Japan Cloud Computing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

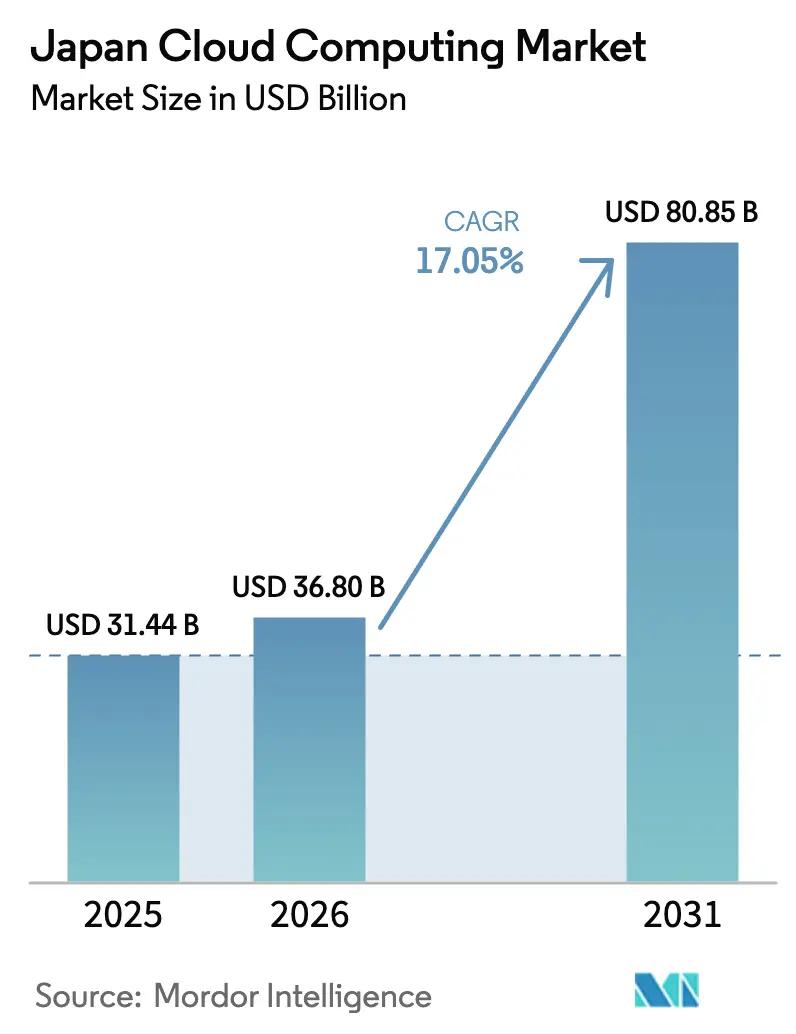

| Base Year Market Size (2025) | USD 31.44 Billion |

| Market Size (2026) | USD 36.8 Billion |

| Market Size (2031) | USD 80.85 Billion |

| Growth Rate (2026 - 2031) | 17.05% CAGR |

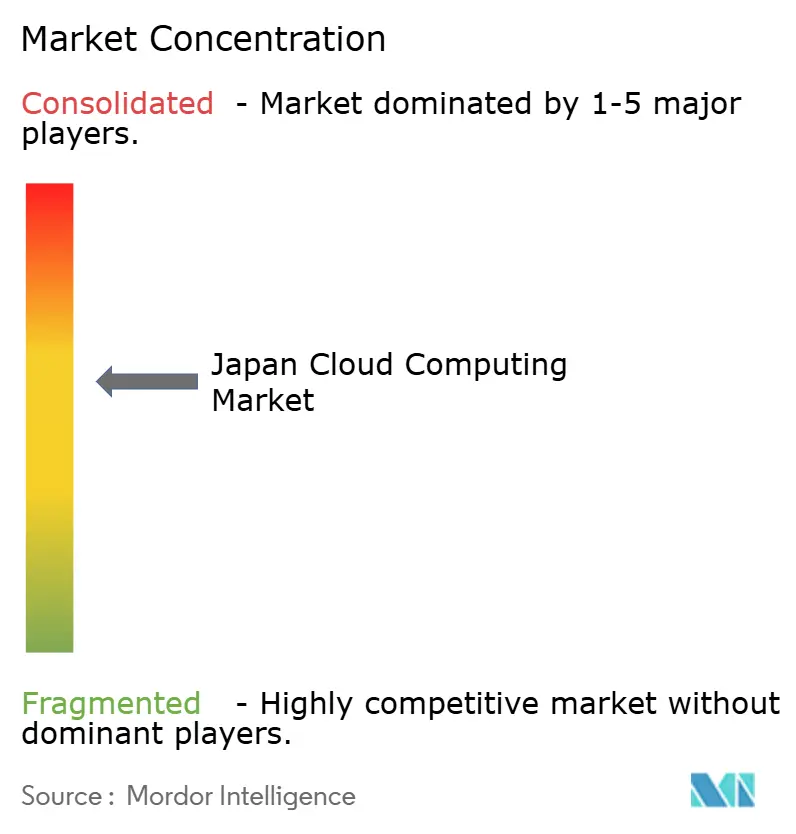

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Japan Cloud Computing Market Analysis by Mordor Intelligence

The Japan Cloud Computing market size is expected to grow from USD 31.44 billion in 2025 to USD 36.8 billion in 2026 and is forecast to reach USD 80.85 billion by 2031 at 17.05% CAGR over 2026-2031. Growth reflects three powerful forces: the sovereign-AI agenda, accelerated digital-transformation programs, and heavy foreign hyperscaler investment that is reshaping enterprise IT strategies. Central-government “Cloud-by-Default” rules compel agencies to adopt domestic platforms, while manufacturers, banks, and healthcare providers rely on cloud services to modernize legacy environments and deploy generative-AI workloads. Foreign providers have pledged more than USD 25 billion in new capacity, yet domestic firms capture sensitive workloads by pairing regulatory compliance with leading-edge GPU infrastructure. Labor shortages, tax incentives for green data-centres, and Tokyo-area power congestion all reinforce the migration away from on-premises servers toward elastic cloud resources. Taken together, these factors position the Japan cloud computing market for robust multi-year expansion.[1]Digital Agency, “Global Site|Digital Agency,” digital.go.jp

Key Report Takeaways

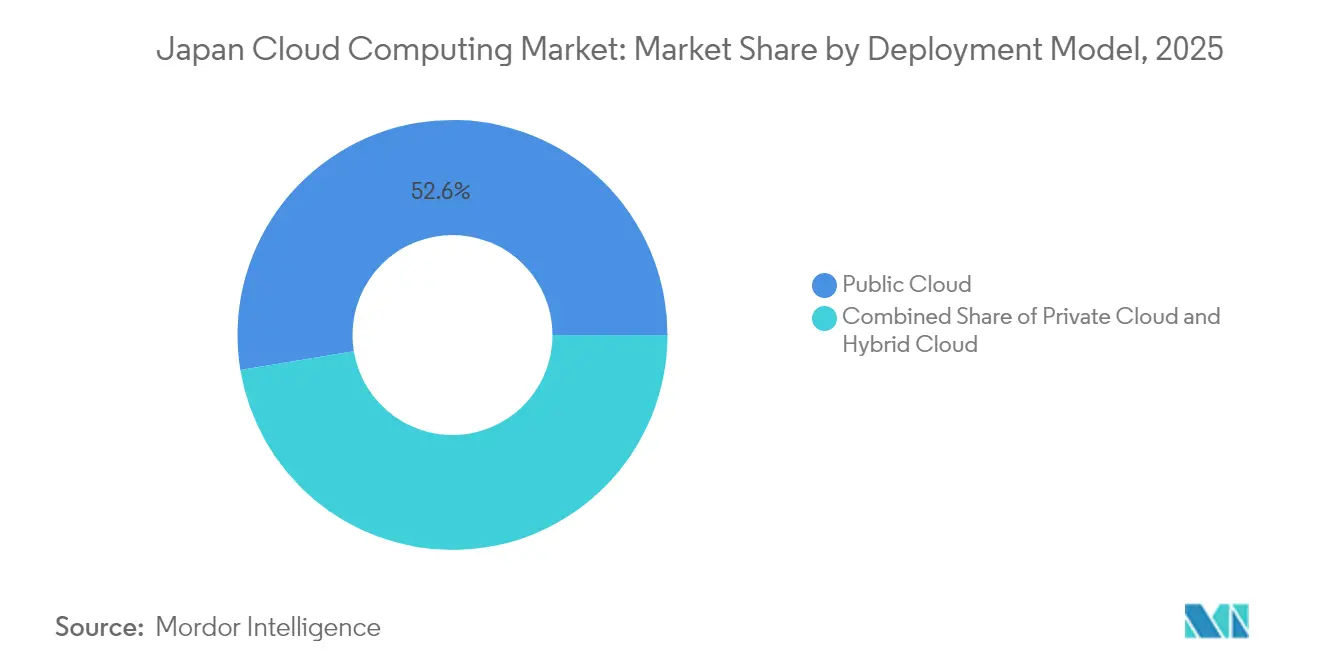

- By deployment model, the public-cloud segment led with 52.60% of Japan cloud computing market share in 2025, whereas hybrid-cloud services are projected to expand at a 18.45% CAGR through 2031.

- By service model, Software-as-a-Service accounted for 46.10% of the Japan cloud computing market size in 2025, while Platform-as-a-Service is forecast to grow at 21.10% CAGR over 2026-2031.

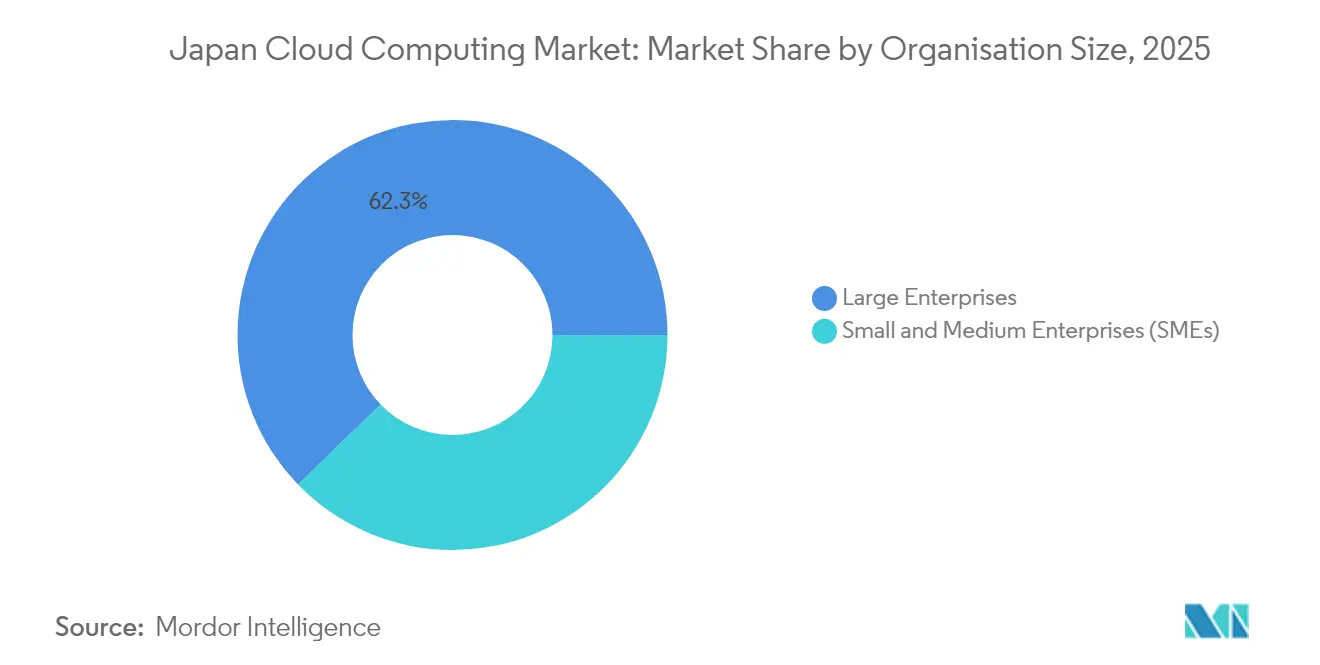

- By organisation size, large enterprises held 62.25% revenue share in 2025; the SME segment is advancing at a 19.05% CAGR to 2031.

- By end-user industry, manufacturing commanded 21.05% of Japan cloud computing market share in 2025, while healthcare is the fastest-growing segment at 18.65% CAGR to 2031.

- By workload type, ERP & core business applications retained 29.30% share of the Japan cloud computing market size in 2025 and AI/ML workloads are progressing at a 22.60% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Japan holds a defined position within a broader international distribution. The cloud computing market share data by Mordor Intelligence maps that allocation across all contributing countries and regions, globally.

Japan Cloud Computing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Generative-AI workload surge driving demand for sovereign compute | +4.2% | Nationwide, concentrated along the Tokyo–Osaka corridor | Medium term (2-4 years) |

| Government “Cloud-by-Default” policy and Digital Agency Government Cloud rollout | +3.8% | Nationwide, with early adoption in central government | Short term (≤2 years) |

| Robust digital-transformation programs in manufacturing and BFSI | +3.5% | Nationwide, strongest in major industrial regions | Medium term (2-4 years) |

| Vendor-financed mainframe-to-cloud migration schemes | +2.4% | Nationwide, particularly in finance and other large-enterprise segments | Medium term (2-4 years) |

| Tax incentives encouraging regional green data-centres powered by renewables | +2.1% | Regional, focused on Hokkaido, Kyushu and other rural prefectures | Long term (≥4 years) |

| Acute GPU/ASIC shortages pushing enterprises toward pay-as-you-go IaaS models | +1.3% | Global trend, acutely felt in Japan’s AI development hubs | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Generative-AI workload boom demanding sovereign compute

Japan’s appetite for high-performance compute has exploded since the government earmarked JPY 72.5 billion (USD 483 million) for five domestic providers tasked with building sovereign-AI infrastructure.[2]Ministry of Economy, Trade and Industry, “Approval of Plans for Ensuring a Stable Supply of Cloud Programs under the Economic Security Promotion Act,” meti.go.jp This funding mitigates the global GPU shortage and reduces reliance on foreign clouds, a dependency that produced a digital-trade deficit of JPY 5.5 trillion in 2023. SoftBank’s plan to deploy the world’s first DGX SuperPOD in Tokyo with a JPY 150 billion investment by 2025 illustrates private-sector alignment with sovereign goals. Start-ups receive subsidised access through the Generative-AI Accelerator Challenge, which feeds demand for domestic IaaS and creates a feedback loop: more compute capacity enables advanced local models, which in turn justify further capacity additions. International players such as OpenAI now maintain Tokyo offices, heightening competitive urgency for local alternatives that guarantee data residency compliance.

Government “Cloud-by-Default” and Digital Agency Gov-Cloud rollout

The Digital Agency’s Cloud First Principle mandates that all new government systems adopt cloud services unless a stronger rationale exists for other models. Under the agency’s certification scheme, Sakura Internet became the first domestic provider to pass the rigorous ISMAP security assessment, setting a procurement precedent that favours in-country operators. Pilot projects running generative-AI chatbots for document drafting and citizen-service inquiries proved viable during December 2023 March 2024 field tests, leading ministries to budget additional cloud spending in fiscal 2025Municipalities also migrate legacy registries to the Government Cloud framework, reducing fragmented IT contracts and freeing funds for broader digital-transformation efforts.

Tax incentives for regional green data-centres using renewables

Extended through 2028, Japan’s Carbon Neutrality and Digital Transformation tax regime grants up to JPY 5 billion per project for data-centres powered by renewables.[3]PwC Japan Group, “Overview of 2025 Tax Reform Proposals,” pwc.com Regional authorities layer extra benefits such as five-year corporate-tax holidays, producing effective tax rates below 10% in several prefectures. Hokkaido leverages cooler temperatures and abundant wind energy to attract hyperscale builds, while Kyushu draws on geothermal resources. The Ministry of Economy, Trade and Industry couples these incentives with GX-aligned investment strategies that reward providers for integrating green power into facility design. Shifting workloads away from the congested Tokyo grid both lowers energy cost and diversifies disaster-recovery footprints.

Robust DX programs in manufacturing and BFSI

Industrial and financial incumbents accelerate cloud migration to avert the “2025 cliff,” when technical-debt costs could reach JPY 12 trillion annually. Toyota’s AI-platform initiative lets plant staff generate machine-learning models autonomously, cutting model-creation hours by 20% and expanding annual model output from 8,000 to 10,000.[4]Google Cloud, “How Toyota is revolutionizing manufacturing with AI,” cloud.google.com Mizuho has earmarked JPY 100 billion for a multi-cloud marketing engine that customises offers at individual level. Japan’s Information-technology Promotion Agency reports rising software investment as firms digitalise production lines and customer channels to offset labour shortages. These projects frequently mix public, private, and on-premises environments, increasing demand for hybrid management platforms.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Strict cross-border data-residency and privacy rules | -2.8% | Nationwide, strictest in government and financial sectors | Long term (≥4 years) |

| Cloud-native talent scarcity and wage inflation | -1.9% | Nationwide, most acute in the Tokyo metropolitan area | Medium term (2-4 years) |

| Tokyo power-grid congestion delaying hyperscale data-centre permits | -1.2% | Tokyo metropolitan area, with spill-over into neighbouring prefectures | Short term (≤2 years) |

| Keiretsu-based vendor lock-in slowing multicloud adoption | -0.8% | Nationwide, especially among large traditional enterprises | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Strict cross-border data-residency and privacy rules

Amendments to the Act on the Protection of Personal Information broaden restrictions on offshore processing, while the Economic Security Promotion Act classifies cloud systems as critical infrastructure that must undergo domestic supply-chain verification. Although Japan recently endorsed the Data Free Flow with Trust framework to ease certain transfers, regulators still apply a cautious stance toward sensitive datasets, compelling enterprises to retain core information inside national borders. Financial institutions respond by segmenting platforms: regulated workloads remain in domestic availability zones, while less-sensitive services run overseas. Compliance complexity increases provider switching costs and raises barriers for smaller foreign entrants.

Cloud-native talent scarcity and wage inflation

Japan may be short 220,000–450,000 IT professionals by 2030, with cloud-engineering roles commanding salaries upwards of JPY 15 million (USD 100,000). SMEs struggle most, prompting many to adopt managed services or low-code tools. In response, the government’s five-year JPY 400 billion reskilling fund trains workers in advanced cloud disciplines, and vendors expand certification programmes to widen the talent pipeline. Automation helps: AI-assisted development environments and policy-driven orchestration platforms reduce manual tasks, allowing scarce engineers to manage larger estates. Still, wage pressure adds recurring cost and can delay complex migrations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Model: Hybrid Architectures Address Sovereignty Concerns

Hybrid architectures record a 18.45% CAGR to 2031 as Japanese enterprises blend global reach with in-country data control. Public-cloud options captured 52.60% of Japan cloud computing market share in 2025, yet sensitive workloads remain on private clouds or domestic infrastructure. Government projects typically position regulated data within sovereign regions while shifting public-facing portals to hyperscale nodes. Migration roadmaps frequently phase legacy mainframes into containerized microservices that connect to public APIs. This staged approach minimizes downtime and aligns with risk-mitigation guidelines issued by the Financial Services Agency.

Hybrid frameworks also solve latency and energy-availability constraints. Firms deploy on-premises edge nodes for deterministic manufacturing processes while bursting AI training tasks into GPU clusters housed in Tokyo or Osaka mega-facilities. The Digital Agency’s Gov-Cloud design codifies this model, combining local IaaS with community clouds accessible by prefectural agencies. Consequently, the Japan cloud computing market benefits from diversified spend across both foreign and domestic providers, amplifying total capacity without breaching residency mandates.

By Service Model: Platform Services Enable Rapid AI Development

Software-as-a-Service led with 46.10% of the Japan cloud computing market size in 2025 because pre-configured applications accelerate time-to-value. Enterprises tap SaaS for ERP modernisation, unified communications, and cybersecurity posture management. However, Platform-as-a-Service registers the fastest 21.10% CAGR through 2031, driven by the need to build and iterate AI solutions rapidly. PaaS offerings bundle data pipelines, model-training environments, and DevSecOps toolchains, freeing developers from infrastructure administration.

Infrastructure-as-a-Service remains foundational, but price competition compresses margins. Providers differentiate by pairing bare-metal GPU instances with managed Kubernetes and serverless functions. The joint proposal by NTT, KDDI, Fujitsu, NEC, and Rakuten to deliver Beyond-5G PaaS underscores this shift toward integrated stacks tuned for subsector use cases. As native-language large-language-models proliferate, demand for specialised PaaS accelerates, sustaining high utilisation of sovereign compute clusters and reinforcing the broader Japan cloud computing market.

By Organisation Size: SMEs Accelerate Cloud Adoption Through Necessity

Large enterprises controlled 62.25% of revenue in 2025, benefitting from early migration waves and multilayer vendor contracts. Yet SMEs outpace them with a 19.05% CAGR because cloud consumption allows enterprise-grade capability without capex. Subscription billing and automatic scaling align with SME cash-flow patterns, and government subsidy schemes reduce onboarding fees for small firms engaging in digital-transformation projects. Managed application platforms abstract away skills gaps, so SMEs can deploy e-commerce storefronts, AI chatbots, or robotic-process-automation routines in days rather than months.

Talent scarcity still weighs on SME project timelines. Many partner with local system integrators that offer turnkey migrations, including security hardening that satisfies data-residency rules. The Japan cloud computing market gains breadth as these smaller firms enlarge the addressable user base; their aggregate demand smooths cyclical spending by large enterprises.

By End-user Industry: Healthcare Transformation Drives Rapid Growth

Manufacturing retained 21.05% of Japan cloud computing market share in 2025 owing to Industry 4.0 initiatives, but healthcare jumps ahead with a 18.65% CAGR to 2031. Hospitals deploy cloud-hosted imaging platforms that use generative-AI to detect anomalies, cutting radiologist workload and improving diagnostic accuracy. Telemedicine portals surged during pandemic years and continue to attract investment because an ageing population forces remote care expansion. Electronic health record upgrades rely on secure cloud environments certified under the ISMAP framework, further enlarging healthcare demand.

Meanwhile, banks modernise core systems to deliver personalised products built on real-time data analytics, and insurers trial GPT-based claims adjudication models hosted on sovereign PaaS. Retailers harness inventory-optimisation algorithms and augmented-reality shopping experiences, enhancing omnichannel engagement. Each sector’s use case propagates industry-specific cloud templates, stimulating vertical-solution ecosystems inside the broader Japan cloud computing market.

By Workload Type: AI/ML Workloads Transform Computing Demands

ERP and other core business suites still represent 29.30% of the Japan cloud computing market size in 2025, but AI/ML and high-performance-compute workloads exhibit a blistering 22.60% CAGR. Providers scramble for NVIDIA H100 and B200 GPUs; Sakura Internet now operates 2.0 EFLOPS of capacity, a figure unthinkable two years ago. Enterprises train proprietary language models to summarise legal documents, forecast supply-chain risk, and generate design prototypes.

Edge workloads also rise as 5G deployment reaches nationwide coverage, letting industrial sensors stream data into predictive-maintenance services in near real time. Real-time data analytics frameworks ingest telemetry, apply anomaly-detection models, and trigger automation back to factory lines. This compute-heavy choreography cements the role of AI-optimised IaaS plus PaaS, underpinning sustained expansion in the Japan cloud computing market.

Geography Analysis

Tokyo and Osaka remain the epicentre of cloud-infrastructure spending, hosting the majority of availability zones, interconnection hubs, and managed-service headquarters. Oracle’s USD 8 billion pledge and Microsoft’s USD 2.9 billion AI-capacity expansion confirm that foreign hyperscalers still view these metros as anchor regions for the Japan cloud computing market. Yet power-grid saturation and soaring land prices trigger a pronounced shift toward secondary cities. Kansai Electric has upgraded four Osaka-area substations for data-centre loads, while TEPCO invests in micro-grid technologies that stabilise renewable input during peak AI-training cycles.

In Hokkaido, cooler climates cut cooling-system energy draw by up to 30%, and local governments offer combined tax incentives worth JPY 5 billion per siteCompanies locate backup nodes near Sapporo to meet disaster-recovery objectives and qualify for green-energy rebates that align with corporate ESG targets. Kyushu leverages geothermal and solar resources to lure AI cloud clusters, with Fukuoka positioning itself as a start-up gateway. Edge-compute demand for connected vehicles and smart-factory deployments fuels mini-data-centre rollouts across industrial corridors in Aichi and Shizuoka.

Disaster-resilience planning also diversifies footprints. Enterprises favour at least one availability zone outside the Pacific earthquake belt, often in inland or northern prefectures that present lower seismic risk. The Regional Investment Promotion Tax Measure, renewed in the 2025 budget, further sweetens rural economics by allowing accelerated depreciation on qualifying cloud infrastructure. Together, these forces distribute capacity more evenly, extending the reach of the Japan cloud computing market to communities previously overlooked by hyperscalers.

Mordor Intelligence delivers a comprehensive view of the cloud computing market across all major regions such as Europe, Asia, and South America, alongside country-level analysis for India, South Korea, Germany, Brazil, United Arab Emirates, and Israel, each offering a view of the local market realities.

Competitive Landscape

Market structure balances global scale and local advantage. AWS, Microsoft Azure, and Google Cloud together control a majority of general-purpose workloads, offering unmatched service breadth and R&D budgets. Still, sovereignty mandates and ISMAP procedures carve room for domestic providers such as Sakura Internet, NTT Communications, and Fujitsu Cloud Service for OSS. These firms win sensitive contracts by combining in-country data custody with comparable service-level agreements. As of 2025, the top five vendors account for roughly 58% of total spend, indicating moderate concentration.

AI infrastructure emerges as the new battleground. Sakura Internet’s 2,000-GPU cluster, SoftBank’s DGX SuperPOD, and KDDI’s forthcoming Osaka facility with NVIDIA Blackwell processors exemplify capital-intensive strategies aimed at AI model training workloads. Partnerships flourish: Equinix co-locates Sakura’s GPU cloud inside its metro campuses, while Fujitsu and AWS cooperate on legacy-modernisation projects targeting 800 customer. Foreign firms respond by expanding Tokyo-region capacity and forming compliance alliances with local telecoms to satisfy residency checks.

Sustainability differentiators gain weight as power tariffs rise. Operators advertise 100% renewable-energy contracts and liquid-cooling systems that cut PUE values. NEC pilots hydrogen-fuel-cell backup units in its Kyushu edge sites. Meanwhile, system integrators like TIS and Kyndryl specialise in accelerated mainframe-to-cloud migrations, offering packaged toolchains that shorten project timelines by one-third. Competitive intensity therefore centres on specialised AI silicon availability, compliance tooling, and energy-efficient design all essential to capturing share in the Japan cloud computing market.

Japan Cloud Computing Industry Leaders

Microsoft Corporation

Amazon Web Services, Inc

Google LLC

Oracle Corporation

IBM Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: KDDI and HPE announced collaboration to launch an AI data-centre in Osaka by fiscal year-end, utilising NVIDIA Blackwell chips and hybrid cooling systems to minimise environmental impact while providing cloud-based GPU services through KDDI’s WAKONX platform.

- June 2025: Canon IT Solutions launched PREMIDIX migration service offering comprehensive support from assessment to maintenance for legacy-system migration to cloud environments, targeting quadruple business scale growth by 2028 through AI-enhanced migration tools.

- June 2025: Tokyo System House became a Silver sponsor of Google Cloud Next Tokyo, presenting COBOL-modernisation solutions and “AI Veteran Engineer” for automated legacy-system documentation and migration support.

- May 2025: TIS completed Japan Airlines’ mileage-system modernisation from IBM mainframe to AWS cloud within eight months using Xenlon modernisation service, achieving zero operational issues post-migration.

Japan Cloud Computing Market Report Scope

Cloud computing delivers computing services via the internet, encompassing servers, storage, databases, networking, software, analytics, and intelligence. This approach fosters quicker innovation, adaptable resources, and economies of scale. Typically, customers pay solely for the cloud services they utilize, leading to reduced operational costs, more efficient infrastructure management, and the ability to scale in line with evolving business needs.

Japan cloud computing market report is segmented by type (public cloud [ IaaS, Paas, Saas], private cloud, hybrid cloud), by organization size (SMEs, large enterprises), and by end-user industries (manufacturing, education, retail, transportation, and logistics, healthcare, BFSI, telecom and IT, government and public sector, and others including utilities, media & entertainment, etc.). The market sizes and forecasts are provided in terms of value (USD) for all segments.

| Public Cloud |

| Private Cloud |

| Hybrid Cloud |

| Infrastructure-as-a-Service (IaaS) |

| Platform-as-a-Service (PaaS) |

| Software-as-a-Service (SaaS) |

| Large Enterprises |

| Small and Medium Enterprises (SMEs) |

| BFSI |

| Manufacturing |

| Healthcare |

| Retail and E-Commerce |

| Telecom and IT |

| Government and Public Sector |

| Others |

| AI / ML and HPC |

| ERP and Core Business Apps |

| Web Hosting and CDN |

| Dev/Test and CI-CD |

| Data Analytics and Big Data |

| IoT and Edge Workloads |

| By Deployment Model | Public Cloud |

| Private Cloud | |

| Hybrid Cloud | |

| By Service Model | Infrastructure-as-a-Service (IaaS) |

| Platform-as-a-Service (PaaS) | |

| Software-as-a-Service (SaaS) | |

| By Organisation Size | Large Enterprises |

| Small and Medium Enterprises (SMEs) | |

| By End-user Industry | BFSI |

| Manufacturing | |

| Healthcare | |

| Retail and E-Commerce | |

| Telecom and IT | |

| Government and Public Sector | |

| Others | |

| By Workload Type | AI / ML and HPC |

| ERP and Core Business Apps | |

| Web Hosting and CDN | |

| Dev/Test and CI-CD | |

| Data Analytics and Big Data | |

| IoT and Edge Workloads |

Key Questions Answered in the Report

What is the current value of the Japan cloud computing market?

The market is valued at USD 36.8 billion in 2026 and is projected to reach USD 80.85 billion by 2031.

Which deployment model is growing fastest in Japan?

Hybrid cloud services are expanding at a 18.45% CAGR as firms combine domestic data residency with global scalability.

Why is healthcare the fastest-growing end-user segment?

Hospitals and insurers adopt cloud-based AI diagnostics and telemedicine platforms to manage ageing-population pressures, lifting healthcare’s CAGR to 18.65%.

How are tax incentives influencing data-centre locations?

National and prefectural tax measures cut effective rates below 10% for renewable-powered facilities, encouraging builds in Hokkaido, Kyushu, and other rural areas.

What challenges threaten cloud growth in Japan?

Strict data-residency laws and a projected shortfall of up to 450,000 cloud-skilled workers raise compliance costs and wage inflation.

Which workload category is expanding quickest?

AI/ML and high-performance-compute workloads lead with a 22.60% CAGR, driving demand for GPU-rich IaaS and specialised PaaS platforms.

Page last updated on: