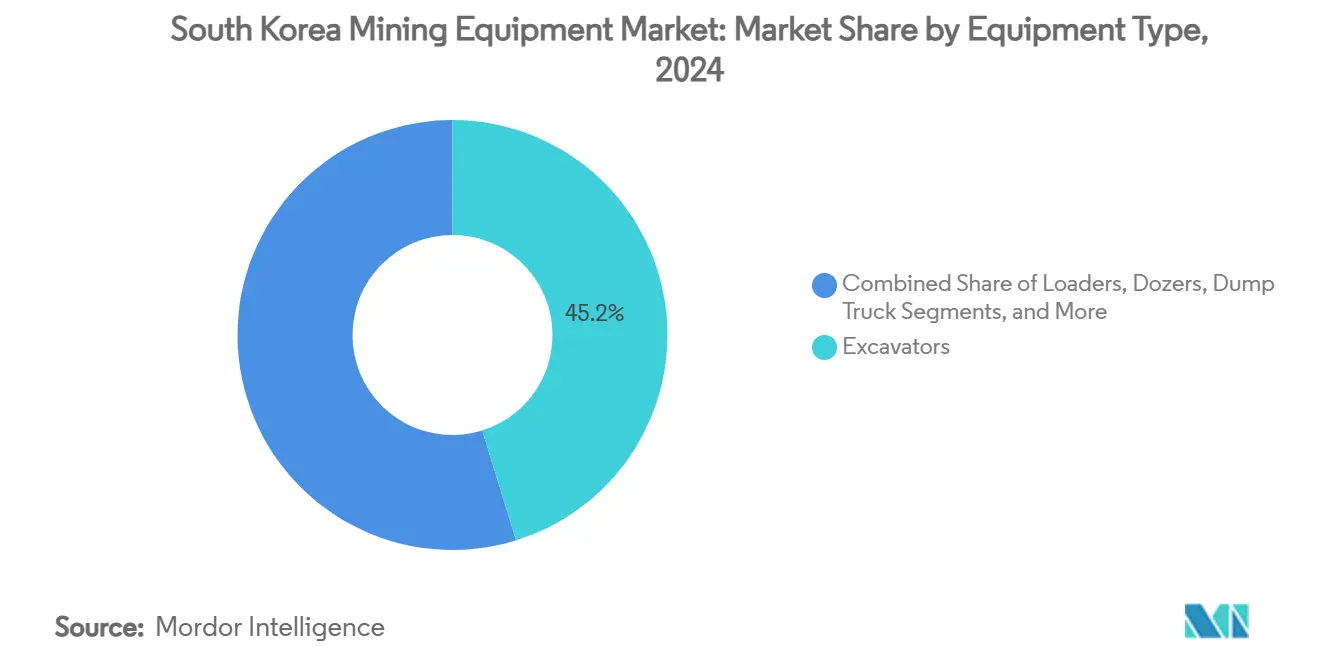

- By equipment type, excavators led the South Korean mining equipment market, with 45.21% of the share in 2024; the same category is projected to expand at a 5.97% CAGR through 2030.

- By mining method, surface operations accounted for 66.43% of the South Korea mining equipment market share in 2024, whereas underground mining is advancing at a 6.46% CAGR to 2030.

- By application, metal mining captured a 49.85% share of the South Korea mining equipment market size in 2024, and mineral mining is set to grow at a 6.93% CAGR through 2030.

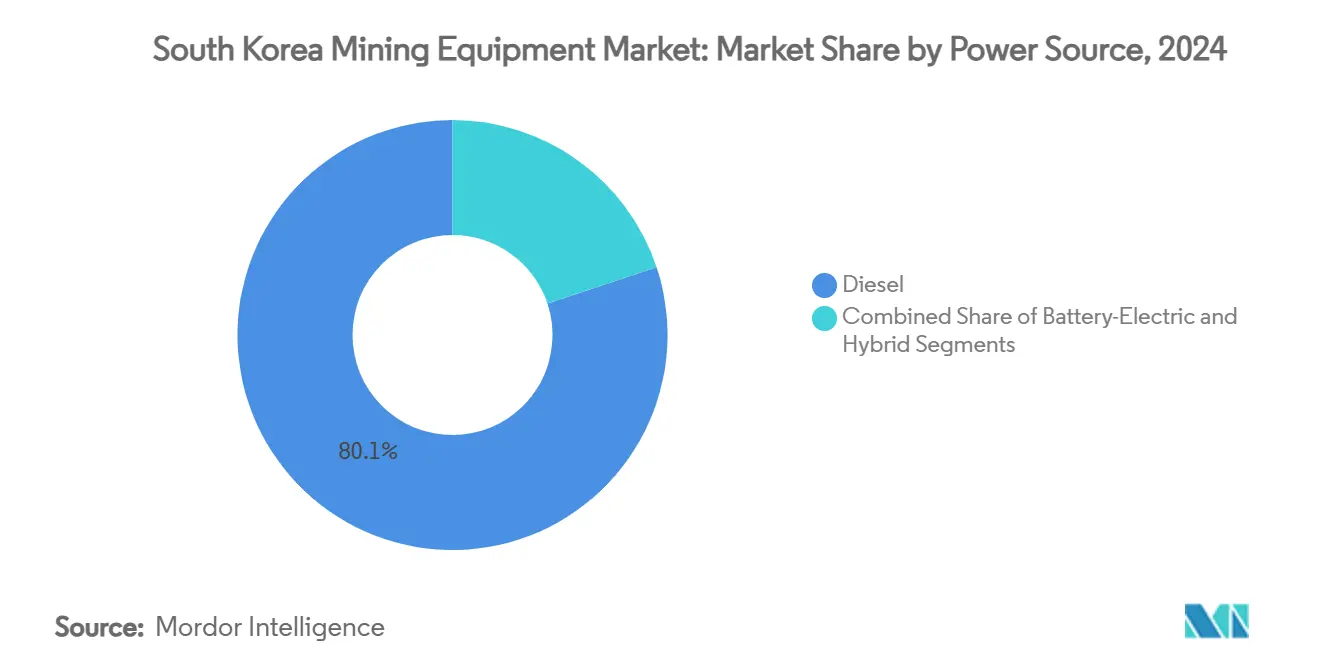

- By power source, diesel equipment dominated the South Korea mining equipment market, with an 80.13% share in 2024, while battery-electric alternatives are rising at an 8.13% CAGR over 2025-2030.

- By automation level, manual systems held 74.17% of the South Korea mining equipment market share in 2024, yet fully autonomous solutions are poised for a 15.16% CAGR to 2030.

- By geography, the Seoul Capital Area controlled 45.33% of the South Korea mining equipment market share in 2024 and Yeongnam is forecast to log the fastest 7.11% CAGR to 2030.

South Korea Mining Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Electrification Push from Steel and Battery Giants | +1.2% | Seoul Capital Area, Yeongnam | Medium term (2-4 years) |

| Critical-Minerals Exploration Subsidies | +0.9% | National, early gains in Yeongnam and Hoseo | Long term (≥4 years) |

| Tier-4 Final Engine Retrofit Program (2027) | +0.8% | National | Short term (≤2 years) |

| Mine-site 5G Private Networks | +0.7% | Seoul Capital Area, Yeongnam | Medium term (2-4 years) |

| OEM-agnostic “K-SmartMine” Data Platform | +0.5% | National | Medium term (2-4 years) |

| Rare-earth Process-waste Recycling | +0.4% | Seoul Capital Area, Honam | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Electrification push from domestic steel and battery giants

The South Korean steel giant POSCO has announced a bold investment strategy, pledging 121 trillion won (equivalent to $88 billion) by 2030. Of this, a significant 45 trillion won (around $35 billion) will be directed towards international markets, all aimed at pioneering new emissions reduction initiatives. This amplifies orders for battery-electric excavators, loaders, and haul trucks for its facilities.

Additionally, the steelmaker’s demand for high-precision surface drills and crushers is high. Mandatory battery-traceability disclosures by Hyundai Motor and Kia deepen pressure on upstream traceability, forcing mines to install sensor-rich, data-ready equipment that integrates with K-SmartMine dashboards. Concurrently, LG Energy Solution and SK On’s overseas cell-plant build-outs magnify domestic scramble for mineral security, sustaining multi-year equipment procurement cycles for primary extraction and urban-mining recyclers.

Government-backed critical-minerals exploration subsidies

South Korea is investing significantly to reduce import dependence on critical minerals by offering grants covering up to 30% of the capital expenditure for Tier-4 final compliant drills, autonomous LHDs, and ore-sorting systems.[1]“Critical Minerals Subsidy Framework,” Ministry of Trade, Industry & Energy, mk.co.kr. As the lead nation within the Minerals Security Partnership, Seoul aligns subsidy disbursement with joint procurement schemes that lower per-unit costs for high-spec equipment. Revitalizing the Sangdong tungsten mine exemplifies subsidy effectiveness, driving orders for narrow-vein jumbos, battery-powered haulers, and advanced ventilation packages. Expanded stockpiling capacity from 54 to 100 days elevates demand for specialized handling cranes, palletizers, and real-time stock-monitoring sensors.

Mandatory retrofit program for Tier-4-final engines (2027)

In the coming years, every in-service diesel engine exceeding 56 kW will comply with Tier-4 final NOx and PM standards, spurring a swift fleet renewal in South Korea's mining equipment market. Operators weigh retrofit kits against full replacements, yet total cost of ownership analyses increasingly favor battery-electric units with lower ventilation and fuel overheads. The rule also compels the acquisition of SCR-ready gensets, acoustic dampers, and aftertreatment diagnostics, benefiting component suppliers with compliance-centric product lines. Noise-emission curbs around urban pits reinforce parallel demand for low-decibel rigs and electric drivetrains optimized for night-shift operations.

Mine-site 5G private-network roll-outs enabling autonomy

Some active mine sites now benefit from dedicated 5G slices, achieving latency levels below 10 ms. This advancement supports crucial applications such as tele-remote loading and autonomous drilling. Additionally, AI-driven predictive maintenance boosts both operational efficiency and safety in mining operations. Early adopters report productivity jumps as high as 70% and opex savings topping 20% after integrating edge-AI with high-resolution equipment telemetry. Seoul’s spectrum policy, which reserves 28 GHz blocks for industrial campuses, speeds deployment versus competing jurisdictions, pushing OEMs to pre-install 5G modems, LiDAR arrays, and multi-band antennas. Underground trials using LiDAR-guided robots in GPS-denied stopes demonstrate frontier use cases that promise to narrow operator shortfalls.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Skilled-operator Shortage | -0.8% | National, acute in Seoul Capital Area | Short term (≤2 years) |

| Volatile LG and SK Capex Cycles | -0.6% | Seoul Capital Area, Yeongnam | Medium term (2-4 years) |

| Strict Noise-Emission Limits | -0.4% | Seoul Capital Area, urban peripheries | Long term (≥4 years) |

| Rising Used-Equipment Imports | -0.3% | National, port cities | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Chronic skilled-operator shortage inflating labor costs

An aging workforce and limited mining curricula leave haul-truck utilization rates languishing below 65%, pushing wages up by 18% in 2024 alone [2] “Workforce Trends in Korean Mining,” Korean Society of Mineral & Energy Resources Engineers, ksmer.org. Autonomous retrofits partly offset shortages yet require higher-skilled technicians, perpetuating the talent deficit. Cross-industry poaching by the semiconductor sector exacerbates churn, inflating training budgets and stretching maintenance schedules.

Volatile LG- and SK-controlled capex cycles

LG Chem and SK Innovation’s battery-material pivots can swing quarterly procurement for crushers, dryers, and bulk-handling systems by ±25%, undermining forecast accuracy for OEMs. Their technology bets, from solid-state electrolytes to sodium-ion cells, frequently redirect funds between cathode and precursor plants, cascading order volatility through upstream equipment tiers. Recent Bobcat-Doosan Robotics consolidation further concentrates purchasing power, sharpening price negotiations with component suppliers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Equipment Type: Excavators drive market leadership

Excavators captured 45.21% of 2024 revenues and remain the fastest-expanding line item with a 5.97% CAGR, keeping the South Korea mining equipment market size firmly anchored in high-mobility digging solutions. Their modular boom designs allow rapid switching between rock-bucket, ripper, and hammer attachments, crucial for multi-ore sites ranging from Gwangyang’s nickel laterites to Honam’s limestone benches. Loaders follow as material-handling workhorses feeding surge bins at battery precursor plants, while dozers specialize in tailings-dam lifts and haul-road maintenance. Dump-truck demand accelerates as fully-autonomous haulage systems prove 15% cheaper per ton than manned fleets over five-year horizons, supporting expansion of 100-t class battery-electric rigid-frame models. Drills and breakers flourish in underground stoping where precision charge placement and vibration control enhance ore recovery. Screening and crushing packages enjoy tailwinds from rare-earth waste-recycling streams that require fine-particle liberation.

Excavator vendors leverage 5G tele-remote kits and AI-based swing-angle optimization to trim cycle times by 8%, translating into quantifiable productivity gains that underpin repeat orders. Load-sense hydraulic circuits and high-pressure fuel injectors help Tier-4 final diesel variants meet emission thresholds without power sacrifices. Premium buyers gravitate toward battery-electric crawler platforms equipped with 600 kWh fast-swap packs, gaining up to 12 hour shifts in underground stopes with no exhaust aftertreatment. Such features allow excavators to preserve the largest slice of the South Korea mining equipment market share while remaining innovation leaders.

By Mining Method: Surface operations dominate despite underground potential

Surface mines generated 66.43% of 2024 revenues as open-pit limestone and aggregates feed Seoul’s infrastructure pipeline, yet underground ventures are expected to post the stronger 6.46% CAGR and will nudge the South Korea mining equipment market toward higher-spec jumbos, narrow-vein LHDs, and battery-powered roof bolters. Renewed tungsten output at Sangdong and polymetallic prospects in Gangwon province highlight the shift. Advanced ground-penetrating radar and smart-blast analytics elevate extraction factors, while remote-loader teleremote cabins stationed 3 km away from faces improve safety metrics. Surface operations keep expanding thanks to large-format excavators with 12 m^3 buckets, high-throughput stationary crushers, and dust-suppression sprayers that comply with tougher PM2.5 limits.

Hybrid mining models are gaining attention: operators use surface box-cut entries to access deeper orebodies, transitioning to sublevel stoping as depth increases. This integrated approach requires flexible fleets capable of redeployment, benefiting OEMs that supply interchangeable power modules and modular drivetrain kits. 5G network backhaul common to both surface and underground zones further promotes unified command centers where fleet dispatchers optimize shovel-truck pairings across the two environments.

By Application: Metal mining leads while mineral processing accelerates

Metal mining retained a 49.85% share in 2024, sustained by enduring steel-grade iron ore, molybdenum, and copper output for domestic mills. Yet mineral mining, covering lithium, nickel, and rare-earths, is expected to post a 6.93% CAGR, lifting its slice of the South Korea mining equipment market size as EV supply chains mature. Coal, once dominant, now occupies a niche for specialty coke and industrial boilers, prompting a pivot to low-emission continuous-miner systems. Urban-mining plants reclaim cobalt and palladium from e-scrap; their micro-shredders and eddy-current separators fuel “mineral” category outperformance.

In metal streams, integrated slag-handling robots mitigate labor shortages at steel complexes, whereas mineral players deploy containerized SX-EW units near port refineries to shorten turnaround. POSCO’s Gwangyang campus integrates a 25 MW solar array that supplies surplus energy to lithium-brine evaporators, illustrating cross-sector sustainability alignment. Such operational overlap merges traditional definitions, yet the South Korea mining equipment market continues to segment budgets along metal versus mineral boundaries for procurement clarity.

By Power Source: Diesel dominance faces electric disruption

Diesel engines powered 80.13% of active fleets in 2024, but battery-electric rigs are expected to achieve an 8.13% CAGR and constitute the lodestar of future orders. Mid-size loaders with 200 kWh lithium-iron-phosphate packs deliver zero-tailpipe emissions critical for underground air-quality compliance. Fast-charge nodes stationed along decline ramps replenish 80% capacity in 30 minutes, shrinking idle time. Hybrid genset-battery combinations bridge remote pits lacking grid tie-ins, extending diesel relevance while meeting Tier-4 mandates. Hydrogen fuel-cell prototypes remain nascent, yet early pilot trucks at Ulsan metallurgical complexes demonstrate eventual multi-fuel diversification.

OEMs retrofit legacy diesel frames with modular battery trays to extend life cycles, maintaining supply-chain continuity as suppliers consolidate around high-voltage connectors, immersion-cooled packs, and ISO-15118 charging interfaces. Carbon pricing scenarios further tilt total-cost-of-ownership math toward electric options, accelerating second-generation battery truck launches within the South Korea mining equipment market.

By Automation Level: Manual operations persist amid autonomous surge

Manual systems controlled 74.17% of the installed base in 2024, yet fully-autonomous fleets are expected to compound at 15.16% CAGR as operator scarcity and safety imperatives align. Semi-autonomous trucks equipped with collision-avoidance radar and lane-centering arrive first because they dovetail with existing haul-road layouts. Full autonomy blossoms where 5G and edge-AI are present, yielding truck-shovel networks that self-organize loading queues and reroute around maintenance zones. Underground loaders adopt auto-mucking cycles guided by LiDAR-based SLAM for zero-visibility drifts.

Stakeholders benchmark Net-Present-Value gains: autonomous haulage cuts unit cost by USD 0.45 per ton and boosts annual output by 7% on average, justifying capital surcharges. OEMs bundle autonomy licenses with hardware sales, migrating toward recurring software revenue that hedges cyclical equipment demand. Such platform economics ensure autonomous systems gain share rapidly within the South Korea mining equipment market.

Geography Analysis

The Seoul Capital Area leads the South Korea mining equipment market with a 45.33% share, leveraging its dense financial ecosystem and service hubs. Decision-makers headquartered here centralize capex approvals, but stringent municipal noise curbs constrain in-city demonstration grounds, prompting OEMs to establish satellite proving sites in adjacent Gyeonggi Province. Rental companies concentrate inventories near Incheon port, catering to rapid turnaround projects but facing land-cost inflation that nudges warehouses toward farther suburbs.

Yeongnam’s is expected to compound 7.11% CAGR stems from POSCO’s Gwangyang and Pohang expansions, SK’s cathode precursor plants, and CNGR’s nickel refinery JV, all of which demand truck-shovel fleets, dust-collection systems, and slag-handling robots. The region benefits from shipbuilding synergies: shared fabrication yards, machine heavy-equipment chassis, while automotive suppliers diversify into mining-grade hydraulics, anchoring local supply chains.

Honam and Hoseo regions collectively target limestone, kaolin, and construction aggregates. Honam’s well-established rail links feed ready-mix concrete plants in coastal industrial parks, ensuring steady loader, crusher, and conveyor orders. Hoseo capitalizes on central-corridor logistics, with equipment dealerships positioned along the Daejeon-Sejong route to service smaller quarries and tunneling projects tied to high-speed-rail extensions.

Competitive Landscape

The South Korea mining equipment market remains moderately fragmented. Caterpillar, Komatsu, and Hitachi share the top tier with a combined 38% share, but Hyundai Doosan Infracore’s 34.4% stake acquisition by HD Hyundai vaults the domestic player into a formidable challenger position. Market entry barriers center on emissions compliance, autonomy software, and after-sales support networks rather than purely on manufacturing scale.

Global OEMs are partnering with Korean telecom carriers to embed 5G modems and edge-AI chips into haulage fleets. Epiroc secured a SEK 2.2 billion contract for fully-electric drill rigs that slash CO₂ emissions by 90% and interface seamlessly with Korean 28 GHz networks[3] “SEK 2.2bn Korean Order Announcement,” Epiroc AB, epiroc.com. Sandvik’s AutoMine deployment at Seongshin Minefield introduced the country’s first autonomous underground dump truck fleet, boosting daily mucking rates by 20%.

Domestic mid-caps such as AJ Power and Dong-A Hwasung Machine carve niches in retrofit exhaust systems and high-pressure pumps, respectively. Robotics startups integrate Boston-Dynamics-inspired quadrupeds for conveyor-belt inspections, signaling future competition from non-traditional players. Overall, digital ecosystem depth dictates sustained advantage, compelling hardware firms to bundle sensor suites, analytics dashboards, and cybersecurity layers into integrated proposals.

South Korea Mining Equipment Industry Leaders

Caterpillar Inc.

Komatsu Ltd.

Hyundai Doosan Infracore

Hitachi Construction Machinery

Volvo Construction Equipment

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: HD Hyundai opened a EUR 131 million smart factory in Ulsan, elevating annual excavator and wheel-loader capacity from 9,600 to 15,000 units through AI-driven automation and predictive maintenance platforms.

- January 2023: Sandvik deployed AutoMine-enabled Toro™ TH545i autonomous underground dump trucks at Seongshin Minefield, marking South Korea’s inaugural use of autonomous haulage in limestone mining.

South Korea Mining Equipment Market Report Scope

| Excavators |

| Loaders |

| Dozers |

| Motor Graders |

| Dump Trucks |

| Drills and Breakers |

| Crushing, Pulverizing and Screening |

| Others |

| Underground Mining |

| Surface Mining |

| Metal Mining |

| Mineral Mining |

| Coal Mining |

| Diesel |

| Battery-Electric |

| Hybrid |

| Manual Equipment |

| Semi-Autonomous |

| Fully-Autonomous |

| Seoul Capital Area |

| Yeongnam (South-East) |

| Honam (South-West) |

| Hoseo (Central) |

| Others |

| By Equipment Type | Excavators |

| Loaders | |

| Dozers | |

| Motor Graders | |

| Dump Trucks | |

| Drills and Breakers | |

| Crushing, Pulverizing and Screening | |

| Others | |

| By Mining Method | Underground Mining |

| Surface Mining | |

| By Application | Metal Mining |

| Mineral Mining | |

| Coal Mining | |

| By Power Source | Diesel |

| Battery-Electric | |

| Hybrid | |

| By Automation Level | Manual Equipment |

| Semi-Autonomous | |

| Fully-Autonomous | |

| By Geography | Seoul Capital Area |

| Yeongnam (South-East) | |

| Honam (South-West) | |

| Hoseo (Central) | |

| Others |

Key Questions Answered in the Report

How large is the South Korea mining equipment market in 2025?

The market is valued at USD 1.69 billion and is forecast to reach USD 2.22 billion by 2030.

Which equipment category generates the most revenue?

Excavators lead with a 45.21% share in 2024 and continue to expand fastest at a 5.97% CAGR.

What region shows the highest growth momentum?

Yeongnam in South-East Korea is projected to grow at a 7.11% CAGR through 2030 due to steel and battery material investments.

How fast are battery-electric machines growing?

Battery-electric mining equipment is expected to grow at an 8.13% CAGR as operators pivot away from diesel.

Page last updated on: