South Korea Cloud Computing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

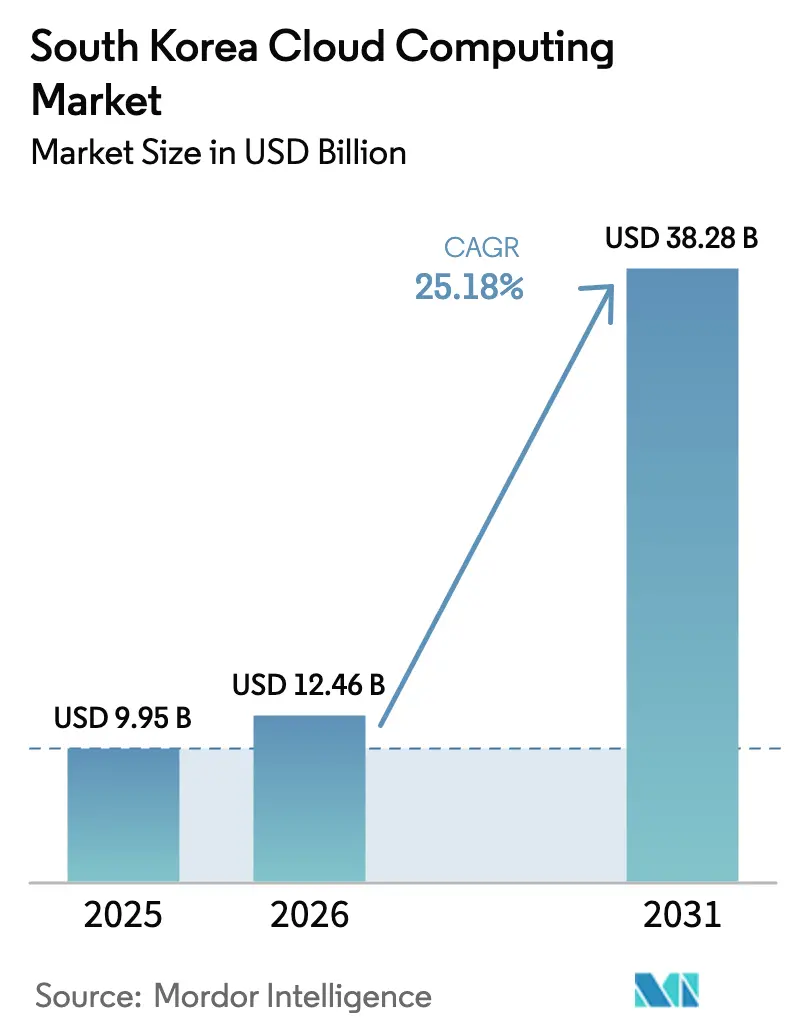

| Base Year Market Size (2025) | USD 9.95 Billion |

| Market Size (2026) | USD 12.46 Billion |

| Market Size (2031) | USD 38.28 Billion |

| Growth Rate (2026 - 2031) | 25.18% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Korea Cloud Computing Market Analysis by Mordor Intelligence

The South Korea Cloud Computing Market size is expected to grow from USD 9.95 billion in 2025 to USD 12.46 billion in 2026 and is forecast to reach USD 38.28 billion by 2031 at 25.18% CAGR over 2026-2031. Rapid public-sector digitalization, subsidized SME adoption, and record hyperscaler investments reinforce this upward trajectory. Intensifying AI workloads, 5G-enabled edge applications, and sovereign-cloud mandates are steering provider strategies toward value-driven differentiation. Enterprise demand for scalable, compliance-ready platforms has elevated hybrid architectures, while AI-native services are redefining monetization models. At the same time, rising cybersecurity threats and data-residency rules are shaping risk-management budgets and influencing vendor selection across the South Korea cloud computing market.[1]Ministry of Science and ICT, “Major R&D Budget for 2025 Set to Be KRW 24.8 Trillion, the Largest in History,” msit.go.kr

Key Report Takeaways

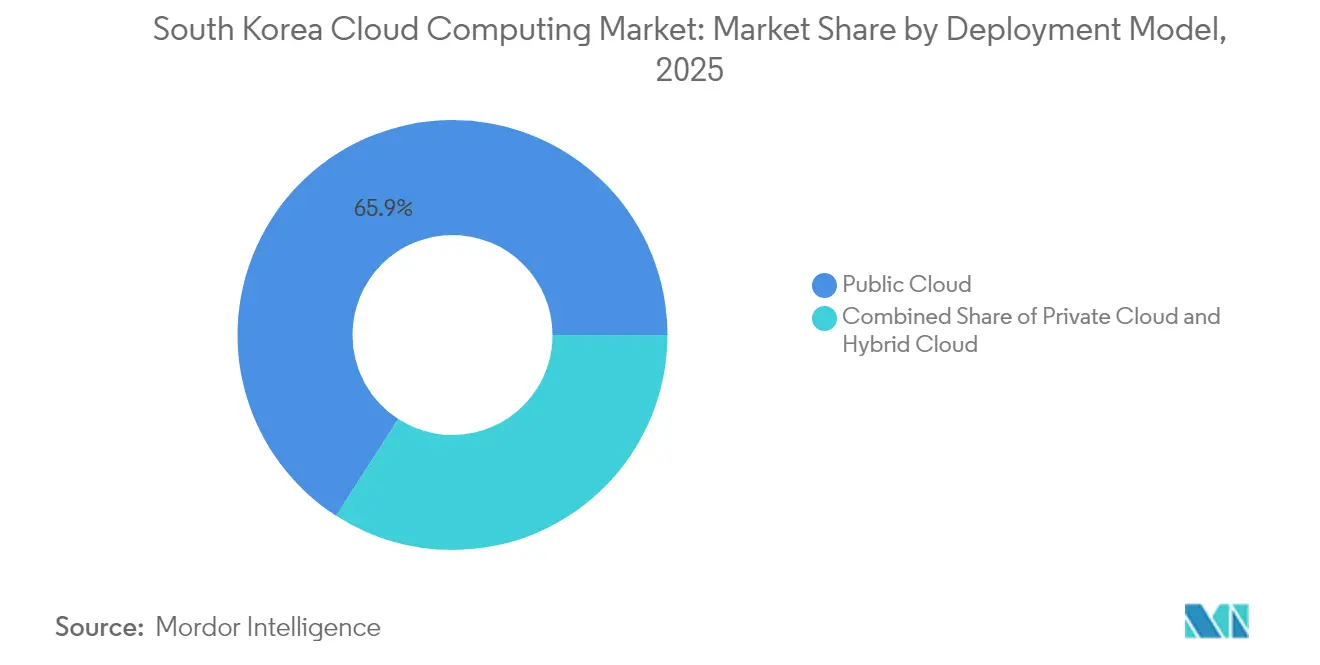

- By deployment model, public cloud held 65.90% of the South Korea cloud computing market share in 2025, whereas hybrid cloud is forecast to post the fastest 28.90% CAGR through 2031.

- By service model, Infrastructure-as-a-Service commanded 47.10% revenue in 2025, while Platform-as-a-Service is primed for a 31.50% CAGR to 2031, reflecting heightened demand for AI development stacks.

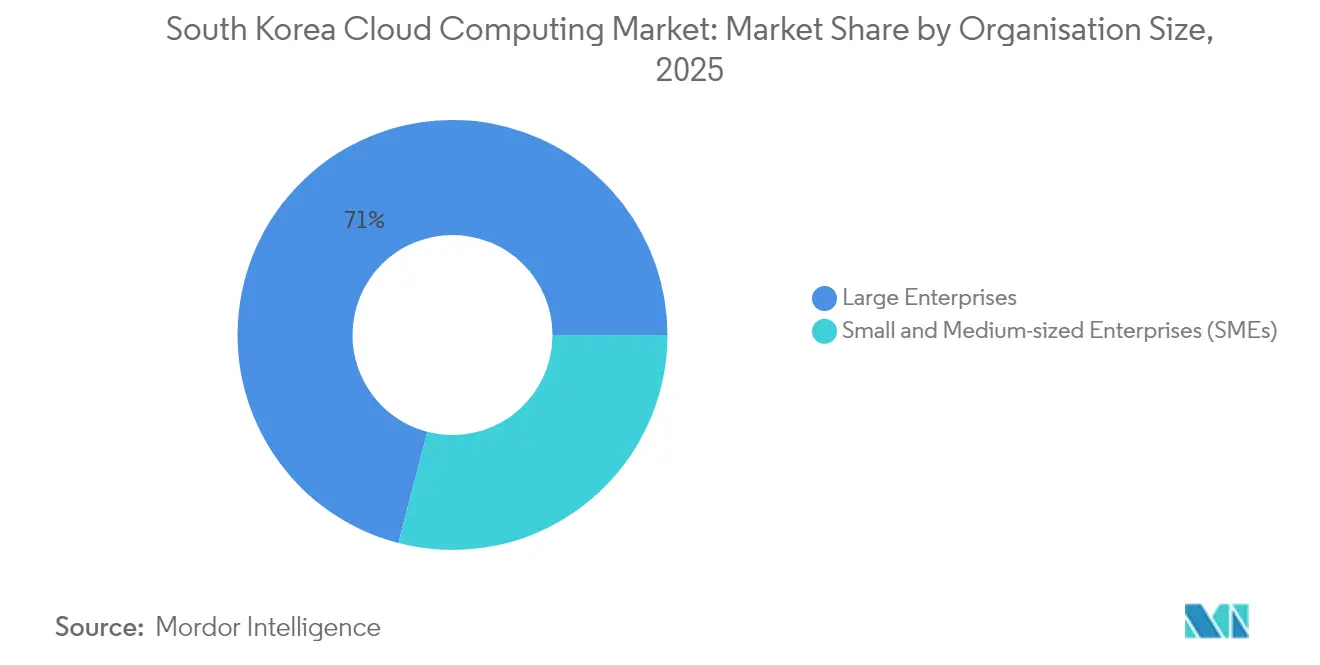

- By organisation size, large enterprises controlled 70.95% of the South Korea cloud computing market size in 2025; SMEs are expanding at 27.20% CAGR under subsidy programs covering up to 80% of adoption costs.

- By end-user industry, BFSI led with 22.95% share of the South Korea cloud computing market size in 2025, while healthcare is advancing at a vigorous 33.40% CAGR to 2031, supported by AI-driven diagnostics.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Dynamics observed within South korea present a country level view when set against the broader international context. The cloud computing market analysis by Mordor Intelligence provides that expanded global perspective.

South Korea Cloud Computing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government cloud-first and digital-platform budgets | +4.2% | Nationwide (Seoul focus) | Medium term (2–4 years) |

| AI/ML workload boom and hyperscale demand | +6.8% | Seoul & Gyeongsang | Short term (≤2 years) |

| Multi-billion-won hyperscaler DC pipeline | +5.1% | Ulsan & Jeollanam-do | Long term (≥4 years) |

| SME cloud subsidy (≤80% cost coverage) | +3.4% | Non-metro emphasis | Medium term (2–4 years) |

| Edge-native 5G ultra-low-latency clouds | +2.9% | Major cities | Short term (≤2 years) |

| MSP consolidation & IPO pipeline | +2.1% | National (Seoul hub) | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Government "Cloud-First" and Digital-Platform budgets surge

The central government has mandated that about 10,000 information systems move to cloud-native stacks by 2030, anchoring the public sector’s largest digital overhaul to date.[2]Samsung SDS, “Digital Government Innovation, Preparing for Hyperscale AI and Cloud,” samsungsds.com Record R&D funding of KRW 24.8 trillion for 2025 directs new money toward AI workloads that depend on elastic, compliance-ready clouds. Streamlined procurement rules under the Digital Service Specialized Contract System shorten project lead times and lower bureaucratic hurdles for vendors. Public adoption validates security frameworks that private firms can reuse, creating a flywheel of confidence in local cloud standards. The initiative also funds a national large-language model, positioning sovereign AI services as a showcase for Korea’s policy-driven cloud growth.

AI/ML workload boom accelerates hyperscale demand

Hyperscale capacity planning has shifted after Naver opened Asia’s largest data-center campus in Sejong, capable of housing 600,000 racks to serve GPU-intensive training jobs.[3]KED Global, “Naver Cloud, NHN Cloud to Co-Work for Hyperscale AI,” kedglobal.com A KRW 1.5 trillion government GPU program is intensifying competition among Naver, Kakao, and others for next-generation AI infrastructure contracts. High-bandwidth memory, liquid cooling, and energy-efficient designs have become standard procurement criteria, raising the specification bar industry-wide. Providers are beginning to swap hourly compute pricing for outcome-based fees tied to AI inference performance. Domestic chip development projects, such as Samsung’s work with Naver, signal an emerging trend toward vertically integrated AI stacks that sit natively in the cloud.

Multi-billion-won hyperscaler DC pipeline (AWS-SK, etc.)

New data-center builds now feature LNG cold-energy cooling and renewable-energy sourcing as AWS and SK Group break ground on a USD 5 billion, 60,000-GPU campus in. LG heir Brian Koo’s USD 35 billion, 3 GW “mega” facility in Jeollanam-do will create one of the world’s most powerful cloud hubs by 2028. These projects extend sovereign-cloud capacity, satisfy data-residency rules, and stimulate local supply chains in construction, power, and advanced cooling. Their scale also attracts co-location tenants and managed-service partners seeking low-latency proximity to hyperscale AI clusters. Long build-out timelines ensure a multi-year tailwind for equipment vendors and regional employment.

SME cloud subsidy covering up to 80% of costs

The SME Cloud Service Distribution and Expansion Project underwrites up to 80% of adoption expenses, capped at KRW 10 million for typical migrations and KRW 80 million for intensive cases. Subsidies bundle consulting and security audits, shifting buyer focus from price to business outcomes. Approved suppliers such as Gabia and Inspien are packaging turnkey solutions that automate electronic data interchange without on-prem-hardware investment. Early results show faster procurement cycles and rising cloud spend outside the Seoul Capital Area. By neutralizing cost hurdles, the program levels the playing field for smaller firms and broadens the market’s geographic reach.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent data-sovereignty & residency mandates | –3.1% | Nationwide (cost variance) | Long term (≥4 years) |

| Escalating cyber-attacks on public clouds | –2.4% | Seoul primary target | Short term (≤2 years) |

| Cost squeeze on domestic MSPs vs. US hyperscalers | –1.8% | National | Medium term (2–4 years) |

| Acute DevOps/FinOps talent shortage | –2.7% | Seoul & beyond | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Stringent data-sovereignty and residency mandates

K-ISMS certification obliges providers to operate domestic security management systems, forcing global vendors to localize hardware and duplicate audit processes. Additional cryptographic-module testing by the National Cyber Security Center adds time and cost layers for public-sector projects. Financial-services guidance now mirrors EU-style AI risk tiers, injecting compliance uncertainty for cloud-based analytics offerings. Local colocation strategies raise capital-expenditure needs and narrow margin profiles for smaller entrants. The evolving rulebook encourages enterprises to adopt hybrid designs that keep sensitive datasets onshore while limiting international workload mobility.

Escalating cyber-attacks on public clouds

Public institutions endure 1.62 million daily hacking attempts, about 80% traced to North Korean actors, spotlighting persistent nation-state threats. The 2025 SK Telecom breach that exposed 27 million user records underscored vulnerabilities in large Linux server estates. Demand for Cloud Architects and Security Specialists has lifted average salaries, inflating operating costs for providers and customers alike. Enterprises managing multi-cloud estates struggle to maintain uniform security controls, driving adoption of niche zero-trust and posture-management tools. Elevated risk perceptions may slow migration of mission-critical workloads until comprehensive remediation frameworks mature.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Model: Hybrid architectures anchor regulated scalability

Hybrid cloud carved a 28.90% CAGR outlook, even as public cloud retained 65.90% dominance in 2025 within the South Korea cloud computing market. Large enterprises allocate sensitive, regulated workloads to private clusters while bursting seasonal demand into public zones, balancing sovereignty with elasticity. The South Korea cloud computing market size for hybrid solutions is on track to expand as Shinsegae Group’s Nutanix-powered strategy illustrates sustained transaction-peak resilience. Government migrations further solidify public-private interoperability blueprints that smaller enterprises emulate.

Policy alignment, industry compliance packs, and integrated FinOps dashboards are accelerating hybrid uptake among banks and telecoms. Meanwhile, private cloud remains mission-critical for defense, core banking, and public registries that require stringent in-country data residency. The widespread distribution of edge-ready micro-data centers also complements hybrid designs by locating latency-sensitive resources at 5G aggregation points.

By Service Model: Platforms speed AI-centric delivery

Infrastructure-as-a-Service retained 47.10% share, yet Platform-as-a-Service is scaling fastest at 31.50% CAGR, underscoring the jump from raw compute to turnkey AI development stacks. Enterprises select curated data pipelines, MLOps toolkits, and DevSecOps automation to cut application release cycles from months to days, magnifying demand for compliance-ready PaaS blueprints. The South Korea cloud computing market size for PaaS is set to capture incremental AI and LLM experimentation budgets, as exemplified by HyperCLOVA X roll-outs across public education clusters.

Function-as-a-Service, though nascent, appeals to cost-optimized, event-driven workloads such as content personalization and IoT telemetry. SaaS adoption remains steady among HR, CRM, and collaboration suites, especially within subsidized SME cohorts. Provider roadmaps increasingly bundle vertical-specific APIs to distinguish offerings beyond commodity IaaS capacity.

By Organisation Size: SME uptake narrows the digital divide

Large enterprises commanded 70.95% share in 2025; still, SMEs are set to post 27.20% CAGR as vouchers lower barriers, giving rise to templated migration playbooks and managed DevOps support. In value terms, the South Korea cloud computing market share of SMEs is poised to expand, partly driven by Fast Five’s Five Cloud, which exceeded KRW 10 billion in 2024 sales after onboarding 2,600 customers.

SMEs leverage cloud to digitize accounting, e-commerce fulfillment, and AI-assisted customer service without incurring CAPEX. Tier-two providers craft bundled packages—compute credits, cybersecurity insurance, and business-process templates—to compete with hyperscaler marketplaces. Large enterprises continue to allocate multi-year budgets to multi-cloud governance, FinOps tooling, and sovereign-data LLM projects that lock in significant IaaS and PaaS commitments.

By End-User Industry: Healthcare’s AI pivot unlocks new workloads

BFSI led revenue at 22.95% in 2025, while healthcare is projected to surge at 33.40% CAGR to 2031 within the South Korea cloud computing market. Hospitals harness natural-language clinical models, federated learning, and secure imaging repositories that demand high-performance GPUs and privacy-preserving architectures.

Manufacturing, retail, and government segments steadily migrate ERP, logistics optimization, and citizen-service portals to cloud solutions, driven by supply-chain resilience requirements and customer experience imperatives. Telecom operators exploit private 5G and edge services for ultra-low-latency offerings in media streaming and autonomous-drone management. The cross-sector shift from infrastructure modernization to data-driven value creation intensifies competition among platform vendors.

Geography Analysis

The Seoul Capital Area maintained 68.20% of the South Korea cloud computing market in 2025, catalyzed by dense data-center clusters, advanced 5G coverage, and public-sector digital-platform funding. Flagship facilities operated by Naver, KT, and hyperscalers create a critical mass of carrier-neutral interconnectivity that anchors multinational deployments. Seoul’s financial hub status accelerates AI labs and regulatory-tech sandboxes, reinforcing sophisticated hybrid-cloud patterns in banking and insurance.

The Gyeongsang Region, encompassing Ulsan, Daegu, and Gumi, is the fastest-growing zone at 32.10% CAGR. Samsung SDS’s 21.5 billion KRW AI data center in Gumi and the AWS-SK USD 5 billion campus in Ulsan illustrate the pivot toward coastal energy corridors and semiconductor supply-chain proximity. Renewables integration and LNG cold-energy cooling reduce OPEX and carbon intensity, attracting AI-heavy tenants. Prospective infrastructure around Busan’s 2029 Gadeokdo New Airport further elevates regional connectivity, supporting cross-border disaster-recovery nodes and gaming latency objectives.

Beyond the two spearheads, Jeollanam-do’s USD 35 billion “mega” site introduces 3 GW capacity by 2028, redefining national redundancy and distributing hyperscale spillover demand southward. Collaborative municipal projects in Busan and Incheon deploy lightweight AI models for civic efficiency, demonstrating regional public-sector cloud adoption. Universities in Daejeon and Gwangju pilot quantum-computing sandbox environments, reflecting the widening geographic diffusion of specialized cloud resources.

Coverage of the cloud computing market by Mordor Intelligence spans a wide geographic footprint, with regional analysis available for North America, Europe, and Asia, alongside detailed country-level intelligence for China, India, United States, France, Spain, and United Kingdom, each shaped by local operating conditions.

Competitive Landscape

The South Korea cloud computing market hosts a mixed oligopoly in which AWS, Microsoft Azure, and Google Cloud extend regional zones and talent academies, while Naver Cloud, Kakao Enterprise, and KT Cloud leverage in-country data centers and regulatory alignment to secure public contracts. AWS partners with SK Group to construct the Ulsan AI campus, showcasing co-investment models that marry foreign capital with domestic energy expertise.

Domestic incumbents capitalize on sovereign-AI positioning: Naver Cloud serves 60,000 clients and integrates HyperCLOVA X across public agencies, while Kakao Enterprise pilots federated learning in healthcare. IPO activity from Megazone Cloud and LG CNS signals market-maker confidence and funds inorganic expansion into managed services and quantum-computing verticals. Megazone Cloud’s Dell partnership injects high-density GPU nodes tailored to local AI start-ups, underscoring hardware-software co-design as a differentiator.

The managed-service provider segment, valued at KRW 12 trillion in 2024, is consolidating through M&A and strategic alliances, deepening service coverage in cloud security, FinOps, and compliance automation. Edge-computing ecosystems emerge around SK Telecom’s mobile-edge platform, enabling content-delivery partners to slash latency and fortify OTT streaming quality. Competitive narratives thus shift from commodity compute toward verticalized AI, edge integration, and sovereign-data assurances.

South Korea Cloud Computing Industry Leaders

Alibaba Group Holding Limited

Amazon Web Services (AWS)

Google LLC

IBM Corporation

Microsoft Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Megazone Cloud chosen for national quantum computing project, bringing IonQ “Tempo” to Korea and laying a hybrid quantum-classical groundwork.

- June 2025: AWS and SK Group unveil USD 5 billion Ulsan AI data center with 60,000 GPUs and 103 MW capacity.

- June 2025: Government launches USD 1.1 billion GPU program; Naver and Kakao vie for leadership.

- May 2025: Fast Five’s Five Cloud crosses KRW 10 billion revenue, serving 2,600 SMEs.

South Korea Cloud Computing Market Report Scope

Cloud computing provides on-demand access to computer resources, particularly data storage and processing power, without requiring direct management by the user. Computing resources, including physical and virtual servers, data storage, networking capabilities, application development tools, software, and AI-powered analytics, are now accessible over the Internet with a pay-per-use pricing model.

The report covers South Korean cloud computing companies and the market, which is segmented by type (public cloud (IaaS, Paas, and Saas), private cloud, hybrid cloud), organization type (SMEs, large enterprises), end-user industries (manufacturing, education, retail, transportation and logistics, healthcare, BFSI, telecom and IT, government and public sector, and other end-user industries (utilities, media & entertainment, etc.)). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Public Cloud |

| Private Cloud |

| Hybrid Cloud |

| Infrastructure-as-a-Service (IaaS) |

| Platform-as-a-Service (PaaS) |

| Software-as-a-Service (SaaS) |

| Function-as-a-Service (FaaS) |

| Large Enterprises |

| Small and Medium-sized Enterprises (SMEs) |

| BFSI |

| Manufacturing |

| Healthcare |

| Retail and E-commerce |

| Government and Public Sector |

| Telecom and IT |

| Transportation and Logistics |

| Others |

| By Deployment Model | Public Cloud |

| Private Cloud | |

| Hybrid Cloud | |

| By Service Model | Infrastructure-as-a-Service (IaaS) |

| Platform-as-a-Service (PaaS) | |

| Software-as-a-Service (SaaS) | |

| Function-as-a-Service (FaaS) | |

| By Organisation Size | Large Enterprises |

| Small and Medium-sized Enterprises (SMEs) | |

| By End-User Industry | BFSI |

| Manufacturing | |

| Healthcare | |

| Retail and E-commerce | |

| Government and Public Sector | |

| Telecom and IT | |

| Transportation and Logistics | |

| Others |

Key Questions Answered in the Report

What is the current size of the South Korea cloud computing market?

The market is valued at USD 12.46 billion in 2026 and is forecast to reach USD 38.28 billion by 2031 at a 25.18% CAGR.

Which deployment model is growing fastest in South Korea?

Hybrid cloud is expanding at 28.90% CAGR as enterprises balance data-sovereignty needs with scalable public-cloud resources.

Why is healthcare cloud adoption accelerating?

AI-powered diagnostics, federated learning platforms, and supportive regulations are driving a 33.40% CAGR in healthcare cloud spending through 2031.

How do government subsidies influence SME cloud uptake?

Programs covering up to 80% of adoption costs have reduced price sensitivity and enabled SMEs to embrace cloud services at a 27.20% CAGR.

Where are major new data centers being constructed?

Large-scale sites include AWS-SK’s USD 5 billion Ulsan facility and a USD 35 billion 3 GW complex in Jeollanam-do, diversifying capacity beyond Seoul.

What challenges could restrain market growth?

Strict data-residency mandates, increasing cyber-attacks, talent shortages, and cost pressures on local MSPs all exert downward pressure on CAGR forecasts.

Page last updated on: